Fannie Mae Bundle

Who Competes with Fannie Mae in Today's Housing Market?

Fannie Mae, a titan in the U.S. housing finance system, plays a crucial role in the mortgage industry by injecting liquidity into the market. Its historical significance, stemming from its creation during the Great Depression, underscores its enduring impact on homeownership. Understanding the Fannie Mae SWOT Analysis is crucial to grasp its position.

Delving into the Fannie Mae competitive landscape is essential for investors and analysts alike. This analysis allows for a deeper understanding of its rivals, market share, and strategic positioning within the housing market. Examining Fannie Mae's role in the mortgage market and its strategies will provide valuable insights into its financial performance and future outlook. Furthermore, a thorough Fannie Mae market analysis will reveal how it navigates the complexities of the government-sponsored enterprise model.

Where Does Fannie Mae’ Stand in the Current Market?

Fannie Mae holds a significant market position in the U.S. secondary mortgage market. It functions as a crucial source of liquidity for lenders. Understanding the Fannie Mae competitive landscape is essential for anyone involved in the mortgage industry.

The company, along with Freddie Mac, effectively guarantees a large portion of new conforming mortgages in the United States. In 2023, Fannie Mae and Freddie Mac together guaranteed approximately 70% of all single-family mortgage originations. This dominance highlights its critical role in the housing market.

Fannie Mae's core operations involve purchasing conventional, conforming mortgages from lenders. These mortgages are then securitized into mortgage-backed securities (MBS) and sold to investors. Its geographic presence spans the entire United States, making it a nationwide entity.

Fannie Mae and Freddie Mac collectively guarantee a substantial portion of U.S. mortgages. Their consistent presence ensures stability in the mortgage market. Analyzing Fannie Mae market share analysis is key to understanding its influence.

Fannie Mae's primary customers include mortgage lenders, such as banks and credit unions, and institutional investors. These investors purchase the mortgage-backed securities. This structure supports the flow of capital in the mortgage market.

As of the first quarter of 2024, Fannie Mae reported a net income of $2.7 billion, demonstrating its strong financial health. This financial stability is a key factor in its market position. This data is crucial for assessing Fannie Mae's financial performance compared to rivals.

Fannie Mae operates under significant regulatory oversight, particularly since the 2008 financial crisis. This oversight impacts its operational strategies and risk management. Understanding the Fannie Mae's regulatory environment and its impact is important.

Key Market Dynamics

Fannie Mae's positioning has remained consistent in its core mission of providing liquidity, though its operational strategies have adapted to market shifts and regulatory changes. The impact of economic conditions on Fannie Mae is significant.

- Fannie Mae's role in the mortgage market is critical for providing stability.

- Its influence on mortgage rates is substantial, affecting the broader economy.

- The company's risk management practices are constantly evolving.

- Growth Strategy of Fannie Mae provides further insights.

