Fannie Mae Bundle

Can Fannie Mae Continue to Shape the Future of Housing?

Established during the Great Depression, Fannie Mae has been a pivotal force in the U.S. housing market, evolving from a government agency to a government-sponsored enterprise. Its mission to provide liquidity to the mortgage industry has profoundly impacted homeownership accessibility and economic stability. Understanding the Fannie Mae SWOT Analysis is crucial for grasping the company's position.

As a cornerstone of the Mortgage Industry, Fannie Mae's Fannie Mae Growth Strategy and Fannie Mae Future Prospects are of paramount importance to anyone involved in Real Estate Finance. This report dives deep into the Fannie Mae Company's strategic initiatives, examining its role in affordable housing and its impact on the US economy. We'll explore the company's long-term goals, challenges and opportunities, and how it plans to navigate the ever-changing landscape of the Housing Market.

How Is Fannie Mae Expanding Its Reach?

Fannie Mae's expansion initiatives are primarily focused on strengthening its core mission within the housing market. The company concentrates on providing liquidity and stability rather than venturing into new commercial markets. A key aspect of its strategy involves supporting affordable housing and optimizing its risk management programs.

In 2024 and 2025, Fannie Mae continues to emphasize affordable housing. This includes expanding its reach to underserved communities and supporting innovative financing solutions. These efforts aim to increase the supply of affordable rental units and expand homeownership opportunities.

Additionally, Fannie Mae is refining its Credit Risk Transfer (CRT) programs. This involves transferring a portion of the credit risk to private investors to reduce taxpayer exposure and bring private capital into the housing finance system. The company is also exploring ways to streamline the mortgage origination process through digitalization and data standardization.

Fannie Mae's commitment to affordable housing is a key component of its expansion strategy. The company supports various programs to increase the availability of affordable rental units and homeownership opportunities. These initiatives often involve partnerships with state housing finance agencies and other affordable housing advocates.

Optimizing CRT programs is another significant aspect of Fannie Mae's expansion. By transferring credit risk to private investors, Fannie Mae reduces its exposure and brings private capital into the housing finance system. This helps maintain robust liquidity in the secondary mortgage market.

Fannie Mae is also focused on streamlining the mortgage origination process. This includes initiatives to improve data quality and automate aspects of the loan lifecycle. These efforts aim to reduce costs and speed up transactions for both lenders and borrowers.

These expansion initiatives contribute to Fannie Mae's role in stabilizing the housing market. By supporting affordable housing, managing risk, and improving operational efficiency, the company aims to ensure access to mortgage financing and promote sustainable homeownership. For more insights, check out the Marketing Strategy of Fannie Mae.

Key Expansion Areas

Fannie Mae's expansion strategy focuses on several key areas to strengthen its position in the mortgage industry and support the housing market. These include initiatives to increase affordable housing, optimize credit risk transfer programs, and improve operational efficiency through digitalization.

- Affordable Housing: Expanding programs to support affordable rental units and homeownership.

- Credit Risk Transfer: Refining CRT programs to reduce taxpayer exposure and attract private capital.

- Digitalization: Streamlining mortgage origination through data standardization and automation.

- Market Share Analysis: Maintaining a significant role in the housing market.

