Spandana Sphoorty Financial Bundle

What's the Story Behind Spandana Sphoorty Financial Company?

Ever wondered how a small loan could change someone's life? The Spandana Sphoorty Financial SWOT Analysis reveals a remarkable journey. This Financial Company started with a simple observation and grew into a major player in Microfinance. Let's dive into the Brief History of this inspiring institution.

The History of Spandana is a testament to the power of financial inclusion. From its humble beginnings as an NGO in 1998, Spandana Sphoorty Ltd quickly became a leading force in providing microcredit. Understanding the Spandana Sphoorty Financial Company founder's vision helps to understand the company's mission. Explore the Spandana Sphoorty company overview to learn more about its impact.

What is the Spandana Sphoorty Financial Founding Story?

The Brief History of the Financial Company, Spandana Sphoorty, began in June 1998. It started as a microcredit initiative within an NGO. This journey was inspired by the transformative impact of small loans on the livelihoods of low-income individuals.

Spandana Sphoorty Financial Limited was formally established on March 10, 2003, in Hyderabad, India, under the name Spandana Sphoorty Innovative Financial Services Limited. The company then secured its NBFC registration from the Reserve Bank of India (RBI) on October 16, 2004. The core mission was to provide financial services to those excluded from mainstream banking, particularly women in rural areas.

The company's initial focus was on offering small group loans, primarily to women, without requiring collateral. This approach aimed to empower them to establish sustainable livelihoods. Early funding came from various sources, including investments from JM Financial and Lok Capital in 2007, and Valiant Capital in 2008. One of the significant challenges faced was the Andhra Pradesh microfinance crisis in 2010, which significantly impacted the industry. For a deeper understanding of the company's target market, explore Target Market of Spandana Sphoorty Financial.

Key Milestones in Spandana Sphoorty's History

Here's a look at some of the key events in the company's journey.

- 1998: The microcredit program was initiated within an NGO.

- 2003: Incorporated as Spandana Sphoorty Innovative Financial Services Limited.

- 2004: Received NBFC registration from the RBI.

- 2007-2008: Secured significant investments from JM Financial, Lok Capital, and Valiant Capital.

- 2010: Navigated the Andhra Pradesh microfinance crisis.

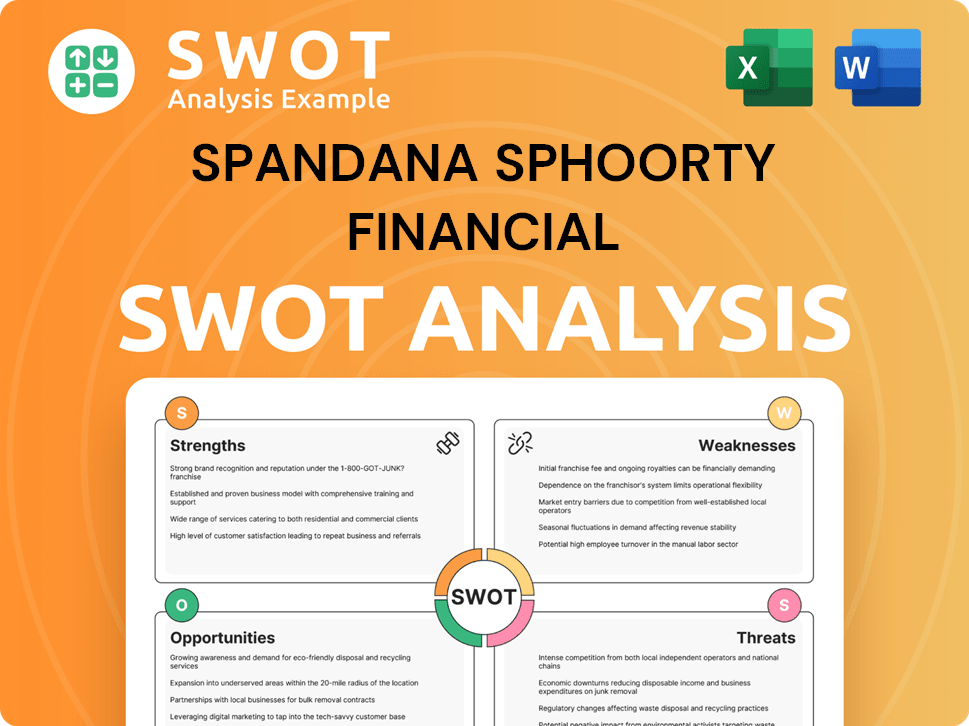

Spandana Sphoorty Financial SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of Spandana Sphoorty Financial?

