Non-Standard Finance Bundle

Can Non-Standard Finance Navigate the Future of Finance?

Non-Standard Finance (NSF), a UK-based player in the alternative lending space, has historically served underserved consumers with products like guarantor loans. Founded in 2014, the company rapidly expanded through acquisitions, establishing itself as a key competitor. But, what does the future hold for this non-standard finance company?

Facing operational and regulatory challenges, including the impact of the pandemic and issues with historical lending practices, Non-Standard Finance must now chart a course for sustainable growth. The company's Non-Standard Finance SWOT Analysis provides critical insights into its strengths, weaknesses, opportunities, and threats. With the financial services industry undergoing significant transformation, the company's growth strategy and future prospects are crucial for its survival and success in the evolving FinTech landscape.

How Is Non-Standard Finance Expanding Its Reach?

Expansion initiatives for a company like this are complex, especially given the recent developments. The historical approach involved acquisitions, aiming to build a portfolio of consumer credit businesses. However, the current landscape points towards a strategic shift.

Public information indicates a focus on winding down the parent company, with shares temporarily suspended as of July 2023. This suggests a period of contraction rather than immediate expansion. Nevertheless, the non-standard finance sector is dynamic, and future strategies could evolve.

The UK financial market's broader trends offer some context. Consumer credit demand is expected to remain robust, even if growth eases to around 6.5% net in both 2025 and 2026. This overall market health could create opportunities for adaptable non-standard finance providers, focusing on Brief History of Non-Standard Finance.

Historically, the company's growth strategy centered on acquiring consumer credit companies. This approach aimed to expand its market presence and diversify its portfolio. The focus on acquisitions was a key element of its initial business model.

The non-standard finance sector requires constant adaptation to market changes. The company's ability to respond to shifts in consumer demand and regulatory changes is crucial. Flexibility in its business model is essential for long-term viability.

Future growth plans would likely necessitate a capital raise. Securing additional funding is vital for any expansion initiatives or strategic repositioning. The ability to attract investment will be a key factor.

The asset-based lending market's expansion could present an opportunity. This sector is experiencing growth, potentially offering a viable avenue for diversification. Considering this area could be a strategic move.

Key Considerations for Future Growth

The company faces several challenges and opportunities. The need to navigate the current market conditions while also considering the future of the non-standard finance market is critical. Strategic decisions will shape its future.

- Regulatory Compliance: Navigating evolving financial regulations is essential.

- Market Trends: Adapting to changing consumer credit demands is crucial.

- Capital Management: Securing and managing capital efficiently will be key.

- Strategic Partnerships: Forming alliances could provide growth opportunities.