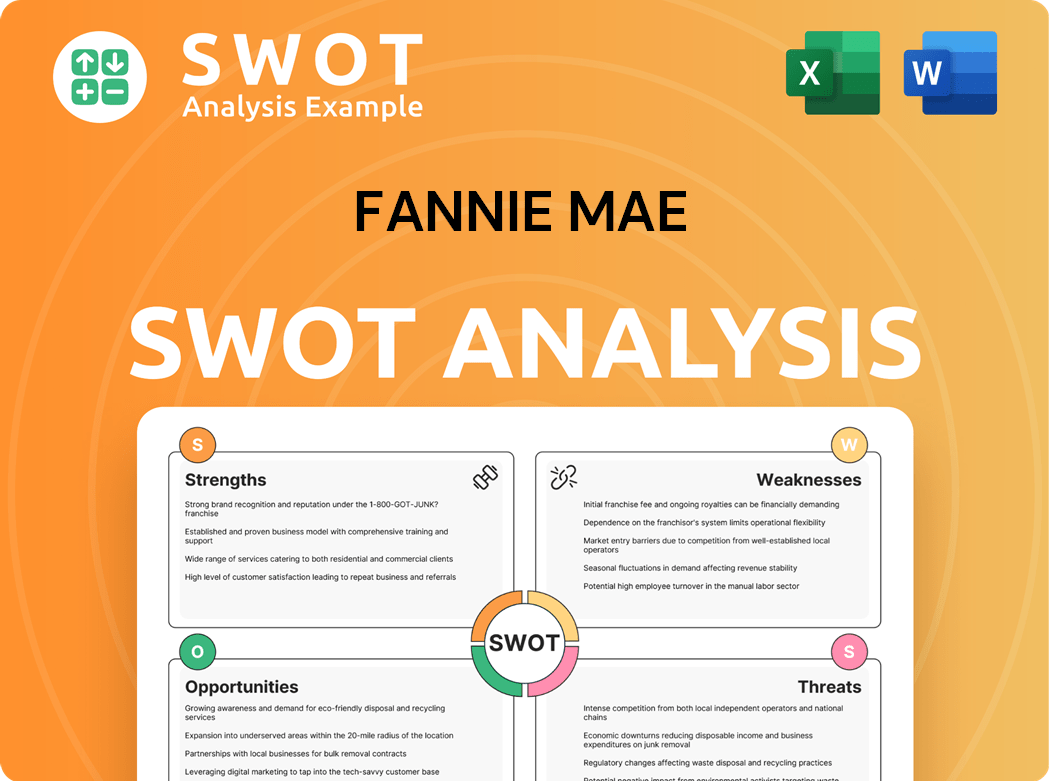

Fannie Mae SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

Who Are the Main Competitors Challenging Fannie Mae?

Understanding the Fannie Mae competitive landscape is crucial for anyone involved in the mortgage industry and housing market. As a government-sponsored enterprise (GSE), its position is unique. This article provides a detailed Fannie Mae market analysis, focusing on its key rivals and the dynamics shaping its operations. To fully grasp its operations, consider exploring the Revenue Streams & Business Model of Fannie Mae.

Fannie Mae's primary business involves purchasing mortgages from lenders, packaging them into mortgage-backed securities (MBS), and guaranteeing these securities. This activity supports liquidity in the mortgage market, ensuring that lenders have funds to offer new mortgages. The competitive environment for Fannie Mae is shaped by its GSE status and the regulatory framework within which it operates.

The competitive dynamics between Fannie Mae and other entities are influenced by several factors, including economic conditions, regulatory directives, and technological advancements. These elements affect Fannie Mae's strategies and its ability to maintain its position in the market.

Direct Competitors: Freddie Mac

Fannie Mae's main competitors in 2024 include Freddie Mac, the other major GSE. They function similarly by purchasing mortgages and securitizing them. The duopoly structure means both entities have a substantial impact on the Fannie Mae market share analysis.

Indirect Competitors: Private Label Securitizers

Private label securitizers, though less active since the 2008 financial crisis, historically competed by securitizing non-conforming mortgages. Their market share is smaller compared to Fannie Mae and Freddie Mac. This sector's activity is influenced by economic cycles and regulatory changes.

Indirect Competitors: Financial Institutions

Large financial institutions that retain mortgages on their balance sheets also indirectly compete. These institutions choose to hold mortgages rather than selling them to the secondary market. Their decisions affect the volume of mortgages available for Fannie Mae to purchase.

Complementary Entities: Ginnie Mae

Ginnie Mae guarantees MBS backed by FHA, VA, and USDA loans, playing a complementary role. While not directly competitive in the conventional mortgage market, Ginnie Mae supports different segments of the housing market. Their activities influence overall market dynamics.

Emerging Players: Fintech Lenders

Fintech lenders are emerging players that primarily compete with primary mortgage lenders. These lenders can influence the types and volume of mortgages available for Fannie Mae to purchase. Technological innovations in mortgage origination affect the competitive landscape.

