Spandana Sphoorty Financial Bundle

Who Does Spandana Sphoorty Serve?

Understanding the core Spandana Sphoorty Financial SWOT Analysis is essential for grasping its strategic direction. Spandana Sphoorty, a prominent financial company, has built its foundation on serving a specific target market. This exploration delves into the customer demographics that define Spandana Sphoorty's success. The microfinance sector's evolution underscores the critical need to adapt and understand the customer profile.

Spandana Sphoorty's commitment to financial inclusion, particularly for low-income women in rural India, has shaped its operational strategies. Analyzing the Spandana Sphoorty customer base analysis reveals insights into their financial aspirations and challenges. This detailed examination of the company's target market segmentation helps to understand how Spandana Sphoorty strategically evolves its services to effectively cater to them, from their age range to their income levels, and geographical locations.

Who Are Spandana Sphoorty Financial’s Main Customers?

The primary customer segments for Spandana Sphoorty Financial Company are low-income women residing in rural and semi-urban areas of India. This financial company focuses on providing microfinance solutions to individuals engaged in income-generating activities. These activities include agriculture, handlooms, handicrafts, and small-scale businesses, reflecting a targeted approach to financial inclusion.

The company's core strategy revolves around the Joint Liability Group (JLG) loan model, which emphasizes collective responsibility among borrowers. This model is specifically designed to support women entrepreneurs. Furthermore, the company also provides loans for education and healthcare, addressing broader financial needs within its target demographic. The customer profile is defined by a focus on women in rural areas, although the company has expanded its offerings.

Spandana Sphoorty's customer base is primarily composed of women in rural and semi-urban India. These individuals are typically involved in various income-generating activities. The company's microfinance approach is designed to support these women. The company's customer acquisition strategy has been a key driver of growth, with a significant number of new borrowers added each year.

The target market for Spandana Sphoorty consists mainly of low-income women in rural and semi-urban areas. These women are typically involved in income-generating activities. The company's focus on the JLG model underscores its commitment to supporting women entrepreneurs and fostering financial inclusion.

The primary target market is women, particularly those involved in agriculture, handlooms, and small businesses. The company also caters to those seeking loans for education and healthcare. This focus aligns with the company's mission of promoting financial inclusion among underserved populations.

Spandana Sphoorty offers a range of loan products, including JLG loans, loans against property (LAP), and nano enterprise loans. These products cater to various needs within the low-income segment. The expansion of product offerings reflects a strategic effort to meet the diverse financial requirements of its customer base.

The company places a strong emphasis on customer acquisition-led growth. In FY24, Spandana Sphoorty added close to 1.39 million new borrowers. This demonstrates a continuous effort to expand its customer base and reach more individuals in need of financial services. The company aims to achieve a total customer base of 4 million by FY25.

Key Statistics and Trends

As of December 2024, Spandana Sphoorty's consolidated borrower base was 2.96 million. The total borrower count rose to 3.32 million in FY24. The average outstanding loan ticket size per borrower was approximately INR 27,386 as of March 2025.

- The company's focus on microfinance, particularly through the JLG model, continues to be a core strategy.

- The expansion into LAP and nano enterprise loans by its subsidiary, Criss Financial Ltd., broadens its service offerings.

- The fluctuation in active borrowers, with a decline to 2.49 million as of March 2025, indicates the dynamic nature of the microfinance sector.

- The company's strategic vision includes diversifying its offerings beyond traditional microfinance while maintaining its commitment to financial inclusion.