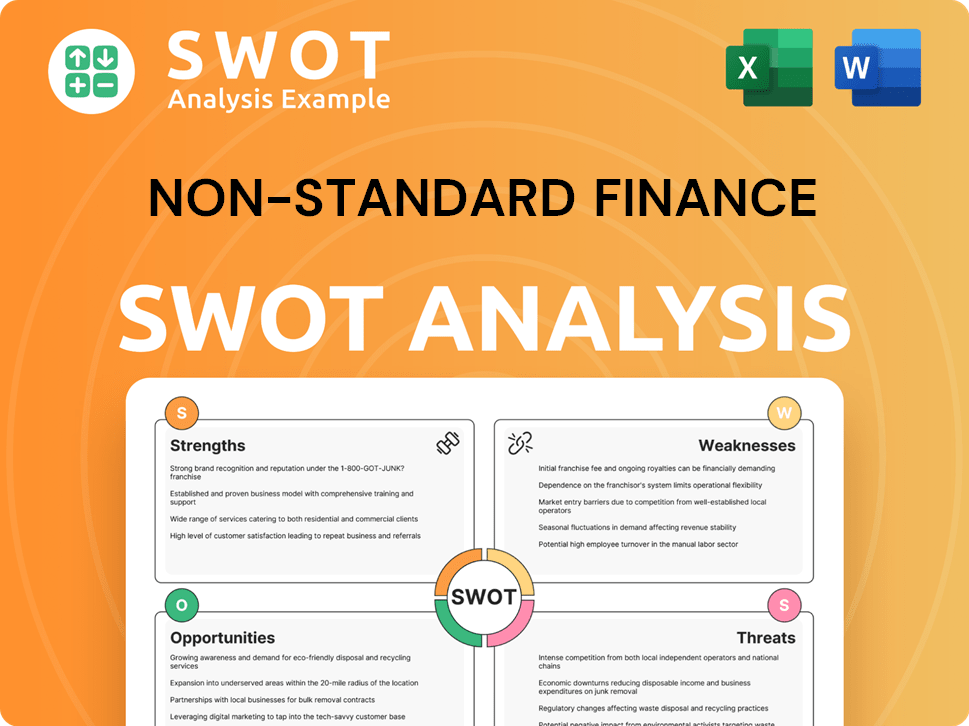

Non-Standard Finance SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Non-Standard Finance Invest in Innovation?

For Non-Standard Finance (NSF), a robust innovation and technology strategy is essential for navigating the evolving financial landscape and achieving sustained Growth Strategy. While specific details on internal R&D efforts or external collaborations might not be publicly available, the broader trends in the FinTech sector offer insights into the strategic direction NSF is likely taking. The company's approach to technology is crucial for staying competitive and meeting the changing demands of its customer base.

The financial services sector is rapidly adopting technologies like artificial intelligence (AI), automation, and digital platforms. These advancements are not just about streamlining processes; they also enhance customer experience and improve risk management. NSF's ability to integrate these technologies will significantly impact its operational efficiency and market positioning, influencing its Future Prospects.

NSF is strategically positioning itself to leverage technological advancements within the financial sector. The appointment of Dr. Richard Leaver, an AI expert, as a Board Adviser in October 2024, with a further appointment as a Non-Executive Director in January 2025, signals a commitment to integrating AI expertise at a high level. This move indicates a strategic intent to harness AI capabilities to improve decision-making processes and enhance customer service.

AI Integration

AI is a key area of focus in the FinTech industry, with applications ranging from automating processes to supporting financial education. Companies are using AI to improve risk management and personalize banking experiences. NSF's strategic move to bring in AI expertise highlights its commitment to this technology.

Regulatory Compliance

The financial services sector is facing increased regulatory scrutiny, particularly around AI decision-making, cybersecurity, and identity verification. NSF must ensure its technological implementations comply with these evolving regulations. Remaining compliant is crucial for maintaining operational integrity.

Automation and Efficiency

Companies are exploring advanced automation and AI to streamline credit application processes. This can lead to greater efficiency and reduced costs. By adopting these technologies, NSF can improve its operational effectiveness and enhance customer experience.

Open Banking

The industry is moving towards a fully interoperable financial ecosystem where users can access real-time financial insights and automated budgeting tools through a single interface, driven by open banking initiatives. This trend presents opportunities for NSF to improve its service offerings.

Digital Platforms

Embracing digital platforms is crucial for non-standard finance companies to improve efficiency and enhance customer experience. Digital platforms offer a more accessible and user-friendly approach to financial services. NSF can enhance its competitiveness by adopting these digital platforms.

Customer Experience

Technological advancements can significantly enhance customer experience by providing personalized services and real-time financial insights. Improved customer experience can lead to increased customer loyalty and satisfaction. NSF can improve customer satisfaction by adopting new technologies.

In the context of Alternative Lending, the adoption of AI-driven credit decisioning and digital platforms is particularly important. These technologies can improve efficiency, enhance customer experience, and maintain competitiveness. For instance, in 2024, the global FinTech market was valued at approximately $111.2 billion, with projections indicating substantial growth. The integration of AI in credit scoring could lead to a reduction in default rates and improved accuracy in risk assessment. To learn more about the company's strategic direction, you can read this article about Non-Standard Finance.

Key Technological Strategies

NSF's technology strategy will likely involve a combination of in-house development, partnerships, and the adoption of off-the-shelf solutions. Key areas of focus will likely include:

- AI-Driven Credit Decisioning: Implementing AI to automate and improve the accuracy of credit assessments, potentially reducing default rates.

- Digital Platforms: Developing or adopting user-friendly digital platforms to enhance the customer experience and streamline the application process.

- Cybersecurity: Investing in robust cybersecurity measures to protect customer data and maintain trust.

- Data Analytics: Utilizing data analytics to gain insights into customer behavior, market trends, and risk management.

- Open Banking Integration: Exploring opportunities to integrate with open banking initiatives to provide customers with a more comprehensive view of their finances.

