BrightHouse Bundle

Can the BrightHouse Story Illuminate Rent-to-Own's Future?

BrightHouse, once a dominant force in the UK's rent-to-own market, offers a compelling case study of success and subsequent collapse. Founded in 1994, the company provided essential household goods through hire purchase agreements, quickly amassing a significant BrightHouse SWOT Analysis and market share. However, its eventual administration in 2020 raises critical questions about business models, financial performance, and the future of the sector.

This analysis transcends a simple company overview, delving into the broader implications of BrightHouse's demise on the rent-to-own landscape. We'll examine the evolution of the BrightHouse business model, its impact on the consumer credit market, and the regulatory shifts that followed. Understanding BrightHouse's financial challenges and opportunities provides valuable insights into the sector's resilience and potential for future growth.

How Is BrightHouse Expanding Its Reach?

As BrightHouse entered administration on March 30, 2020, the company is no longer actively pursuing expansion initiatives. The focus has shifted from its original business model. The company's history is tied to offering hire purchase agreements for household goods through physical retail locations across the UK.

In the context of the post-BrightHouse landscape, the expansion initiatives within the broader rent-to-own or affordable credit sector in the UK would now involve new or existing companies. These entities might look at different strategies. They might explore digital-first strategies, leveraging e-commerce platforms to reach a wider customer base and reduce the overhead associated with brick-and-mortar stores.

There could also be a focus on diversifying product offerings beyond traditional household goods to include services or different types of financial products, addressing gaps left by BrightHouse's exit. Partnerships with community organizations or fintech companies could also be a pathway for new market penetration, aiming to provide more transparent and affordable credit solutions. However, these are hypothetical initiatives for the market rather than for BrightHouse itself.

Companies could focus on online platforms. This approach reduces costs and broadens reach. It allows for greater flexibility in product offerings and customer service. This is in contrast to BrightHouse's physical store model.

Expanding beyond household goods is key. This could include services, such as insurance or warranties. It also involves offering different financial products. This would help to meet a wider range of customer needs.

Collaborations with community organizations are important. These partnerships can help in reaching underserved markets. Fintech companies can also provide technological solutions. This can improve credit assessment and customer management.

The sector must comply with regulations. This includes responsible lending practices. Transparency is also crucial. It helps to build trust with customers. This is a key factor in the current market.

Market Trends

The rent-to-own market is evolving. There is a growing demand for flexible payment options. Digital platforms are becoming more important. Consumer preferences are shifting towards convenience and transparency.

- The UK's consumer credit market was valued at approximately £228 billion in 2023.

- The shift towards digital services is evident, with a significant increase in online transactions.

- Fintech solutions are playing a bigger role in credit assessment and management.

- Regulatory changes continue to shape the industry, focusing on consumer protection.