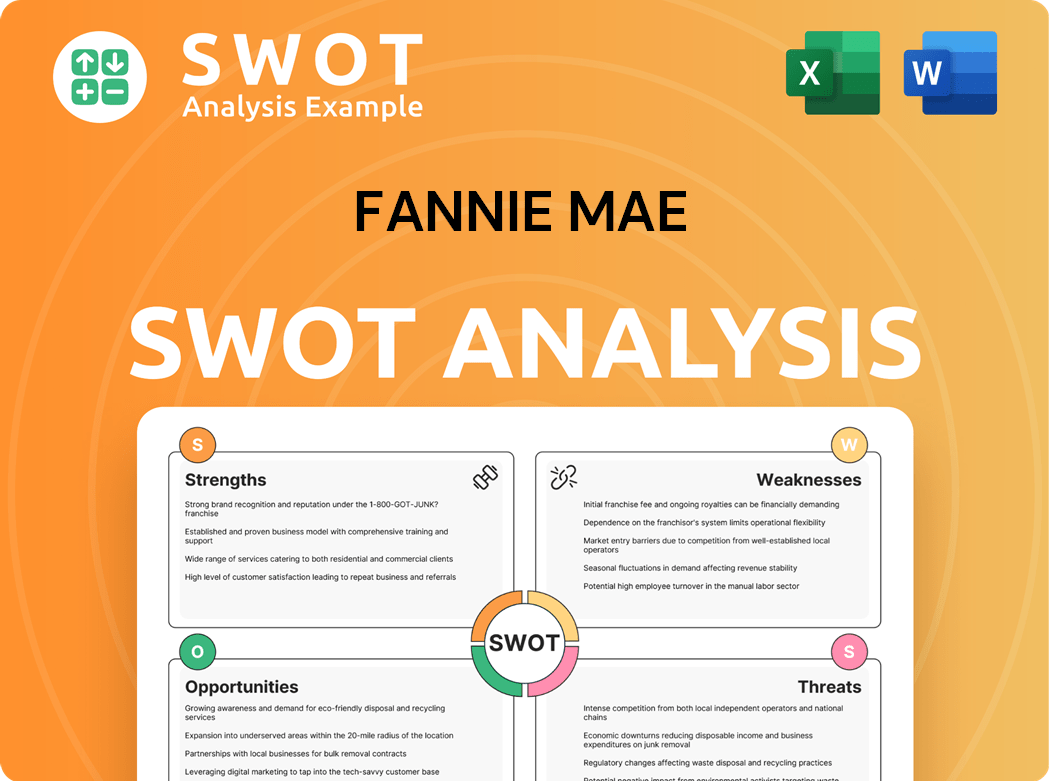

Fannie Mae SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Fannie Mae Invest in Innovation?

Fannie Mae's innovation and technology strategy is crucial for its long-term success within the Mortgage Industry. This strategy focuses on leveraging digital transformation to improve efficiency, manage risk, and enhance the overall mortgage experience for both lenders and borrowers. The company's approach is designed to adapt to the evolving needs of the Housing Market and support its Fannie Mae Growth Strategy.

A key element of Fannie Mae's Future Prospects involves significant investments in data analytics and artificial intelligence (AI). These technologies are being deployed to improve credit risk assessment, detect fraud, and automate various stages of the mortgage lifecycle. By embracing these advancements, Fannie Mae Company aims to streamline operations, reduce costs, and provide more certainty to lenders.

The company is also focused on modernizing its core infrastructure and adopting cloud-based solutions. This transition aims to improve scalability, enhance data security, and enable faster deployment of new tools and services. This modernization supports Fannie Mae's strategic initiatives, ensuring it remains competitive and responsive to market demands.

Data Analytics and AI

Fannie Mae uses AI and machine learning to enhance credit risk assessment and detect fraud. They are developing sophisticated models to predict loan performance and identify market vulnerabilities. This helps in Fannie Mae's risk management practices.

Day 1 Certainty Initiative

The 'Day 1 Certainty' initiative provides upfront certainty on key loan components. This streamlines the underwriting process. It reduces repurchase risk for lenders, supporting Fannie Mae's long-term goals.

Infrastructure Modernization

Fannie Mae is modernizing its core infrastructure and adopting cloud-based solutions. This improves scalability, data security, and speeds up the deployment of new tools. It supports Fannie Mae's technological advancements.

Standardized Data Initiatives

Fannie Mae promotes standardized data across the mortgage industry. This facilitates greater interoperability and efficiency. It simplifies data exchange and reduces operational complexities.

Impact on the Mortgage Process

These technological advancements aim to make the mortgage process more accessible and cost-effective. They contribute to Fannie Mae's growth objectives by increasing transparency for all participants.

Industry Collaboration

Fannie Mae actively collaborates with industry partners. This collaboration is key to developing common data standards and platforms. It streamlines data exchange and reduces operational complexities.

