BrightHouse Bundle

What Led to BrightHouse's Demise in the UK Market?

BrightHouse, a prominent name in the UK's rent-to-own (RTO) sector, once offered a seemingly convenient way for consumers to acquire essential household goods. Founded in 1994, the company provided hire purchase agreements, targeting those with limited access to traditional credit. Its significant expansion across the UK, however, masked underlying challenges that would ultimately lead to its downfall.

This exploration of the BrightHouse SWOT Analysis will dissect the company's competitive arena, evaluating its market position and key rivals. We will conduct a thorough BrightHouse market analysis, examining its BrightHouse competitive landscape and the broader BrightHouse industry trends that influenced its fate. Furthermore, this analysis will provide insights into the BrightHouse business model and BrightHouse financial performance, offering a comprehensive understanding of its strategic positioning and the factors contributing to its eventual collapse, including a deep dive into BrightHouse competitors.

Where Does BrightHouse’ Stand in the Current Market?

Prior to its administration in March 2020, BrightHouse held a significant position within the UK's rent-to-own (RTO) retail sector. The company specialized in providing essential household goods, including electronics, appliances, and furniture, through hire purchase agreements. This business model primarily targeted customers with limited access to mainstream credit. The company's extensive store network across the UK indicated a substantial geographic presence and a considerable customer base within its niche market.

The Growth Strategy of BrightHouse involved a focus on providing goods through hire purchase, catering to a specific demographic. BrightHouse's competitive landscape was shaped by its unique approach to offering goods to customers who might not qualify for traditional credit. Over time, BrightHouse attempted to diversify its offerings, including cash loans, to maintain relevance and revenue streams. This move reflected a shift in its business model to address a broader range of financial needs.

The company faced pressure from regulatory changes, compensation claims, and shifting consumer preferences, ultimately leading to its insolvency. The BrightHouse market analysis reveals that its financial health suffered due to a combination of factors, contrasting sharply with its earlier growth period. Analyzing the BrightHouse competitive landscape shows that the company struggled to adapt to changing market conditions and increased scrutiny of its core RTO model.

While specific market share figures for BrightHouse in its final years are unavailable in recent 2024-2025 data due to its cessation of trading, its extensive store network indicated a broad geographic presence. BrightHouse's customer base was significant within the rent-to-own sector, serving a demographic often excluded from mainstream credit options. Its strategic positioning focused on providing accessible goods.

BrightHouse's business model centered on hire purchase agreements for household goods. To adapt, the company introduced cash loans, broadening its services. This shift aimed to address a wider range of customer financial needs and maintain revenue streams. The BrightHouse business model evolved in response to market pressures.

The BrightHouse financial performance was under pressure due to regulatory changes, compensation claims, and changing consumer preferences. These factors significantly impacted its financial stability, leading to its insolvency. The BrightHouse financial health assessment shows a decline in its later years.

The BrightHouse competitive landscape was influenced by its unique rent-to-own model and its customer base. The company faced challenges from competitors offering similar services and from evolving consumer preferences. BrightHouse's key rivals analysis highlights the pressures it faced in the market.

Key Factors Impacting Market Position

BrightHouse's market position was significantly impacted by its business model and the regulatory environment. The company's customer base, primarily those with limited access to credit, influenced its strategic positioning. The BrightHouse industry faced challenges from changing consumer preferences and increased competition.

- Regulatory Scrutiny: Increased regulation of the rent-to-own sector and compensation claims for past lending practices.

- Consumer Preferences: Shifting consumer demand towards more affordable and flexible credit options.

- Competitive Pressures: Competition from other RTO providers and alternative credit sources.

- Financial Performance: The company's financial health assessment revealed significant pressures.