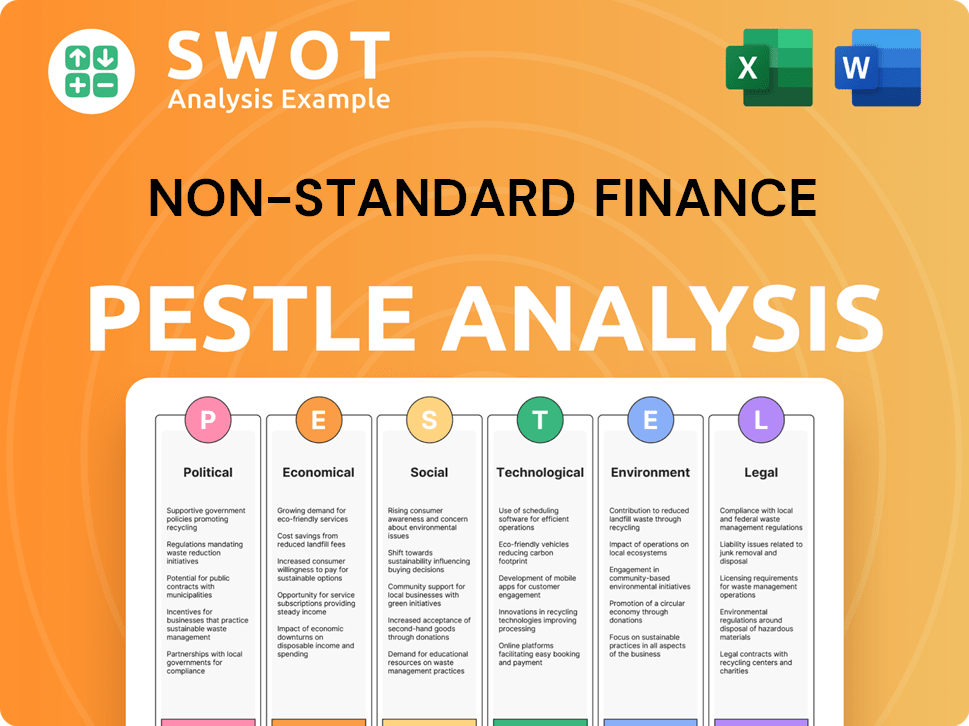

Non-Standard Finance PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Non-Standard Finance’s Growth Forecast?

The financial outlook for Non-Standard Finance reveals a challenging landscape, particularly concerning its growth strategy. The company experienced a pretax loss of £36.2 million in the first half of 2022, a significant increase from the £7.5 million loss the previous year. This downturn was compounded by a 17% decrease in revenue, totaling £56.6 million, primarily due to a contraction in its net loan book. Despite these financial setbacks, the branch-based lending and home credit divisions remained profitable.

The company's future prospects are heavily reliant on securing additional capital. All future growth plans are contingent on completing a capital raise, indicating the critical need for financial restructuring and investment. This dependency underscores the precarious position of the company and its ability to pursue expansion or maintain current operations without external funding.

As of May 2025, analyst predictions suggest a negative trend for the company's shares. There's a potential for a substantial decline in share value, with projections indicating a possible drop from 0.000400 GBX to 0.000001 GBX, which represents a -100.000% change. This bearish outlook signals a high-risk investment environment for the company's shares, reflecting the challenges it faces in the alternative lending market.

Revenue and Profitability

The company's revenue decreased by 17% in the first half of 2022, reaching £56.6 million. Despite this, the branch-based lending and home credit businesses remained profitable, offering some stability in a challenging financial environment.

Capital Raise Dependency

The company's future growth strategy is entirely dependent on a successful capital raise. This highlights the critical need for fresh investment to support any expansion plans or maintain current operations. This is a key factor in understanding the future prospects of Non-Standard Finance.

Share Price Outlook

Analyst predictions as of May 2025 indicate a potentially significant decline in share value. The projected drop from 0.000400 GBX to 0.000001 GBX suggests a high-risk investment scenario and underscores the financial challenges the company faces.

Market Context

While the broader UK bank lending market is forecast to grow by 3.7% in 2025, the company's financial situation requires significant restructuring and capital infusion. This contrasts with the overall market trend and highlights the specific difficulties in the non-standard finance sector.

