Non-Standard Finance Bundle

How Does Non-Standard Finance PLC Navigate the Financial Landscape?

Non-Standard Finance plc (NSF) offers a crucial service in the UK, providing Non-Standard Finance SWOT Analysis to consumers often overlooked by traditional lenders. Established in 2014, NSF has strategically positioned itself within the non-standard finance sector, utilizing both branch-based lending and online platforms to offer products like guarantor loans and home credit. Understanding NSF's operations is vital for anyone interested in the evolving world of financial services and the credit market.

The alternative lending market is experiencing significant growth, with increasing demand for loans from underserved communities. This growth highlights the importance of understanding how companies like NSF operate, especially when considering the complexities of subprime loans and the associated risks. Analyzing NSF's approach offers valuable insights into the broader financial ecosystem and the strategies employed to meet the needs of a specific demographic. For those seeking non-standard finance options for bad credit or exploring the difference between non-standard and traditional loans, this analysis is essential.

What Are the Key Operations Driving Non-Standard Finance’s Success?

Non-Standard Finance (NSF) provides unsecured credit to individuals who may struggle to access loans from traditional banks, operating within the alternative lending sector. Their core business revolves around offering financial services, primarily through branch-based lending and home credit options. This approach allows NSF to cater to a specific demographic often overlooked by mainstream financial institutions, thereby creating a value proposition centered on financial inclusion.

The company's value proposition is built on providing accessible credit solutions. NSF's focus on subprime loans and its operational model, which combines physical branches with digital platforms, allows it to serve customers who may have limited access to financial resources. The company emphasizes responsible lending practices, aiming to ensure that customers can afford to repay their loans, which is crucial in the non-standard finance market.

NSF's operations are supported by investments in branch expansion, recruitment, training, and IT infrastructure, all geared towards improving customer outcomes. This operational model, combining physical presence with digital accessibility, allows NSF to effectively serve a niche demographic often overlooked by mainstream financial institutions. NSF’s established presence and experience in the non-standard finance sector, including a track record of acquiring and integrating businesses, contribute to its deep understanding of the market and informed decision-making.

NSF primarily offers unsecured credit through branch-based lending (Everyday Loans) and home credit (Loans at Home). Everyday Loans serves approximately 66,000 customers across around 75 branches in the UK, demonstrating a significant physical presence.

The operational processes involve a blend of in-person and digital channels for loan origination, customer service, and collections. This hybrid approach allows NSF to reach a broader customer base and offer convenience. The company's strategy includes investments in IT infrastructure to enhance efficiency.

NSF targets individuals who may find it difficult to obtain credit from traditional lenders. This focus on financial inclusion is a key aspect of its value proposition. The company aims to provide accessible credit solutions while emphasizing responsible lending practices.

NSF operates within the non-standard finance sector, a market segment that addresses the needs of individuals who may not meet the criteria of mainstream financial institutions. The company's experience and established presence in this sector contribute to its market understanding. For a deeper dive into the competitive landscape, see Competitors Landscape of Non-Standard Finance.

Key Operational Aspects

NSF's operations are supported by investments in branch expansion, recruitment, training, and IT infrastructure. This strategic approach aims to improve customer outcomes and enhance operational efficiency. The company's ability to acquire and integrate businesses also contributes to its market understanding.

- Branch Network: Approximately 75 branches in the UK.

- Customer Base: Serving around 66,000 customers.

- Digital Integration: Utilizing online platforms to broaden customer reach.

- Responsible Lending: Emphasizing affordability and customer repayment capacity.

