BrightHouse Bundle

How Did BrightHouse Company Operate?

BrightHouse, once a dominant force in the UK's rent-to-own landscape, offered a unique, albeit contentious, service. The company provided household goods through hire purchase agreements, catering to a segment of the population often excluded from traditional credit options. Understanding BrightHouse SWOT Analysis is crucial to understanding the company's operations. The company's eventual collapse offers a valuable case study into the risks of high-cost credit.

This article will dissect the operational mechanics of BrightHouse, exploring its value proposition, revenue streams, and strategic decisions. We'll examine the challenges that led to its downfall, providing insights into the consumer credit market. This analysis will cover aspects like BrightHouse appliance rental, payment plans, and the impact of consumer credit regulations.

What Are the Key Operations Driving BrightHouse’s Success?

The core operation of the BrightHouse company revolved around a rent-to-own model, offering household goods to customers through hire purchase agreements. This allowed individuals to acquire essential items like appliances and furniture by making regular weekly payments. Ownership of the goods transferred to the customer once all payments were completed.

The primary target market for BrightHouse was individuals with low incomes who might struggle to obtain credit from traditional lenders. The company provided an alternative way to access goods without requiring a large upfront payment. This model aimed to make essential items more accessible to a specific demographic.

The operational process involved sourcing products, offering them through its network of physical stores, and managing the collection of weekly payments. BrightHouse also provided services such as warranties and insurance, which customers were often required to take, increasing the overall cost of the goods. Towards the end, the company expanded its offerings to include cash loans.

BrightHouse operated primarily through a rent-to-own model, allowing customers to acquire goods via hire purchase agreements. Customers made weekly payments until they owned the item. The company managed a network of stores and payment collection.

The value proposition for customers was access to household goods without needing upfront cash. This was particularly appealing to those with limited access to traditional credit. The company offered payment plans, making goods affordable over time.

The main customer segment was individuals with low incomes and limited access to credit. These customers often faced challenges in obtaining finance from mainstream lenders. BrightHouse offered an alternative credit solution.

A significant criticism of BrightHouse was the high cost of goods due to interest and fees. Customers often paid much more than the actual value of the items. The business model faced scrutiny for its impact on financially vulnerable customers.

Key Aspects of BrightHouse's Business Model

BrightHouse's business model centered on providing household goods through rent-to-own agreements, targeting low-income customers. The company sourced products, operated through physical stores, and managed weekly payment collections, offering services like warranties and insurance. The model, while providing access to goods without upfront costs, faced criticism for high interest rates and fees.

- Rent-to-Own Agreements: Customers acquired goods through hire purchase, making regular payments.

- Target Market: Focused on low-income individuals with limited access to traditional credit.

- Operational Process: Involved sourcing products, store operations, and payment management.

- Criticisms: High costs due to interest rates and fees, leading to concerns about affordability.