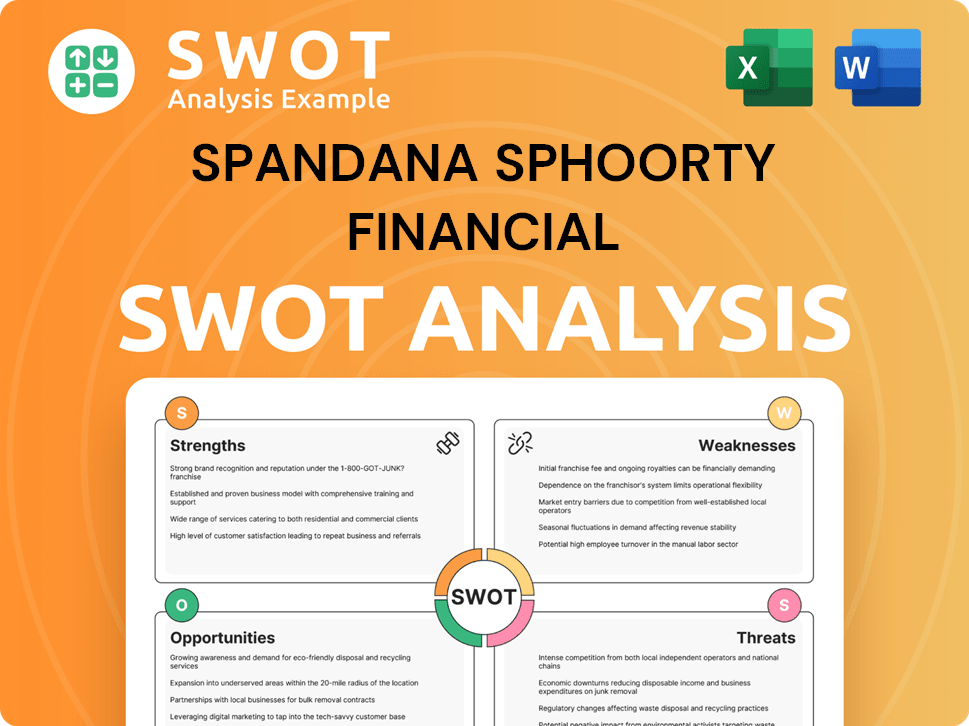

Spandana Sphoorty Financial SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do Spandana Sphoorty Financial’s Customers Want?

Understanding the customer needs and preferences is crucial for any financial company, and for Spandana Sphoorty, this means focusing on the low-income women in rural and semi-urban India. These individuals form the core of the company's target market, driven by the desire for financial empowerment and the ability to generate income. This customer profile is distinct, requiring tailored financial products and services.

The primary motivation for Spandana Sphoorty's customers is to establish or expand micro-enterprises. These micro-enterprises help improve their livelihoods and achieve financial independence. The company addresses unmet needs by providing access to small-value unsecured loans, which traditional banking services often overlook. These loans support income-generating activities such as agriculture, handlooms, cattle rearing, cottage industries, tailoring, and grocery stores.

The purchasing behaviors of Spandana Sphoorty's customers are shaped by the need for accessible, flexible, and affordable credit. The company's 'Chetana' product, a JLG-based micro-loan, reflects this understanding. It offers flexible repayment options and loan tenures ranging from 12 to 30 months. The interest rate for this product is 25% per annum. Ease of access, repayment flexibility, and the direct impact of the loan on their income-generating activities are key decision-making criteria for these borrowers.

Addressing Financial Literacy and Digital Inclusion

Spandana Sphoorty recognizes the importance of financial literacy and digital inclusion within its customer base. Partnering with the NIIT Foundation, the company launched a Digital & Financial Literacy Program in September 2024. This program offers a 5-hour training course covering essential topics such as budgeting, savings, investments, loan management, insurance, and digital payments, including cybersecurity awareness. This initiative helps bridge the knowledge gap in financial planning and digital transactions among its target communities, acknowledging that Indian women are less likely to own smartphones or use mobile internet services compared to men.

This tailored approach, encompassing both product features and educational programs, underscores the company's commitment to adapting to the specific practical and aspirational drivers of its customer base. For a deeper understanding of the competitive landscape, consider exploring the Competitors Landscape of Spandana Sphoorty Financial.

- The Digital & Financial Literacy Program is a direct response to the lack of financial knowledge and digital skills among the target demographic.

- The program's curriculum includes training on digital payments and cybersecurity, addressing key challenges in the digital space.