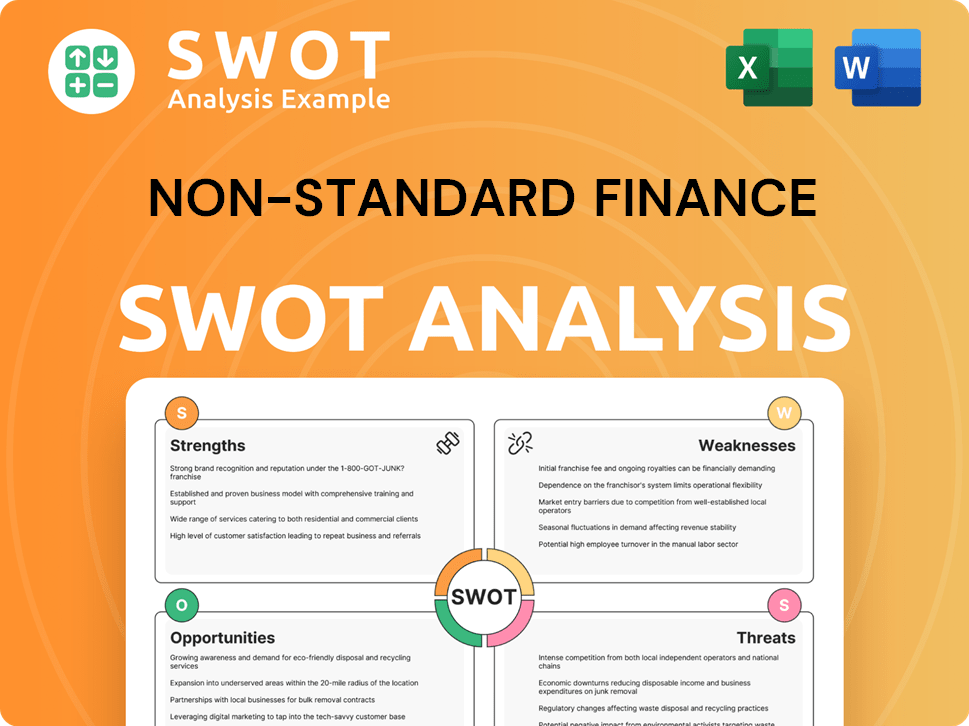

Non-Standard Finance SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Non-Standard Finance Make Money?

The primary revenue streams for Non-Standard Finance (NSF) are centered on interest and fees derived from its credit products. These include branch-based lending, home credit, and, historically, guarantor loans. While precise revenue breakdowns for 2024-2025 are not available in the provided information, the company's core focus remains on these lending activities, demonstrating a commitment to its established financial services model.

Historically, guarantor loans played a significant role in NSF's lending portfolio; however, this segment is now managed for run-off. The home credit sector continues to be a key area of operations. This strategic shift reflects an adaptation to market conditions and regulatory changes, as highlighted in the Growth Strategy of Non-Standard Finance.

NSF's monetization strategy involves tailoring its products to a specific customer base, often those with limited access to mainstream financial services. The company's dual approach, combining branch-based and online lending channels, allows it to reach a broader customer base and adapt to diverse needs. This approach optimizes revenue generation potential within the alternative lending market.

Key Revenue Generation Strategies

NSF's revenue generation is primarily driven by interest and fees from loans, with a strategic focus on specific lending areas. The company's approach involves a customer-centric model, providing financial solutions to those who may find it challenging to access traditional financial services. This targeted approach is crucial for success in the non-standard finance sector.

- Interest and Fees: Revenue is generated through interest charged on loans and various fees.

- Branch-Based Lending: NSF operates through physical branches to provide loans, offering in-person services.

- Home Credit: Home credit services are a key component, providing financial products directly to customers.

- Strategic Adaptation: The company has adapted its offerings, such as reducing its presence in guarantor loans, to align with market and regulatory changes.

