The IHC Group Bundle

How Does the IHC Group Company Navigate the Insurance Landscape?

Independence Holding Company (IHC Group) is a key player in the U.S. insurance market, offering a diverse range of life, annuity, and health insurance products. With a history of strategic acquisitions and a focus on meeting evolving market needs, IHC Group has consistently demonstrated its influence. Understanding the inner workings of this The IHC Group SWOT Analysis is crucial for investors, customers, and industry observers alike.

This exploration will uncover the core operations of the IHC Group company, from its health insurance offerings to its reinsurance activities. We'll examine its value proposition, diverse revenue streams, and competitive advantages to provide a comprehensive understanding of how this insurance company thrives. Whether you're researching IHC Group insurance plans review or seeking details on IHC Group customer service contact, this analysis aims to provide valuable insights.

What Are the Key Operations Driving The IHC Group’s Success?

The IHC Group company operates by providing a range of insurance products designed to meet diverse needs. Their core offerings include medical stop-loss, group term life, short-term medical, and supplemental health insurance plans. These products are tailored for individuals, groups, and employers, ensuring comprehensive coverage options. The Competitors Landscape of The IHC Group reveals how it positions itself in the market.

The IHC Group insurance leverages in-house expertise and strategic partnerships to deliver its services. Their operational focus includes underwriting, claims processing, and policy administration, supported by advanced technological platforms. Distribution channels are diverse, including independent agents, brokers, and direct-to-consumer options, ensuring broad market reach. This approach allows the company to offer specialized and flexible insurance solutions.

The value proposition of IHC Group centers around providing specialized and flexible insurance solutions. This includes financial protection for self-funded employers through medical stop-loss products and accessible coverage options for individuals. Their operational efficiency and focused product development translate into enhanced financial security and cost containment for customers. The company's ability to fill gaps in the market differentiates it from larger insurance providers.

The IHC Group offers a variety of insurance products. These include medical stop-loss, group term life, short-term medical, and supplemental health insurance. These products cater to a wide range of needs, from employer health plans to individual coverage.

The company uses in-house expertise and strategic partnerships. They focus on underwriting, claims processing, and policy administration. Distribution includes independent agents, brokers, and direct channels. This ensures efficient service delivery and broad market access.

Offers specialized and flexible insurance solutions. Provides financial protection for self-funded employers. Offers accessible coverage options for individuals. Focus on operational efficiency and product development.

The IHC Group insurance targets both individuals and groups. They offer solutions for self-funded employers and those seeking individual or supplemental health plans. This broad approach allows them to address various market needs effectively.

Key Benefits of IHC Group Services

The IHC Group services provide several key benefits to its customers. These include specialized insurance solutions, financial protection, and cost containment. They aim to meet the diverse needs of individuals and businesses.

- Specialized insurance products tailored to specific needs.

- Financial protection through medical stop-loss and other plans.

- Cost containment and efficient service delivery.

- Accessible coverage options for individuals and groups.