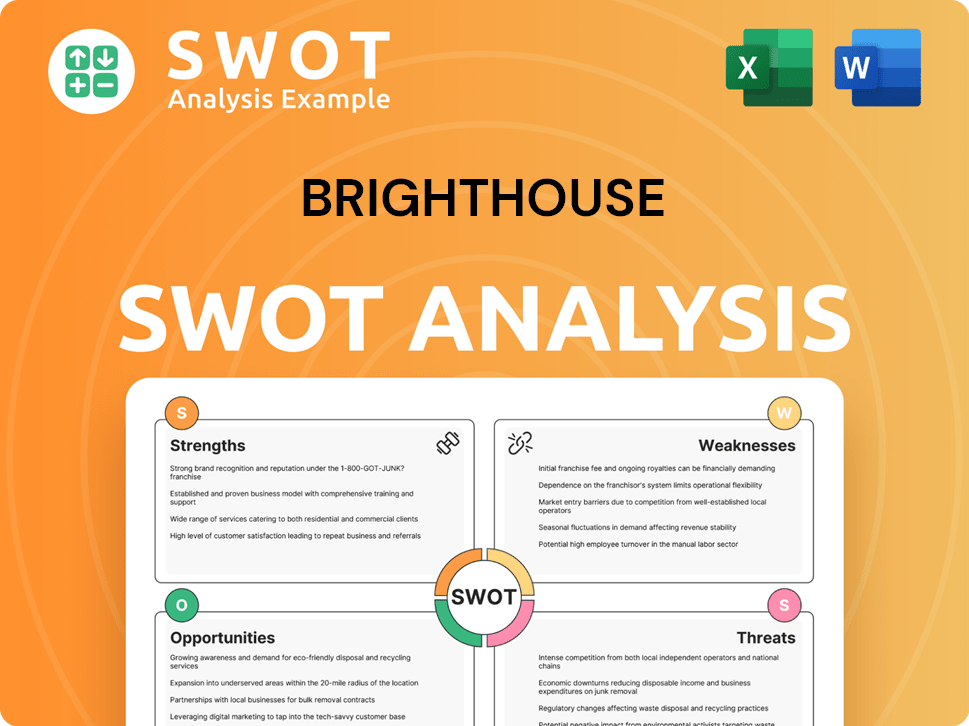

BrightHouse SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does BrightHouse Invest in Innovation?

Given that BrightHouse ceased operations in March 2020, a direct innovation and technology strategy for the company no longer exists. Analyzing the BrightHouse company analysis, its technology focus during its operational period centered on managing hire purchase agreements and customer accounts. This involved internal IT systems for credit checks, payment processing, and inventory management across its store network. The BrightHouse business model relied heavily on in-store sales and physical agreements, which limited its ability to adapt to changing consumer preferences and technological advancements.

The absence of significant R&D investments, adoption of cutting-edge technologies like AI or IoT, or major digital transformation initiatives by BrightHouse, contributed to its challenges in later years. The company's approach remained largely traditional, which contrasted with the evolving demands of the market. The Competitors Landscape of BrightHouse highlights the need for modern strategies in the rent-to-own sector.

Any innovation in the current context of the rent-to-own market would come from new players or existing companies adapting to the void left by BrightHouse. These new strategies would likely involve robust online platforms, data analytics for more accurate credit assessments, personalized customer experiences, and potentially the integration of payment technologies that offer greater flexibility and transparency.

Focus on Online Platforms

Developing robust online platforms is crucial. This includes user-friendly websites and mobile apps for browsing products, applying for credit, and managing accounts. These platforms should offer seamless experiences.

Data Analytics for Credit Assessments

Employing advanced data analytics can significantly improve credit assessment accuracy. This involves analyzing various data points to predict a customer's ability to repay, reducing the risk of defaults. This helps to improve the BrightHouse growth strategy.

Personalized Customer Experiences

Personalizing customer experiences, through tailored product recommendations and flexible payment options, can enhance customer satisfaction and loyalty. This can be achieved through data-driven insights.

Integration of Payment Technologies

Integrating payment technologies that offer greater flexibility and transparency is essential. This includes options like mobile payments, automated payment reminders, and clear terms and conditions. This is important for BrightHouse's future prospects.

Inventory Management Systems

Implementing efficient inventory management systems is vital. This ensures accurate stock levels, reduces waste, and allows for quick order fulfillment. This is a key component of the BrightHouse company analysis.

Customer Relationship Management (CRM)

Utilizing a CRM system to manage customer interactions, track purchase history, and provide customer support can significantly improve customer relationships. This is crucial for understanding BrightHouse's customer demographics and target audience.

Key Technological and Strategic Considerations

For companies seeking to fill the void left by BrightHouse, several technological and strategic considerations are paramount. These elements are critical for success in the evolving rent-to-own sector and influence the BrightHouse market share.

- Data Security and Privacy: Ensuring robust data security and adhering to privacy regulations (like GDPR in Europe and CCPA in California) are non-negotiable. This builds trust with customers.

- Mobile-First Approach: Prioritizing mobile-first design for websites and apps is essential. Mobile devices are the primary way many customers access information and make purchases.

- Automation: Automating key processes, such as credit checks, payment reminders, and customer service inquiries, can improve efficiency and reduce operational costs.

- Integration with Third-Party Services: Seamlessly integrating with third-party services, such as payment gateways, credit bureaus, and delivery services, is vital for a smooth customer experience.

- Continuous Improvement: Regularly analyzing data and customer feedback to improve products, services, and processes is crucial for staying competitive.