Strategic Shift

The company ceased offering its 15% IEC bond product in February 2024, shifting its focus to institutional debt funding. This strategic adjustment shows an attempt to secure more stable and sustainable funding sources for future operations and growth.

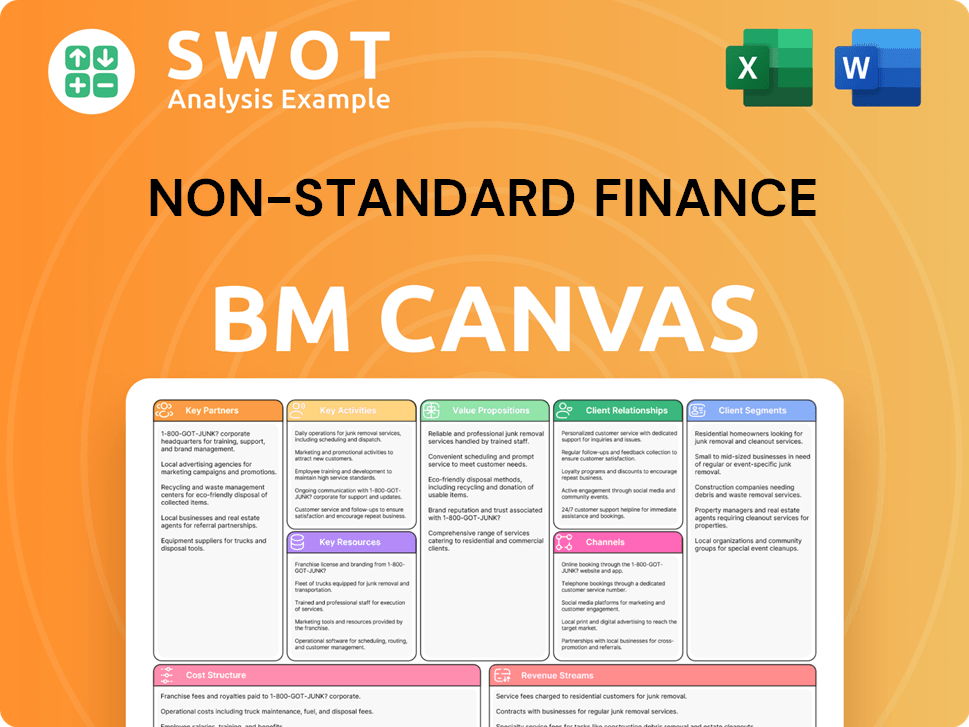

Non-Standard Finance Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Non-Standard Finance’s Growth?

The path for Non-Standard Finance towards growth is fraught with potential pitfalls. The company must navigate a complex landscape of market pressures, regulatory scrutiny, and technological disruption. Understanding and mitigating these risks is crucial for realizing its Growth Strategy and achieving its Future Prospects.

The financial services sector faces increasing regulatory enforcement in areas like AI decision-making, cybersecurity, and identity verification. Financial crime, including fraud and money laundering, continues to be a significant risk, with substantial consequences. These factors, combined with macroeconomic uncertainty, create a challenging environment.

The company's ability to adapt and respond to these challenges will determine its success. This involves responsible lending practices, proactive engagement with regulators, and strategic investments in technology and risk management.

Market Competition

Competition from challenger and specialist banks is intensifying, particularly in lending to smaller businesses. These competitors often leverage FinTech to offer more attractive terms and streamlined services. The Non-Standard Finance sector needs to differentiate itself to maintain market share.

Regulatory Risks

Regulatory changes pose a significant risk, as seen with the FCA review's impact on the guarantor loan division. Ongoing regulatory issues related to historical lending practices can lead to fines, restrictions, and reputational damage. Staying compliant with evolving regulations is essential.

Technological Disruption

Rapid advancements in Financial Innovation, including AI and other FinTech solutions, could disrupt traditional lending models. Companies must invest in technology to remain competitive. The integration of AI also increases the risk of cyberattacks, which are predicted to escalate in 2025.

Cybersecurity Threats

The financial sector faces increasing cyberattacks, which can result in data breaches, financial losses, and reputational damage. The use of AI is predicted to escalate these attacks in 2025. Robust cybersecurity measures, including advanced threat detection and prevention systems, are essential.

