Upstart Bundle

How Did Upstart Revolutionize Lending?

In the fast-paced world of fintech, the Upstart SWOT Analysis reveals a fascinating story of innovation. This Upstart company, born from the vision of former Google employees, has dramatically reshaped how we think about credit. Let's dive into the brief history of this Upstart journey.

From its business origins in 2012, Upstart's company evolution has been nothing short of remarkable. The Startup quickly distinguished itself by leveraging AI to assess creditworthiness, moving beyond traditional methods. Understanding the Upstart company's early days is key to grasping its significant impact on the lending industry and its impressive growth trajectory.

What is the Upstart Founding Story?

The Upstart company, a prominent player in the fintech sector, has an intriguing

Brief history

that began with a vision to revolutionize lending. TheUpstart

journey started in April 2012, with a clear goal to leverage technology and data to transform the way loans are assessed and offered.The

Upstart company

was founded by Dave Girouard, Anna Counselman, and Paul Gu. Girouard, bringing his experience as a former President of Enterprise Google, provided leadership, while Gu, a Thiel Fellow, and Counselman, with her background in Google's operations, brought crucial expertise in technology and operations. This combination of skills set the stage for their entry into the financial technology space.The founders identified a significant flaw in the traditional lending system: the over-reliance on FICO scores, which often excluded creditworthy individuals. They aimed to create a more accurate and fair loan approval process using AI and machine learning.

Early Days of Upstart

The

Upstart

Startup

initially launched with an 'Income Share Agreement' (ISA) product.- The ISA allowed individuals to raise money by sharing a percentage of their future income.

- This model gained some initial traction and was even featured in The New York Times.

- However, the anticipated scale of the ISA model did not materialize as expected.

- In May 2014, Upstart pivoted to a personal loan marketplace.

The shift to a personal loan marketplace in May 2014 marked a

Company evolution

forUpstart

. This new model offered traditional 3-year and 5-year loans. The company developed an income and default prediction model that incorporated a wider range of data, including education, area of study, GPA, and work history, in addition to traditional underwriting criteria. The initial funding forUpstart

included a seed round in 2012, followed by a Series A round.By 2024,

Upstart

had facilitated over $40 billion in loans. The company's revenue for 2024 was approximately $600 million, demonstrating significant growth since its inception. TheBusiness origins

ofUpstart

laid the foundation for its current success in the lending industry, with its innovative approach to assessing creditworthiness. TheUpstart company

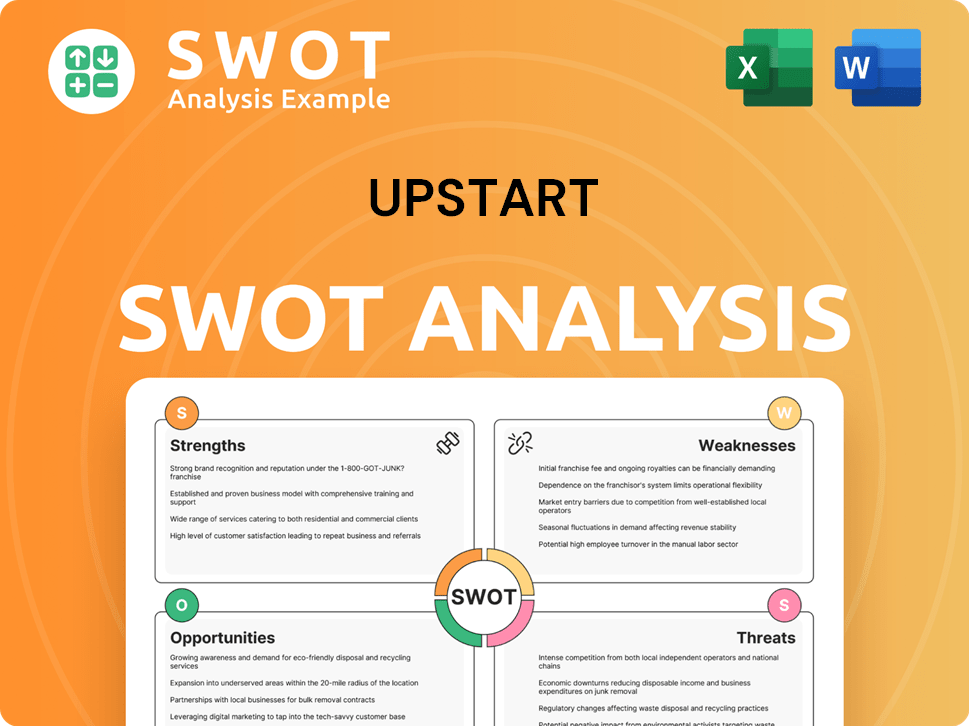

continues to evolve, adapting to market changes and technological advancements.Upstart SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of Upstart?

