Upstart Bundle

Can AI Revolutionize Lending: A Look at Upstart?

Upstart, a leading fintech innovator, is reshaping the lending landscape with its AI-driven approach. By utilizing artificial intelligence and machine learning, Upstart is not only redefining credit risk assessment but also expanding access to personal loans for a wider audience. This shift towards a more data-driven model is challenging traditional financial institutions and opening up new possibilities for borrowers.

Upstart's Upstart SWOT Analysis reveals the company's strengths and weaknesses in a competitive market. Understanding the Upstart platform and how it assesses risk is crucial for anyone considering Upstart loans or evaluating the future of fintech. This article will explore how Upstart operates, from its loan application process to its impact on interest rates and customer service, providing a comprehensive Upstart loan review.

What Are the Key Operations Driving Upstart’s Success?

The core operations of the company revolve around its AI-powered lending platform. This platform connects borrowers seeking personal loans with a network of lending partners. The company's value proposition is centered on a more inclusive and efficient credit assessment process compared to traditional FICO-based models.

The company's platform analyzes over 1,600 data points, including education, employment, and financial behavior, to build a more comprehensive picture of a borrower's credit risk. This approach aims to increase approval rates for qualified borrowers who might be overlooked by conventional lending criteria and potentially offer them lower interest rates. The company does not directly lend money; instead, it acts as an intermediary, facilitating the loan origination process for its bank and credit union partners.

The operational process begins when a borrower applies for a loan through the company's online platform. The company's AI models instantly assess the applicant's creditworthiness and, if approved, match them with a suitable lending partner from its network. This involves handling the initial application, risk assessment, and verification, streamlining the process for both borrowers and lenders. This unique operational model allows the company to differentiate itself by offering a faster, more accessible, and potentially more affordable lending solution.

The company's core operation centers on its AI-powered lending platform, which connects borrowers with lending partners. This platform uses advanced algorithms to assess creditworthiness, going beyond traditional FICO scores. The company's approach aims to provide a more inclusive and efficient credit assessment process.

The company's value lies in its ability to offer a more inclusive and efficient credit assessment. By analyzing a wide range of data points, the company aims to provide access to credit for a broader range of borrowers. This approach can potentially lead to lower interest rates for qualified applicants.

The process starts with a borrower applying for a loan through the online platform. The company's AI models assess the applicant's creditworthiness instantly. If approved, the applicant is matched with a lending partner, streamlining the loan origination process.

The company's proprietary AI models continuously learn and improve their predictive accuracy. The company's supply chain is primarily digital, focusing on data acquisition and model development. This model offers a faster, more accessible, and potentially more affordable lending solution.

Key Features and Benefits of the Company

The company's platform offers several key features and benefits, including a streamlined loan application process and the potential for lower interest rates. The company's use of AI allows for a more comprehensive assessment of creditworthiness, which can benefit both borrowers and lenders. Understanding the Growth Strategy of Upstart provides further insights into its operational model.

- Faster loan approval process.

- Potentially lower interest rates.

- Broader access to credit for qualified borrowers.

- Efficient and data-driven credit assessment.

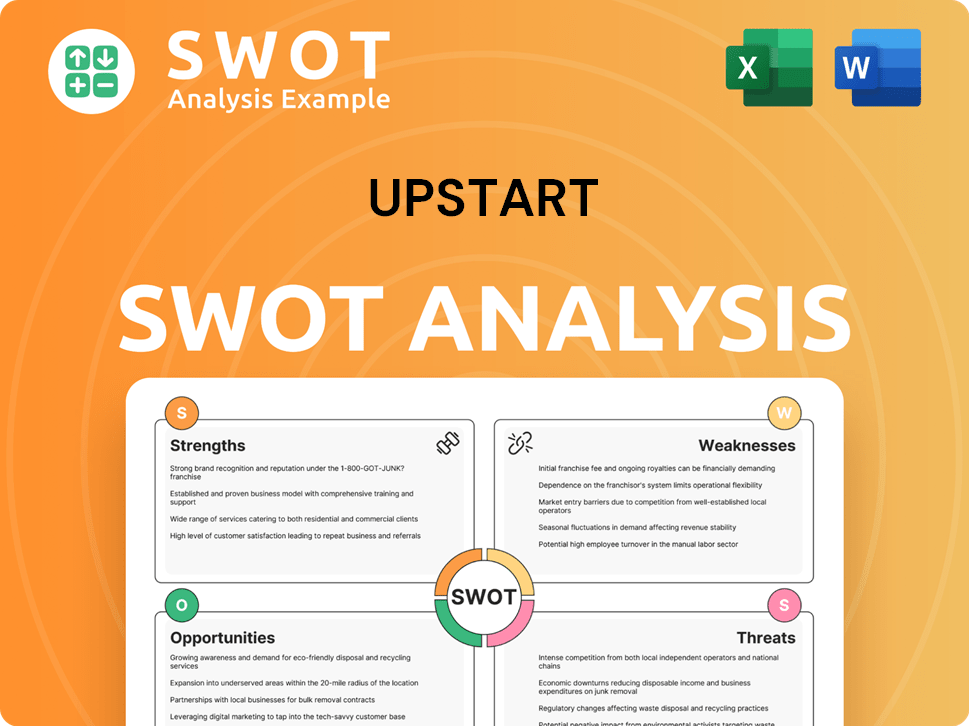

Upstart SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Upstart Make Money?

