The IHC Group Bundle

How Well Does The IHC Group Know Its Customers?

In the complex world of insurance, understanding the The IHC Group SWOT Analysis is crucial for success. This involves a deep dive into customer demographics and a strategic target market analysis. For The IHC Group, knowing who their customers are, from age demographics to income levels, directly impacts their ability to thrive.

This exploration of the IHC Group's customer base will reveal how the company strategically adapts to serve its target market. We'll examine the demographic data, market segmentation, and how IHC Group defines its target market. Understanding these aspects is key to grasping the company's market position and future growth potential, including insights into their marketing strategies based on demographics and the characteristics of their ideal customer.

Who Are The IHC Group’s Main Customers?

The IHC Group, a company operating in the insurance sector, strategically focuses on two main customer segments: Business-to-Business (B2B) and Business-to-Consumer (B2C). This approach allows the company to cater to a diverse range of needs, from employer groups seeking risk management solutions to individuals looking for flexible health insurance options. Understanding the customer demographics and target market analysis is crucial for the company's success in these varied segments.

In the B2B sector, the IHC Group primarily serves small to medium-sized businesses (SMBs). These businesses often require medical stop-loss insurance to protect against high-cost employee health claims. The decision-makers within these companies, such as HR managers, CFOs, or business owners, prioritize financial stability and comprehensive coverage for their workforce. The company's ability to provide tailored insurance solutions is key to attracting and retaining these clients.

For its B2C offerings, the IHC Group targets individuals and families. This demographic includes those in transition, self-employed individuals, or those seeking to supplement their existing health coverage. This segment is often proactive in managing healthcare costs and seeking flexible insurance solutions. The company's success depends on its ability to offer products that meet the evolving needs of this diverse customer base.

The B2B segment primarily includes small to medium-sized businesses (SMBs). These businesses often seek medical stop-loss insurance to manage the financial risks associated with employee health claims. Decision-makers typically include HR managers and CFOs.

The B2C segment focuses on individuals and families. This includes those in transition, self-employed individuals, or those seeking supplemental health coverage. This demographic is often proactive in managing healthcare costs.

Key products include medical stop-loss insurance for SMBs and short-term medical and supplemental health insurance for individuals. These products cater to the specific needs of each customer segment.

The company focuses on the self-funded employer market and the demand for flexible individual health plans. This strategic focus allows the company to adapt to evolving healthcare regulations and employer benefit trends.

IHC Group's Market Segmentation

The IHC Group's market segmentation strategy involves targeting both B2B and B2C segments with specialized insurance products. This approach allows the company to address the diverse needs of employers and individuals seeking health and life insurance solutions. The company's focus on the self-funded employer market and flexible individual health plans reflects its adaptability to changing healthcare trends. For more insights, see Revenue Streams & Business Model of The IHC Group.

- B2B: Small to medium-sized businesses (SMBs) seeking medical stop-loss insurance.

- B2C: Individuals and families needing short-term medical and supplemental health insurance.

- Product Focus: Medical stop-loss, short-term medical, and supplemental health insurance.

- Market Trends: Adapting to self-funded employer market and flexible individual health plans.