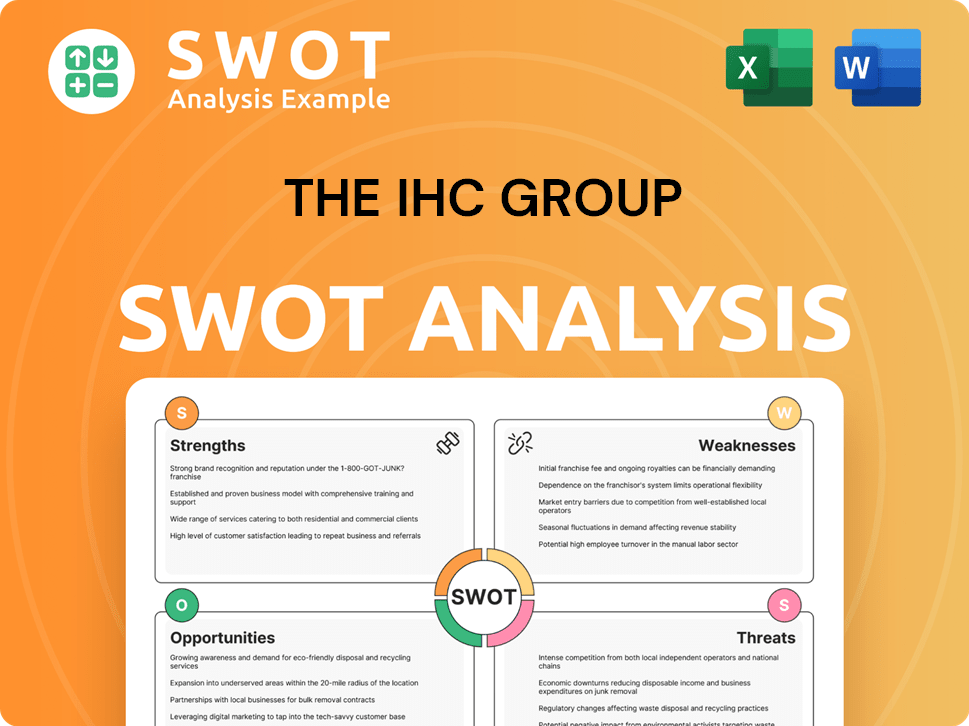

The IHC Group SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does The IHC Group Make Money?

The IHC Group's revenue streams are primarily derived from insurance premiums, reflecting its diverse offerings in life, annuity, and health insurance. As an insurance company, the IHC Group generates income by collecting premiums from various insurance products. The company's financial performance is significantly influenced by these premium revenues, which are essential for its operational sustainability and growth.

A substantial portion of the IHC Group's revenue comes from premiums earned on its insurance products. These include fully insured products like short-term medical, group life, and supplemental health, alongside medical stop-loss coverage. For instance, in Q1 2024, the IHC Group reported gross premiums written of $150.2 million, highlighting the ongoing revenue generation capacity. The medical stop-loss segment is a key contributor, with employers paying premiums to cover high-cost employee health claims.

Beyond direct premiums, the IHC Group also benefits from investment income derived from its investment portfolio. This is a standard practice in the insurance industry, where premiums are invested until claims are paid. While not the primary source of operating revenue, investment income is crucial for overall profitability. The company's monetization strategies involve tiered pricing for different coverage levels and cross-selling opportunities across its product lines, such as offering group life or supplemental health benefits to employers purchasing medical stop-loss.

Premium Revenue

The main revenue stream comes from insurance premiums. These premiums are collected from various insurance products offered by the IHC Group.

Product Lines

Key product lines include fully insured products (short-term medical, group life, supplemental health) and medical stop-loss. These products cater to different insurance needs.

Investment Income

Investment income from the company's portfolio also contributes to revenue. This is a standard practice in the insurance sector.

Monetization Strategies

Strategies include tiered pricing and cross-selling opportunities. For example, offering additional benefits to existing customers.

Reinsurance

Reinsurance services contribute to revenue through premiums ceded or assumed. This diversifies the financial base of the IHC Group.

Supplemental Products

Supplemental health products like dental, vision, critical illness, and accident insurance provide additional revenue streams for the IHC Group.

Key Revenue Components and Strategies

The IHC Group's financial success relies on a multifaceted approach to revenue generation and monetization. This involves various insurance products and strategic financial management. To learn more about the company's expansion, read about the Growth Strategy of The IHC Group.

- Premiums from diverse insurance products: This includes a range of offerings, such as short-term medical, group life, and supplemental health insurance.

- Medical stop-loss segment: A significant revenue source where employers pay premiums to cover high-cost employee health claims.

- Investment income: Generated from the company's investment portfolio, which plays a crucial role in overall profitability.

- Tiered pricing and cross-selling: Strategies to maximize revenue by offering different coverage levels and additional products.

- Reinsurance services: Contributing to revenue through premiums ceded or assumed, diversifying the financial base.