The early phase of Spandana Sphoorty Financial Company was marked by rapid expansion and market consolidation within the microfinance sector. Initially launched as an NGO program, it quickly grew to become the largest MFI in India by 2003. The company officially transitioned to Spandana Sphoorty Financial Limited on January 3, 2008, reflecting its evolution into a formal corporate structure.

Spandana Sphoorty focused heavily on expanding its geographical presence during its growth period. As of December 31, 2024, the company's operations spanned across 19 states and 1 union territory, demonstrating a broad reach across India. This expansion was crucial for increasing its customer base and overall market penetration.

The financial performance of Spandana Sphoorty, as a Financial Company, showed significant growth. By March 2024, assets under management (AUM) reached approximately ₹119.7 billion, a 41% year-on-year increase. Disbursements also grew by about 30% year-on-year to ₹39.7 billion in FY24, reflecting robust business activity.

Customer acquisition was a key driver of Spandana Sphoorty's growth. The company added approximately 440,000 customers in Q4 FY24, bringing the total borrower count to 3.32 million. This growth in customer base underscores the company's ability to attract and retain clients.

Spandana Sphoorty diversified its product offerings to include Loans Against Property (LAP) and Nano enterprise loans. As of April 2024, these non-MFI loan products accounted for an AUM of ₹520 million across 3,000 customers. The company aimed to grow this segment to ₹4-5 billion by FY25.

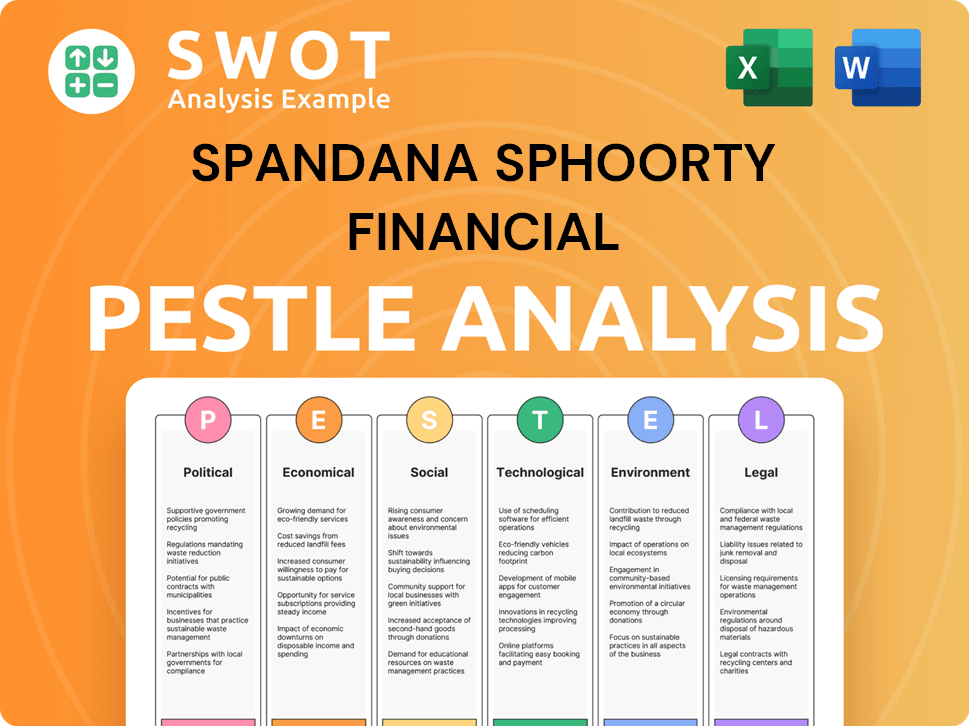

Spandana Sphoorty Financial PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in Spandana Sphoorty Financial history?

The Financial Company, Spandana Sphoorty has experienced significant developments, including strategic expansions and responses to market challenges. The company's journey reflects its adaptation to the evolving financial landscape and its commitment to serving its customer base. The Brief History of Spandana Sphoorty highlights its growth and resilience in the microfinance sector.

| Year | Milestone |

|---|---|

| 2010 | The company faced a major setback due to the Andhra Pradesh government's ordinance, impacting its IPO plans. |

| 2019 | Achieved 99% cashless monthly disbursements by March, demonstrating technological and operational advancements. |

| Ongoing | Expanded its product portfolio to include Loans against Property (LAP), Housing Loans, and Business Loans, diversifying its offerings. |

| 2024 | Reported a net loss of ₹601 crore for the nine months ending December 31, 2024, reflecting financial challenges. |

| 2024 | Capital Adequacy Ratio (CAR) of 36.0% as of December 31, 2024, providing a buffer against potential losses. |

One of the key innovations of Spandana Sphoorty was the implementation of cashless loan disbursements, which streamlined operations and improved efficiency. This shift towards digital transactions marked a significant step in the company's modernization efforts.