Key Technological Advancements

Fannie Mae's technological advancements are designed to enhance its operational efficiency and improve the overall mortgage experience. These advancements are critical for maintaining its position in the Real Estate Finance sector. The company’s strategic investments in technology are directly linked to its ability to achieve its long-term financial and operational goals, contributing to its Fannie Mae's financial performance analysis.

- AI-Driven Risk Assessment: Fannie Mae utilizes AI and machine learning to refine credit risk models. This allows for more accurate predictions of loan performance, helping to mitigate potential losses.

- Automation of Mortgage Processes: Automation streamlines various stages of the mortgage lifecycle. This reduces manual errors and speeds up the processing time, improving efficiency.

- Cloud-Based Infrastructure: Transitioning to cloud-based solutions enhances scalability and data security. This also enables faster deployment of new services and tools.

- Data Standardization: Initiatives promoting standardized data across the mortgage industry improve interoperability. This reduces operational complexities for lenders and other stakeholders.

- Day 1 Certainty: This initiative provides upfront certainty on key loan components. It streamlines underwriting and reduces the risk for lenders.

For more insights into how Fannie Mae generates revenue, you can read about the Revenue Streams & Business Model of Fannie Mae.

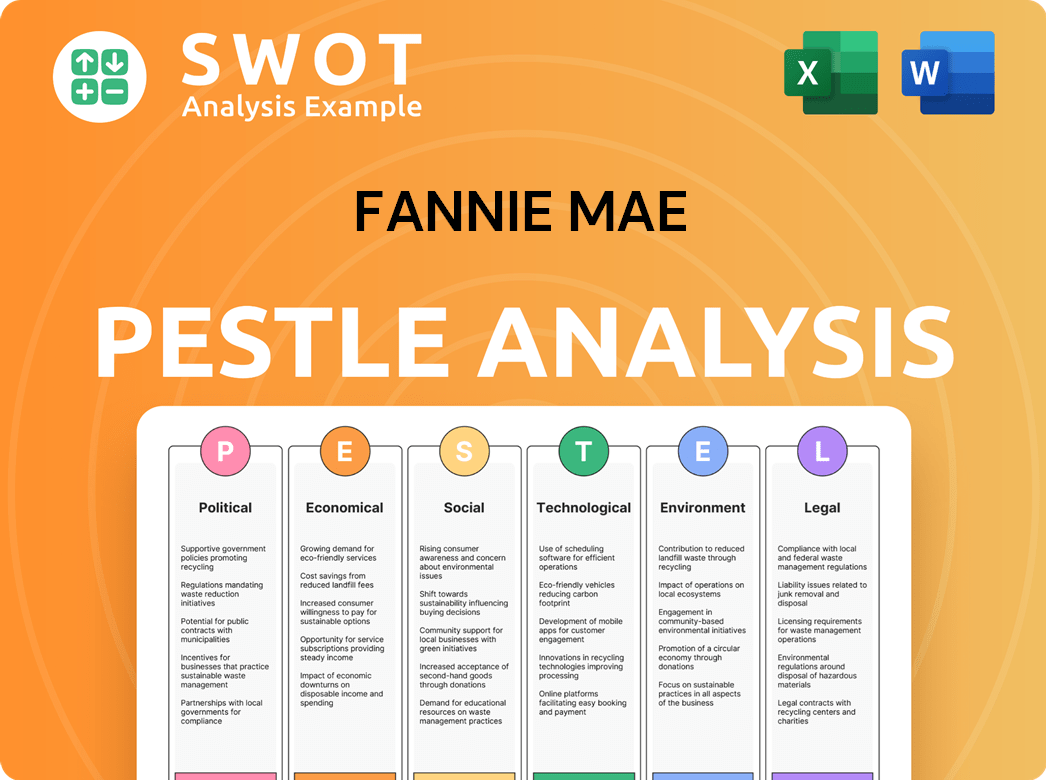

Fannie Mae PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Fannie Mae’s Growth Forecast?

The financial outlook for the Fannie Mae Company in 2024 and beyond is closely tied to the performance of the U.S. housing market and broader economic conditions. As a key player in the mortgage industry, its financial health is significantly influenced by interest rate movements, inflation, and regulatory changes. The company's strategic focus on risk management and capital adequacy is crucial for its long-term stability and its ability to support the housing market.