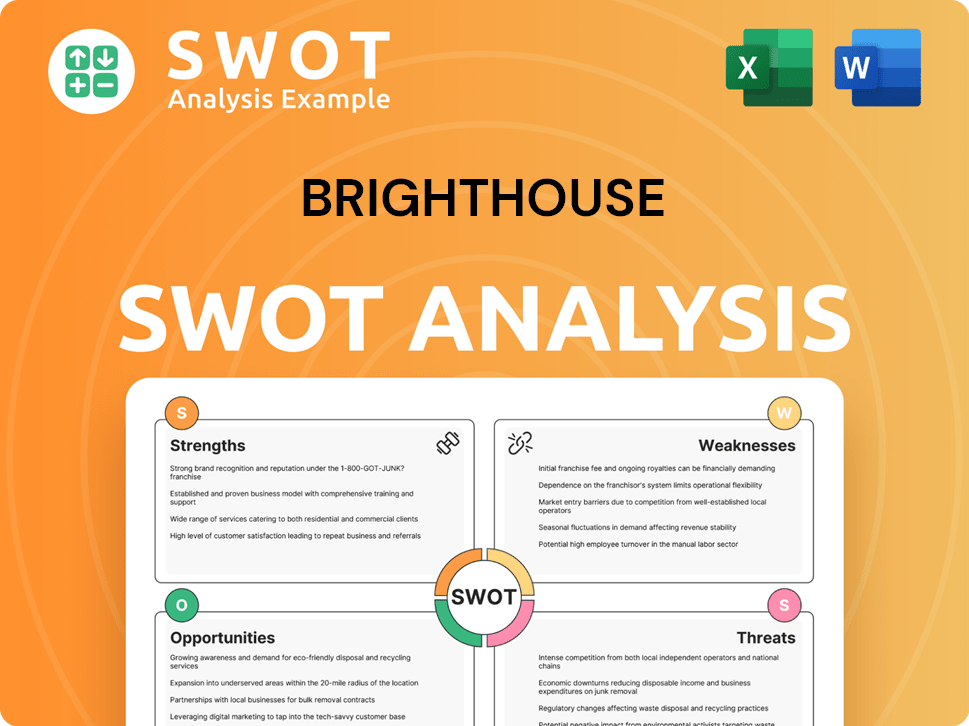

BrightHouse SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

Who Are the Main Competitors Challenging BrightHouse?

The BrightHouse competitive landscape was characterized by a mix of direct and indirect competitors, all vying for the same customer base. BrightHouse's business model, centered on rent-to-own agreements, placed it in a unique position within the retail sector, facing challenges from both traditional retailers and alternative finance providers. Understanding these competitors is crucial for a comprehensive BrightHouse market analysis.

Direct competitors offered similar products and services on hire purchase agreements. Indirect competitors presented alternative ways for customers to acquire goods or access credit. The competitive environment was dynamic, with shifts in consumer behavior and regulatory changes impacting the viability of BrightHouse's business model and its overall financial performance.

BrightHouse's primary direct competitor was PerfectHome. Both companies focused on providing household goods to customers through manageable payment plans. The competition involved product offerings, payment terms, and geographic reach. Data from 2023 showed that PerfectHome held a significant market share in the UK rent-to-own sector, indicating the intensity of the competition.

Mainstream Retailers

Major retailers offered interest-free credit and buy-now-pay-later schemes. These options provided consumers with alternatives to rent-to-own agreements.

Online Lenders

Online lenders and alternative credit providers offered more flexible or lower-cost financing options. This increased the competitive pressure on BrightHouse.

Pawnbrokers and Credit Unions

Pawnbrokers and credit unions served segments of BrightHouse's target market. They offered different forms of accessible credit.

Second-Hand Goods and Charities

The availability of second-hand goods and charitable organizations providing household essentials also impacted BrightHouse. These options provided consumers with alternatives to purchasing new items.

Regulatory Scrutiny

Increased regulatory scrutiny on high-cost credit added to the challenges faced by BrightHouse. This included changes to affordability checks and interest rate caps.

Market Trends

Changing consumer preferences and economic conditions also influenced the competitive landscape. The rise of online shopping and the impact of inflation played a role.

The eventual administration of BrightHouse highlighted the difficulties in sustaining its business model against these varied pressures. The company's challenges underscore the importance of understanding the BrightHouse industry and the strategies needed to compete effectively. Analyzing the BrightHouse key rivals is crucial for any assessment of the company's strategic positioning and its ability to navigate the market. The BrightHouse SWOT analysis would reveal the company's strengths, weaknesses, opportunities, and threats within this complex competitive environment. Data from 2024 indicates that the rent-to-own market continues to evolve, with changing consumer needs and regulatory pressures shaping the future growth prospects of companies in this sector.

