Fannie Mae Bundle

Who Really Owns Fannie Mae?

Unraveling the question of "Who owns Fannie Mae?" is key to understanding the dynamics of the U.S. housing market. This isn't your typical corporate ownership story; it's a complex interplay of government influence, private investment, and regulatory oversight. Understanding Fannie Mae's ownership structure is crucial for investors and anyone interested in the financial landscape.

Founded as the Federal National Mortgage Association (FNMA) in 1938, Fannie Mae's journey from government-backed entity to a publicly traded company, and back to government conservatorship, offers a fascinating case study in financial regulation. This exploration will dissect the current ownership landscape, including the influence of the U.S. Treasury and private shareholders, and explain Fannie Mae SWOT Analysis. We'll examine who controls Fannie Mae's operations and its pivotal role in the secondary mortgage market, providing insights into who profits from Fannie Mae and its relationship with the US government.

Who Founded Fannie Mae?

The story of Fannie Mae, or the Federal National Mortgage Association (FNMA), begins not with individual entrepreneurs, but with an act of Congress. Established in 1938 under the National Housing Act, its creation was a direct response to the economic challenges of the Great Depression. The primary goal was to stabilize the housing market and provide much-needed liquidity to lenders.

Initially, Fannie Mae operated as a wholly government-owned entity. The U.S. government, through the Federal Housing Administration (FHA) within the Reconstruction Finance Corporation, held complete control. This structure was designed to facilitate the purchase of FHA-insured mortgages, injecting capital into the market and encouraging homeownership.

There were no private shareholders or founders in the early days. The U.S. government served as the sole owner, providing all capital and operational directives. This setup reflected the critical need for federal intervention to address the failures of the private mortgage market, ensuring access to financing for prospective homeowners during a time of economic crisis. For more insights, you can explore a brief history of Fannie Mae.

Government Foundation

Fannie Mae was created by the U.S. Congress in 1938.

It was established under the National Housing Act.

The initial purpose was to support the housing market.

Early Ownership

Fannie Mae was entirely government-owned at the start.

The Federal Housing Administration (FHA) oversaw its operations.

There were no private investors or shareholders initially.

Operational Structure

All capital and directives came from the U.S. government.

The focus was on purchasing FHA-insured mortgages.

This provided liquidity to lenders and stimulated the market.

Economic Context

Fannie Mae was created during the Great Depression.

It aimed to address failures in the private mortgage market.

The goal was to ensure access to housing finance.

No Private Stakeholders

There were no angel investors or private equity.

No vesting schedules or buy-sell clauses applied.

The government was the sole stakeholder.

Government Intervention

Reflected urgent need for federal intervention.

Addressed the failures of the private market.

Ensured access to financing for homeowners.

Key Takeaways

Fannie Mae's initial ownership was entirely governmental, established to support the housing market during the Great Depression.

- Created under the National Housing Act of 1938.

- Operated as a wholly government-owned entity.

- Aimed to stabilize the housing market by purchasing FHA-insured mortgages.

- Reflected the need for federal intervention in the mortgage market.