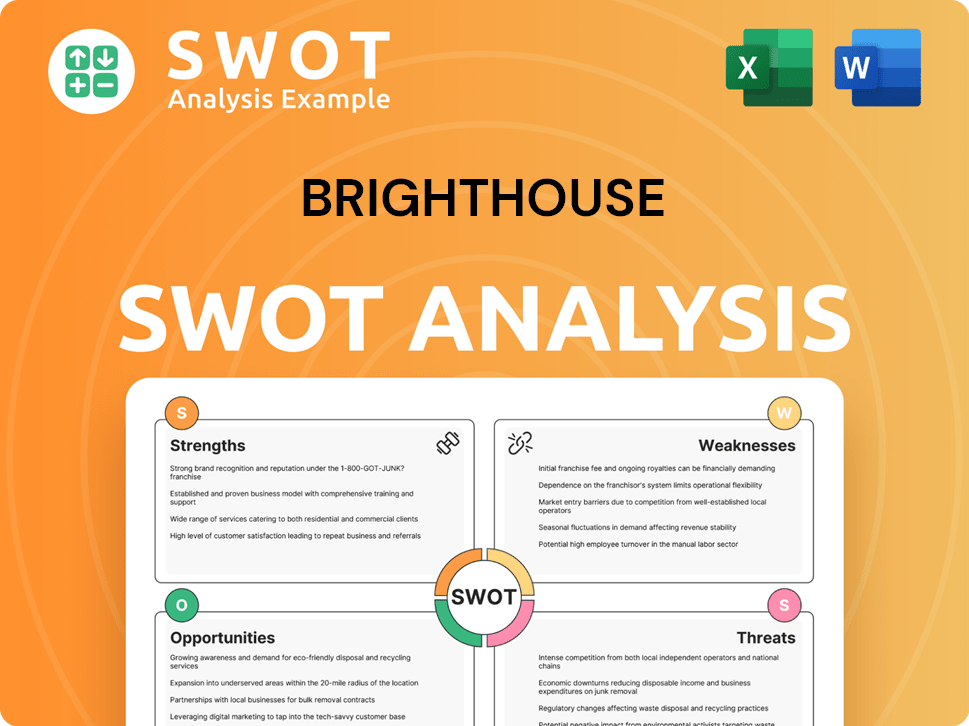

BrightHouse SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does BrightHouse Make Money?

The primary revenue stream for the BrightHouse company was through hire purchase agreements, essentially a form of rent-to-own for household goods. This model allowed customers to acquire items like home electronics, appliances, and furniture by making weekly payments, which included the cost of the product and significant interest charges. The structure provided access to goods for those who might not have been able to afford them upfront, but at a considerable cost over time.

Additional revenue was generated through the sale of warranties and insurance, often bundled with the hire purchase agreements. These add-ons increased the total amount customers paid. In its later years, the company also introduced cash loans, offering up to £1,000 for a fixed term, expanding its financial services offerings.

The financial model of the

Key Revenue and Monetization Strategies

The

- Hire Purchase Agreements: The core of the business, offering goods like appliances and furniture through rent-to-own agreements.

- Interest Charges: Significant interest rates were applied to the weekly payments, increasing the overall cost of the items.

- Warranties and Insurance: Additional products bundled with agreements, increasing the total cost paid by customers.

- Cash Loans: Introduction of short-term cash loans to diversify financial services.

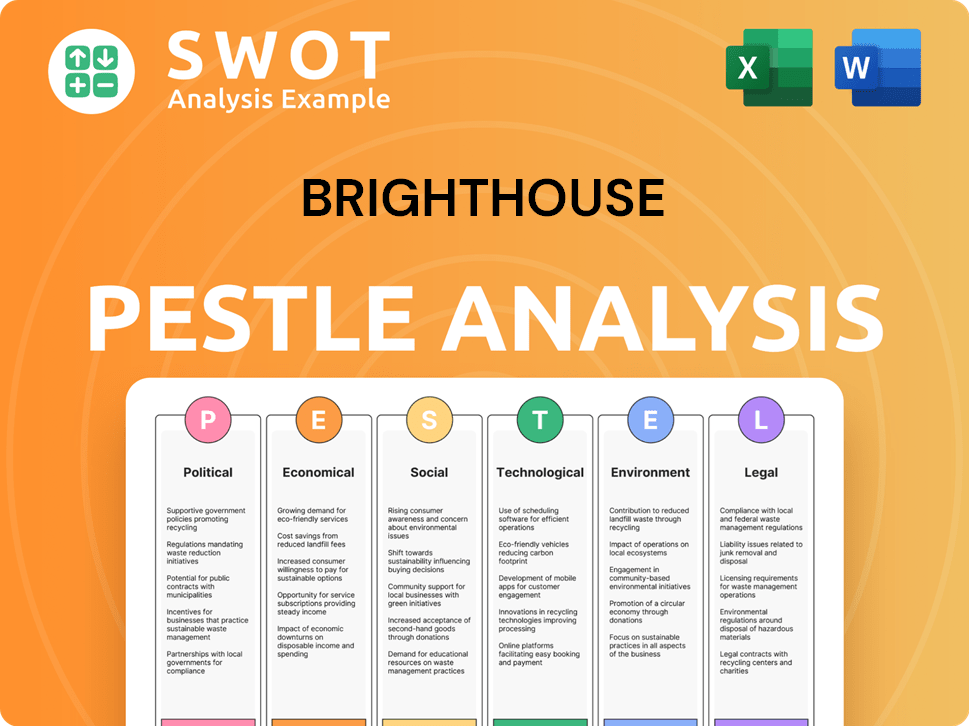

BrightHouse PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped BrightHouse’s Business Model?

The story of the BrightHouse company, originally Crazy George, offers a stark lesson in the consumer credit market. From its rebranding in 2002 to its eventual collapse in 2020, the company navigated a landscape of shifting regulations and consumer behaviors. Key milestones, strategic moves, and the company's competitive edge provide insight into its rise and fall.