Fannie Mae's financial performance in 2023 showed resilience, with a net income of $12.5 billion, although slightly down from $12.9 billion in 2022. This reflects the company's ability to navigate market fluctuations while maintaining a strong capital position. The company's total capital stood at $68.6 billion as of December 31, 2023, exceeding its minimum capital requirements, which provides a solid foundation for future operations. The company has consistently played a vital role in the real estate finance sector.

In Q1 2024, Fannie Mae reported a net income of $2.2 billion, a decrease from the prior quarter, primarily due to fair value losses and lower net interest income. Despite these short-term fluctuations, the company's core business remains strong. Its long-term goals are centered on maintaining a stable and liquid secondary mortgage market while returning capital to the U.S. Treasury, a practice it has followed since 2014. For a deeper understanding of its origins, consider reading a Brief History of Fannie Mae.

Fannie Mae reported a net income of $12.5 billion for the full year 2023. This was a slight decrease from $12.9 billion in 2022. The decrease was primarily due to a decrease in net interest income, showing the impact of market conditions on its revenue streams.

As of December 31, 2023, Fannie Mae had total capital of $68.6 billion. This robust capital base exceeds its minimum capital requirement, providing a buffer against potential market downturns. This strong capital position supports its mission.

In Q1 2024, Fannie Mae reported a net income of $2.2 billion. This was a decrease from $4.3 billion in the prior quarter. The decrease was primarily due to fair value losses and lower net interest income, reflecting the impact of market dynamics.

Fannie Mae's primary revenue sources include guarantee fees from the mortgages it securitizes and net interest income from its retained portfolio. The focus on Credit Risk Transfer (CRT) programs is also a key part of its financial strategy.

Key Strategic Initiatives

Fannie Mae's strategic initiatives are focused on maintaining a stable secondary mortgage market and managing risk. These initiatives are designed to enhance its financial resilience and support its long-term goals in the mortgage industry.

- Credit Risk Transfer (CRT) programs to reduce exposure to credit losses.

- Focus on maintaining capital adequacy to withstand market fluctuations.

- Continued efforts to return capital to the U.S. Treasury.

- Adaptation to changing interest rate environments and market conditions.