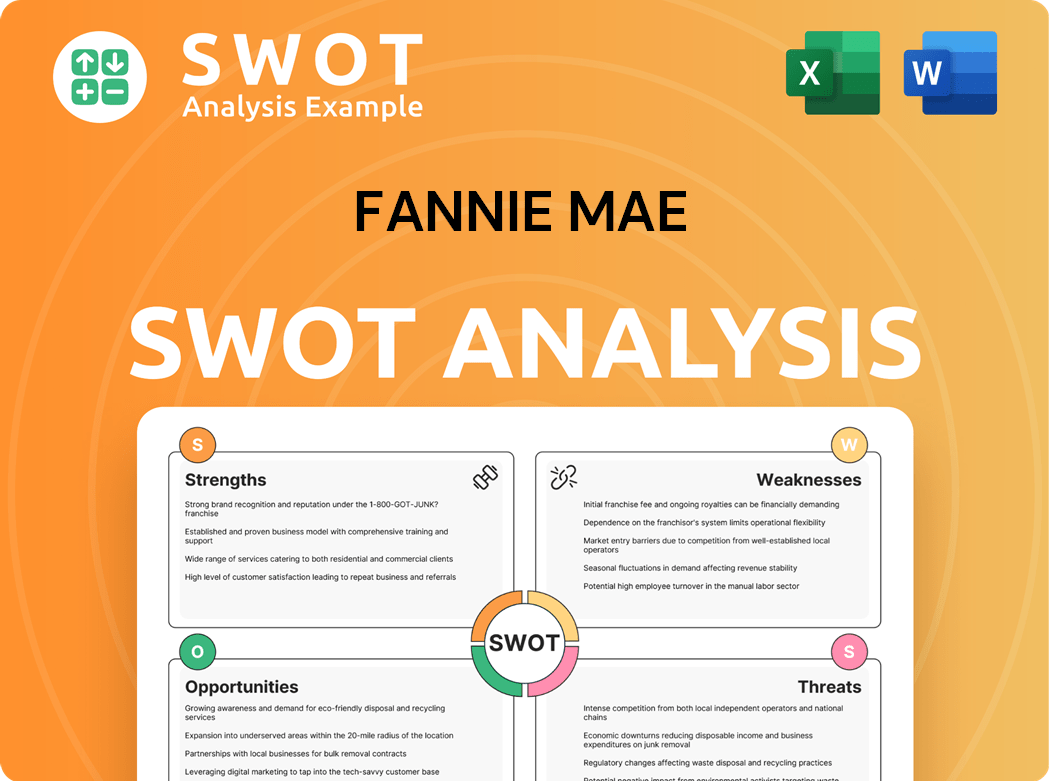

Fannie Mae SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Has Fannie Mae’s Ownership Changed Over Time?

The ownership structure of the Federal National Mortgage Association (FNMA), commonly known as Fannie Mae, has significantly evolved since its establishment. Initially a government agency, it was rechartered in 1968 as a Government-Sponsored Enterprise (GSE), transitioning into a publicly traded company. This shift allowed private investors to purchase shares through an initial public offering (IPO). For many years, Fannie Mae's stock was listed on the New York Stock Exchange, with ownership spread among various institutional investors, mutual funds, and individual shareholders.

The most critical change occurred during the 2008 subprime mortgage crisis. The Federal Housing Finance Agency (FHFA) placed Fannie Mae into conservatorship on September 7, 2008. This action effectively nationalized the company, with the U.S. Treasury providing substantial financial backing via a Senior Preferred Stock Purchase Agreement. Under this agreement, the Treasury received senior preferred stock and warrants, acquiring the right to purchase 79.9% of Fannie Mae's common stock. While common stock continues to trade, the U.S. Treasury now holds the majority of the economic interest and control.

| Timeline | Event | Impact on Ownership |

|---|---|---|

| 1938 | Fannie Mae Established | Government Agency |

| 1968 | Rechartered as GSE | Publicly Traded |

| September 7, 2008 | Conservatorship | U.S. Treasury Dominant Stakeholder |

As of early 2025, Fannie Mae remains in conservatorship, with the U.S. Treasury as the primary stakeholder. Discussions about ending the conservatorship and recapitalizing Fannie Mae are ongoing, but no definitive plan has been fully executed. This situation leaves the government with significant control over Fannie Mae's strategic direction and governance. The long-term goal is to transition Fannie Mae back to a more traditional structure, but the timing and specifics of this transition remain uncertain. The current status reflects the ongoing efforts to stabilize the housing market and ensure the availability of mortgage financing.

Key Takeaways on Fannie Mae Ownership

Fannie Mae's ownership has shifted dramatically from a government agency to a publicly traded company and, finally, to government control.

- The U.S. Treasury currently holds the dominant stake, influencing Fannie Mae's operations.

- The conservatorship has been in place since 2008, with ongoing discussions about its future.

- Understanding the ownership structure is essential for anyone interested in Fannie Mae's role in the housing market.

- The future of Fannie Mae involves potential changes in ownership and regulatory oversight.