The early growth and expansion of the Upstart company following its pivot to the personal loan marketplace in May 2014, was marked by significant milestones. This period was characterized by strategic partnerships and diversification of product offerings. The company's innovative approach to credit assessment fueled faster approvals and competitive rates. Upstart's growth trajectory reflects its efforts to scale operations and penetrate new markets.

Securing its first major bank partnership in 2014 was a key milestone for Upstart's marketplace model. By 2016, the company had originated $100 million in loans, demonstrating growing demand for its AI-powered lending solutions. A significant portion of loans were automated, with 91% of Upstart's loans fully automated in the fourth quarter of 2024.

Upstart expanded its product offerings beyond personal loans, including auto loans, home equity lines of credit (HELOC), and small-dollar relief loans. In the fourth quarter of 2024, auto originations jumped 60%, HELOCs grew 60%, and small-dollar loans surged 115% quarter over quarter. This diversification aimed to tap into various consumer lending segments and reduce reliance on personal loans.

Upstart focused on expanding its market reach through strategic partnerships. In December 2024, First Commonwealth Federal Credit Union partnered with Upstart to expand personal loan access. In early April 2025, Upstart signed its first committed capital arrangement with Fortress Investment Group, agreeing to purchase up to $1.2 billion in consumer loans.

For the full year 2024, Upstart's total revenue was $637 million, up 24% year-over-year, with 697,092 loans originated totaling $5.9 billion, an increase of 28% year-over-year. The company's conversion rate improved to 16.5% in 2024, up from 9.7% in 2023. In the first quarter of 2025, Upstart reported total revenue of $213 million, up 67% year-over-year, and total originations of over $2.1 billion, reflecting a 19.1% conversion rate.

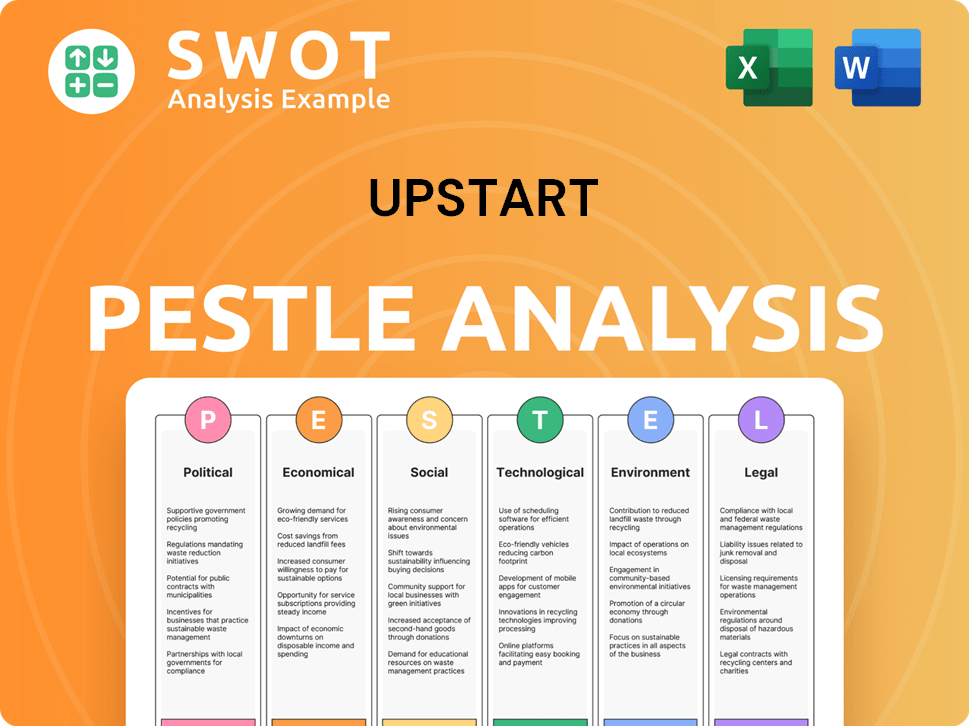

Upstart PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in Upstart history?