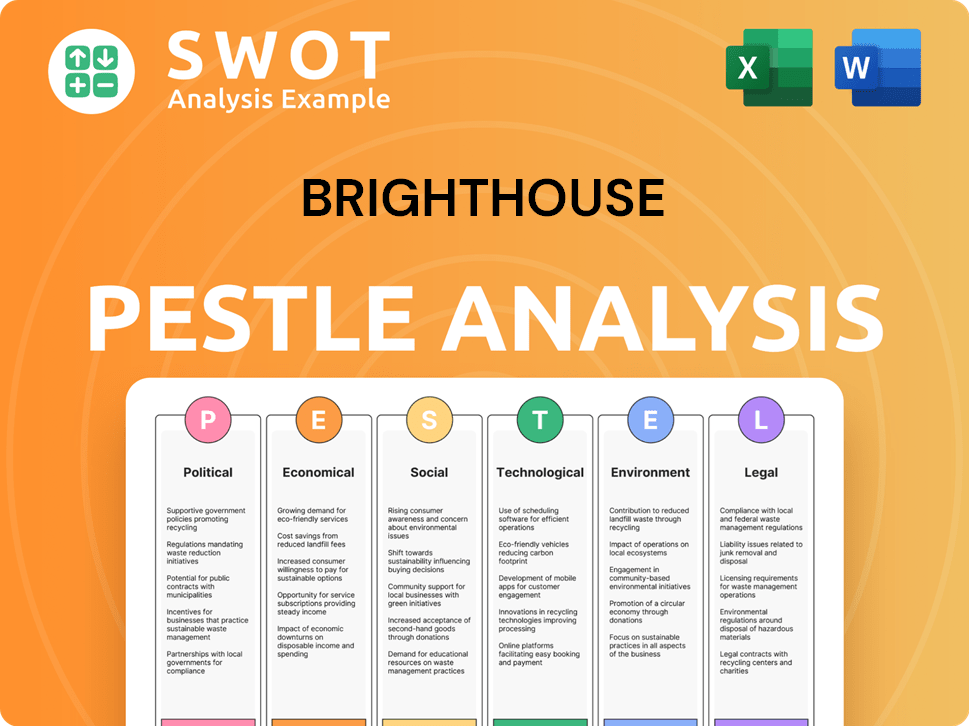

BrightHouse PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is BrightHouse’s Growth Forecast?

Given that BrightHouse entered administration on March 30, 2020, a financial outlook specifically for the company is not applicable. The company's trajectory concluded with its administration, making any future financial projections for it impossible. The Revenue Streams & Business Model of BrightHouse provides insights into the company's past operations, but not its future.

Prior to its administration, BrightHouse faced significant financial challenges. These challenges included increasing regulatory pressures and substantial provisions for customer redress. Its financial performance was marked by losses, stemming from issues related to affordability and subsequent compensation payments. These factors ultimately led to an unsustainable business model.

Any discussion of the financial outlook in the rent-to-own market post-BrightHouse would focus on the strategies of surviving or new market participants. These entities would need to demonstrate sustainable business models and robust financial health to succeed. Key aspects would include transparent pricing, responsible lending practices, and diversified revenue streams.

Regulatory Pressures

The rent-to-own sector, post-BrightHouse, faces heightened regulatory scrutiny. The Financial Conduct Authority (FCA) continues to enforce stricter lending practices. This includes affordability checks and transparency in pricing. These measures aim to protect consumers from unsustainable debt.

Consumer Sentiment

Consumer perception of rent-to-own services has shifted. There's increased awareness of the high costs associated with these agreements. This has led to a decline in demand for traditional rent-to-own products. Companies must now build trust through ethical practices.

Market Dynamics

The market is experiencing consolidation, with fewer players. The remaining companies are adapting their business models. They are offering more flexible payment options and focusing on higher-quality products. This is a shift from the previous focus on volume.

Financial Health

Financial sustainability is critical for any new or existing market participant. This involves maintaining healthy profit margins, managing debt responsibly, and ensuring sufficient capital reserves. The goal is to withstand economic downturns and regulatory changes.

