Non-Standard Finance Bundle

Who Does Non-Standard Finance Serve?

In the dynamic world of financial services, understanding customer demographics and the target market is crucial for success. Non-Standard Finance plc (NSF), a prominent player in the UK's Non-Standard Finance SWOT Analysis, has evolved its strategies to meet the needs of a specific customer base. This exploration delves into the core of NSF's customer profile, examining who they are and how the company tailors its offerings.

The shift towards digital platforms by Non-Standard Finance reflects a broader trend in the financial services sector, driven by changes in consumer behavior. Understanding the target market, including their income levels and credit score requirements, is vital for effective customer acquisition strategies and retention. This analysis aims to provide insights into the customer demographics of non-standard finance, helping to identify the demographic profile of subprime borrowers and the impact of economic factors.

Who Are Non-Standard Finance’s Main Customers?

The primary customer segments for Non-Standard Finance plc (NSF) are individuals underserved by mainstream financial institutions in the UK. This includes those with impaired credit histories, lower incomes, or a need for small, short-term loans that traditional banks often avoid. NSF's offerings, such as guarantor loans and home credit, are tailored to meet the needs of this specific demographic.

While specific demographic breakdowns aren't publicly detailed, the core customer base often includes working-class individuals, single-parent households, or those facing unexpected expenses. These customers may not meet the stringent criteria of high-street banks. The company's services are designed to provide financial solutions to those who find it difficult to access traditional financial products.

Recent shifts indicate an increasing focus on a younger, digitally-savvy demographic that prefers online platforms. This expansion is evident in the launch of new digital lending platforms in 2024, aiming to capture a broader range of customers who value convenience and speed. This change reflects evolving market trends and the company's strategic decision to enhance accessibility.

The customer base primarily consists of individuals with subprime credit scores. This often includes those with limited credit history or those who have faced financial difficulties. These customers may have been rejected by traditional banks and are seeking alternative finance options.

NSF segments its target market based on the type of loan needed and the customer's preferred interaction method. Guarantor loans cater to younger adults or new residents with limited credit history. Home credit services target those who prefer doorstep collection and a personal relationship with their lender.

While specific age ranges are not publicly available, the customer base likely includes a broad spectrum, with a significant portion being younger adults seeking to build credit or those in middle age facing unexpected financial challenges. The shift towards digital platforms may attract a younger demographic.

Customers typically have lower incomes compared to those using mainstream financial services. This is a key factor in their difficulty accessing traditional loans. NSF's services are designed to be accessible to individuals with varying income levels who may not meet the criteria of high-street banks.

Non-Standard Finance Customer Behavior Analysis

Customer behavior is influenced by factors like credit history, income, and the need for quick access to funds. Many customers seek loans to cover unexpected expenses. The move towards digital platforms reflects a desire for convenience and speed in the application process.

- Credit Score Requirements: Customers typically have lower credit scores, making them ineligible for traditional loans.

- Customer Acquisition Strategies: NSF uses various channels, including online platforms and branch networks, to reach its target audience.

- Customer Retention Strategies: Providing good customer service and flexible repayment options is essential for retaining customers.

- Impact of Economic Downturn: Economic downturns can increase demand for non-standard finance as more people face financial difficulties.

For a deeper understanding of the competitive landscape, consider reviewing the Competitors Landscape of Non-Standard Finance.