The Upstart company has seen significant milestones since its inception, driven by its innovative approach to lending. These achievements reflect its growth and impact on the financial sector.

| Year | Milestone |

|---|---|

| 2018 | Upstart went public on NASDAQ under the ticker symbol UPST. |

| 2020 | The company surpassed $1 billion in originated loans, demonstrating its increasing influence in the lending market. |

| Q4 2024 | Upstart launched 'Model 19,' a new credit pricing model that incorporates APR and generates approximately 1 million predictions per applicant. |

| May 14, 2025 | Upstart hosted its inaugural 'AI Day' in New York City to highlight its AI technology and business strategy, with CEO Dave Girouard outlining a vision to become the 'everything store for credit'. |

Upstart's innovations center on its AI-driven credit assessment model. This model utilizes over 90 million data points and analyzes 1,600 variables to evaluate creditworthiness, significantly improving risk accuracy compared to traditional systems.

AI-Driven Credit Assessment

The AI model uses over 90 million data points and analyzes 1,600 variables to assess creditworthiness.

Improved Approval Rates

The AI model enables 44% more borrowers to be approved than traditional credit models.

Lower APRs

The AI model approves borrowers at 36% lower APRs than traditional credit models.

Reduced Defaults

The AI model results in 53% fewer defaults at the same approval rate.

Automation

92% of loans are fully automated, eliminating human bias and accelerating decisions.

Model 19

The new credit pricing model integrates Annual Percentage Rate (APR) as a key feature and generates approximately 1 million predictions for each applicant.

Upstart has faced challenges, particularly due to economic uncertainties and market volatility. The company's stock experienced a decline after its IPO, and its business model is affected by interest rate changes and consumer spending.

Economic Uncertainty

Rising interest rates and inflationary pressures have impacted the company's performance.

Market Volatility

The cyclical nature of its business model means revenue and earnings can be affected by changes in interest rates and consumer spending.

Funding Challenges

Maintaining a stable and diverse funding base has been a key challenge, as the asset-backed securities (ABS) market has been volatile.

Stock Performance

After an initial surge following its IPO in late 2020, the stock experienced a steep decline amid rising interest rates and inflationary pressures in 2023.

Competition

Upstart operates in a competitive lending market, facing challenges from both traditional financial institutions and other fintech companies.

Regulatory Changes

Changes in lending regulations can impact Upstart's operations and compliance costs.

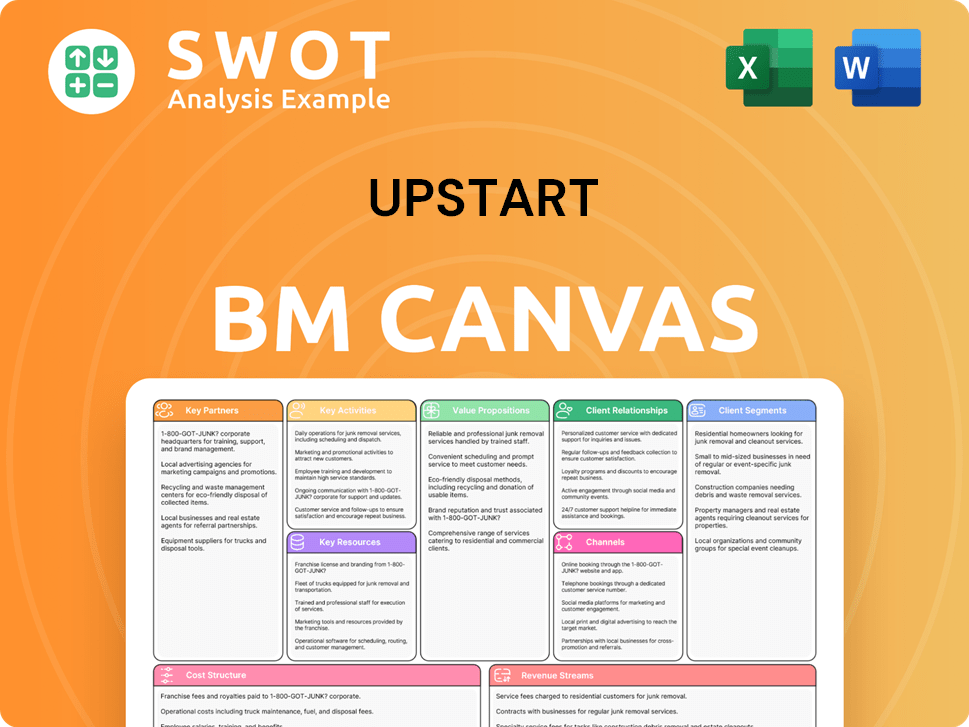

Upstart Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for Upstart?