Understanding the revenue streams and monetization strategies of a company like Upstart is crucial for investors and anyone interested in the fintech sector. The company has developed a unique approach to lending, which is reflected in its financial model. This model is designed to generate revenue while minimizing risk.

The core of Upstart's revenue generation revolves around its role in facilitating loans. The company employs a multi-faceted approach, primarily earning through referral and servicing fees. These fees are derived from the loans originated and managed through its platform.

Upstart's primary revenue streams are referral fees and servicing fees. Referral fees are earned from its bank partners for each loan originated through the Upstart platform. Servicing fees are generated from managing loan payments, customer inquiries, and collections on behalf of its lending partners.

Revenue Streams in Detail

Upstart's financial success is rooted in its ability to generate revenue through several key avenues. The company's model allows it to scale operations effectively. The platform's expansion into new loan categories also contributes to its revenue diversification.

- Referral Fees: Upstart receives a referral fee, typically a percentage of the loan principal, from its bank partners for each loan originated on the platform. This is a direct result of the company's ability to connect borrowers with lenders.

- Servicing Fees: Upstart earns servicing fees by managing loans on behalf of its lending partners. This includes handling loan payments, customer service, and collections. This provides a recurring revenue stream.

- Platform Fees: Upstart offers a 'platform fee' to some lending partners, where it provides the technology and AI models, while the bank handles funding and servicing. This approach allows Upstart to scale without taking on significant balance sheet risk.

- Expansion into New Loan Categories: Expanding into new loan categories, such as auto loans, allows Upstart to tap into larger markets and apply its AI-driven risk assessment to a wider range of credit products. This strategy potentially increases transaction volume and associated fees.

In its Q4 2023 earnings report, Upstart reported total revenue of $140.5 million. This financial performance underscores the effectiveness of its revenue model. The company's strategic initiatives, including the expansion into auto loans, are expected to further diversify its revenue streams and enhance its market position.

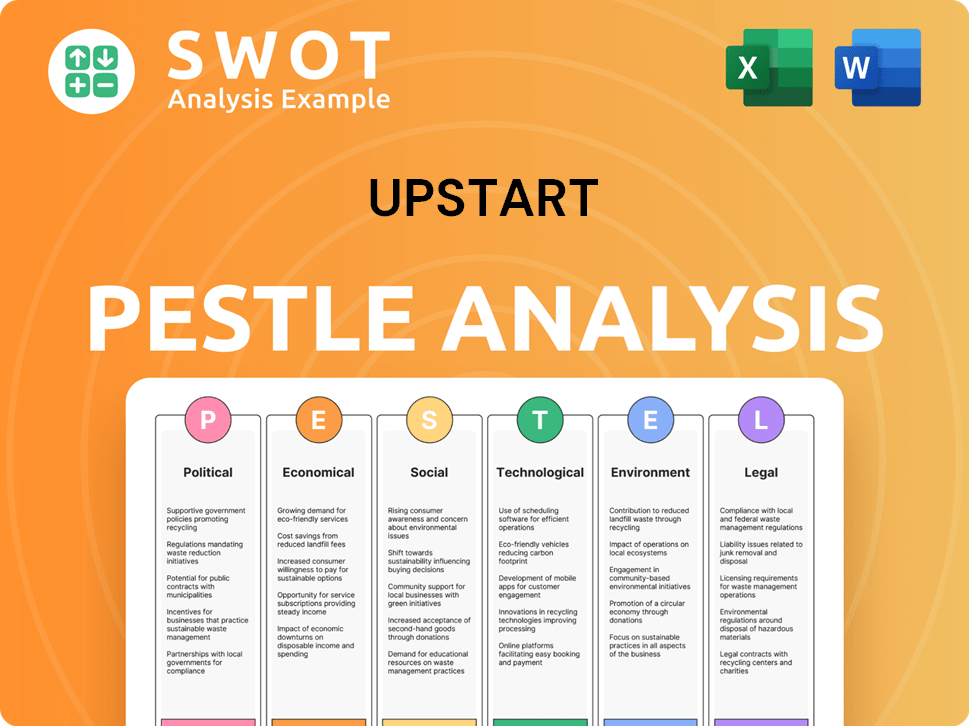

Upstart PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Upstart’s Business Model?