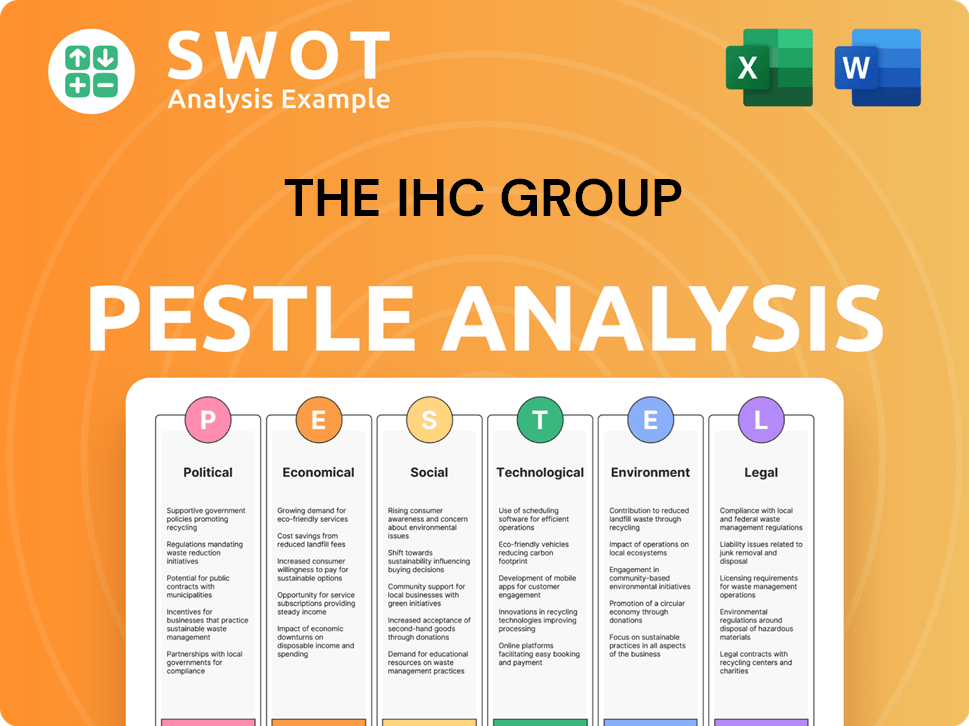

The IHC Group PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped The IHC Group’s Business Model?

The operational and financial journey of the IHC Group company has been shaped by strategic initiatives and adaptations to market changes. Instead of a single 'breakthrough product launch,' the company's history is marked by consistent product diversification and strategic acquisitions, expanding its market reach and strengthening its portfolio. The company has focused on expanding its presence in specialized insurance niches, such as medical stop-loss, which has proven to be a resilient and growing market segment.

Operational challenges for the IHC Group, similar to the broader insurance industry, can include evolving regulatory landscapes, healthcare cost inflation impacting claims, and intense competition. The company's response has typically involved disciplined underwriting, efficient claims management, and continuous product refinement to meet changing consumer and employer demands. For example, adapting to the Affordable Care Act (ACA) and subsequent regulatory shifts has been an ongoing process, requiring flexibility in product design and distribution.

The IHC Group's competitive advantages are multifaceted. Its brand strength, built over years of operation, fosters trust among policyholders and brokers. The company benefits from its specialized expertise in certain product lines, particularly medical stop-loss, which requires specific underwriting knowledge and risk assessment capabilities. Its diversified product portfolio provides a hedge against downturns in any single market segment. Furthermore, the company's robust distribution network, encompassing independent agents and brokers, provides extensive market penetration. IHC Group continues to adapt to new trends by focusing on digital transformation initiatives to enhance customer experience and operational efficiency, and by exploring new opportunities within the evolving healthcare and insurance ecosystems.

The IHC Group company has achieved significant milestones through strategic acquisitions and product diversification. These moves have broadened its market presence and strengthened its portfolio, particularly in specialized insurance niches. The company has consistently adapted to market dynamics, ensuring its continued growth and relevance in the insurance industry. For more insights, read about the Growth Strategy of The IHC Group.

Strategic moves by the IHC Group have included a focus on specialized insurance areas, such as medical stop-loss. The company has responded to evolving regulations and market changes through disciplined underwriting and product refinement. Digital transformation initiatives are also a key strategic focus, enhancing customer experience and operational efficiency.