Financial Crime

Financial institutions face the ongoing threat of fraud and money laundering, which can result in substantial monetary, reputational, and regulatory consequences. Effective anti-fraud and anti-money laundering (AML) programs are crucial for mitigating these risks. According to recent reports, financial institutions globally lost approximately $20 billion to fraud in 2024.

Macroeconomic Factors

Geopolitical tensions and macroeconomic factors introduce uncertainty into the market. Economic downturns can increase credit risk and decrease demand for loans. Companies must be prepared to adapt to changing economic conditions and manage their portfolios accordingly.

Non-Standard Finance can mitigate risks through several strategies. Focusing on responsible lending practices is crucial to minimize defaults and regulatory scrutiny. Maintaining good relations with regulators helps in identifying and resolving issues proactively. Investing in robust risk management systems and cybersecurity is essential.

The need for a significant capital raise indicates financial challenges. The ongoing orderly wind-down of the parent company highlights operational obstacles. Addressing these financial and operational issues is critical for the company's long-term viability. The ability to secure funding and streamline operations will be key to its Growth Strategy.

To thrive, Non-Standard Finance needs to adapt its business model. This includes embracing Alternative Lending models and leveraging FinTech to improve efficiency and customer experience. A proactive approach to regulatory compliance and risk management is essential. For more insights, consider reading the Marketing Strategy of Non-Standard Finance.

The Non-Standard Finance market is influenced by several trends. These include the increasing adoption of digital lending platforms and the growing demand for personalized financial products. The sector's future depends on its ability to innovate and adapt to these changes. Market analysis indicates a projected growth rate of approximately 5-7% annually in the Alternative Lending market through 2025.

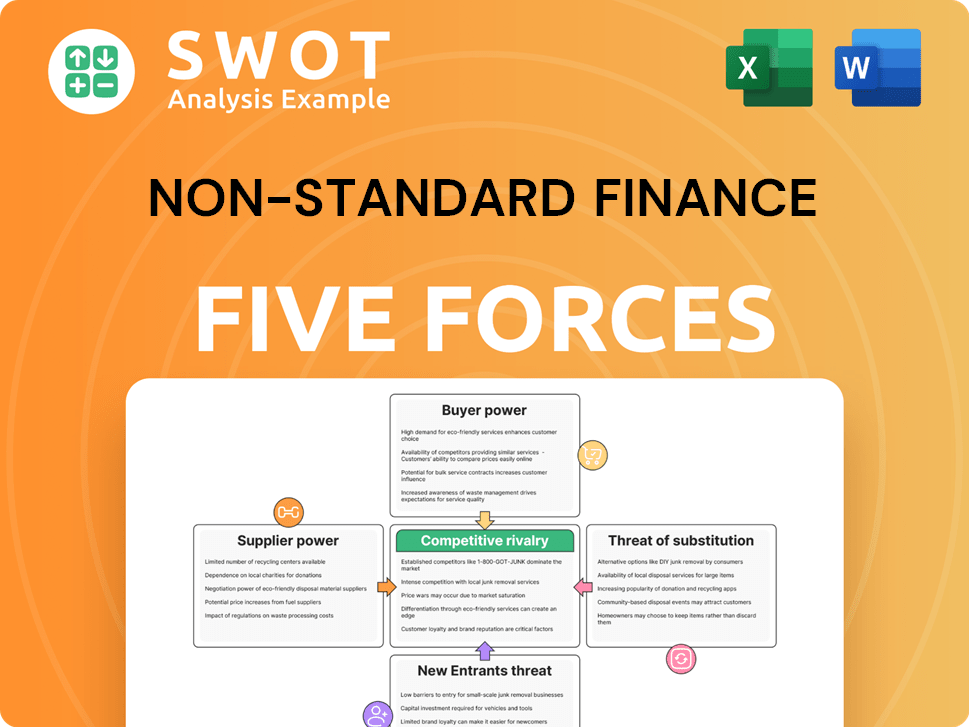

Non-Standard Finance Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Non-Standard Finance Company?

- What is Competitive Landscape of Non-Standard Finance Company?

- How Does Non-Standard Finance Company Work?

- What is Sales and Marketing Strategy of Non-Standard Finance Company?

- What is Brief History of Non-Standard Finance Company?

- Who Owns Non-Standard Finance Company?

- What is Customer Demographics and Target Market of Non-Standard Finance Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.