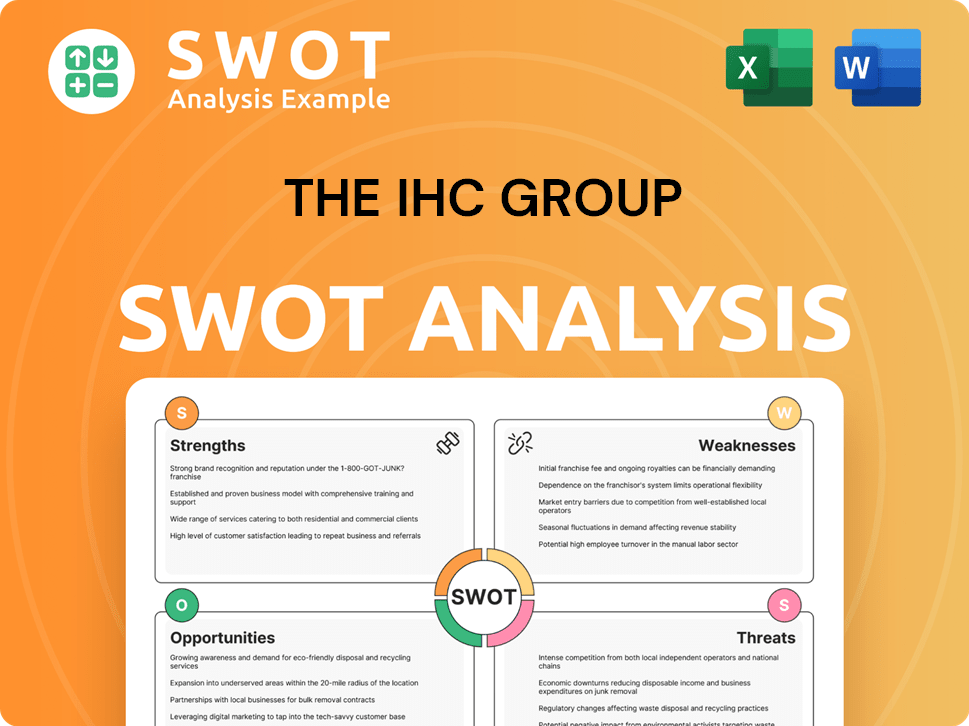

The IHC Group SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do The IHC Group’s Customers Want?

Understanding the customer needs and preferences is crucial for the success of the IHC Group. The company caters to a diverse customer base, each with unique requirements and expectations. This analysis helps in tailoring products and marketing strategies effectively.

The IHC Group's approach to customer needs is multifaceted, considering both the business-to-business (B2B) and business-to-consumer (B2C) segments. This dual focus allows the company to address a wide range of insurance needs, from financial risk mitigation for businesses to flexible coverage options for individuals. The company's ability to adapt to these varied needs is central to its market positioning.

The IHC Group's customer base is driven by a complex interplay of practical, financial, and psychological needs. For B2B clients utilizing medical stop-loss insurance, the primary motivation is financial risk mitigation and predictability in healthcare expenditures. Their decision-making criteria center on the policy's deductible levels, coverage limits, claims processing efficiency, and the insurer's financial stability and reputation.

B2B Customer Needs

B2B clients prioritize financial risk mitigation. They seek predictability in healthcare spending and evaluate policies based on deductibles, coverage limits, and claims processing.

B2C Customer Needs

B2C customers value affordability, flexibility, and immediate coverage. They often need short-term solutions and are influenced by ease of enrollment and clear policy terms.

Key Decision Factors

For B2B, financial stability and claims processing efficiency are critical. B2C customers focus on cost-effectiveness and the ability to customize coverage.

Product Tailoring

The IHC Group tailors products to meet specific needs, such as offering various deductible options and supplemental benefits to cater to diverse customer segments.

Marketing Strategies

Marketing efforts highlight flexibility and cost-effectiveness, appealing to those who value control over healthcare spending and immediate access to coverage.

Customer Feedback

The IHC Group likely uses customer feedback and market trends to refine product features, ensuring they meet evolving customer needs effectively.

In the B2C segment, customers for short-term medical and supplemental health insurance prioritize affordability, flexibility, and immediate coverage. These individuals often have specific, immediate needs, such as bridging gaps in coverage between jobs, providing temporary protection, or supplementing high-deductible health plans. Their purchasing behaviors are influenced by ease of enrollment, clear policy terms, and the ability to customize coverage to their specific health and financial situations. They are often looking for practical solutions to specific pain points, such as unexpected medical bills or the inability to access affordable comprehensive plans. Growth Strategy of The IHC Group shows how the company addresses these unmet needs by offering tailored products that are often more cost-effective than traditional plans, particularly for those who are relatively healthy and seeking basic coverage. The company likely leverages customer feedback and market trends to refine its product features, such as offering various deductible options or adding specific supplemental benefits. Marketing efforts are tailored to highlight the flexibility and cost-effectiveness of these solutions, appealing to individuals who value control over their healthcare spending and immediate access to coverage.