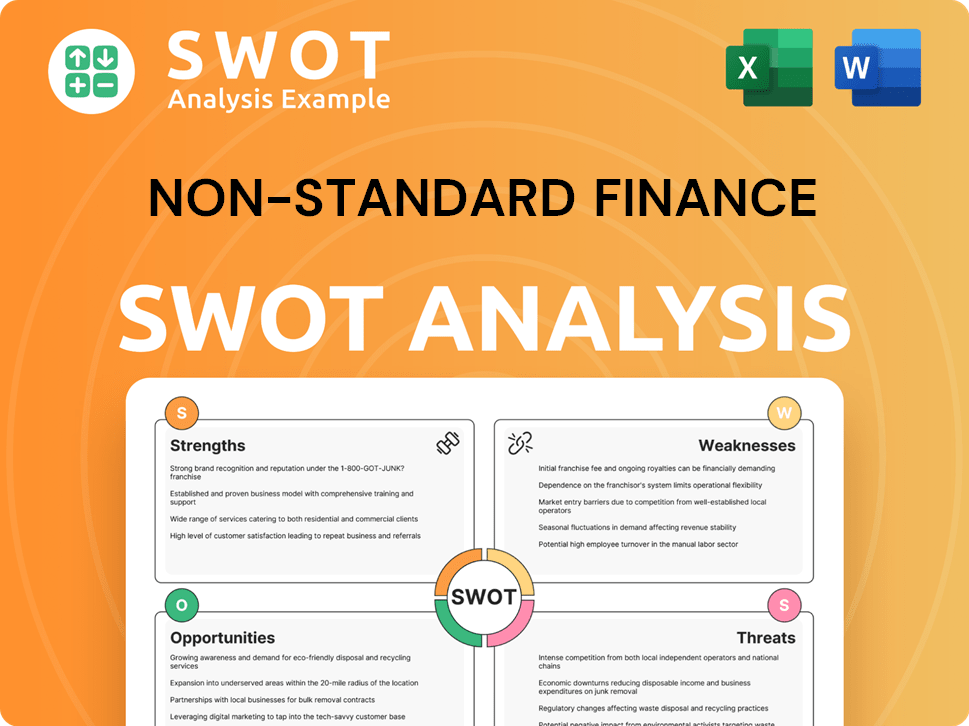

Non-Standard Finance SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do Non-Standard Finance’s Customers Want?

The core needs of customers seeking services from companies like Non-Standard Finance (NSF) center around accessibility and flexibility in obtaining credit. These individuals often face barriers in accessing traditional financial products, leading them to seek alternative finance solutions. Their primary motivation is to address immediate financial needs, such as unexpected expenses or bridging income gaps.

Purchasing behaviors are driven by urgency, with decisions heavily influenced by the ease of application, transparency of terms, and the speed of fund disbursement. The customer base frequently demonstrates a preference for manageable repayment schedules, and some appreciate the personal interaction offered by home credit agents. Understanding these preferences is crucial for tailoring products and services effectively.

Psychological drivers include a desire for financial stability and stress reduction, while practical drivers focus on covering essential expenses. Aspirational drivers, though less prominent, involve improving credit scores for future access to mainstream finance. The company addresses common pain points, such as rejection from traditional lenders and complex application processes, by offering streamlined solutions.

Key Customer Needs and Preferences

The target market for Owners & Shareholders of Non-Standard Finance is characterized by specific needs and behaviors. These customers often have limited access to mainstream financial services, making them reliant on alternative finance options. Understanding these needs is critical for product development and customer service.

- Accessibility: Customers require easy access to credit, often due to rejection from traditional lenders.

- Flexibility: They need flexible repayment terms that align with their financial situations.

- Speed: Quick access to funds is essential to address immediate financial needs.

- Transparency: Clear and understandable loan terms are crucial for building trust.

- Personalization: Some customers prefer the personal touch of home credit agents.

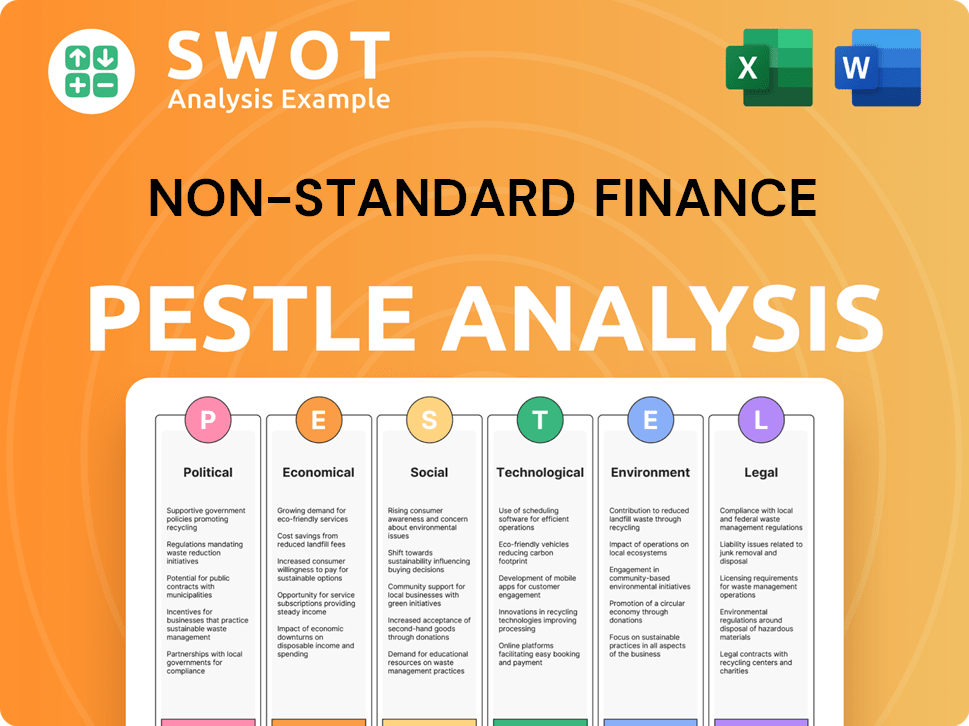

Non-Standard Finance PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does Non-Standard Finance operate?