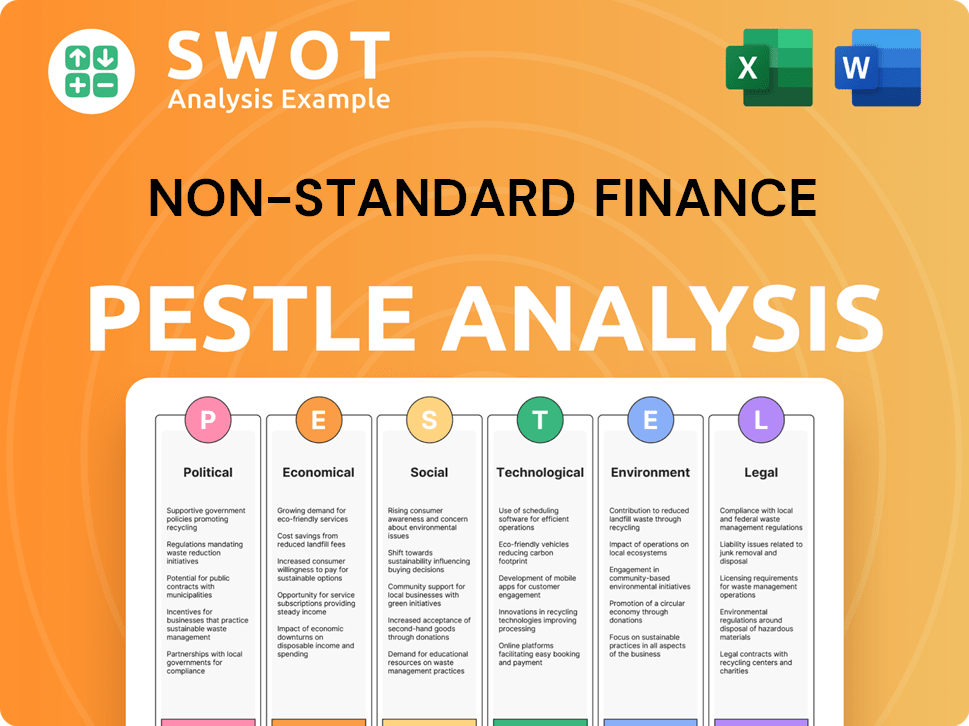

Non-Standard Finance PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Non-Standard Finance’s Business Model?

In 2014, the company was established with the goal of acquiring and developing businesses within the UK's non-standard consumer finance sector. It began by raising £102 million through a listing as a cash shell. This marked the start of its journey in the financial services industry, focusing on alternative lending solutions.

A key strategic move involved completing three acquisitions, which solidified its position as a major player in the market. The acquisition of Everyday Loans Holdings Limited in 2016 was particularly significant, strengthening its presence in branch-based lending. The company's strategic focus on the non-standard finance market highlights its commitment to serving underserved consumers.

The company has navigated operational and market challenges, including regulatory issues and the impact of the pandemic. These factors influenced its financial performance, leading to a pre-tax loss. In response, the company pursued a scheme of arrangement to address historical unaffordable lending liabilities, a crucial part of a proposed recapitalization plan. This recapitalization aimed to boost its financial position and restore Everyday Loans to profitability.

Founded in 2014, the company's initial public offering raised £102 million. The acquisition of Everyday Loans in 2016 was a pivotal moment, expanding its reach in branch-based lending. The company's history reflects its strategic focus on the non-standard finance market and its ability to adapt to industry changes.

The company's strategic moves include acquisitions to grow its market presence. It has also implemented a scheme of arrangement to address liabilities. The company's strategies show its commitment to strengthening its financial position and adapting to market conditions.

The company's competitive advantages stem from its established presence in the non-standard finance sector. Its focus on underserved consumers creates consistent demand for its services. The company uses multiple lending channels, including branches and online platforms, to enhance market reach.

The company is exploring opportunities to leverage technology and artificial intelligence. This includes optimizing operational processes and potentially expanding its lending model. These efforts demonstrate the company's commitment to innovation and improving its services.

Competitive Advantages and Future Strategies

The company's competitive edge lies in its established presence in the non-standard finance sector, providing a deep understanding of the market. Its focus on underserved consumers ensures a steady demand for services, and it benefits from multiple lending channels. The company is also exploring new technologies.

- Established Market Presence: A long-standing presence in the non-standard finance sector provides a deep understanding of market dynamics and customer needs.