- By focusing on financial literacy, Spandana Sphoorty aims to empower its customers to make informed financial decisions.

- The company acknowledges the digital divide and tailors its services to address the specific needs and challenges faced by its customers.

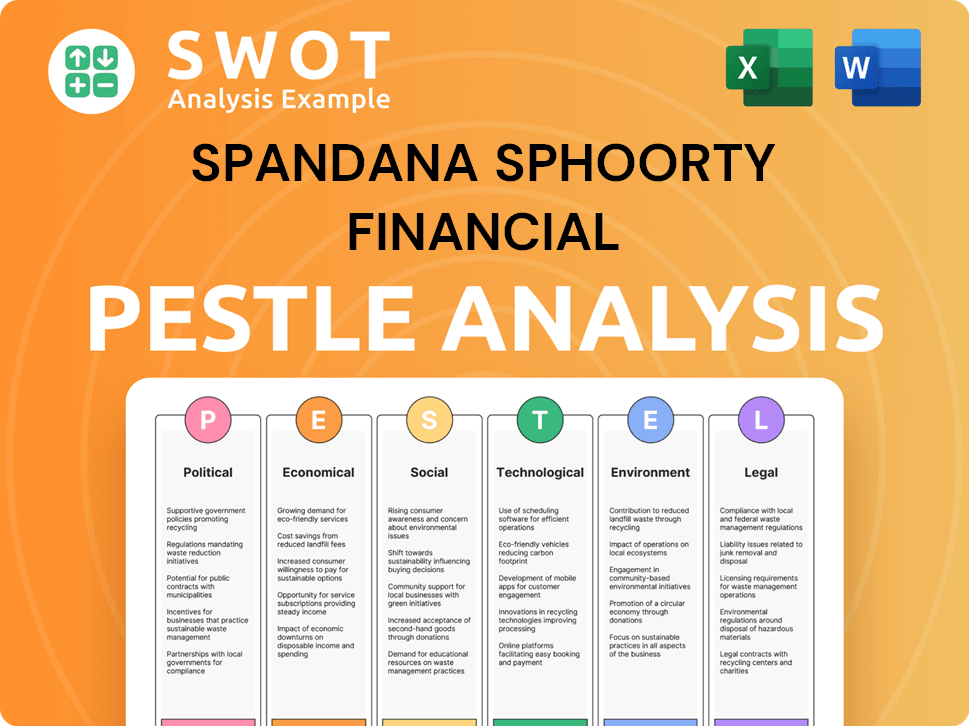

Spandana Sphoorty Financial PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does Spandana Sphoorty Financial operate?

The geographical market presence of the financial company, is a key factor in its operational strategy. The company strategically focuses on rural and semi-urban areas across India, ensuring a broad reach to its target market. This approach allows the financial company to cater to the specific needs of its customer demographics, particularly those in underserved regions.

As of March 2025, the company's operations spanned across 20 states and Union Territories, demonstrating a wide geographical footprint. This extensive reach is supported by a significant branch network, which stood at 1,804 branches as of March 2025, up from 1,774 branches in December 2024. This expansion reflects the company's commitment to increasing its presence and accessibility within its target market.

The financial company's strategy includes a focus on balancing regional exposure. While it aims to limit single-state concentration, its portfolio remains diversified. For instance, Madhya Pradesh accounted for 13.4% of the standalone AUM as of March 2025. The top three states—Odisha, Madhya Pradesh, and Bihar—combined for 37.9% of the portfolio, showcasing a strategic approach to manage risk and maintain a broad customer base. To learn more about the company's journey, you can read the Brief History of Spandana Sphoorty Financial.

Rural and Urban Focus

The company's loan exposure is primarily distributed in rural areas, with approximately 85% of its portfolio in these regions. This focus highlights the company's commitment to financial inclusion, targeting underserved populations. The remaining 15% is in urban areas, providing a balanced approach to market penetration.

Strategic Market Adjustments

The company has adopted a calibrated growth approach, including strategic withdrawals from certain states while strengthening its presence in others. Disbursements were paused during February-April 2025 and restarted in May 2025, indicating a cautious response to market conditions. This approach allows the company to optimize its operations and manage risk effectively.