The Upstart company has a fascinating journey. From its early days as a startup, it has evolved significantly. Initially focused on Income Share Agreements (ISAs), the company transitioned to a personal loan marketplace. This shift marked a pivotal moment in its business origins. The company's founders, Dave Girouard, Anna Counselman, and Paul Gu, set out to redefine lending using AI.

| Year | Key Event |

|---|---|

| April 2012 | Upstart is founded, launching with an Income Share Agreement (ISA) product. |

| May 2014 | Upstart pivots from ISAs to a personal loan marketplace, changing its business model. |

| 2016 | The company reaches $100 million in loans originated, demonstrating early growth. |

| 2018 | Upstart goes public on the NASDAQ under the ticker symbol UPST, a significant milestone. |

| 2020 | Upstart surpasses $1 billion in loans originated, reflecting substantial expansion. |

| Q4 2024 | Reports total revenue of $219 million, up 56% year-over-year, and originates 245,663 loans totaling $2.1 billion; launches 'Model 19'. |

| December 2024 | Partners with First Commonwealth Federal Credit Union to expand personal loan access. |

| February 11, 2025 | Announces Q4 and full-year 2024 financial results, projecting $1 billion in revenue for full-year 2025. |

| April 2025 | Signs a committed capital arrangement with Fortress Investment Group to purchase up to $1.2 billion in consumer loans. |

| May 6, 2025 | Announces Q1 2025 financial results, with total revenue of $213 million (up 67% YoY) and total originations exceeding $2.1 billion (up 89% YoY). |

| May 14, 2025 | Hosts its inaugural 'AI Day,' highlighting its AI-powered lending platform and future strategy. |

Upstart anticipates approximately $1.01 billion in revenue for the full year of 2025. The company's revenue from fees is projected to be around $920 million. This reflects significant growth and market penetration.

The company aims to return to GAAP net income profitability in the second half of 2025. It also expects to be profitable for the full calendar year. This demonstrates a positive financial trajectory.

Upstart plans to expand into new lending segments, such as auto and student loans. It will continue investing in technology to improve user experience. Strategic partnerships with banks and credit unions are crucial.

Analyst predictions for Upstart's stock price in 2025 vary. Some estimates reach $108.00, driven by revenue growth. Conservative estimates suggest a price target around $14.00, due to stock volatility.

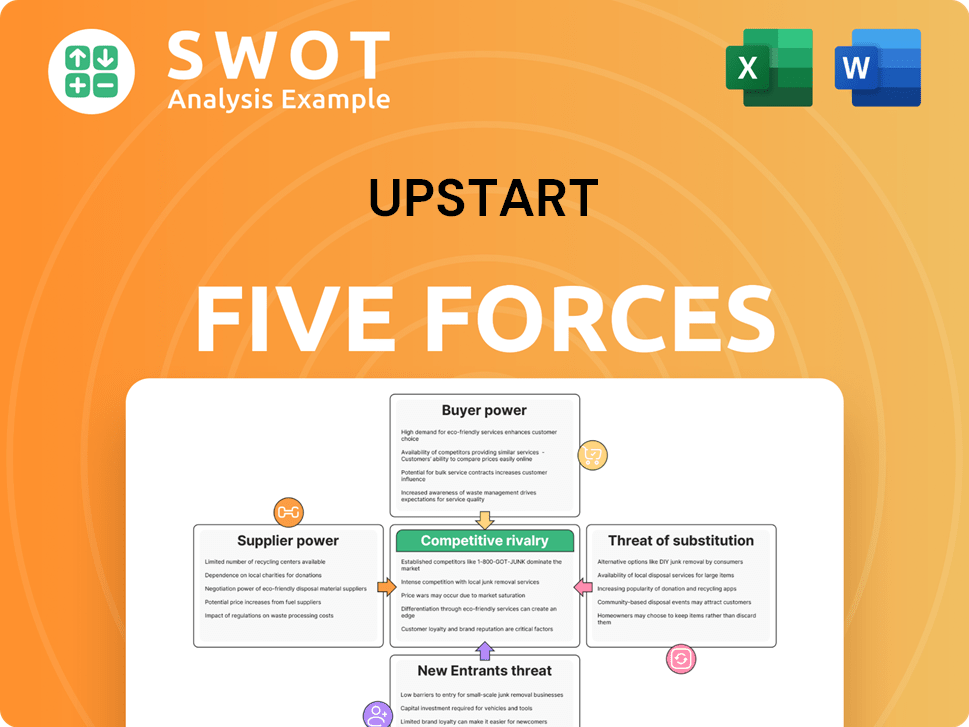

Upstart Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of Upstart Company?

- What is Growth Strategy and Future Prospects of Upstart Company?

- How Does Upstart Company Work?

- What is Sales and Marketing Strategy of Upstart Company?

- What is Brief History of Upstart Company?

- Who Owns Upstart Company?

- What is Customer Demographics and Target Market of Upstart Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.