- Focus on Underserved Consumers: Targeting underserved consumers creates consistent demand for financial services, offering Owners & Shareholders of Non-Standard Finance.

- Multiple Lending Channels: Utilizing both branch networks and online platforms enhances market reach and accessibility, catering to diverse customer preferences.

- Technological Integration: Exploring opportunities to leverage technology and AI to optimize operations and expand lending models.

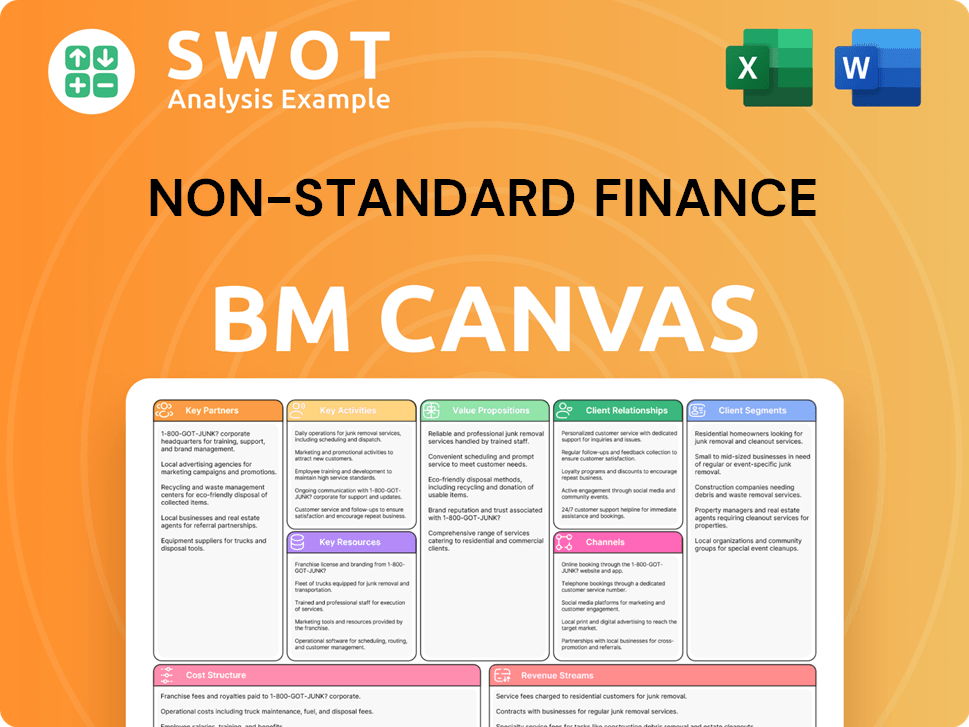

Non-Standard Finance Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Non-Standard Finance Positioning Itself for Continued Success?

In the UK, the company, a prominent player in the non-standard finance sector, has established itself as a significant provider of unsecured credit, particularly to those often overlooked by mainstream financial institutions. Its operational strategy, which combines both physical branches and online platforms, helps broaden its reach and improve customer accessibility. The non-prime consumer credit market in the U.S. alone reached $1.2 trillion in 2024, demonstrating substantial and growing demand that the company is positioned to address.

Several factors could impact the company's operations and revenue. Intensified regulatory scrutiny, particularly from the UK's focus on consumer protection, could lead to stricter rules and higher compliance costs. Past financial difficulties, including a significant drop in share price and a scheme of arrangement, have also affected investor confidence and access to capital. The company delisted from the London Stock Exchange in July 2023.

The company holds a significant position within the UK's non-standard finance sector, specializing in unsecured credit for underserved consumers. Its multi-channel strategy, integrating branch-based lending with online platforms, enhances market reach. The company aims to sustain and expand its ability to make money by continuing to cater to its target demographic and adapting to market conditions.