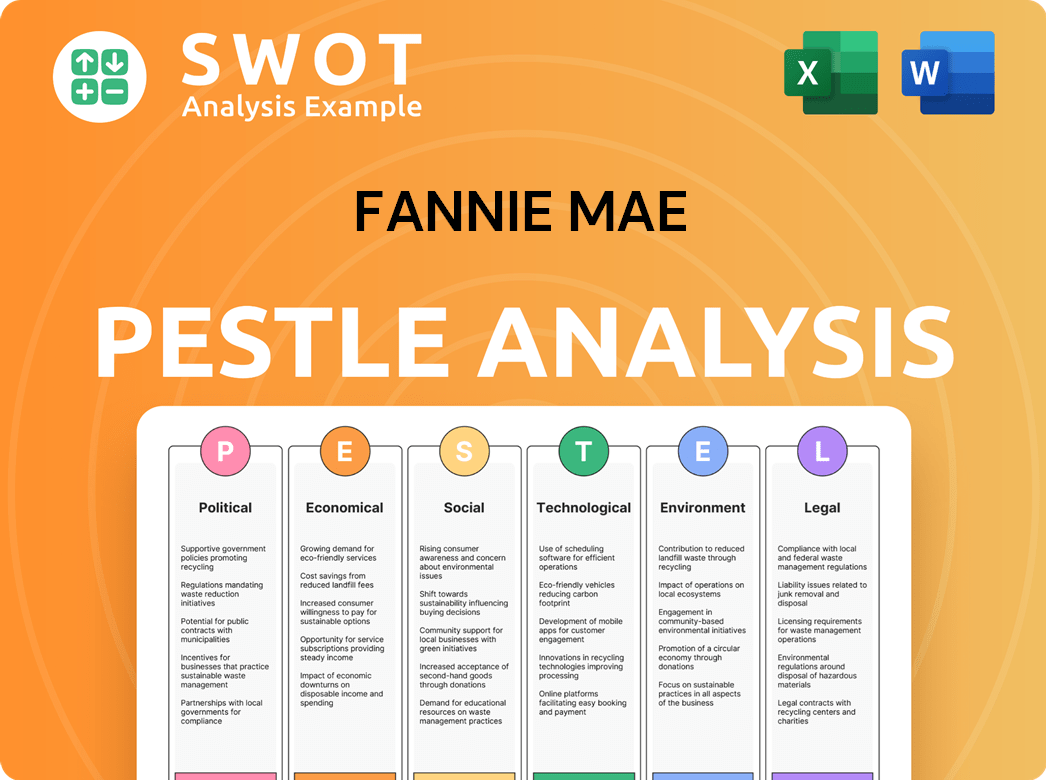

Fannie Mae PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Who Sits on Fannie Mae’s Board?

Understanding the ownership structure of the Federal National Mortgage Association (FNMA), commonly known as Fannie Mae, requires a look at its Board of Directors. Under the conservatorship of the Federal Housing Finance Agency (FHFA), the Board operates with the FHFA holding ultimate authority. The board is composed of a mix of independent directors, along with individuals experienced in the financial and housing sectors. As of the latest available public information, the board includes members like Michael J. Heid, who serves as Chairman, and other directors with expertise in finance, risk management, and housing policy. These directors are appointed with the FHFA's approval, underscoring the government's significant influence over the company's governance.

The composition and responsibilities of the Board are critical, especially given the company's role as a Government-Sponsored Enterprise (GSE). The board's decisions are subject to the FHFA's oversight, which ensures adherence to regulatory requirements and the conservatorship's objectives. This structure highlights the unique position of Fannie Mae, balancing its operational needs with the government's broader goals for the housing market and financial stability. The board's actions are closely monitored, reflecting the public interest and the significant financial stakes involved.

| Board Member | Title | Relevant Experience |

|---|---|---|

| Michael J. Heid | Chairman | Experience in finance, risk management, and housing policy |

| (Other Directors) | Director | Experience in finance, risk management, and housing policy |

| (Other Directors) | Director | Experience in finance, risk management, and housing policy |

The voting power within Fannie Mae is largely influenced by the U.S. Treasury's senior preferred stock and warrants. These instruments give the Treasury substantial economic interest and control, which diminishes the voting power of common shareholders on major strategic decisions. Common shareholders can still vote on specific corporate matters, but their influence is limited compared to the FHFA's authority and the Treasury's financial stake. Ongoing debates and legal challenges from common shareholders seeking to end the conservatorship and reclaim equity value highlight the governance challenges associated with a GSE under government control. The relationship between Fannie Mae and the U.S. government remains a key aspect of its operations and future.

Key Takeaways on Fannie Mae Ownership

Fannie Mae's Board of Directors operates under the FHFA's authority, reflecting government oversight.

- The U.S. Treasury's financial stake significantly impacts voting power.

- Common shareholders' influence is limited due to the conservatorship.

- Fannie Mae's governance is shaped by its status as a GSE.

- Ongoing legal and financial debates continue to influence the company's direction.