Geographical Diversification

The company's aim to reduce single-state concentration to no more than 13% by the end of FY25 demonstrates its commitment to geographical diversification. This strategy helps mitigate risks associated with over-reliance on any single market. The company's balanced approach across multiple states ensures stability and resilience.

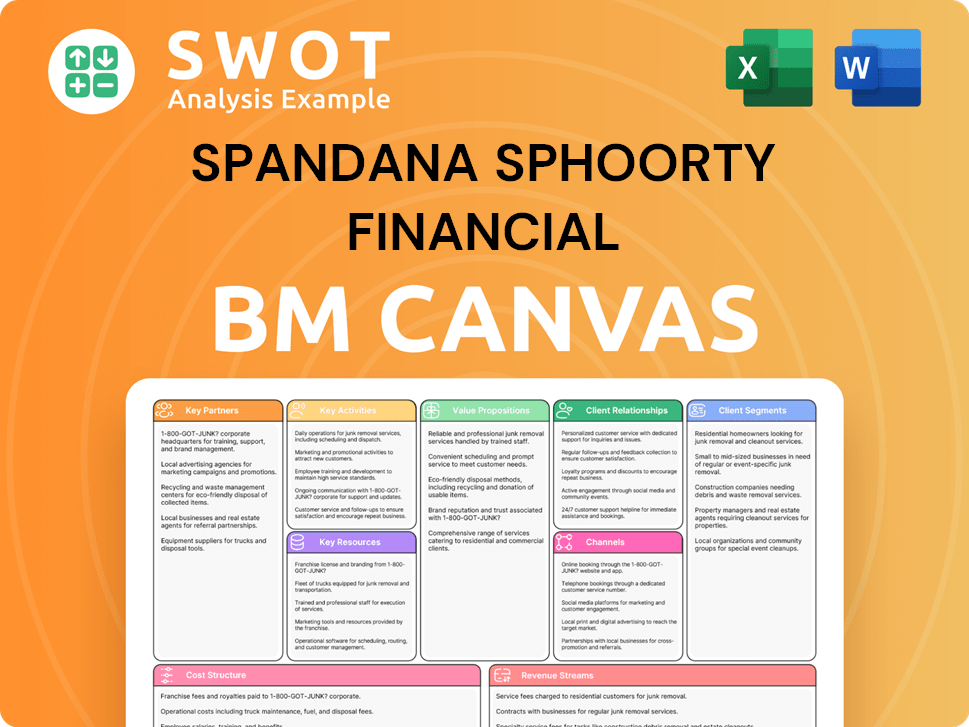

Spandana Sphoorty Financial Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does Spandana Sphoorty Financial Win & Keep Customers?

To understand the customer acquisition and retention strategies of a financial company like Spandana Sphoorty, it's crucial to examine how they attract and keep their clients. The company focuses heavily on acquiring new customers, using a multi-pronged approach that includes an extensive branch network and direct outreach. This strategy is particularly effective in reaching the target market, which primarily consists of individuals in rural and semi-urban areas where access to traditional financial services is limited.

Spandana Sphoorty's growth is heavily reliant on acquiring new borrowers. In FY24, the company successfully added approximately 1.39 million new borrowers, reflecting a substantial 59% increase compared to the previous year. A significant portion, over 50%, of the total loans disbursed were allocated to new borrowers. This highlights the company's dedication to expanding its customer base and reaching underserved communities. The company aims to increase its customer base to 4 million by FY25, up from 3.32 million in FY24, showing an ambitious growth plan.

The company uses a variety of marketing channels, with a strong emphasis on direct outreach and community engagement. Given the customer profile, which is predominantly rural and low-income, these methods are crucial. The Joint Liability Group (JLG) model is a key element, functioning as a community-based acquisition tool. This model fosters shared responsibility among borrowers, encouraging referrals and building trust within the community. Additionally, the company diversifies its product offerings, including Loan Against Property (LAP) and Nano loans through its subsidiary, Criss Financial Ltd., to attract new segments and cater to the changing needs of its current customer base. This shows a strategic approach to expand its services and meet the varied needs of its target market.

