BrightHouse Bundle

What Defined BrightHouse's Customer Base?

Understanding the BrightHouse SWOT Analysis reveals the crucial role of customer demographics and target market in shaping a business's destiny. For BrightHouse, a rent-to-own giant, identifying its ideal customer was not just a strategic imperative but a matter of survival. This deep dive explores the customer demographics and target market of the BrightHouse company, uncovering the factors that led to its rise and fall.

Delving into the consumer profile of BrightHouse's clientele, we'll uncover the BrightHouse customer age range, BrightHouse customer income levels, and BrightHouse customer location data. This analysis will shed light on what are the typical BrightHouse customer needs, their BrightHouse customer buying behavior analysis, and how the company's market segmentation strategies evolved. Ultimately, we aim to understand who is the target audience for BrightHouse and the implications of their BrightHouse customer financial situation.

Who Are BrightHouse’s Main Customers?

The primary customer segments for the company were primarily consumers (B2C) who faced limitations in accessing traditional credit. This target market, a core strength of the company, provided immediate access to essential household goods through manageable installments. Understanding the customer demographics and target market is crucial for analyzing the company's business model and its eventual challenges.

A significant portion of the company's customer base was characterized by low incomes. This financial vulnerability was a key aspect of their consumer profile. The company's business model catered to around 200,000 customers with active agreements in 2018, highlighting the scale of its operations within this specific market segment.

The company attempted to shift its target segments over time. In February 2020, the company indicated a desire to move away from rent-to-own agreements and instead focus on cash loans. This shift was likely prompted by increasing regulatory pressure and a surge in compensation claims related to unaffordable lending practices.

Over two-thirds (67%) of customers who stated their household income reported it to be under £18,000. More than half (59%) had no savings, and only 9% had savings of £500 or more. These figures underscore the financial constraints faced by the company's target market.

Accepted customers were more likely to be female, with a broad spread across age groups. Approximately half of the customers had children, and only about one-third were in employment. The typical rent-to-own customer profile was often a young female lone parent.

The ideal customer often lived in rented accommodation and was almost exclusively from low-income households, wholly or partly reliant on welfare benefits. This focus on a specific demographic shaped the company's business practices and market segmentation.

The company operated across various locations, primarily targeting areas with a high concentration of its target demographic. Data on customer location is crucial for understanding the company's reach and market penetration.

Key Takeaways

The company's target market was primarily low-income consumers with limited access to credit. Understanding the customer demographics is essential for analyzing the company's business model and its challenges. The shift towards cash loans reflected regulatory pressures and compensation claims.

- Low-income households were the primary customer base.

- The company's customer base was predominantly female.

- The company aimed to move away from rent-to-own agreements.

- The customer profile was often a young, lone parent.

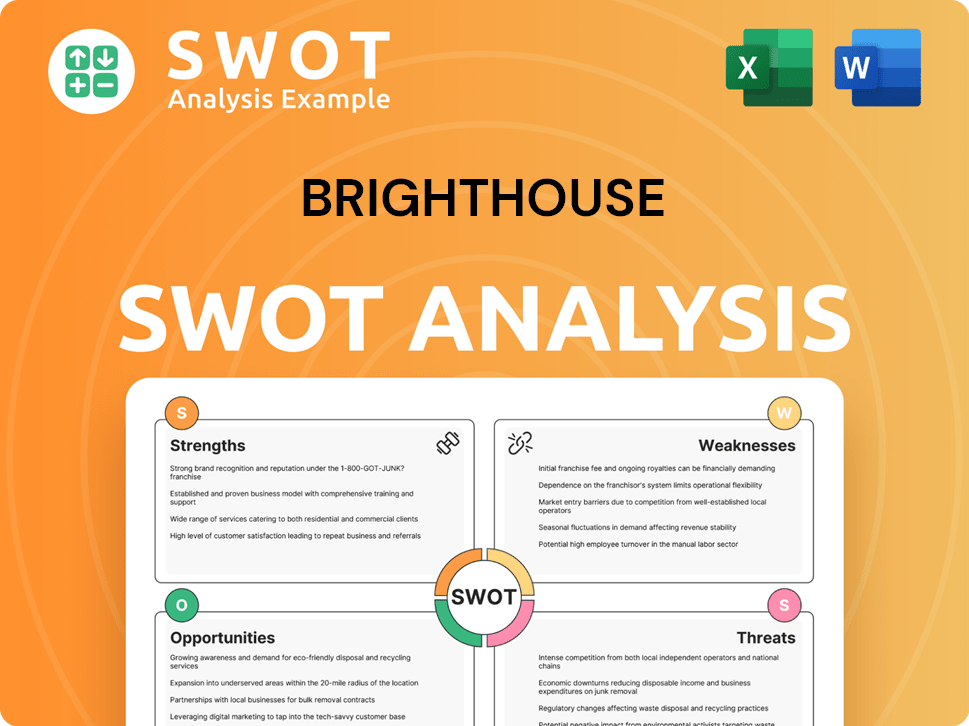

BrightHouse SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do BrightHouse’s Customers Want?