The primary geographical market for Non-Standard Finance plc is the United Kingdom. Its operations are largely concentrated in the UK, with a historical focus on areas with a higher density of underserved populations. The company's branch-based lending operations have traditionally been strongest in England, Wales, and Scotland.

The company's strategy includes a shift towards a more geographically flexible approach within the UK. This is facilitated by the launch of online platforms, which began in 2024. This allows the company to reach customers regardless of their physical proximity to a branch.

This digital expansion aims to broaden the market reach beyond traditional strongholds. It also aims to capture customers in areas where a physical presence might not be economically viable. Differences in customer demographics and preferences exist across these regions, necessitating a localized approach.

Geographic Focus

The UK remains the core market for Non-Standard Finance. The company's physical branches are historically located in regions with higher concentrations of underserved populations. This focus reflects the demand for Revenue Streams & Business Model of Non-Standard Finance.

Digital Expansion

The company is expanding its digital presence to reach a wider customer base. Online platforms launched in 2024 allow for a more geographically agnostic approach. This strategy aims to extend the reach beyond areas with physical branches.

Localized Approach

The company recognizes regional differences in customer demographics and preferences. It maintains both physical and digital channels to cater to diverse customer needs. This ensures customers can choose their preferred method of engagement.

Market Segmentation

The company likely segments its target market based on geography. This segmentation helps tailor its offerings and marketing efforts. This approach ensures that the company can effectively reach its target audience.

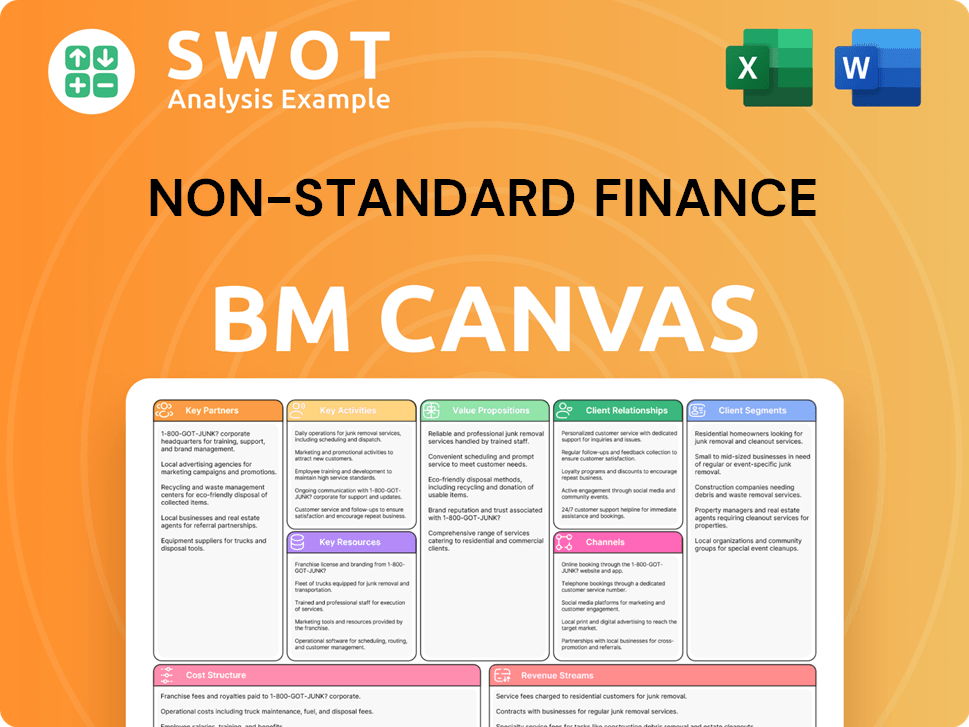

Non-Standard Finance Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does Non-Standard Finance Win & Keep Customers?

The customer acquisition and retention strategies of non-standard finance companies are crucial for success in the financial services industry. These strategies are tailored to reach and serve the specific needs of their target market, which often includes individuals with limited access to traditional financial products. The approach involves a blend of traditional methods and digital channels to effectively engage with potential and existing customers.

Historically, customer acquisition relied heavily on word-of-mouth referrals and local advertising, especially in communities where the company’s presence was strong. However, the shift towards digital platforms has become increasingly important. Digital marketing, including online advertising, SEO, and social media campaigns, helps reach a broader audience, streamline the application process, and enhance user experience for online customers. This hybrid approach aims to improve customer lifetime value and reduce churn rates.