The IHC Group's competitive edge stems from its brand strength, specialized expertise, and diversified product portfolio. A robust distribution network and digital transformation initiatives further enhance its market penetration and customer experience. These factors collectively position the IHC Group as a strong player in the insurance market.

While specific financial data for 2024 or 2025 is not available, the IHC Group’s performance is closely tied to its ability to manage risk, control costs, and adapt to market changes. The insurance industry faces ongoing challenges, including rising healthcare costs and regulatory changes. The company's success depends on its ability to navigate these challenges effectively.

Key Advantages of IHC Group

The IHC Group's advantages include brand recognition and specialized expertise in niches like medical stop-loss. Its diversified product offerings and robust distribution network provide a competitive edge. The company is also focused on digital transformation to improve customer service and operational efficiency.

- Strong brand reputation built over years of operation.

- Specialized knowledge in medical stop-loss insurance.

- A diversified product portfolio to mitigate risks.

- A wide distribution network for market reach.

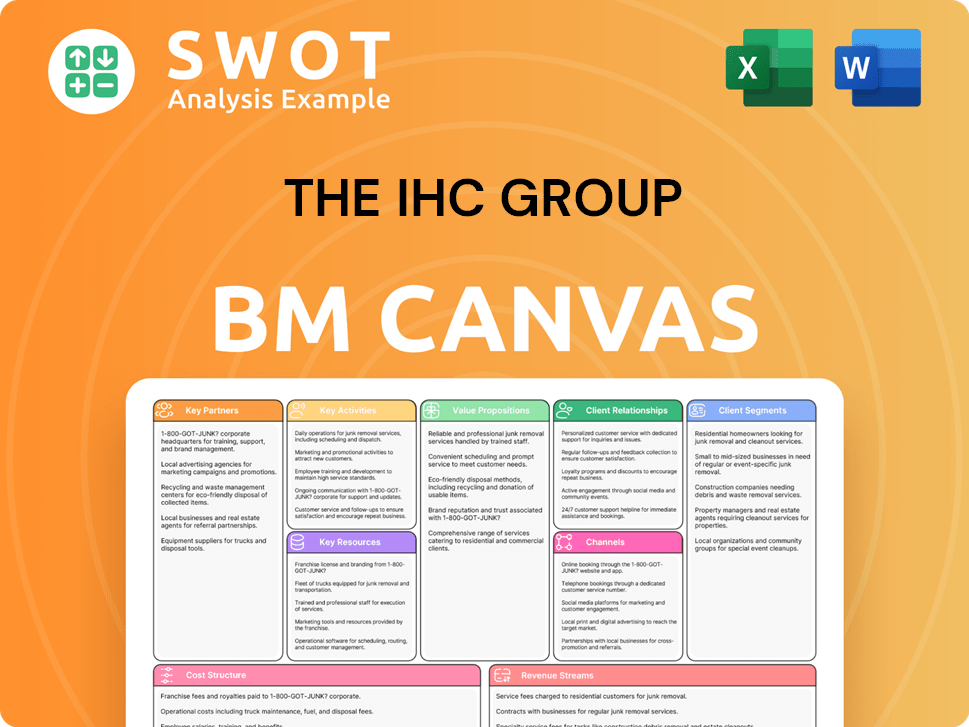

The IHC Group Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is The IHC Group Positioning Itself for Continued Success?

The IHC Group company holds a specialized position within the U.S. insurance sector, particularly in medical stop-loss insurance. While not a dominant player in overall market share, it maintains a significant presence in its niche, supported by tailored solutions and responsive service. This focus on specific market segments and client needs differentiates IHC Group insurance from larger, more diversified competitors.

The IHC Group's operations are primarily focused on the U.S. market, where it faces risks from regulatory changes, intense competition, and technological disruptions. The company must continually adapt to evolving consumer preferences and market shifts to maintain its competitive edge and financial performance. Understanding the nuances of the healthcare and insurance sectors is crucial for its strategic planning and operational success.

The IHC Group insurance company specializes in medical stop-loss insurance, holding a significant position in this niche market within the U.S. insurance industry. Its customer loyalty and tailored solutions are key to its market standing. The company's focus is primarily on the U.S. market, allowing for a concentrated approach to its operations and customer base.