Understanding the customer needs and preferences is crucial for analyzing the BrightHouse company. The BrightHouse company primarily catered to individuals who needed essential household items but lacked the immediate financial means to purchase them. This hire purchase model offered a solution by allowing customers to acquire goods through manageable weekly payments.

The target market for the BrightHouse company was driven by the need for furniture, appliances, and electronics. The ability to spread payments over time was a key driver, making these items accessible to those with limited access to traditional credit. This approach addressed a significant pain point for many potential customers.

For nearly half of the accepted customers, the need for a new product arose from a broken previous one, highlighting the urgency for replacements. This indicates a demand for immediate solutions to household needs, which the company aimed to fulfill.

Customer Purchasing Behaviors and Financial Implications

Customers of the BrightHouse company often relied on installment plans, which resulted in paying significantly more than the retail price of the goods. This was due to high interest rates and additional charges. For example, a washing machine costing £358 could end up costing £1,092 due to interest and fees.

- The high interest rates, ranging from 69.9% to 99.9% APR, significantly increased the overall cost.

- Additional charges included delivery, installation, and compulsory warranties, further inflating the total expense.

- Despite the high costs, the ability to obtain immediate possession of goods through weekly payments was a key factor in customer loyalty.

- The company's lending practices faced criticism for targeting vulnerable individuals, leading to regulatory scrutiny.

The BrightHouse company's practices underwent scrutiny, particularly regarding its lending to vulnerable individuals. The Financial Conduct Authority (FCA) intervened in 2017, ordering the company to pay £14.8 million in redress to 249,000 customers due to unaffordable lending agreements. This led to store closures and a reform plan, indicating a shift in response to external pressures. To learn more about the company's background, you can read a Brief History of BrightHouse.

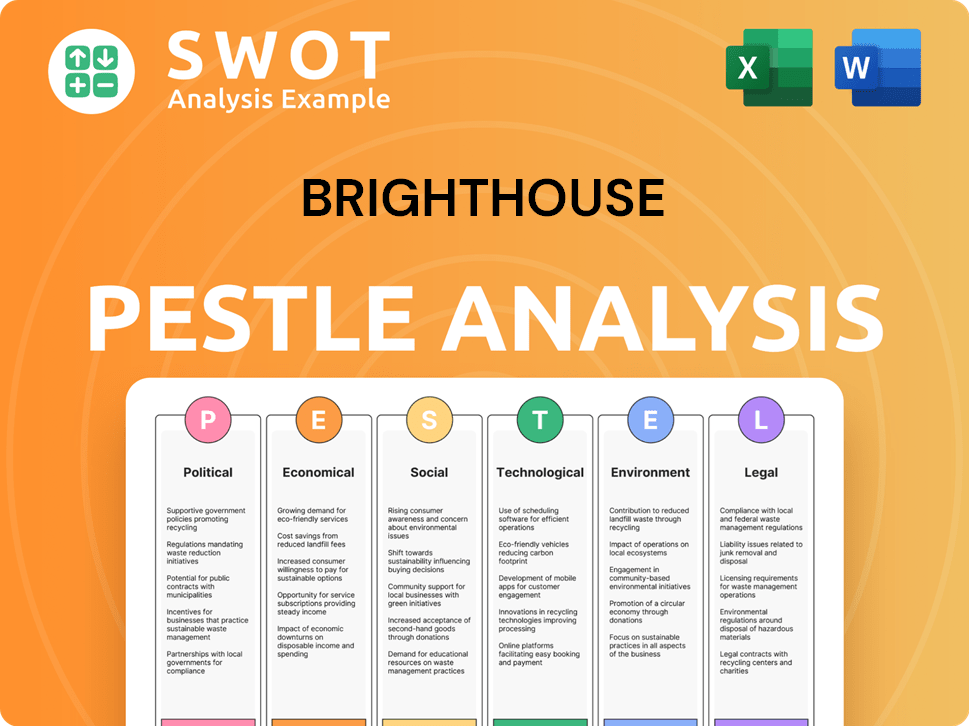

BrightHouse PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does BrightHouse operate?