Key Customer Needs

The IHC Group addresses the needs of two main customer segments: B2B and B2C. Understanding these needs is crucial for effective market segmentation and product development. Customer demographics and market segmentation are key factors.

- B2B: Focus on financial risk mitigation, predictability in healthcare costs, and efficient claims processing.

- B2C: Prioritize affordability, flexibility, ease of enrollment, and immediate coverage for short-term or supplemental needs.

- Customer Preferences: Customers want tailored products, clear policy terms, and the ability to customize coverage.

- Marketing Strategies: Highlight cost-effectiveness and flexibility to attract customers seeking control over their healthcare spending.

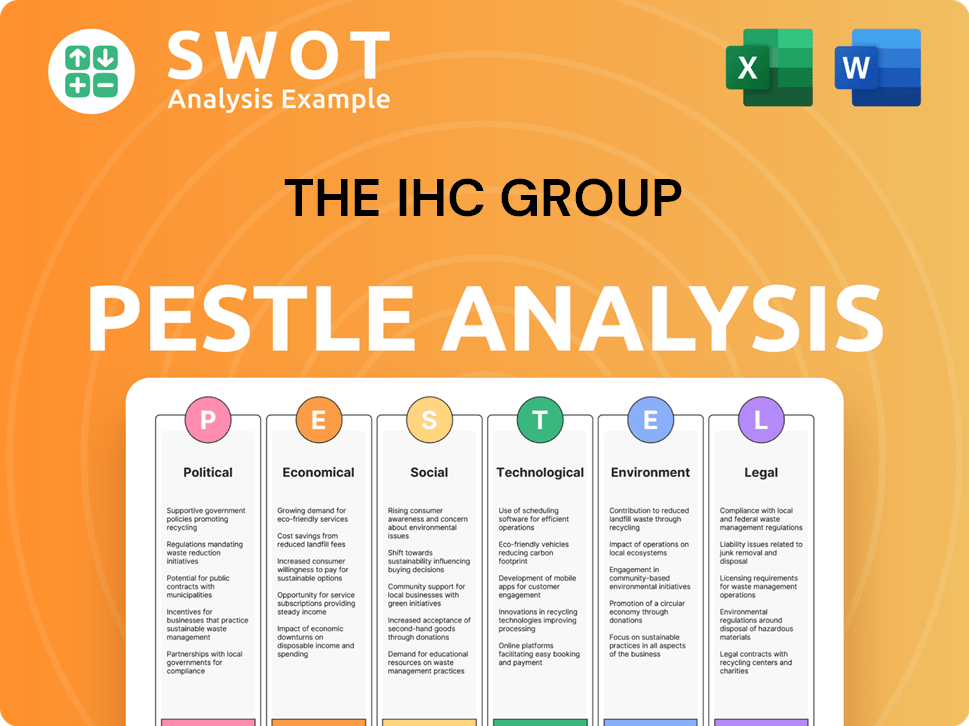

The IHC Group PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does The IHC Group operate?

The IHC Group, as an insurance and reinsurance provider, maintains a broad geographical market presence across the United States. While specific market share data by state or city isn't extensively detailed in public filings, the company's operations span various regions with different demographic and economic profiles. Its diverse product portfolio, including medical stop-loss and individual health insurance, suggests a strategic approach to market segmentation and geographic distribution.

The company's market presence is significantly influenced by state-specific insurance regulations and market demand. For instance, states with more favorable regulatory environments for specialized health and life insurance products likely see a higher concentration of sales and growth. Digital distribution channels also enable the company to reach customers across diverse geographical areas, expanding its reach beyond physical locations.

Understanding the geographical distribution of the Growth Strategy of The IHC Group is crucial for assessing its market penetration and identifying potential growth areas. The company's focus on tailoring its offerings to comply with state-specific regulations and addressing regional differences in customer preferences indicates a localized approach to its target market.

The medical stop-loss business targets areas with a high concentration of small to medium-sized businesses. This strategy implies a significant presence in states with robust economic activity and a strong entrepreneurial spirit.

