Uniqa Bundle

How Does the Uniqa Company Thrive in a Competitive Market?

UNIQA Insurance Group AG, a European insurance powerhouse, boasts a rich history and a vast customer base. With a presence across 17 countries and a portfolio encompassing life, health, and property and casualty insurance, understanding the inner workings of Uniqa SWOT Analysis is key to grasping its success. This article unravels the strategies behind UNIQA's impressive financial performance and market position.

Delving into the specifics, you'll discover how Uniqa insurance generates revenue through its diverse Uniqa services and Uniqa financial products. We'll explore Uniqa policies, analyze Uniqa customer service and the company's strategic initiatives. Whether you're curious about Uniqa insurance contact number, seeking insights from a Uniqa car insurance review, or exploring Uniqa health insurance plans, this analysis provides a comprehensive view of the Uniqa company.

What Are the Key Operations Driving Uniqa’s Success?

The Uniqa Insurance Group AG delivers value through its diverse insurance products. These include life, health, and property and casualty (P&C) insurance, catering to retail, corporate, and banking clients. Their operations are supported by a strong direct insurer model, especially in Austria and Central and Eastern Europe (CEE).

Uniqa focuses on operational efficiency through strategic initiatives. They've modernized their IT landscape and streamlined financial processes. This includes implementing SAP S/4HANA Finance across multiple countries to standardize finance and controlling platforms.

Uniqa's distribution networks are extensive, using hired sales forces, agencies, brokers, banks, and direct sales. Collaboration with banks enables integrated financial services. This multi-channel approach, combined with strong risk management, contributes to their operational effectiveness. Geographic diversification, with a significant portion of Gross Written Premiums (GWP) from international markets, provides market differentiation and resilience.

Uniqa offers a wide array of insurance products. These include life insurance to cover economic risks, health insurance for medical needs, and P&C insurance, such as car and commercial property coverage. Their offerings are designed to meet the diverse needs of various customer segments.

Uniqa streamlines operations through technology and process improvements. They've implemented SAP S/4HANA Finance, standardizing financial processes. Robotic Process Automation (RPA) is used to automate transactions, improving efficiency and reducing supervision time.

Uniqa utilizes a multi-channel distribution strategy. This includes a hired sales force, general agencies, brokers, banks, and direct sales. Partnerships with banks enable integrated financial services through digital platforms.

Uniqa emphasizes risk management and underwriting discipline. Uniqa Re, a licensed reinsurer, manages group-internal reinsurance business. This contributes to effective risk and capital management within the group.

Key Benefits and Features

Uniqa's core capabilities translate into customer benefits through tailored solutions and efficient service delivery. Their geographic diversification, with 39% of Gross Written Premiums (GWP) coming from international markets, provides market differentiation and resilience. To learn more about the company's history, you can read this article about Uniqa.

- Comprehensive insurance products across life, health, and P&C.

- Streamlined financial processes with SAP S/4HANA Finance.

- Multi-channel distribution network for customer accessibility.

- Strong risk management practices.