Regulatory and Economic Influences

Fannie Mae's competitive dynamics are significantly shaped by regulatory directives and economic conditions. These factors influence Fannie Mae's strategies and its ability to manage risk. Changes in interest rates and housing demand also play a role.

Key Competitive Factors

Several factors influence Fannie Mae's competitive position, including its ability to manage risk, promote housing affordability, and adapt to technological changes. Understanding these factors provides insight into Fannie Mae's strategies and performance.

- Fannie Mae's ability to maintain its market share depends on its risk management practices.

- Regulatory changes and economic conditions significantly impact Fannie Mae's operations.

- Technological advancements in mortgage origination and servicing also influence its competitive environment.

- The relationship between Fannie Mae and Freddie Mac is a central aspect of the Fannie Mae competitive landscape.

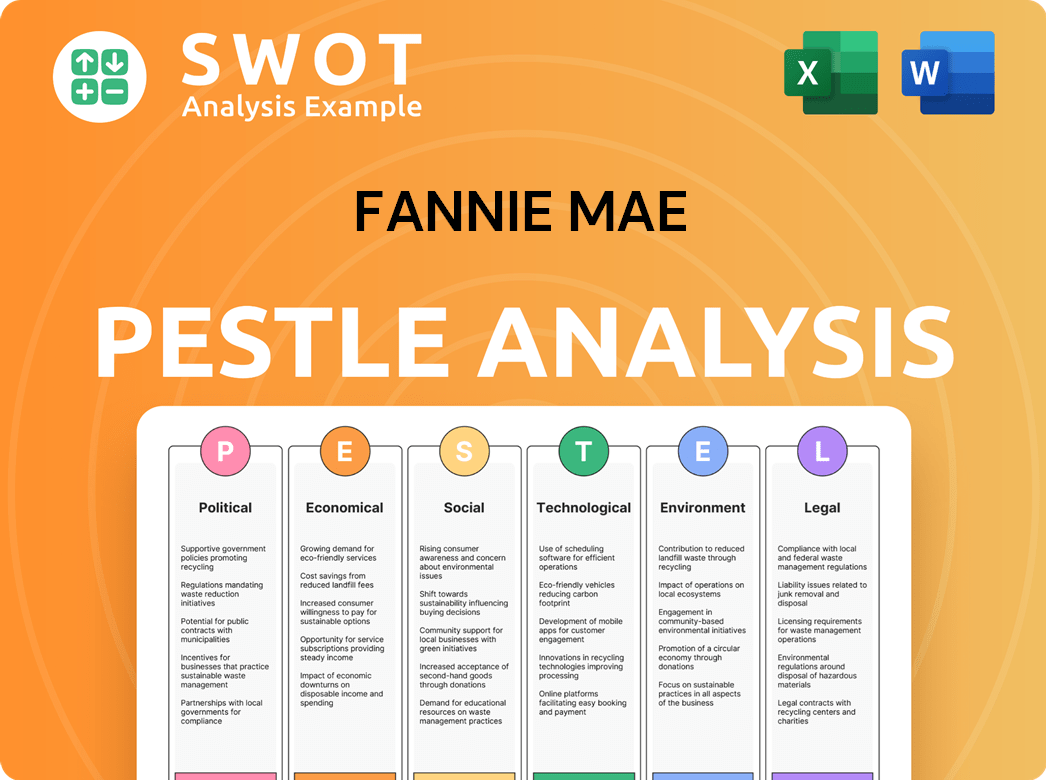

Fannie Mae PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Gives Fannie Mae a Competitive Edge Over Its Rivals?

Understanding the Fannie Mae competitive landscape requires a deep dive into its core strengths. As a government-sponsored enterprise (GSE), it holds a unique position in the mortgage industry, influencing the housing market significantly. This GSE status provides several key advantages that shape its interactions with Fannie Mae competitors and the broader financial ecosystem.

Fannie Mae's market analysis reveals that its competitive edge stems from its ability to secure funding at lower costs than private entities. This cost advantage allows it to offer competitive pricing to lenders. Furthermore, its vast scale and established infrastructure provide significant economies of scale in mortgage securitization and servicing, ensuring a consistent flow of mortgage originations through its extensive distribution network.