The company's journey highlights the importance of adapting to regulatory changes and maintaining sustainable business practices. The acquisitions by Vision Capital and Apollo Management marked significant shifts in ownership, but the underlying challenges related to its business model persisted. Ultimately, the company's reliance on high-cost credit and its targeting of vulnerable consumers led to its demise.

The collapse of the BrightHouse company serves as a case study in the risks associated with high-cost credit and the impact of regulatory scrutiny. The company's story provides valuable lessons for both consumers and businesses operating in the consumer credit sector.

Founded as Crazy George in 1994, the company rebranded to BrightHouse in 2002. The company was acquired by Vision Capital in July 2007. Later, Apollo Management acquired it in December 2017. The Financial Conduct Authority (FCA) ordered the company to pay £14.8 million in redress in October 2017.

In response to challenges, the company planned to close 28 stores in 2017 and another 30 in February 2019. The company aimed to shift from rent-to-own to cash loans in February 2020. The COVID-19 pandemic forced the closure of its 240 shops. The company went into administration on March 30, 2020.

The company's advantage was serving consumers unable to access mainstream credit. It provided access to essential household goods through rent-to-own and payment plans. However, high-cost credit and additional charges undermined this advantage. Stricter affordability assessments and redress schemes led to its downfall.

The company's collapse was due to unsustainable lending practices. The FCA's scrutiny and redress schemes, coupled with the impact of the COVID-19 pandemic, led to its administration. The company's business model, which relied on high-cost credit, became unsustainable under increased regulatory pressure. The Target Market of BrightHouse was significantly impacted.

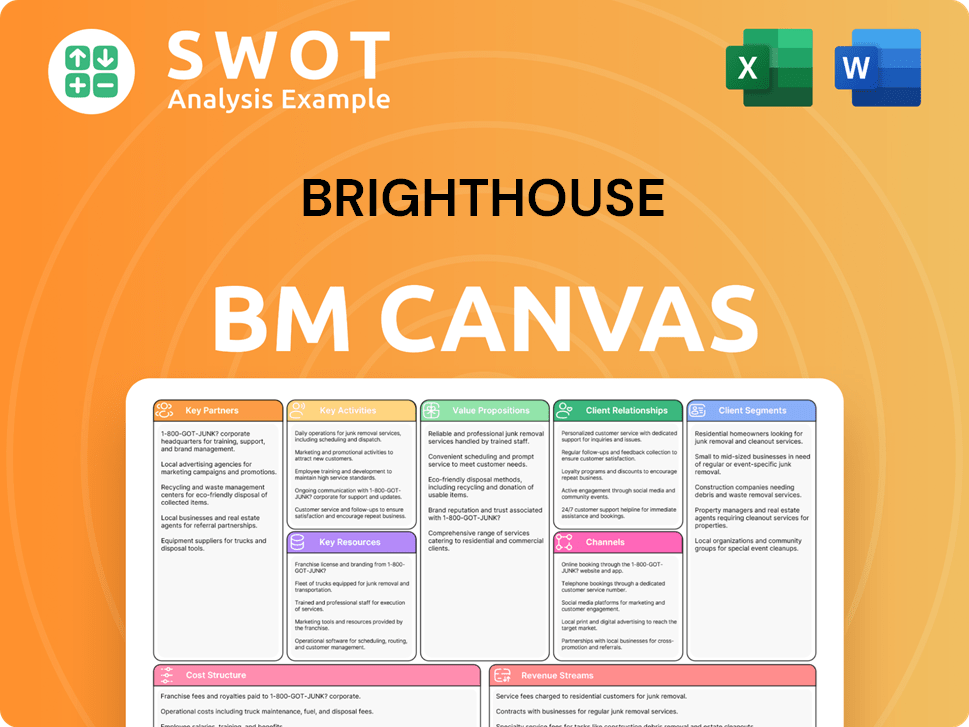

BrightHouse Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is BrightHouse Positioning Itself for Continued Success?

Before its administration, the BrightHouse company held a leading position in the UK rent-to-own market. It operated 240 stores and served approximately 200,000 customers, primarily those with low incomes. BrightHouse offered home electronics, domestic appliances, and furniture through rent-to-own agreements. However, its business model faced significant challenges due to regulatory changes and public scrutiny.