The company's market presence for individual health insurance products is influenced by state-specific insurance regulations. Some states may have a higher propensity for short-term health plans due to their regulatory environment.

Digital distribution channels enable the company to reach customers across diverse geographical areas. This broadens the company's reach beyond physical locations and allows for increased market penetration.

The company localizes its offerings to comply with state-specific regulations and address regional differences. This includes tailoring product features and marketing messages to resonate with specific consumer needs.

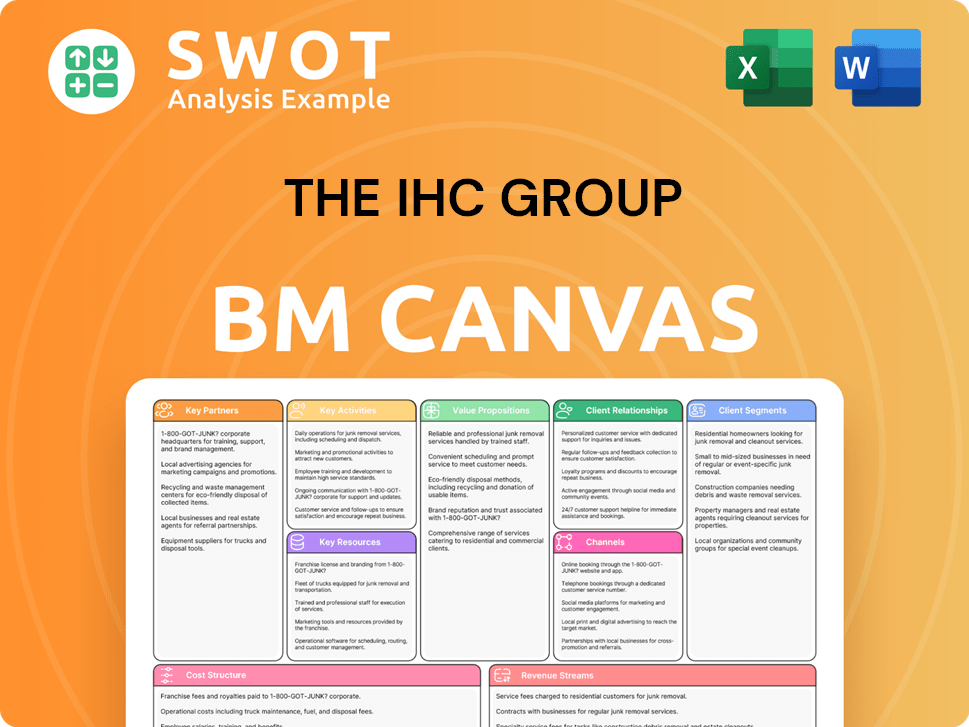

The IHC Group Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does The IHC Group Win & Keep Customers?

The IHC Group employs a multifaceted approach to customer acquisition and retention, varying its strategies based on whether it's targeting businesses (B2B) or individual consumers (B2C). This approach includes both traditional methods and digital marketing techniques. The company focuses on building strong relationships with its customers through excellent service and tailored communications to boost customer loyalty.

For its B2B segment, the company likely uses direct sales teams and partnerships with brokers and consultants. In the B2C sector, digital marketing is a key driver, with a strong emphasis on online channels and partnerships. The company uses customer data and CRM systems to segment its audience and tailor marketing messages, improving the effectiveness of its campaigns. The goal is to increase customer acquisition and retention rates while adapting to changing market trends.

The company's customer acquisition and retention strategies include a focus on digital marketing, especially for its B2C products. This involves search engine optimization (SEO), pay-per-click (PPC) advertising, and social media campaigns, and partnerships with online insurance marketplaces. For retention, the focus is on transparent policy terms, streamlined processes, and responsive customer service. The IHC Group likely uses customer data and CRM systems to segment its audience and tailor marketing messages, improving the effectiveness of its campaigns.

The IHC Group likely uses direct sales teams and partnerships with brokers and consultants to acquire B2B customers. This strategy is particularly relevant for products like medical stop-loss insurance. Industry conferences and targeted digital advertising are also probable tactics for reaching HR professionals and business owners.