Fannie Mae's role in the mortgage market is crucial, and its competitive advantages have evolved over time, particularly with enhanced regulatory oversight post-2008, leading to even more robust risk management and capital requirements, reinforcing its stability. This stability is essential for maintaining liquidity in the mortgage market and supporting a consistent flow of capital to lenders.

Fannie Mae's GSE status allows it to borrow at lower interest rates. This translates to reduced funding costs for the mortgages it purchases. In 2024, this advantage helped it maintain competitive pricing, supporting its role in the mortgage market and influencing mortgage rates.

The company's vast scale provides significant economies of scale in mortgage securitization and servicing. This efficiency helps manage costs and maintain profitability. Its extensive distribution network, encompassing thousands of lenders across the country, ensures a consistent flow of mortgage originations.

Fannie Mae's proprietary technology and sophisticated risk management models are developed over decades. These tools are essential for assessing and managing the credit risk of millions of mortgages. This robust risk management is critical for maintaining stability and investor confidence.

The company's brand equity is exceptionally strong within the financial industry, signifying stability and reliability. Its long-standing relationships with lenders and its deep understanding of the housing market further solidify its position. This trust is essential for maintaining its market share and attracting investors.

Key Advantages and Market Dynamics

Fannie Mae's competitive advantages and disadvantages are shaped by its unique position as a GSE. Its advantages include lower funding costs, economies of scale, and strong brand recognition. However, it also faces regulatory scrutiny and the potential for political influence.

- Lower Funding Costs: The implicit government backing allows Fannie Mae to borrow at lower rates, giving it a cost advantage.

- Economies of Scale: Its size enables efficient mortgage securitization and servicing.

- Strong Relationships: Long-standing relationships with lenders and a deep understanding of the housing market.

- Regulatory Scrutiny: Subject to significant regulatory oversight and capital requirements.

- Market Influence: Influences mortgage rates and the availability of credit in the housing market.

For a deeper understanding of the target market, consider reading about the Target Market of Fannie Mae. The Fannie Mae vs. Freddie Mac comparison highlights similar advantages and disadvantages, as both are GSEs. Understanding Fannie Mae's main competitors in 2024 and their strategies is essential for a comprehensive Fannie Mae market share analysis. The impact of economic conditions on Fannie Mae, along with its strategies to compete with other lenders, are critical factors. Fannie Mae's financial performance compared to rivals and its regulatory environment and its impact are also key considerations. Fannie Mae's influence on mortgage rates and its competitive landscape in the US are central to its operations. Finally, examining Fannie Mae's risk management practices and its technology and innovation provides insights into its future outlook in the mortgage industry.