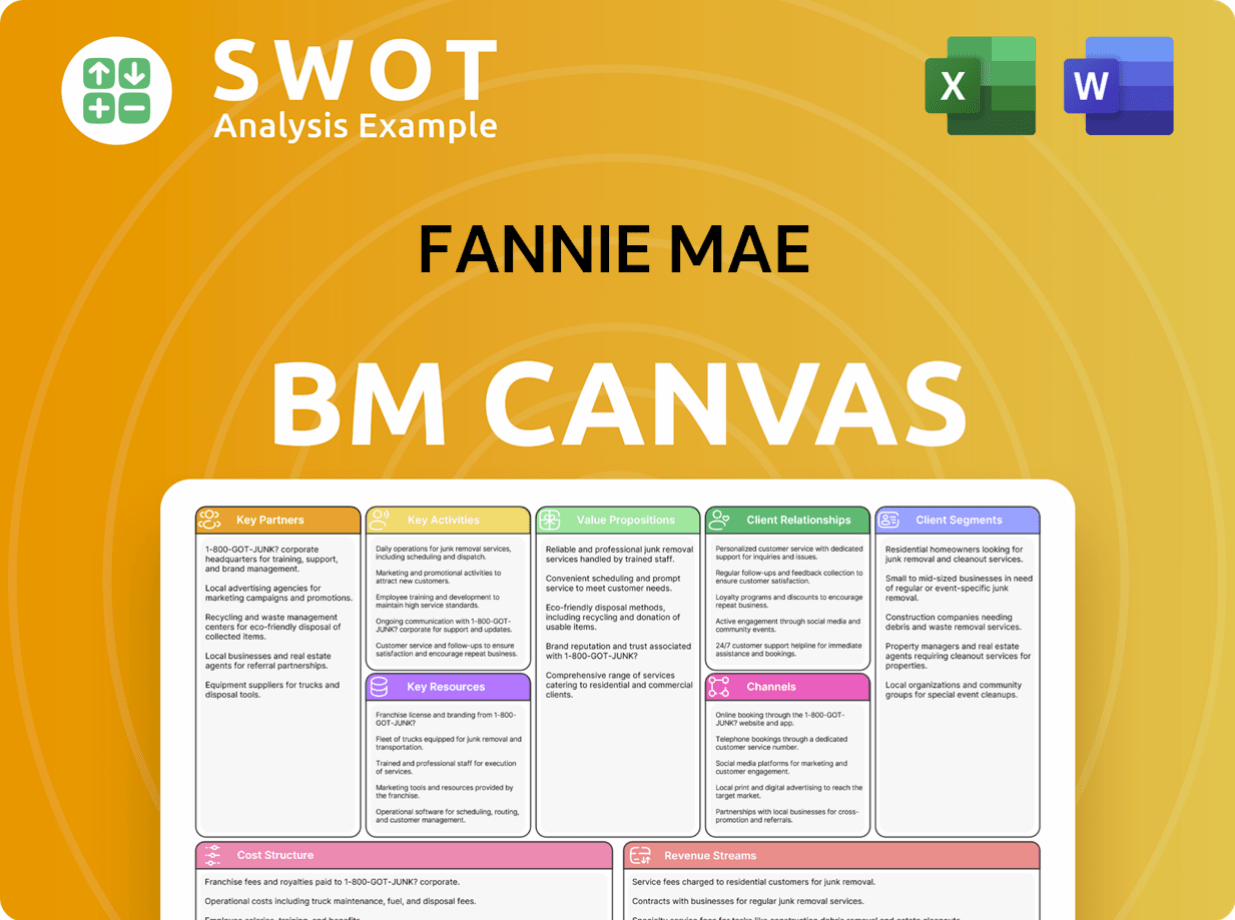

Fannie Mae Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Recent Changes Have Shaped Fannie Mae’s Ownership Landscape?

In the past 3-5 years, the ownership of Fannie Mae, also known as the Federal National Mortgage Association (FNMA), has been largely shaped by its ongoing conservatorship. The U.S. Treasury remains the primary economic beneficiary and controller. Discussions around recapitalization and ending the conservatorship have been ongoing, with proposals emerging from Congress and the Treasury, but a definitive path out of conservatorship remains elusive as of early 2025. This situation has kept the ownership structure relatively stable, with the government holding the majority of the economic interest.