Cashless Disbursements

Achieved 99% cashless monthly disbursements by March 2019, enhancing operational efficiency.

Product Diversification

Expanded offerings beyond microfinance to include Loans against Property (LAP), Housing Loans, and Business Loans.

Digital Transformation

Embraced digital technologies to improve customer service and streamline loan processes.

Strategic Partnerships

Formed strategic alliances to enhance market reach and service delivery.

Risk Management

Implemented robust risk management practices to mitigate financial risks.

Customer-Centric Approach

Focused on providing tailored financial solutions to meet the diverse needs of its customer base.

Despite these advancements, Spandana Sphoorty has faced significant challenges, including regulatory hurdles and financial setbacks. The company's recent performance has been impacted by factors such as asset quality deterioration and increased credit costs.

Regulatory Challenges

The Andhra Pradesh ordinance in October 2010 significantly impacted operations and IPO plans.

Financial Setbacks

Reported a net loss of ₹601 crore for the nine months ending December 31, 2024, reflecting financial strain.

Asset Quality Deterioration

Consolidated Gross Stage 3 (GS3) assets increased to 5.25% and Net Stage 3 (NS3) assets to 1.11% as of December 31, 2024.

Increased Credit Costs

Incurred incremental credit costs of ₹666 crore for Q3 2025, impacting profitability.

Market Volatility

Fluctuations in the microfinance market have affected the company's financial performance.

Operational Challenges

Managing field-level attrition and maintaining credit discipline have posed challenges.

To navigate these challenges, Spandana Sphoorty has implemented strategic adjustments, including recalibrating its growth strategy and focusing on improving asset quality. The company's Marketing Strategy of Spandana Sphoorty Financial has also evolved to adapt to changing market conditions.

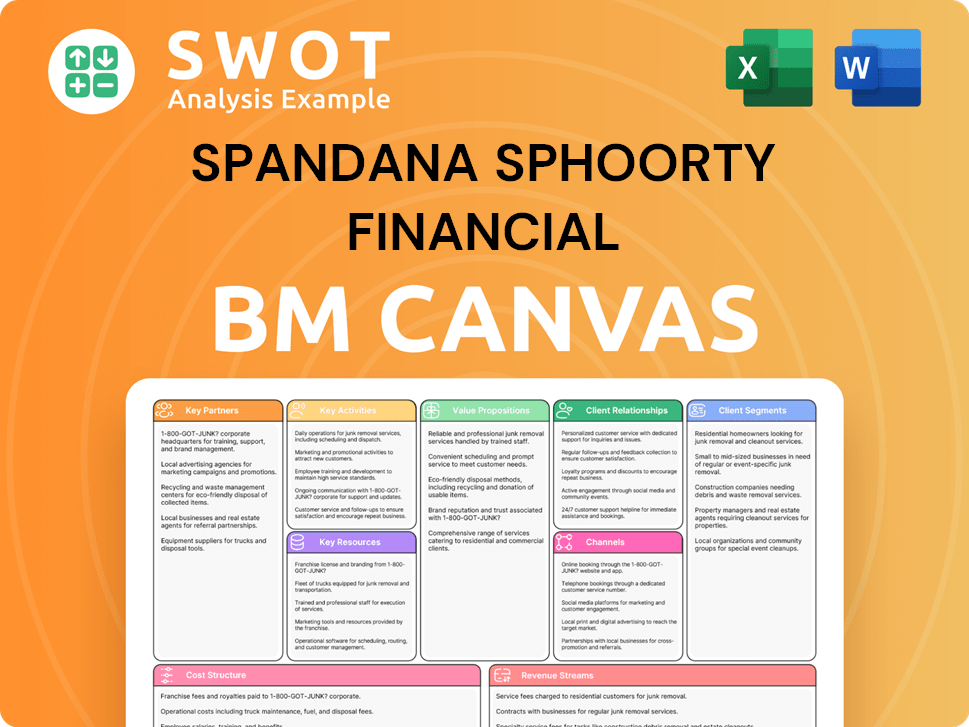

Spandana Sphoorty Financial Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for Spandana Sphoorty Financial?