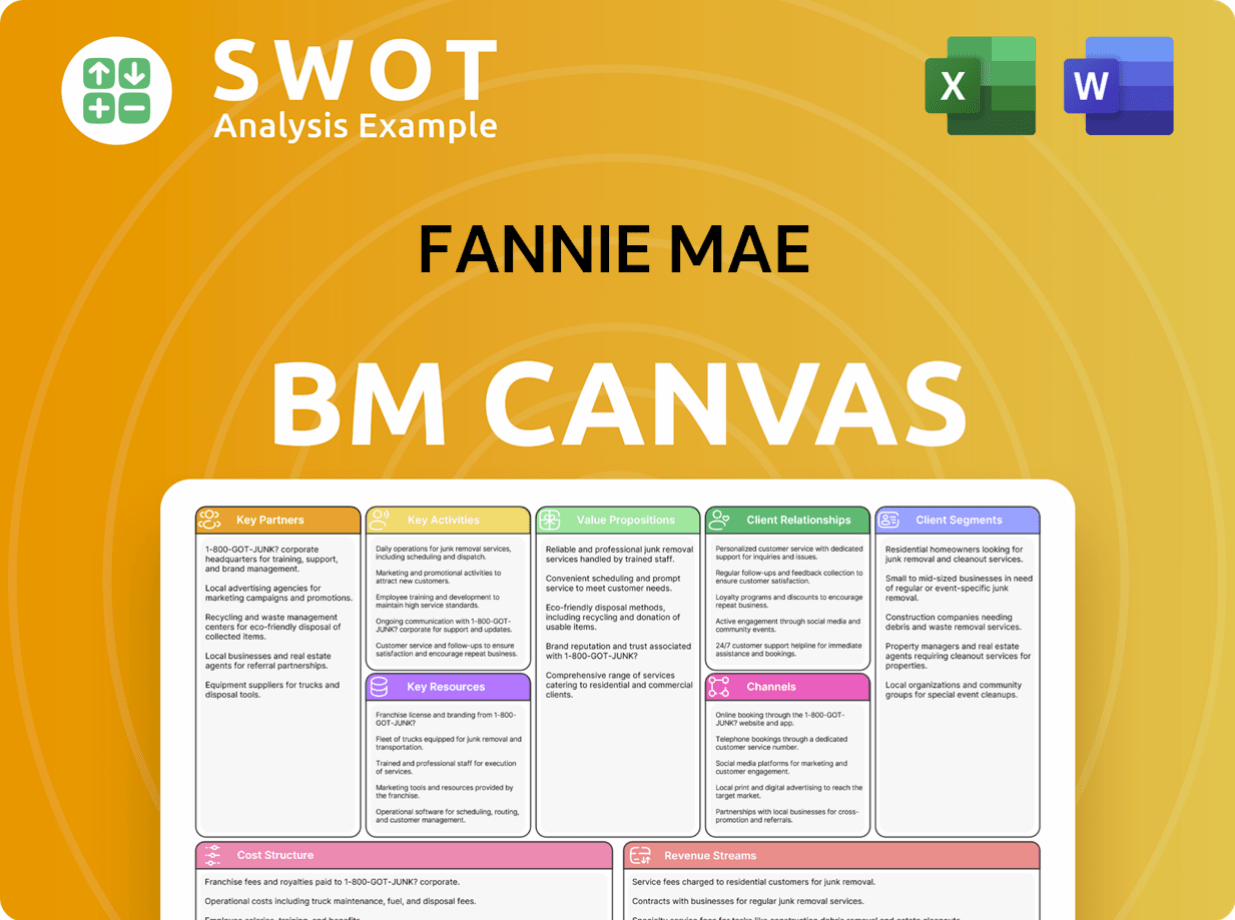

Fannie Mae Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Fannie Mae’s Growth?

The future of the Fannie Mae Company hinges on navigating several significant risks and obstacles. These challenges span market competition, regulatory changes, and technological disruptions. Understanding these potential pitfalls is crucial for assessing the Fannie Mae Growth Strategy and its ability to achieve its long-term goals within the Mortgage Industry.

One primary concern is the increasing competition from private capital in the secondary mortgage market. Regulatory uncertainties, including potential shifts in conservatorship status and capital requirements, also pose a threat. Furthermore, the rapid evolution of technology in the Real Estate Finance sector demands continuous innovation and adaptation.

Economic factors, such as interest rate fluctuations and housing market downturns, can significantly impact Fannie Mae's financial performance analysis. Global economic instability and geopolitical events add further layers of complexity. The company's risk management frameworks and ongoing dialogue with stakeholders are essential for mitigating these challenges and ensuring its stability.

Market Competition

Increased participation from private sector entities in mortgage securitization and credit risk transfer could reduce Fannie Mae's market share analysis and potentially lower guarantee fees. The Fannie Mae's competitive landscape is evolving, requiring strategic responses. The company must maintain its competitive edge while fulfilling its mission.

Regulatory Changes

Changes in conservatorship status, capital requirements, or mission parameters could significantly affect Fannie Mae's business model. Ongoing discussions about GSE reform and potential re-privatization create long-term regulatory uncertainty. The Fannie Mae's regulatory environment is subject to change.

Technological Disruption

Rapid advancements in fintech could lead to new business models that bypass traditional mortgage finance channels. Adapting to emerging technologies, like blockchain, is crucial. Fannie Mae's technological advancements play a key role in its future.

Economic Factors

Sustained high interest rates, housing market downturns, or recessions could lead to increased mortgage defaults and credit losses. Global economic instability and geopolitical events can indirectly affect the U.S. housing market. These factors impact Fannie Mae's financial performance analysis.

Risk Management

Robust risk management frameworks, including credit modeling and stress testing, are essential for mitigating potential losses. Extensive credit risk transfer programs help diversify exposure. Fannie Mae's risk management practices are critical to its stability.

Stakeholder Engagement

Continuous dialogue with regulators and industry stakeholders is vital for anticipating and preparing for challenges. Proactive engagement helps in navigating the complex landscape. Understanding the Fannie Mae's challenges and opportunities is key.