The focus for Fannie Mae is on governmental policy and regulatory decisions regarding its future. Public statements from the company and analysts consistently highlight the need for a long-term resolution to the conservatorship. Such a resolution would fundamentally alter its ownership structure, potentially returning it to a more traditional publicly traded model. This shift could allow private capital to bear more risk, leading to a significant change in its stakeholder base. For further insights, consider exploring the Competitors Landscape of Fannie Mae.

| Ownership Aspect | Details | Status (Early 2025) |

|---|---|---|

| Conservatorship Status | Under the control of the Federal Housing Finance Agency (FHFA). | Ongoing; no definitive exit plan. |

| U.S. Treasury's Role | Primary economic beneficiary due to preferred stock agreement. | Dominant; receives a significant portion of profits. |

| Publicly Traded Shares | Common stock is traded, but the government controls the economic benefits. | Limited influence of common shareholders due to conservatorship. |

The continued conservatorship has meant that traditional ownership trends, such as increased institutional ownership, are less relevant. Instead, the focus remains on the government's actions and policy decisions that will shape Fannie Mae's future ownership structure.

The U.S. government's significant stake has led to a relatively stable ownership profile. This stability is primarily due to the ongoing conservatorship.

The future of Fannie Mae's ownership depends on the resolution of the conservatorship. This resolution could lead to a significant shift in its stakeholder base.

The primary players are the U.S. Treasury, the FHFA, and common shareholders. The government's role is the most significant.

The conservatorship has limited the influence of common shareholders. It has also made the U.S. government the primary beneficiary.

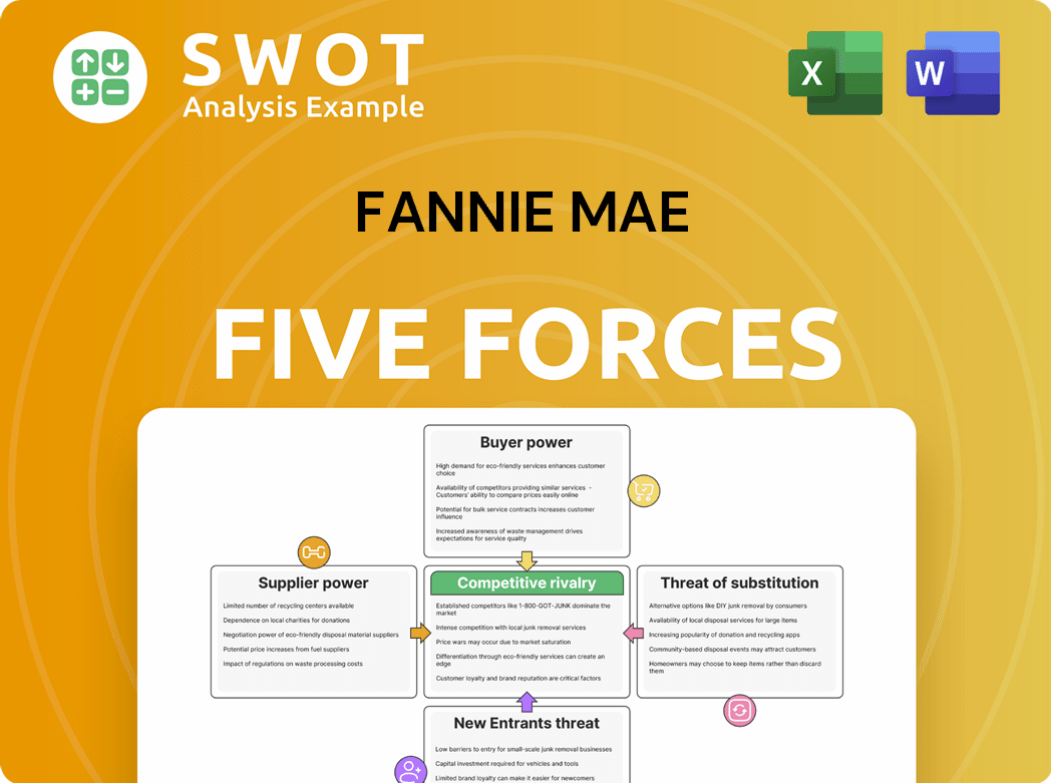

Fannie Mae Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Fannie Mae Company?

- What is Competitive Landscape of Fannie Mae Company?

- What is Growth Strategy and Future Prospects of Fannie Mae Company?

- How Does Fannie Mae Company Work?

- What is Sales and Marketing Strategy of Fannie Mae Company?

- What is Brief History of Fannie Mae Company?

- What is Customer Demographics and Target Market of Fannie Mae Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.