Key risks include increased regulatory pressure and higher compliance costs due to the UK's focus on consumer protection. Past financial struggles, such as a significant share price drop and a scheme of arrangement, have impacted investor trust. As of May 2025, the company's shares were trading at 0.04p, significantly below previous levels.

Despite challenges, there's potential for growth in the underserved consumer market, expected to be worth $200 billion by late 2024. Strategic initiatives include expanding into international markets and leveraging AI to optimize lending processes. Brief History of Non-Standard Finance provides further context.

The company's market capitalization was £0.12m as of a previous close. The company delisted from the London Stock Exchange in July 2023. The non-prime consumer credit market in the U.S. alone reached $1.2 trillion in 2024, indicating a significant and growing demand.

Strategic Initiatives and Market Dynamics

The company is exploring international expansion and using AI to improve lending processes. This includes assessing non-standard finance options for bad credit. Leadership is focused on strengthening the business. The company's strategy involves adapting to market conditions and catering to its target demographic.

- Non-standard finance companies assess risk through various methods, including credit scores, income verification, and employment history.

- Interest rates for subprime loans are typically higher than those for prime loans, reflecting the increased risk.

- The eligibility criteria for alternative loans often include factors like income, employment status, and credit history.

- Understanding the difference between non-standard and traditional loans is crucial for borrowers seeking financial solutions.

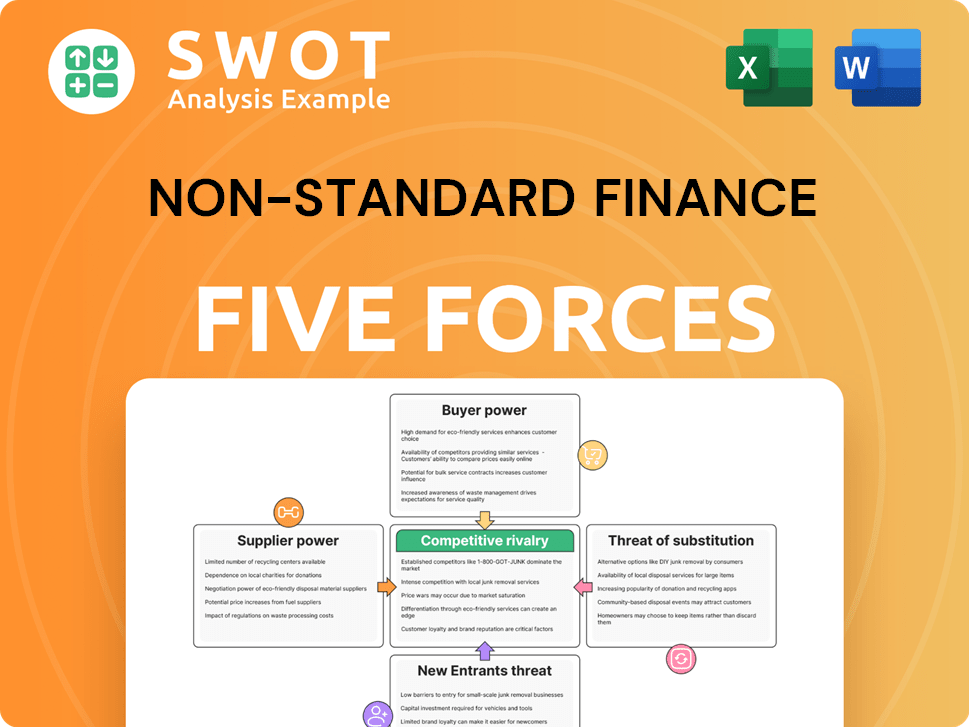

Non-Standard Finance Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Non-Standard Finance Company?

- What is Competitive Landscape of Non-Standard Finance Company?

- What is Growth Strategy and Future Prospects of Non-Standard Finance Company?

- What is Sales and Marketing Strategy of Non-Standard Finance Company?

- What is Brief History of Non-Standard Finance Company?

- Who Owns Non-Standard Finance Company?

- What is Customer Demographics and Target Market of Non-Standard Finance Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.