Key risks for BrightHouse included interventions by the Financial Conduct Authority (FCA), which deemed it not a 'responsible lender'. The FCA mandated substantial redress payments to customers. A price cap on rent-to-own agreements, limiting repayments to no more than double the retail price, also impacted its business. Compensation claims for mis-selling and the economic effects of the COVID-19 pandemic, leading to store closures, further contributed to its downfall.

BrightHouse was the largest rent-to-own company in the UK before its administration. It offered various products, including appliances and furniture, through payment plans. Its dominant market position was challenged by regulatory changes and consumer credit concerns.

The company faced significant risks, including regulatory interventions from the FCA. It was required to pay redress to customers. The price cap on rent-to-own agreements and compensation claims also impacted the business model.

After entering administration in March 2020, BrightHouse ceased to operate as a standalone entity. Existing agreements continued, but refunds to compensation claimants were unlikely. The collapse highlighted risks in high-cost credit models.

The UK consumer credit market saw net borrowing rise to £1.2 billion in July 2024, with an annual growth rate of 7.8%. Consumer finance new business grew by 11% compared to December 2023, reaching £114.9 billion for the full year, a 2% increase from 2023. The rent-to-own market was valued at USD 4713.12 million in 2024.

BrightHouse and the Consumer Credit Landscape

The failure of BrightHouse highlights the risks within the consumer credit sector. The FCA's actions and the impact of the pandemic accelerated its demise. The broader market continues to evolve, with changing consumer behaviors and regulatory scrutiny impacting companies like BrightHouse that offered rent-to-own and payment plans.

- The FCA's intervention was a significant factor in BrightHouse's downfall.

- The rent-to-own market is projected to grow at a CAGR of 4.3%.

- Consumer credit in the UK is increasing, with net borrowing up in 2024.

- The article Owners & Shareholders of BrightHouse provides additional insights.

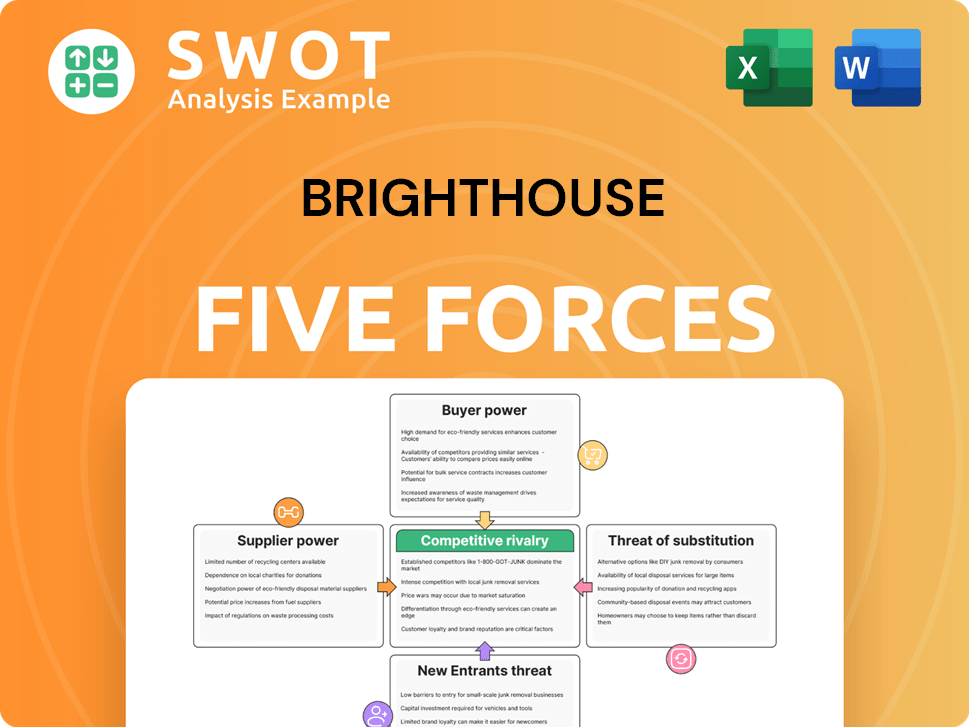

BrightHouse Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of BrightHouse Company?

- What is Competitive Landscape of BrightHouse Company?

- What is Growth Strategy and Future Prospects of BrightHouse Company?

- What is Sales and Marketing Strategy of BrightHouse Company?

- What is Brief History of BrightHouse Company?

- Who Owns BrightHouse Company?

- What is Customer Demographics and Target Market of BrightHouse Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.