Retention Strategies and Challenges

For customer retention, the financial company focuses on strengthening processes, governance, and technology. They have refined processes by adopting appropriate tools and technologies and have scaled up multiple technology-related initiatives. This includes digitizing the loan process to improve efficiency and customer experience.

- To enhance financial literacy and customer engagement, Spandana Sphoorty launched the Digital & Financial Literacy Program in partnership with the NIIT Foundation in September 2024. This initiative equips clients with essential financial management and digital skills, fostering trust and long-term engagement.

- The introduction of shorter tenure loans (12 and 18 months) could potentially aid in higher earnings and improve repayment cycles.

- Challenges such as high employee attrition and issues like borrower overleveraging have impacted collection efficiency, which dropped to 90.6% as of March 2025, down from 98.5% in March 2024.

- To address these challenges, Spandana Sphoorty has expanded its field presence and operational infrastructure to increase recoveries.

For more insights, you can explore the Growth Strategy of Spandana Sphoorty Financial.

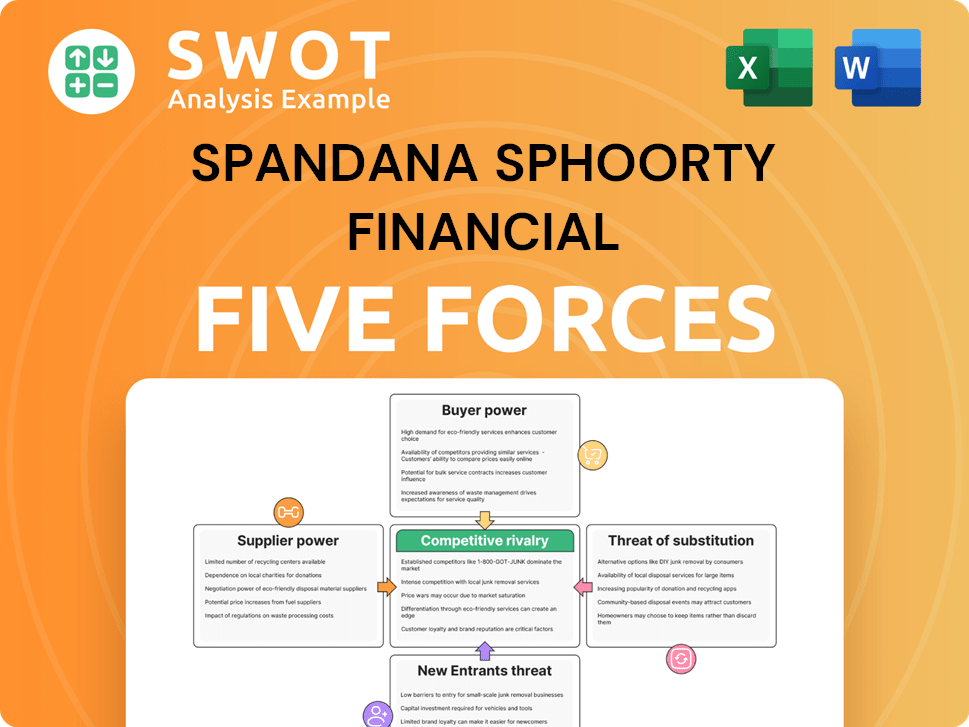

Spandana Sphoorty Financial Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Spandana Sphoorty Financial Company?

- What is Competitive Landscape of Spandana Sphoorty Financial Company?

- What is Growth Strategy and Future Prospects of Spandana Sphoorty Financial Company?

- How Does Spandana Sphoorty Financial Company Work?

- What is Sales and Marketing Strategy of Spandana Sphoorty Financial Company?

- What is Brief History of Spandana Sphoorty Financial Company?

- Who Owns Spandana Sphoorty Financial Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.