The geographical market presence of the former rent-to-own company, which was once the largest in the UK, was primarily centered within the United Kingdom. The company's strategy heavily relied on physical stores to directly engage with its customer base. At its peak, the company had an extensive network of over 240 stores across the UK in 2019, a significant footprint that facilitated its operations.

The company strategically positioned its stores in areas with a high concentration of its target customers, often in economically disadvantaged neighborhoods. This approach was designed to serve specific demographics who might have limited access to mainstream financial services. This localized focus suggests an understanding of regional economic disparities and the prevalence of its target market within those areas, which helped to define its Growth Strategy of BrightHouse.

Towards the end of its operations, the company announced plans to close stores, reflecting a response to changing market dynamics and regulatory pressures. The company's collapse into administration on March 30, 2020, effectively ended its geographic market presence.

Store Locations

The company's physical stores were a crucial part of its business model, providing direct customer touchpoints and sales centers. These stores were strategically located in areas with a high density of its target market. This approach allowed the company to cater to the specific needs of its customer base.

Target Market Focus

The company's target market consisted of individuals who lacked access to mainstream financial services. The company's store locations were chosen to align with the demographics of its ideal customer, often in economically disadvantaged areas. This focus helped the company to understand and serve the needs of its target customer.

Market Dynamics

The company's eventual store closures and collapse into administration were influenced by changing market conditions and regulatory pressures. Increased competition and scrutiny of its lending practices played a significant role. These factors ultimately led to the end of its geographical market presence.

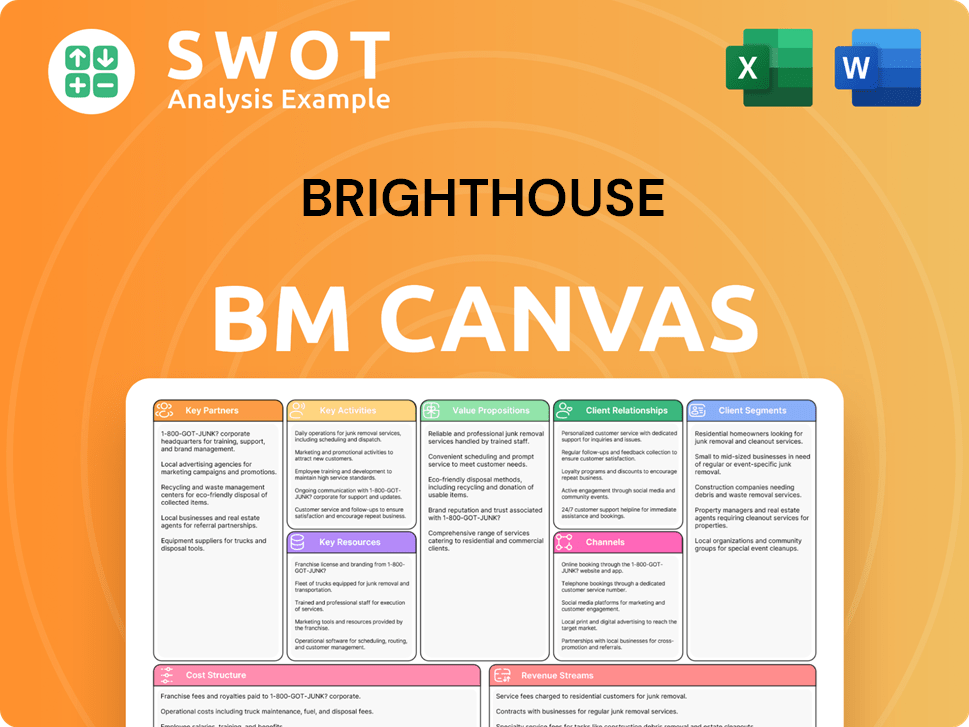

BrightHouse Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does BrightHouse Win & Keep Customers?

The customer acquisition and retention strategies of the company heavily influenced its operational success. The company, which primarily offered rent-to-own goods, utilized a specific approach to attract and retain customers. Understanding these strategies provides insight into the company's business model and its eventual challenges.

The company's primary method for acquiring customers involved leveraging its physical store presence. By 2019, the company operated over 240 stores across the UK. These stores served as direct sales centers, facilitating product showcases and in-store agreements. The company's marketing focused on accessibility, promoting essential home goods through manageable weekly payments. This strategy aimed to attract lower-income households and those with less-than-perfect credit, creating a specific target market.

Customer retention was largely dependent on ongoing hire purchase agreements. In 2018, approximately 200,000 customers had active agreements. The nature of the business model itself fostered retention through long-term payment plans. However, the company's practices led to significant issues, ultimately impacting customer loyalty.