Revenue Diversification

Companies are diversifying their revenue streams. This reduces reliance on traditional rent-to-own agreements. They are exploring options such as offering insurance products, repair services, and extended warranties. This provides multiple income sources.

Technological Advancements

Digital transformation is crucial for the rent-to-own sector. Companies are investing in online platforms, mobile apps, and data analytics. These tools improve customer experience, streamline operations, and enhance risk management. This is a key area for innovation.

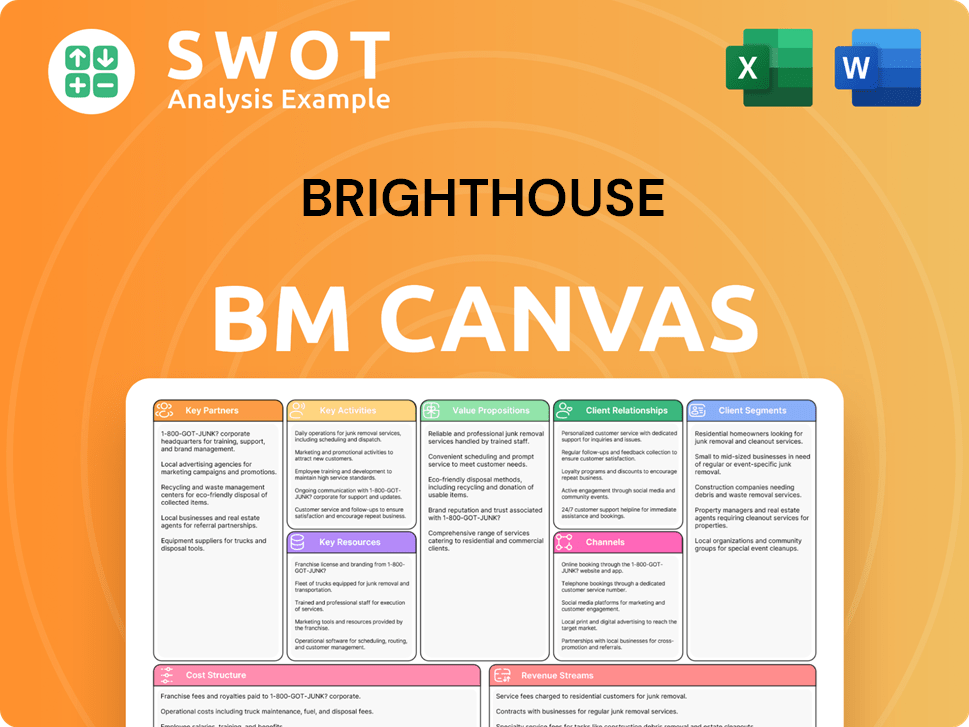

BrightHouse Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow BrightHouse’s Growth?

Since the company is no longer operating, the potential risks and obstacles it faced offer valuable lessons. Any entity operating in the rent-to-own or affordable credit sector faces significant challenges, particularly in the UK market. Understanding these risks is crucial for anyone analyzing the Target Market of BrightHouse and similar business models.

The collapse of the company highlights key areas of concern. These include regulatory scrutiny, market competition, and reputational damage. Furthermore, technological advancements and internal resource constraints add to the complexity of operating in this sector. A thorough understanding of these factors is essential for assessing future prospects.

The company's experience underscores the importance of robust risk management. Compliance with regulations, ethical business practices, and adaptability to market changes are crucial for long-term sustainability. Businesses in this space must prioritize consumer protection and responsible lending to navigate these challenges successfully.

Regulatory Risk

The Financial Conduct Authority (FCA) plays a critical role in regulating the financial services industry in the UK. The FCA's focus on consumer protection means any business in the rent-to-own or affordable credit sector faces intense scrutiny. Compliance with affordability assessments and responsible lending guidelines is paramount.

Market Competition

The market for consumer credit and durable goods is competitive. Traditional retailers, online credit providers, and charitable organizations offer alternatives. Businesses must differentiate themselves through competitive pricing, flexible terms, and superior customer service to maintain market share.

Reputational Risk

Negative public perception can quickly erode customer trust. High costs or aggressive collection practices can lead to reputational damage. Maintaining ethical practices and transparency is crucial to building and preserving a positive brand image in the eyes of consumers and stakeholders.