Key Competitive Factors

Several factors influenced the competitive dynamics within the BrightHouse market. These included product range, pricing strategies, and the availability of credit. The overall financial health assessment of BrightHouse was impacted by its ability to adapt to these factors.

- Product Range: The variety and appeal of the products offered by BrightHouse and its competitors.

- Pricing Strategy: The competitiveness of interest rates and payment terms.

- Credit Availability: The ease with which customers could obtain credit.

- Geographic Reach: The number and location of stores.

- Customer Service: The quality of customer support.

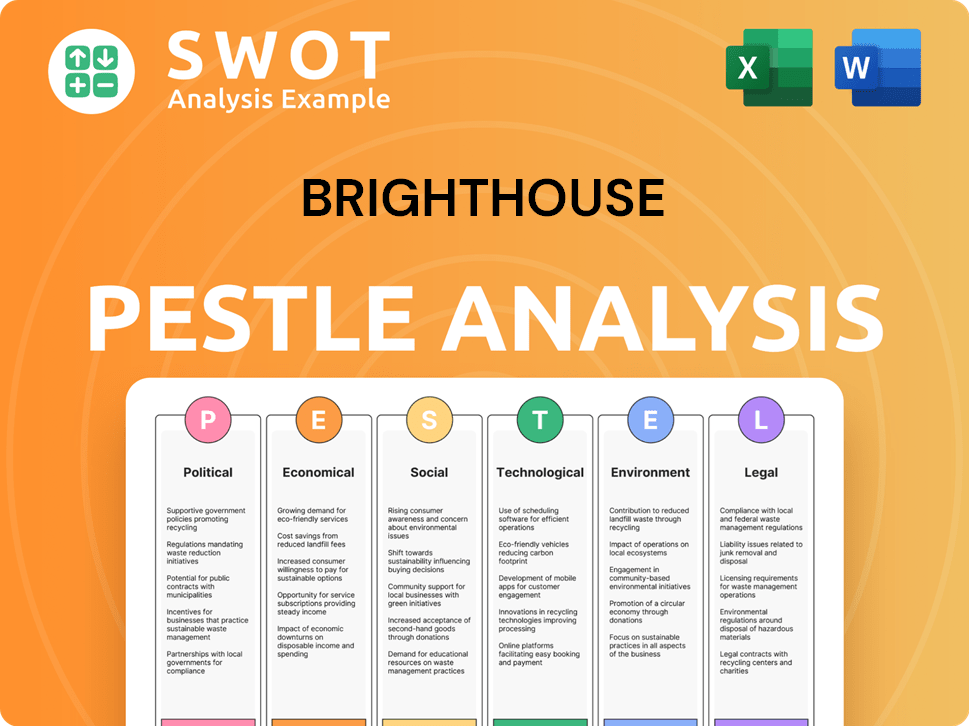

BrightHouse PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Gives BrightHouse a Competitive Edge Over Its Rivals?

The competitive advantages of the company, despite ultimately leading to its administration, revolved around its accessible credit model and extensive retail presence. This accessibility was a key factor, particularly for individuals who might not qualify for traditional loans. The company's physical stores across the UK provided a tangible presence, allowing direct customer interaction, crucial for its service model.

The company developed a customer base that, for a time, showed loyalty due to the perceived convenience and flexibility of its payment plans. The ability to acquire essential household items without a large upfront cost, spread over manageable weekly payments, was a distinct value proposition. However, these advantages faced increasing erosion due to evolving regulatory standards and growing consumer awareness of alternative financing options.

Understanding the Owners & Shareholders of BrightHouse is crucial to grasping the company's competitive landscape and the factors that led to its eventual challenges in the market. The company's business model, while initially successful, came under increasing scrutiny, ultimately leading to its decline.

The company's primary advantage was its ability to offer hire purchase agreements to a customer segment underserved by mainstream credit providers. This allowed customers to acquire essential household goods without a large upfront payment. This model was particularly attractive to those with limited access to traditional credit.

A widespread network of physical stores across the UK provided a tangible presence and allowed for direct customer interaction. This face-to-face interaction was a key element of its service model, enabling product demonstrations and personalized assistance. This physical presence was a key differentiator in the market.