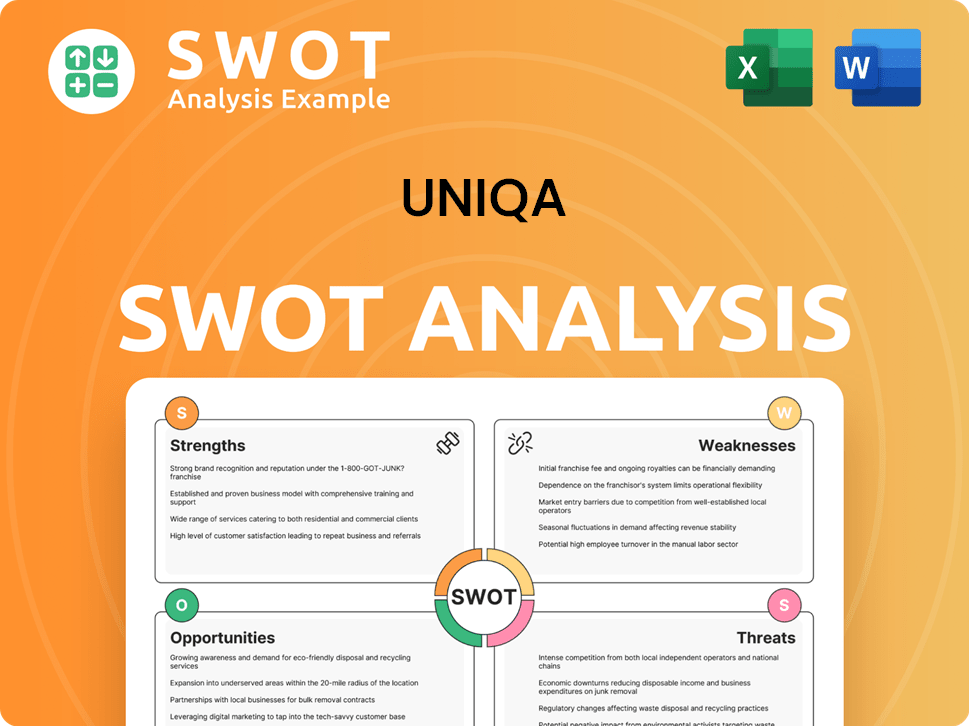

Uniqa SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Uniqa Make Money?

The Uniqa company generates revenue primarily through premiums from its insurance products, including property and casualty, life, and health insurance. This diversified approach allows Uniqa insurance to capture a broad market and mitigate risks associated with any single product line. In addition to premiums, Uniqa services also include investment income from its asset base, contributing to its overall financial performance.

In 2024, Uniqa's total premium volume, including savings portions from unit-linked and index-linked life insurance, reached €7,839.7 million, marking a 9.1% increase. This growth reflects the company's strong market position and effective monetization strategies. The company's strategic program 'UNIQA 3.0 - Growing Impact,' launched in 2025, aims for an average annual premium growth of 5% and an increase in net result by an average of 6%.

The company's insurance revenue, in accordance with IFRS 17, increased by 9.4% in 2024 to €6,557.2 million. In the first quarter of 2025, insurance revenue rose by 10.3% to €1,751.2 million. This demonstrates the company's continued ability to grow its core business and generate consistent revenue streams.

Key Revenue Streams and Performance Indicators

The following data highlights the key revenue streams and performance indicators for Uniqa insurance:

- In 2024, property and casualty insurance accounted for 59.7% of the total premium volume, with premiums written reaching €4,678.3 million, an increase of 11.0%.

- Life insurance contributed 20.9% of the total premium volume, with premiums written of €1,634.9 million, an increase of 3.3%.

- Health insurance premiums written rose by 10.0% to €1,526.5 million.

- In the first quarter of 2025, property and casualty insurance accounted for approximately 65% of the Group's total premium volume, with an extraordinary growth of 17.5%.

- Health insurance premiums written grew by 6.3% to €411.6 million, and life insurance saw a 16.2% increase in insurance revenue in Q1 2025.

- Net investment income fell to €108.8 million in the first three months of 2025.

- The overall financial result amounted to €21.1 million in the first three months of 2025.

For more details on Uniqa's strategic direction, consider reading about Growth Strategy of Uniqa.