Key risks include regulatory changes, intense competition, and technological disruption. Adapting to consumer preferences and market shifts is crucial. The insurance industry is subject to constant change, requiring continuous adaptation to maintain a competitive edge.

Strategic initiatives focus on medical stop-loss, supplemental health offerings, and technology. Emphasis is placed on prudent underwriting, disciplined capital management, and strategic partnerships. Continued investment in digital platforms is critical for future growth and profitability.

The IHC Group company aims to capitalize on its expertise, diversify its product portfolio, and proactively adapt to market changes. This approach is designed to sustain and expand its ability to generate revenue. The company's strategic focus is critical for long-term growth and success.

Strategic Initiatives and Market Adaptation

The IHC Group is likely to concentrate on expanding its supplemental health offerings and leveraging technology to improve operational efficiency. The company's approach involves prudent underwriting and strategic partnerships to navigate the dynamic insurance landscape. For example, the company will continue to invest in digital platforms for policy administration and claims processing.

- Expansion of supplemental health offerings to meet evolving consumer demands.

- Investment in digital platforms for policy administration and claims processing.

- Focus on prudent underwriting and disciplined capital management.

- Exploring synergistic partnerships to enhance market reach and service capabilities.

To gain a deeper understanding of the specific market segments and customer profiles that IHC Group targets, you can explore the Target Market of The IHC Group.

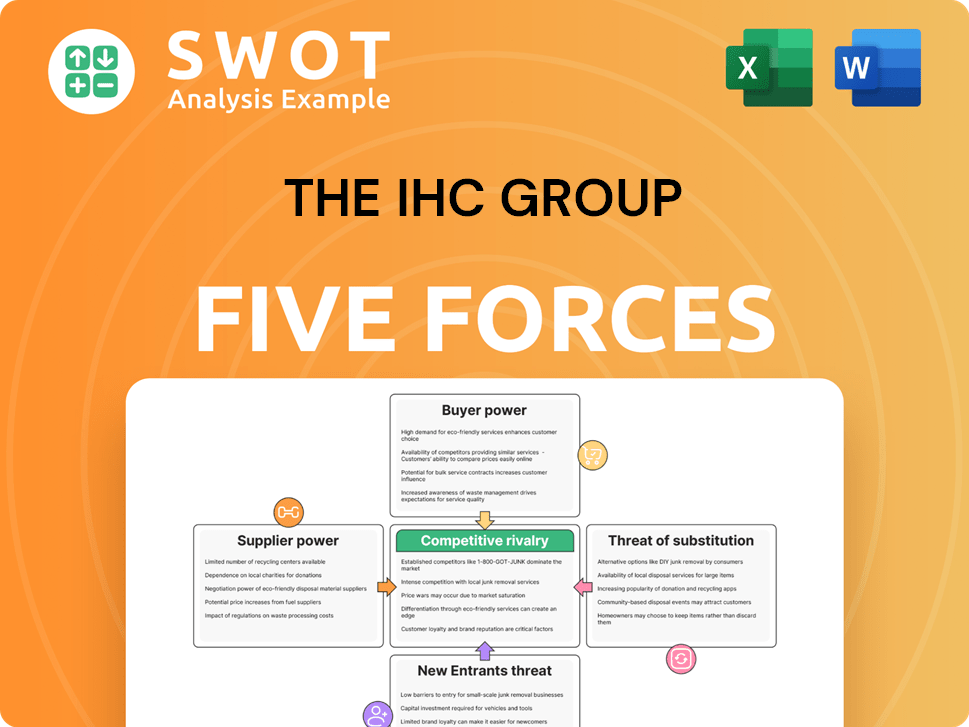

The IHC Group Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of The IHC Group Company?

- What is Competitive Landscape of The IHC Group Company?

- What is Growth Strategy and Future Prospects of The IHC Group Company?

- What is Sales and Marketing Strategy of The IHC Group Company?

- What is Brief History of The IHC Group Company?

- Who Owns The IHC Group Company?

- What is Customer Demographics and Target Market of The IHC Group Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.