The perceived convenience and flexibility of payment plans fostered a degree of customer loyalty. The ability to spread payments over manageable weekly installments was a distinct value proposition. This payment structure was a key factor in attracting and retaining customers.

The company strategically positioned itself to serve a specific market segment, focusing on those with limited access to traditional credit options. This focus allowed the company to build a strong customer base. This strategic focus initially provided a competitive advantage.

Erosion of Advantages

The company's competitive advantages were gradually eroded by several factors, including evolving regulatory standards and increasing consumer awareness of alternative financing options. The financial conduct authority's interventions and the increasing scrutiny of high-cost credit led to significant reassessment of its business practices.

- Regulatory Scrutiny: Increasing regulatory pressure questioned the affordability and fairness of the high-interest model.

- Consumer Awareness: Growing consumer awareness of alternative, often cheaper, financing options eroded the company's value proposition.

- Financial Conduct Authority (FCA) Interventions: Interventions by the FCA led to a reassessment of business practices.

- Decline: These factors ultimately undermined the sustainability of the company's advantages, contributing to its eventual decline.

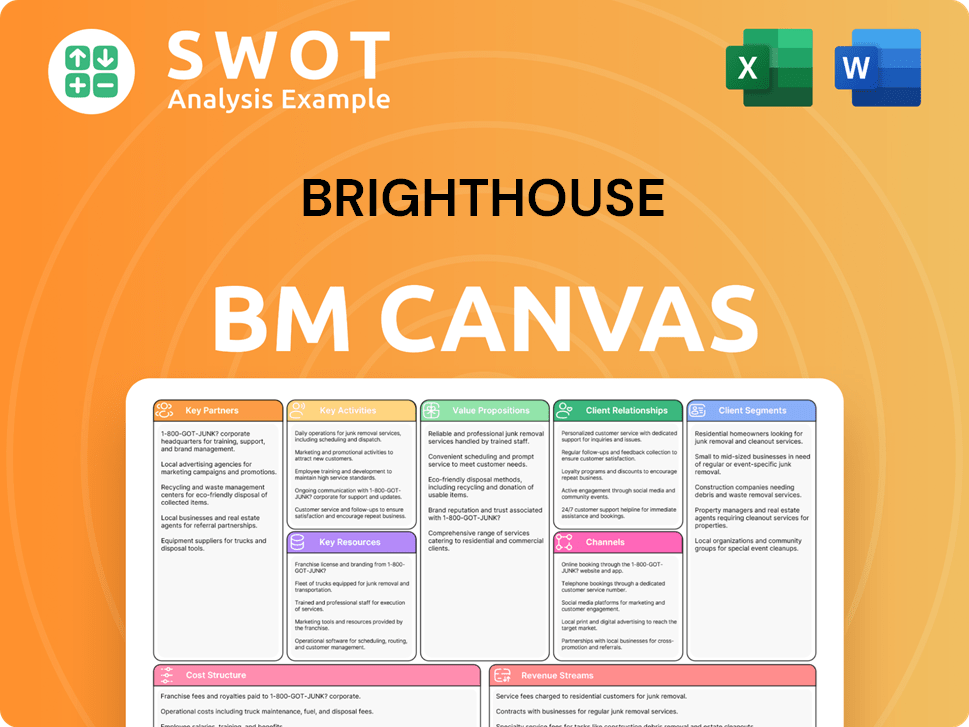

BrightHouse Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Industry Trends Are Reshaping BrightHouse’s Competitive Landscape?

The Marketing Strategy of BrightHouse faced significant challenges due to evolving industry trends and increased competition. The company operated within the rent-to-own (RTO) sector, where regulatory scrutiny and shifts in consumer behavior were key factors. The competitive landscape for BrightHouse involved navigating a complex environment with both traditional rivals and emerging financial technologies.

BrightHouse's business model was significantly impacted by changes in consumer preferences and regulatory pressures. The financial performance of companies like BrightHouse was directly affected by the need to adapt to stricter lending practices and the rise of alternative credit solutions. Understanding these trends is crucial for assessing the company's strategic positioning and future growth prospects.