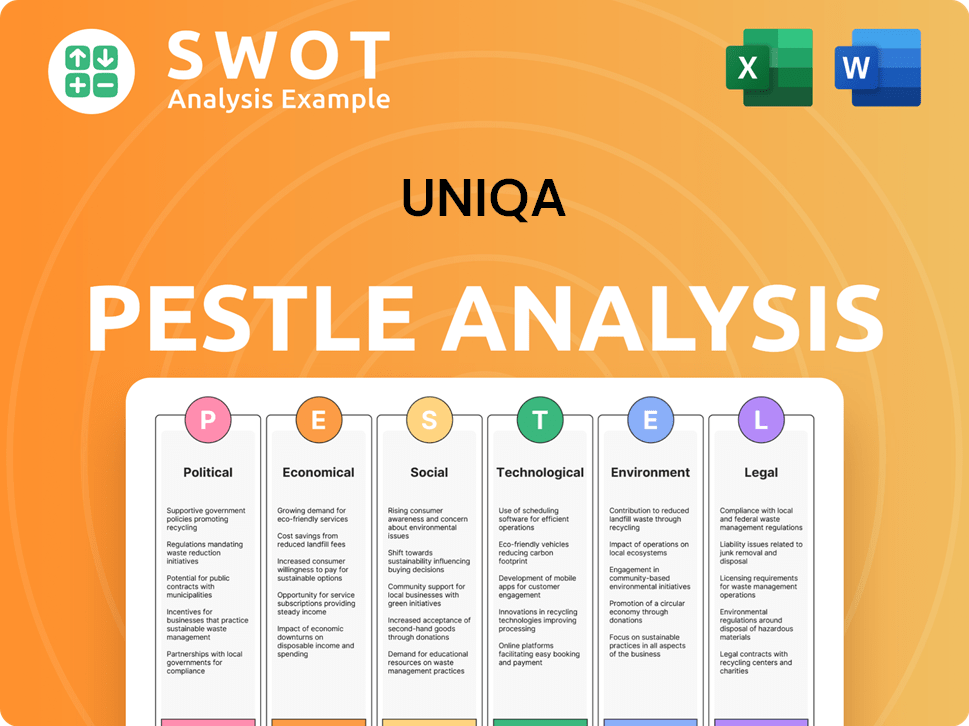

Uniqa PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Uniqa’s Business Model?

UNIQA Insurance Group AG has strategically navigated the evolving insurance landscape, marked by significant milestones and strategic shifts. The company's journey reflects a commitment to modernization, geographic optimization, and a strong focus on customer-centricity. These efforts have positioned UNIQA to maintain a competitive edge in the market.

A key strategic move was the implementation of the 'UNIQA 3.0 - Seeding The Future' program, which concluded in December 2024, and its successor, 'UNIQA 3.0 - Growing Impact,' launched in 2025. These programs outline ambitious targets, including an average annual premium growth of 5% and a 6% average increase in net result. UNIQA's focus on technological advancements, strategic divestments, and sustainability initiatives underscores its adaptability and forward-thinking approach.

UNIQA's competitive advantages are rooted in its strong brand presence and diversified product portfolio. The company's commitment to ESG factors and a robust financial position further solidify its standing in the insurance industry. To learn more about the marketing strategies of the company, you can read the Marketing Strategy of Uniqa.

The successful rollout of SAP S/4HANA Finance across 18 countries, standardizing finance and controlling, reducing closing times, and enhancing data-driven decision-making. The expansion of the msg.Insurance Suite, which has handled all new private life business since 2021 and expanded to non-life insurance in 2023, with further migrations planned through mid-2024.

The launch of 'UNIQA 3.0 - Growing Impact,' which outlines ambitious targets, including an average annual premium growth of 5% and a 6% average increase in net result. The sale of its 75% holding in 'Insurance Company Raiffeisen Life' (Russia) and the decision to sell its shares in SIGAL UNIQA Group AUSTRIA sh.a. (Albania) to optimize its geographic footprint.

Strong brand presence in Austria and Central and Eastern Europe. A diversified product portfolio and robust distribution channels. Client-centric approach and bancassurance cooperation with Raiffeisen Bank International in Austria and CEE, and with mBank in Poland.

Maintained a strong net combined ratio of 93.1% in 2024. A solvency ratio of 264% in 2024 and 274% in Q1 2025. The company is committed to increasing dividends annually, with a payout ratio between 50% and 60%.

Key Areas of Focus

UNIQA's strategic priorities include operational efficiency, geographic optimization, and sustainability. The company is investing in modernizing its IT landscape and processes while also streamlining its business through strategic divestments.