Retention in the B2B segment depends on strong account management, efficient claims processing, and demonstrating consistent value in mitigating high-cost claims. Providing excellent service and building long-term relationships are crucial for maintaining customer loyalty. This approach helps ensure customer satisfaction and reduces churn rates.

For B2C products like short-term medical insurance, the company relies heavily on digital marketing. This includes SEO, PPC advertising, and social media campaigns targeting individuals seeking immediate or temporary health coverage. Partnerships with online insurance marketplaces and lead generation services are also key.

Retention efforts in the B2C sector focus on transparent policy terms, streamlined renewal processes, and responsive customer service. Personalized communications and proactive outreach regarding policy changes or new offerings are also likely employed. The company uses customer data to segment its audience and tailor marketing messages.

Data-Driven Strategies

The IHC Group uses customer data and CRM systems to segment its audience and tailor marketing messages. This data-driven approach helps improve the effectiveness of its campaigns and personalize customer interactions. This strategy is crucial for understanding the Owners & Shareholders of The IHC Group and their needs.

- Market Segmentation: Dividing the market into distinct groups based on demographics, needs, and behaviors.

- Targeted Advertising: Creating specific ads for each segment to increase relevance and conversion rates.

- Personalized Communication: Tailoring messages to individual customers based on their profile and history.

- Customer Relationship Management (CRM): Using CRM systems to manage customer interactions and track engagement.

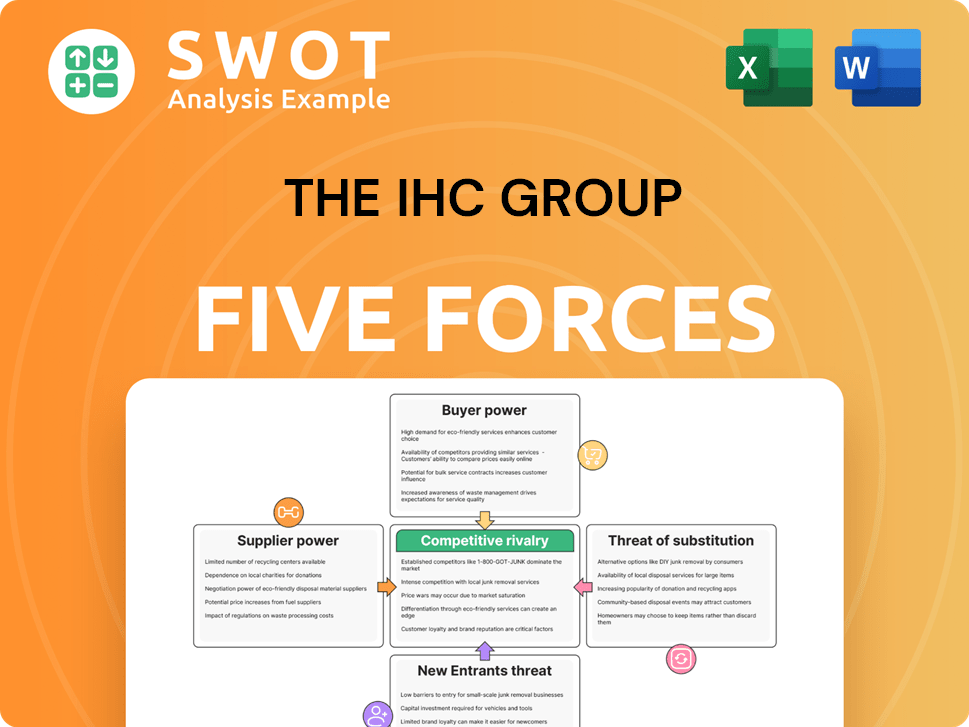

The IHC Group Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of The IHC Group Company?

- What is Competitive Landscape of The IHC Group Company?

- What is Growth Strategy and Future Prospects of The IHC Group Company?

- How Does The IHC Group Company Work?

- What is Sales and Marketing Strategy of The IHC Group Company?

- What is Brief History of The IHC Group Company?

- Who Owns The IHC Group Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.