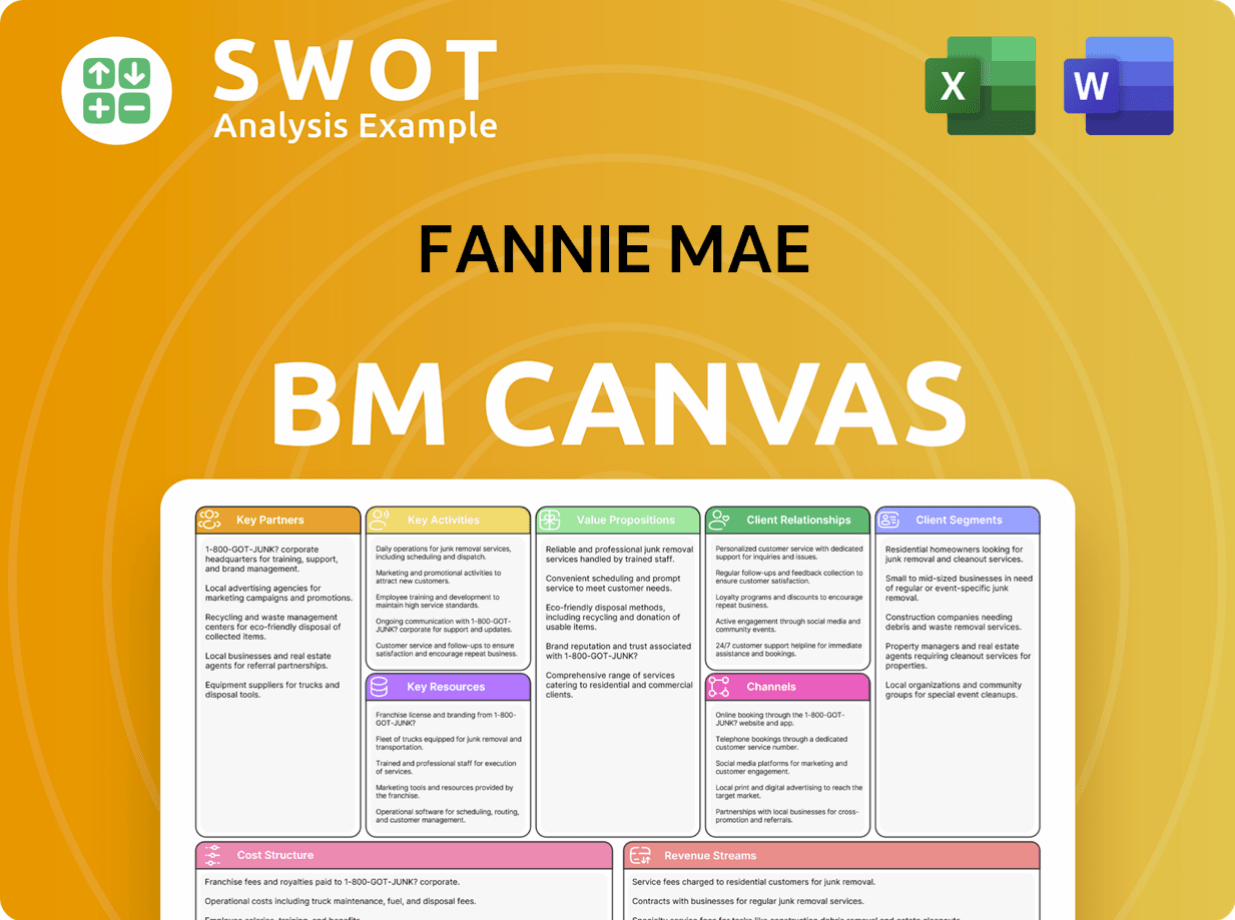

Fannie Mae Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Industry Trends Are Reshaping Fannie Mae’s Competitive Landscape?

The Fannie Mae competitive landscape is significantly influenced by industry trends, regulatory changes, and shifts in consumer behavior. The mortgage industry is dynamic, with technological advancements and economic fluctuations constantly reshaping the competitive dynamics. Understanding these factors is crucial for analyzing Fannie Mae's market share analysis and its strategic positioning within the housing market.

Key risks include changes in government sponsorship and potential downturns in the housing market. Opportunities lie in expanding affordable housing initiatives and leveraging data analytics. The future outlook for Fannie Mae in the mortgage industry depends on its ability to adapt to technological advancements and navigate regulatory complexities.

Technological advancements, such as AI and automation, are streamlining mortgage processes. Regulatory changes and discussions around GSE reform impact operations. Consumer preferences for digital experiences and affordable housing solutions are also evolving.

A reduction in government sponsorship could impact funding costs. A sustained downturn in the housing market or rising mortgage defaults pose financial risks. Navigating the political environment surrounding its conservatorship remains a key challenge.

Expanding affordable housing initiatives provides growth potential. Exploring new securitization models and leveraging data analytics are also key. These strategies support maintaining market liquidity and managing risk effectively.

Fannie Mae focuses on maintaining market liquidity and managing risk. Supporting a stable and accessible housing finance system is a priority. The company is adapting to technological advancements and regulatory reforms.