Technological Disruption

Consumers increasingly expect digital, convenient, and personalized financial services. Businesses must invest in technology to meet these expectations. Digital platforms, mobile apps, and online customer service are essential for staying competitive in the modern market.

Internal Resource Constraints

Managing complex regulatory requirements and customer complaints effectively requires significant resources. Businesses need robust risk management frameworks and skilled personnel to handle these challenges. Investing in training and compliance programs is essential.

Financial Penalties

Financial penalties and compensation claims can significantly impact a company's financial performance. The company faced substantial penalties due to regulatory breaches, highlighting the financial risks associated with non-compliance. Ensuring compliance is critical to avoid these costly consequences.

The FCA's ongoing scrutiny of the consumer credit market requires constant vigilance. Businesses must stay updated on regulatory changes and adapt their practices accordingly. This includes regular audits and proactive engagement with regulatory bodies to ensure compliance.

Building and maintaining customer trust is essential for long-term success. Transparency in pricing, fair lending practices, and responsive customer service are key. Addressing customer complaints promptly and effectively is also crucial to preserving a positive reputation.

Investing in digital platforms and customer service tools is vital. Companies must offer online account management, mobile apps, and efficient communication channels. This enhances customer experience and streamlines operations. The goal is to provide a seamless and user-friendly service.

Maintaining financial stability requires careful management of costs and risks. Responsible lending practices, effective debt collection strategies, and robust financial planning are critical. Diversifying revenue streams can also help mitigate financial risks.

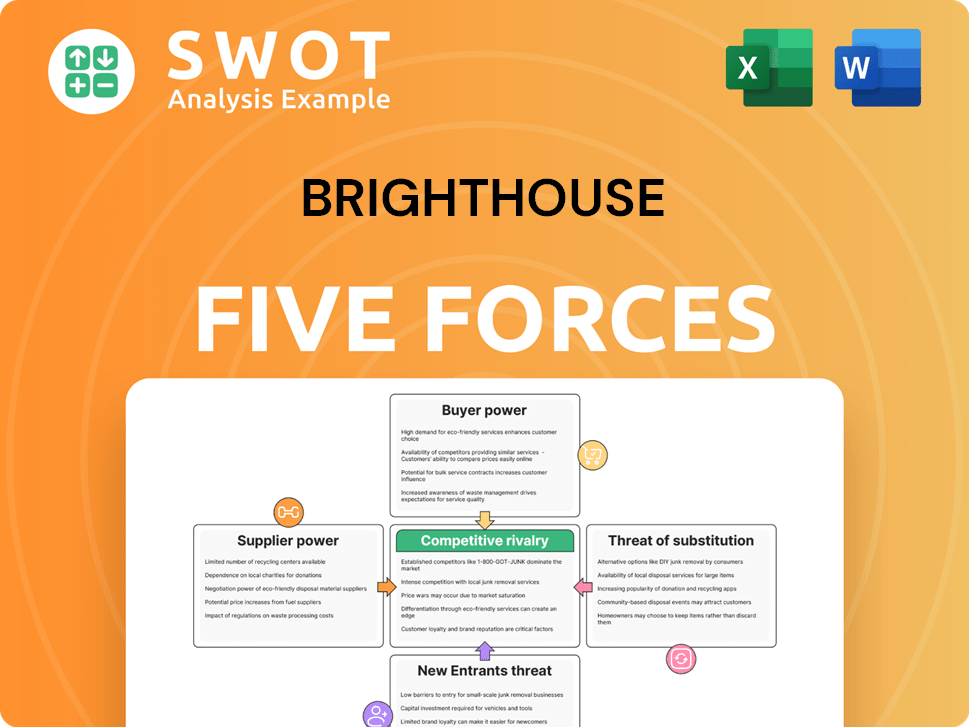

BrightHouse Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of BrightHouse Company?

- What is Competitive Landscape of BrightHouse Company?

- How Does BrightHouse Company Work?

- What is Sales and Marketing Strategy of BrightHouse Company?

- What is Brief History of BrightHouse Company?

- Who Owns BrightHouse Company?

- What is Customer Demographics and Target Market of BrightHouse Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.