In 2024, the Fannie Mae Company continued to hold a significant share of the mortgage market, but competition from private entities remains a factor. The company's ability to maintain its market position depends on its strategic initiatives and its capacity to adapt to evolving market dynamics. The Fannie Mae's market share analysis shows a competitive landscape.

The regulatory landscape for Fannie Mae is subject to ongoing changes and scrutiny. Discussions regarding GSE reform and potential adjustments to capital requirements will continue to shape the company's operations. The Fannie Mae's regulatory environment is constantly evolving, impacting its long-term goals.

Economic conditions, including interest rate fluctuations and potential downturns in the Housing Market, pose significant risks. High interest rates can lead to reduced affordability and potentially increase default rates. Understanding the impact of these factors is essential for Fannie Mae's investment strategies.

The rapid pace of technological advancements in fintech requires continuous adaptation and investment. Staying at the forefront of digital transformation and leveraging technologies like blockchain will be critical. For more details, read about the Target Market of Fannie Mae to understand its position.

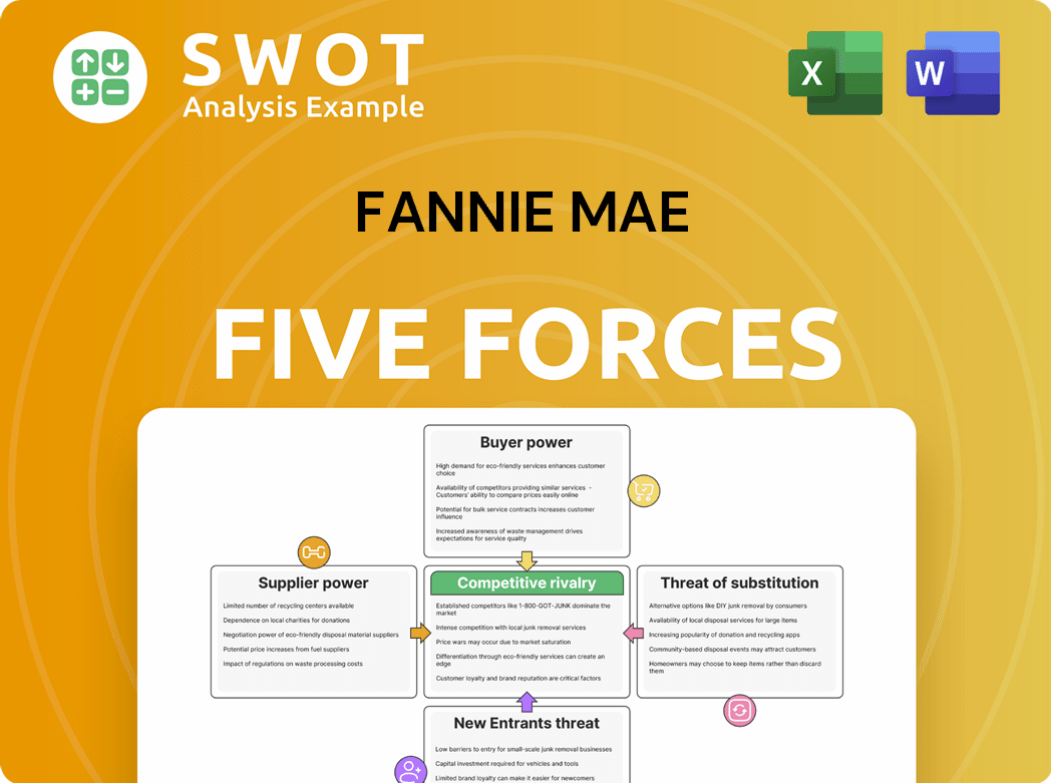

Fannie Mae Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Fannie Mae Company?

- What is Competitive Landscape of Fannie Mae Company?

- How Does Fannie Mae Company Work?

- What is Sales and Marketing Strategy of Fannie Mae Company?

- What is Brief History of Fannie Mae Company?

- Who Owns Fannie Mae Company?

- What is Customer Demographics and Target Market of Fannie Mae Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.