The journey of Upstart has been marked by significant milestones, notably its initial public offering (IPO) in December 2020. This event provided substantial capital for growth and increased its visibility. The company has continuously refined and expanded its AI models, which has been crucial for improving loan approval rates and risk assessment accuracy. Strategic moves include its expansion beyond personal loans into the auto loan market, diversifying its product offerings.

Upstart has faced operational challenges, particularly during economic uncertainty, which can impact lending volumes. However, the company has responded by focusing on its core AI technology, demonstrating the adaptability of its models to changing economic conditions. Upstart's competitive edge lies in its proprietary AI and machine learning algorithms, which are difficult for competitors to replicate. This technology allows Upstart to assess risk more effectively than traditional credit bureaus.

Furthermore, its growing network of bank and credit union partners creates a strong ecosystem effect, making its platform more valuable for both borrowers and lenders. Upstart continues to adapt to new trends by investing in research and development to enhance its AI capabilities and explore new lending verticals. You can learn more about the company's origins in this Brief History of Upstart.

The IPO in December 2020 was a crucial milestone, providing capital for expansion. Continuous improvements to AI models have enhanced loan approval rates. Expansion into auto loans has broadened product offerings and market reach.

Diversification into auto loans represents a key strategic move for growth. Focusing on core AI technology has helped navigate economic fluctuations. Partnerships with banks and credit unions create a strong ecosystem.

Proprietary AI and machine learning algorithms provide a significant advantage. These algorithms enable more effective risk assessment. The platform's value is enhanced by its network of partners.

Economic downturns can impact lending volumes, posing operational challenges. The company has adapted by focusing on its core AI technology. Investment in R&D is ongoing to enhance AI capabilities.

Upstart's AI Advantage

Upstart's use of AI allows for more accurate risk assessment compared to traditional methods. This leads to higher approval rates for borrowers and potentially lower loss rates for lenders. The AI models analyze a wide range of data points beyond traditional credit scores.

- Higher Approval Rates: Upstart's platform often approves borrowers who might be rejected by traditional lenders.

- Lower Interest Rates: The AI can identify borrowers who are less risky, potentially leading to lower interest rates.

- Improved Risk Management: The AI models continuously learn and adapt, improving risk assessment over time.

- Data-Driven Decisions: The platform uses a comprehensive set of data to make lending decisions.

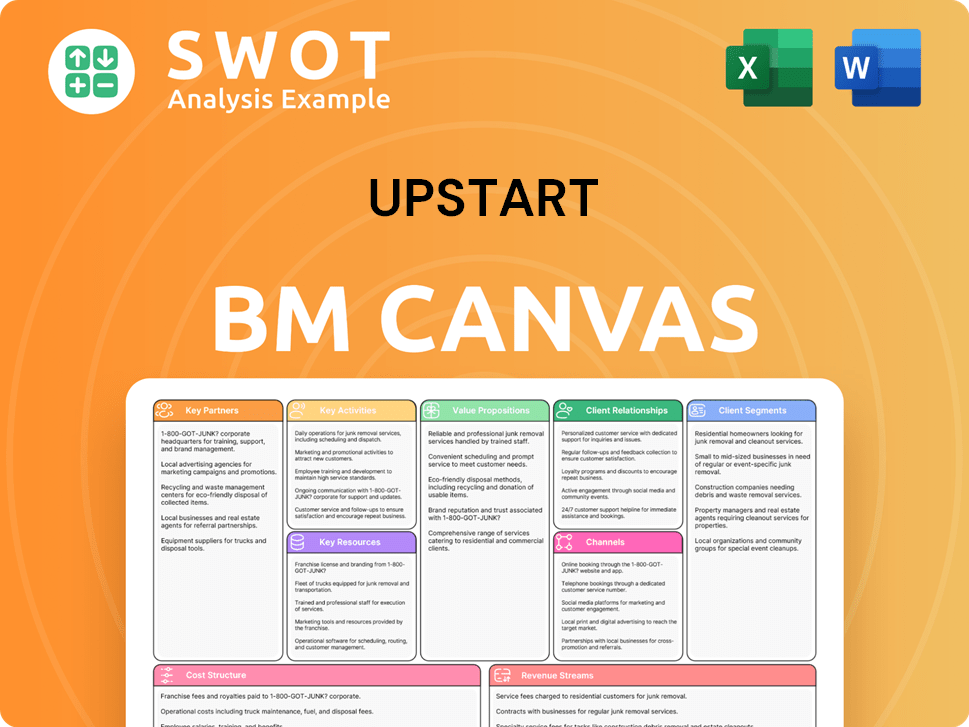

Upstart Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Upstart Positioning Itself for Continued Success?