- Modernization of IT infrastructure, including the expansion of the msg.Insurance Suite.

- Strategic divestments to optimize geographic footprint and reduce market dependencies.

- Integration of ESG factors into investment and product policies, targeting net-zero emissions.

- Focus on customer service and expanding Uniqa services.

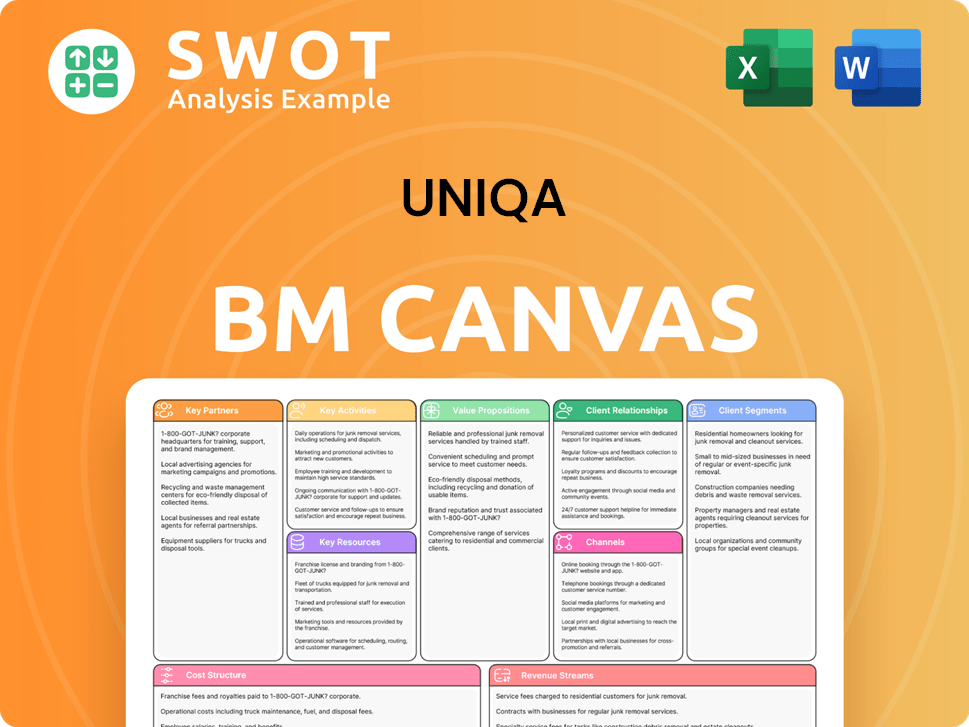

Uniqa Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Uniqa Positioning Itself for Continued Success?

The Uniqa company maintains a strong position in the European insurance market, particularly in Austria and Central and Eastern Europe (CEE). It holds the second-largest market share in Austria, approximately 21%, and serves over 17 million customers across 14 CEE countries. This geographic diversification, with 39% of its Gross Written Premiums (GWP) coming from international operations, helps buffer against regional economic fluctuations.

Despite its strengths, Uniqa insurance faces risks such as capital market volatility, regulatory changes, and natural catastrophes. A significant drop in net investment income in Q1 2025, specifically a 54.2% year-on-year fall, highlights the impact of market volatility. Regulatory compliance, including the EU's Digital Operational Resilience Act (DORA) and Corporate Sustainability Reporting Directive (CSRD), also poses ongoing challenges. While diversification helps, high growth in some CEE markets and the recurring threat of natural disasters, like 'Storm Boris' in 2024, continue to be relevant concerns.

Second-largest insurance group in Austria with around 21% market share. Operates in 14 CEE countries. Serves over 17 million customers, demonstrating a broad reach and customer loyalty.

Capital market volatility and regulatory changes pose challenges. Natural catastrophes and competitive pressures in high-growth markets are constant threats. A 54.2% year-on-year drop in net investment income in Q1 2025 reflects market volatility.