Competitive Advantages and Disadvantages

Fannie Mae's competitive advantage lies in its government sponsorship, which lowers funding costs. A potential disadvantage is the risk tied to the housing market's performance and any changes in its government support. The company's ability to adapt to regulatory changes is also crucial.

- Government sponsorship provides a significant advantage in terms of funding costs.

- The company faces risks related to housing market downturns and mortgage defaults.

- Adaptability to regulatory changes is essential for long-term competitiveness.

- Fannie Mae's initiatives support affordable housing, a key strategic focus.

For a deeper understanding of how Fannie Mae approaches its market strategy, consider reading about the Marketing Strategy of Fannie Mae. This analysis of the Fannie Mae competitive landscape reveals its position within the mortgage industry, highlighting the interplay between its role as a government-sponsored enterprise and its response to dynamic housing market conditions. The company's strategies are continually evolving to meet challenges and capitalize on opportunities within this complex environment.

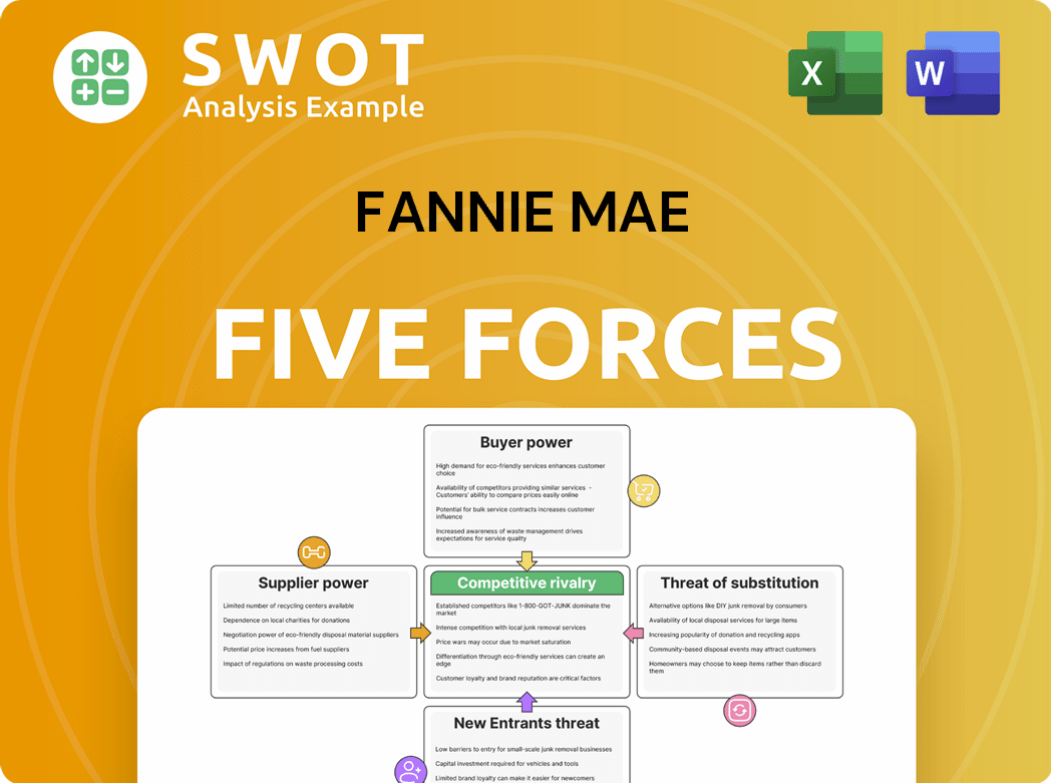

Fannie Mae Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Fannie Mae Company?

- What is Growth Strategy and Future Prospects of Fannie Mae Company?

- How Does Fannie Mae Company Work?

- What is Sales and Marketing Strategy of Fannie Mae Company?

- What is Brief History of Fannie Mae Company?

- Who Owns Fannie Mae Company?

- What is Customer Demographics and Target Market of Fannie Mae Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.