The company's extensive network of physical stores was a cornerstone of its customer acquisition strategy. These stores served as direct sales centers, allowing for product showcasing and in-store agreements.

Marketing campaigns emphasized accessibility, promoting essential home goods through manageable weekly payments and 'no deposit' offers. This approach targeted lower-income households and those with imperfect credit histories.

Customer retention was heavily reliant on the ongoing hire purchase agreements. The business model itself fostered a form of retention through the long-term payment plans for goods.

The company's lending practices often led to financial difficulties for customers, with roughly half experiencing late payments and over 10% having their goods repossessed.

The Financial Conduct Authority (FCA) found the company had not acted as a 'responsible lender.' The company was found to have treated customers unfairly by signing them up to 'unaffordable' lending agreements. This led to a redress payment of £14.8 million to 249,000 customers in 2017. These issues, combined with high interest rates and compulsory add-ons, contributed to high customer churn rates and ultimately, the company's downfall. Understanding the Competitors Landscape of BrightHouse provides additional context.

Customer Demographics

The company's customer base primarily consisted of lower-income households and individuals with less-than-perfect credit. This is a crucial aspect of understanding the customer profile.

Target Market

The target market was defined by the need for essential home goods and the ability to afford manageable weekly payments, even with limited upfront capital. This is a key element of market segmentation.

Customer Acquisition

The company used physical stores and accessible payment plans to acquire customers. This strategy aimed to attract customers who needed immediate access to goods.

Retention Challenges

High interest rates, compulsory warranties, and affordability issues led to customer financial difficulties and high churn rates. This impacted customer loyalty.

FCA Involvement

The FCA found the company to be an irresponsible lender, leading to significant redress payments and ultimately, contributing to the company's collapse. This highlighted the importance of ethical lending practices.

Impact of Lending Practices

The company's lending practices, including high interest rates and add-ons, significantly increased the overall cost of goods. This affected the ideal customer.

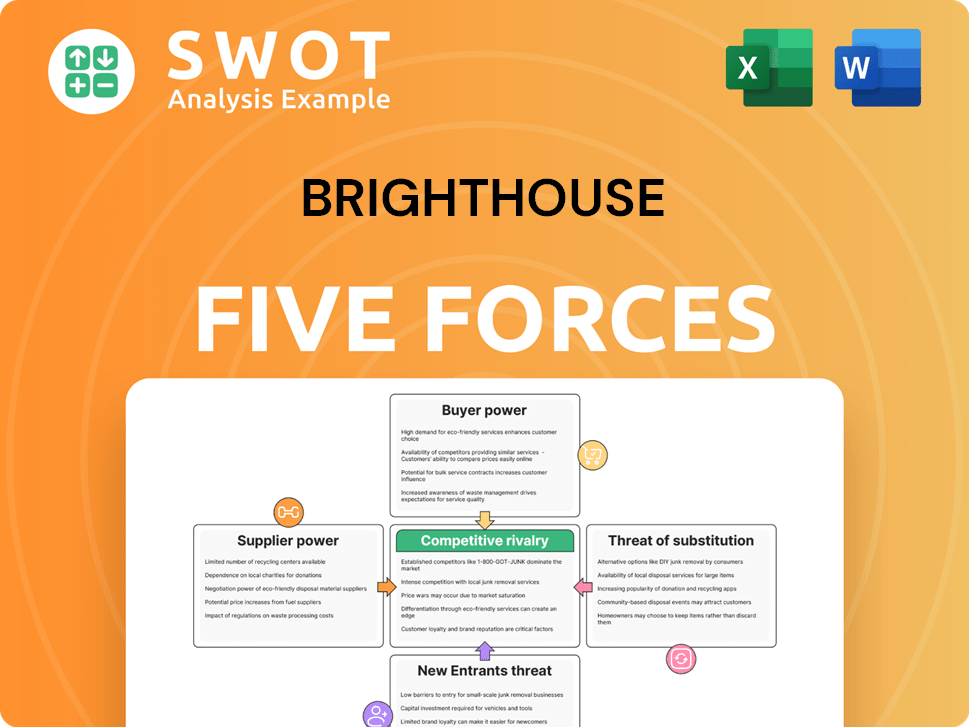

BrightHouse Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of BrightHouse Company?

- What is Competitive Landscape of BrightHouse Company?

- What is Growth Strategy and Future Prospects of BrightHouse Company?

- How Does BrightHouse Company Work?

- What is Sales and Marketing Strategy of BrightHouse Company?

- What is Brief History of BrightHouse Company?

- Who Owns BrightHouse Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.