Focus on the 'UNIQA 3.0 - Growing Impact' strategic program. Forecasts an average revenue growth of 5.0% per annum over the next three years. Emphasis on digital transformation and sustainability initiatives.

Net-zero emissions in Austrian operations by 2040 and group-wide by 2050. Building green investments to over €2 billion by 2025. Expansion of the msg.Insurance Suite to enhance efficiency.

Looking ahead, Uniqa services is guided by its 'UNIQA 3.0 - Growing Impact' strategy for 2025-2028, which focuses on improving core underwriting and profitability in Austria and driving profitable growth in CEE markets. The company anticipates an average annual revenue growth of 5.0% over the next three years, with earnings per share expected to grow by 4.7% annually. Sustainability is central to its strategy, targeting net-zero emissions in Austria by 2040 and group-wide by 2050, with over €2 billion in green investments planned by 2025. Digital transformation, including the expansion of its msg.Insurance Suite, is also a key focus. The company's strong solvency ratio of 274% in Q1 2025 is expected to support its financial performance and market expansion.

Key Strategic Areas

The company is committed to several key strategic areas to ensure future success. These include enhancing core underwriting, profitable growth in CEE, and digital transformation.

- Improving core underwriting business and profitability in Austria.

- Achieving profitable growth in CEE markets.

- Focusing on digital transformation to improve efficiency.

- Integrating sustainability into the core business.

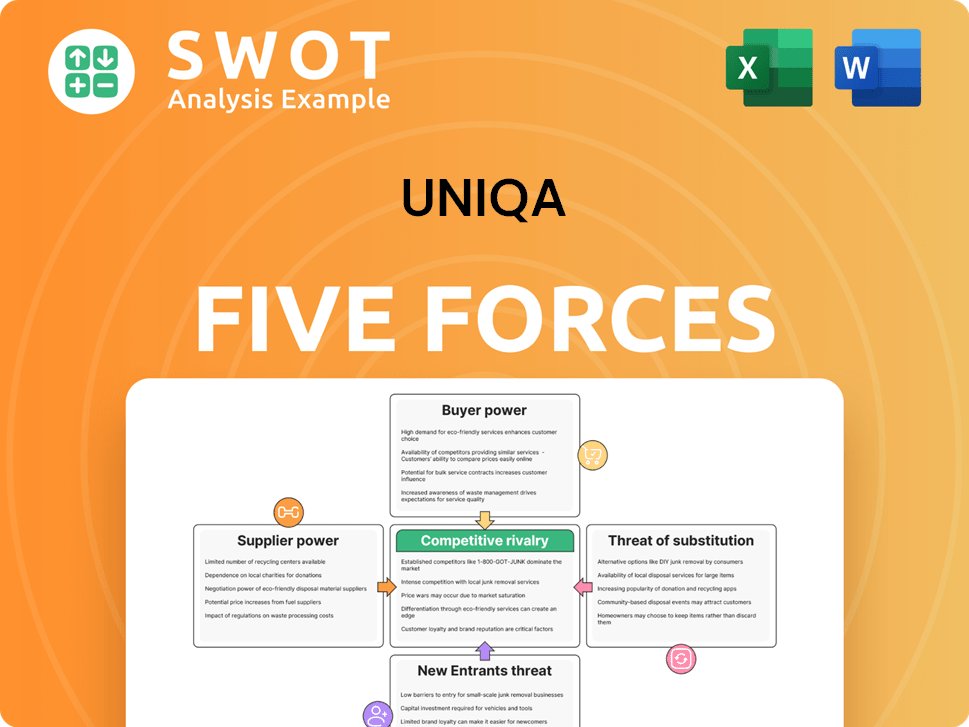

Uniqa Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Uniqa Company?

- What is Competitive Landscape of Uniqa Company?

- What is Growth Strategy and Future Prospects of Uniqa Company?

- What is Sales and Marketing Strategy of Uniqa Company?

- What is Brief History of Uniqa Company?

- Who Owns Uniqa Company?

- What is Customer Demographics and Target Market of Uniqa Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.