The Brief History of Spandana Sphoorty Financial Company, a prominent Financial Company, is marked by key milestones, beginning as a microcredit program and evolving into a publicly listed NBFC-MFI. From its inception in 1998 as an NGO initiative, the company has navigated significant challenges, including the Andhra Pradesh microfinance crisis in 2010. It has expanded its operations, secured NBFC-MFI status from the RBI, and conducted an IPO in 2019. Recent financial data indicates a consolidated AUM of approximately ₹119.7 billion as of March 31, 2024. The company continues to adapt to market dynamics, focusing on strategic growth and financial inclusion within rural India.

| Year | Key Event |

|---|---|

| 1998 | Founded as a microcredit program of an NGO. |

| 2003 | Incorporated as Spandana Sphoorty Innovative Financial Services Limited. |

| 2004 | Obtained NBFC registration from RBI. |

| 2008 | Name changed to Spandana Sphoorty Financial Limited. |

| 2010 | Impacted by the Andhra Pradesh microfinance crisis, leading to corporate debt restructuring. |

| 2015 | Granted NBFC–Microfinance Institution (NBFC-MFI) status by the RBI. |

| 2019 | Shares listed on Indian stock exchanges following an IPO. |

| 2024 | Consolidated AUM reached approximately ₹119.7 billion. |

| 2024 | Reported consolidated AUM of ₹8,936 crore; Gross Stage 3 assets at 5.25% and Net Stage 3 assets at 1.11%. |

| 2025 | Reported a consolidated net loss of ₹434.30 crore for the quarter. |

| 2025 | Ashish Kumar Damani appointed as interim CEO. |

Spandana Sphoorty aims to grow its customer base to 4 million by FY25 through customer acquisition-led strategies. This growth strategy is a key focus for the company.

The company plans to expand its non-MFI loan book, including LAP and Nano enterprise loans. The target is to reach ₹4-5 billion by FY25.

Spandana Sphoorty is working on improving its cost of borrowings. The company anticipates the challenging situation to normalize by the second quarter of the current financial year.

The company is looking to raise up to ₹750 crore in confidence capital to strengthen its net worth. This capital raise is part of the company's strategy.

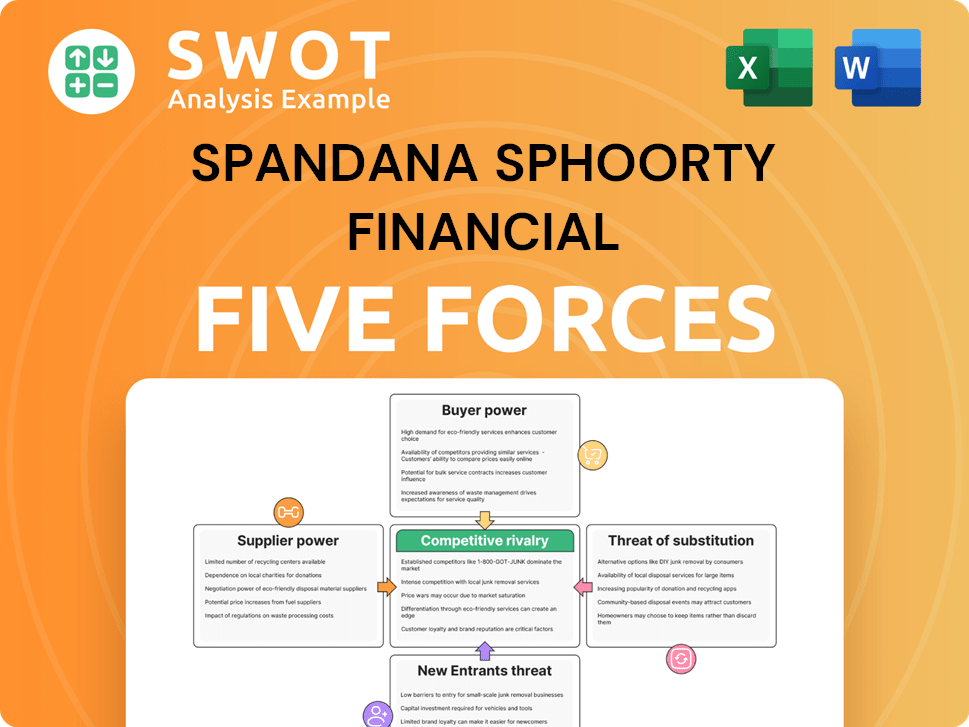

Spandana Sphoorty Financial Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of Spandana Sphoorty Financial Company?

- What is Growth Strategy and Future Prospects of Spandana Sphoorty Financial Company?

- How Does Spandana Sphoorty Financial Company Work?

- What is Sales and Marketing Strategy of Spandana Sphoorty Financial Company?

- What is Brief History of Spandana Sphoorty Financial Company?

- Who Owns Spandana Sphoorty Financial Company?

- What is Customer Demographics and Target Market of Spandana Sphoorty Financial Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.