In the fintech lending space, Upstart holds a distinctive position, primarily due to its AI-driven approach to credit assessment. Unlike traditional banks that heavily rely on FICO scores, the ability of Upstart to analyze numerous alternative data points gives it a competitive edge. This enables them to reach underserved borrower segments and offer potentially more competitive rates. The company's market share is growing, particularly in personal and auto loans, where its technology allows for more efficient risk pricing.

However, Upstart faces several risks. Regulatory changes regarding fair lending practices and data privacy could impact its operational model. The emergence of new competitors with similar AI capabilities or a shift in investor sentiment towards riskier assets could also pose challenges. Furthermore, economic downturns or rising interest rates could reduce loan demand and increase default rates, directly impacting Upstart's revenue and profitability.

Upstart leverages AI to assess creditworthiness, setting it apart from traditional lenders. This approach allows for more inclusive lending practices. The company's focus on technology and data analytics has positioned it as a key player in the fintech industry. Upstart's platform is known for its user-friendly interface, which enhances the customer experience.

Regulatory changes and data privacy concerns pose significant risks to Upstart's operations. Economic downturns and rising interest rates could negatively affect loan demand and increase default rates. Competition from other fintech companies with similar AI capabilities is also a threat. Changes in investor sentiment towards riskier assets could impact Upstart's funding.

Upstart plans to expand its AI models into new asset classes and deepen relationships with lending partners. The company is focused on improving its AI's efficiency and accuracy to maintain its competitive edge. Leadership emphasizes responsible lending and democratizing access to credit. The future depends on innovation, regulatory navigation, and economic management.

Upstart offers personal loans, auto loans, and is exploring mortgages. The company aims to provide accessible and competitive loan products. The Upstart platform is designed to streamline the loan application process. For those considering their options, understanding the Competitors Landscape of Upstart can be beneficial.

Key Strategic Initiatives

Upstart's strategic initiatives include expanding its AI models into new areas, such as mortgages, and strengthening partnerships. The company is focused on enhancing its AI to maintain a competitive edge. Leadership is committed to responsible lending practices.

- Expansion into new asset classes.

- Enhancement of AI models.

- Strengthening partnerships with lenders.

- Focus on responsible lending.

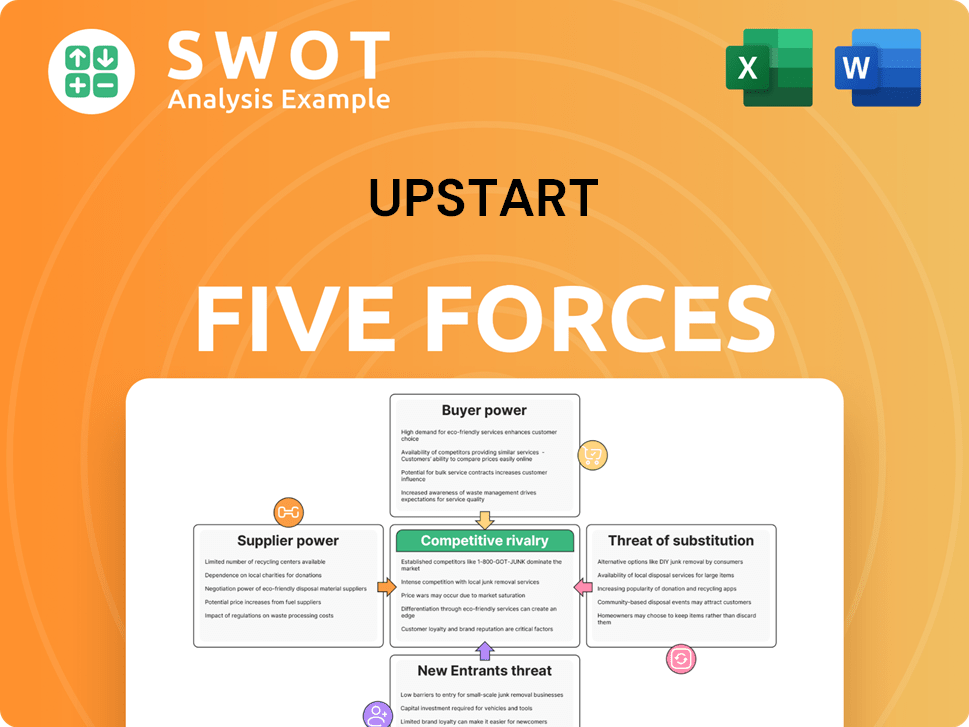

Upstart Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Upstart Company?

- What is Competitive Landscape of Upstart Company?

- What is Growth Strategy and Future Prospects of Upstart Company?

- What is Sales and Marketing Strategy of Upstart Company?

- What is Brief History of Upstart Company?

- Who Owns Upstart Company?

- What is Customer Demographics and Target Market of Upstart Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.