The BrightHouse industry experienced significant shifts due to increased regulatory scrutiny and changes in consumer behavior. The Financial Conduct Authority (FCA) in the UK imposed caps on the cost of credit and mandated greater transparency, directly impacting the BrightHouse business model. These changes required companies to reassess their pricing models and lending criteria.

Future challenges for the RTO sector include further regulatory reforms and adapting to a competitive landscape. The rise of online lenders and buy-now-pay-later (BNPL) schemes offers consumers more flexible options. These trends pose a threat to the traditional RTO model, requiring companies to innovate and adapt to remain competitive.

Opportunities for the RTO sector include embracing responsible lending practices and exploring hybrid business models. Focusing on niche markets where traditional credit remains inaccessible can also provide growth opportunities. Adapting to changing consumer demands is essential for long-term viability.

The BrightHouse competitive landscape includes traditional credit providers and fintech solutions. The market analysis reveals that the industry's evolution will likely see a move towards greater transparency and lower costs. Companies must adapt to remain relevant in the broader financial landscape.

Key Considerations for BrightHouse

To navigate the challenges, BrightHouse needed to consider several key factors. The company's BrightHouse market share compared to competitors was under pressure from alternative credit providers. A BrightHouse SWOT analysis would have highlighted the need for strategic adjustments, including potentially revising the BrightHouse pricing strategy compared to rivals.

- Focus on responsible lending to mitigate regulatory risks.

- Explore partnerships with fintech companies to offer more flexible payment options.

- Adapt to changing customer demands by providing more transparent and affordable credit solutions.

- Analyze BrightHouse key rivals analysis to understand their competitive advantages.

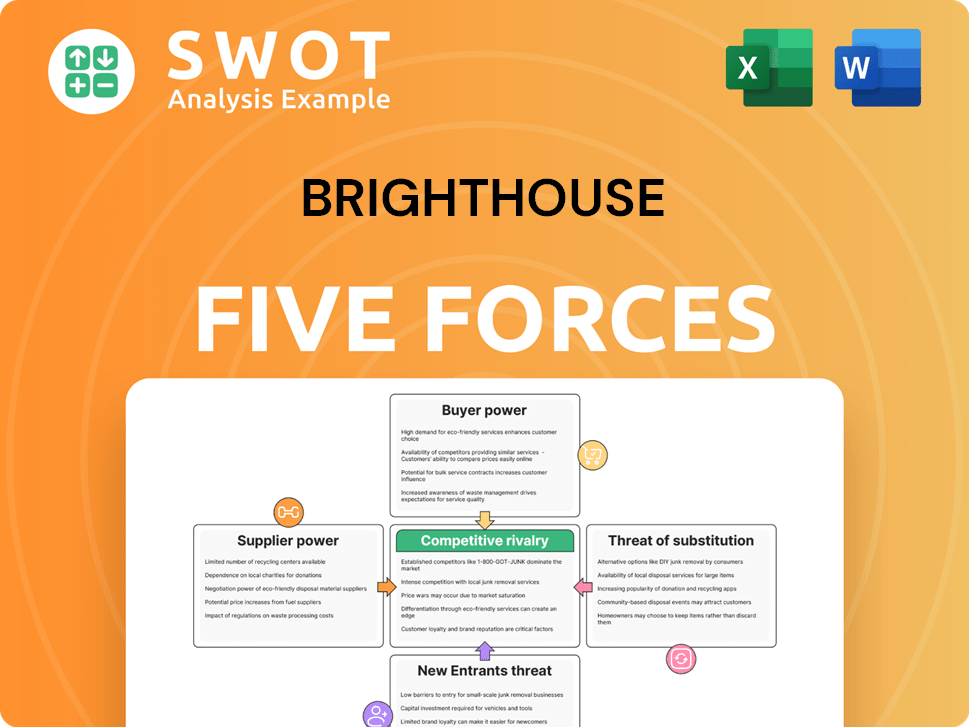

BrightHouse Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of BrightHouse Company?

- What is Growth Strategy and Future Prospects of BrightHouse Company?

- How Does BrightHouse Company Work?

- What is Sales and Marketing Strategy of BrightHouse Company?

- What is Brief History of BrightHouse Company?

- Who Owns BrightHouse Company?

- What is Customer Demographics and Target Market of BrightHouse Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.