The company focuses on building trust through transparent communication about loan terms and responsible lending practices. Customer retention is strengthened through personalized experiences, consistent customer service, and addressing individual financial needs. The ability to offer flexible repayment options and understanding in cases of financial difficulty also contributes to customer loyalty.

Non-standard finance companies utilize a variety of channels to acquire customers. These include online advertising, search engine optimization (SEO), and social media campaigns to reach a broader audience. Traditional methods such as local advertising and referrals still play a role, especially in specific communities.

The launch of digital lending platforms is a key part of acquisition strategy. These platforms aim to streamline the application process and improve the user experience. This shift indicates a significant investment in digital acquisition to meet evolving customer preferences and market demands.

Sales tactics often involve clear communication of loan terms and responsible lending practices. This approach builds trust with a demographic that may be wary of financial services. Transparency and ethical practices are crucial in the subprime lending market.

Customer retention is fostered through personalized experiences and consistent customer service. Offering flexible repayment options and understanding in cases of financial difficulty helps build customer loyalty. CRM systems are increasingly used for targeted campaigns.

Key Strategies for Customer Acquisition and Retention

Effective strategies for acquiring and retaining customers in the non-standard finance sector focus on understanding the target market and providing tailored services. The goal is to increase customer lifetime value.

- Digital Marketing: Utilizing online advertising, SEO, and social media campaigns to reach a broader audience.

- Streamlined Application Processes: Simplifying the application process through digital platforms to improve user experience.

- Transparent Communication: Clearly communicating loan terms and promoting responsible lending practices to build trust.

- Personalized Customer Service: Offering tailored experiences and consistent support to meet individual financial needs.

- Flexible Repayment Options: Providing flexible repayment plans and understanding during financial difficulties to retain customers.

- Data-Driven Insights: Using customer data and CRM systems to target campaigns and understand customer segments.

Analyzing the Growth Strategy of Non-Standard Finance can provide additional insights into how these strategies are implemented and how they contribute to overall business success. The evolution from field-based approaches to hybrid models that integrate digital platforms demonstrates a commitment to adapting to changing market dynamics and customer preferences.

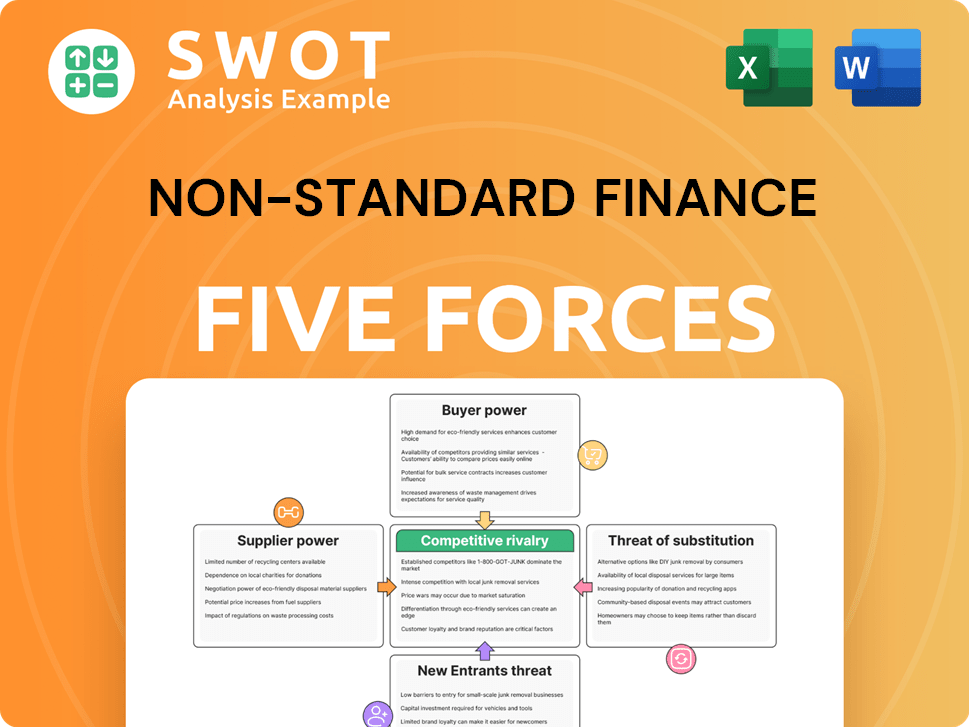

Non-Standard Finance Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Non-Standard Finance Company?

- What is Competitive Landscape of Non-Standard Finance Company?

- What is Growth Strategy and Future Prospects of Non-Standard Finance Company?

- How Does Non-Standard Finance Company Work?

- What is Sales and Marketing Strategy of Non-Standard Finance Company?

- What is Brief History of Non-Standard Finance Company?

- Who Owns Non-Standard Finance Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.