Jana Bank Bundle

Unveiling Jana Bank: How Does It Thrive in India's Financial Landscape?

Jana Small Finance Bank (Jana SFB) has rapidly become a key player in India's financial inclusion story. Originally Janalakshmi Financial Services, this Jana Bank SWOT Analysis reveals the bank's strategic moves since becoming a small finance bank in 2018. Its expansion from microfinance to comprehensive banking services has made it a vital resource for underserved communities.

With 778 branches across India as of late 2024, Jana Bank operations are designed to serve a wide customer base. Its recent financial performance, highlighted by a ₹501 crore profit after tax for the fiscal year ending March 31, 2025, showcases its growth. Understanding Jana Bank's strategies, including its focus on secured loans and deposit growth, is crucial for anyone interested in the evolution of this important financial institution.

What Are the Key Operations Driving Jana Bank’s Success?

Jana Small Finance Bank (Jana SFB) focuses on providing financial products and services to individuals and small businesses, particularly those underserved by traditional banking. It offers a range of banking services, including deposit accounts like savings and fixed deposits, and various loan products. This approach allows Jana SFB to cater to a diverse customer base, including those in rural and unbanked areas.

The bank's core operations involve a mix of physical and digital channels. As of March 2024, Jana SFB had over 770 banking outlets spread across 22 states and 2 union territories. This extensive physical presence is complemented by robust digital banking solutions, including free UPI, NEFT, RTGS, and IMPS transactions, which help reduce operational costs. This blend of physical and digital infrastructure enhances accessibility and convenience for its customers.

A key aspect of Jana SFB's value proposition is its customer-centric approach and focus on building long-term relationships. The bank aims to provide personalized services, including dedicated relationship managers for current account holders. Its supply chain and distribution networks are designed to reach marginalized sections of society, with a significant portion of its outlets in unbanked rural centers, demonstrating its commitment to financial inclusion. For more insights, you can explore the Growth Strategy of Jana Bank.

Jana SFB offers a wide array of banking services. These include deposit accounts, such as savings accounts and fixed deposits, designed to meet various customer needs. The bank also provides a range of loan products, including secured business loans, microloans against property (M-LAP), MSME loans, affordable housing loans, two-wheeler loans, and gold loans.

Jana SFB has a strong focus on digital banking solutions to enhance customer convenience and reduce operational costs. Its digital offerings include free UPI, NEFT, RTGS, and IMPS transactions. These digital services are designed to provide customers with seamless online account management and transaction capabilities, making banking more accessible and efficient.

The bank's loan portfolio includes a variety of options to cater to different financial needs. These include secured business loans, microloans against property (M-LAP), MSME loans, affordable housing loans, two-wheeler loans, and gold loans. Jana SFB also offers unsecured options like agricultural loans and group loans, providing comprehensive financial solutions.

Jana SFB prioritizes building long-lasting customer relationships by providing personalized services. This includes dedicated relationship managers for current account holders. The bank aims to create a customer-centric environment. This approach helps foster loyalty and trust, making Jana SFB a preferred choice for its customers.

Strategic Shift in Lending

Jana SFB is strategically shifting towards a more secured loan portfolio to strengthen its asset quality and risk management. The share of secured assets is targeted to increase to 70% of its AUM by March 31, 2025, from 60% in March 2024. This focus on collateralized lending demonstrates the bank's commitment to financial stability and prudent lending practices.

- The bank aims to increase its focus on secured lending.

- This strategic shift enhances asset quality and risk management.

- The bank is committed to financial inclusion.

- Jana SFB provides accessible and affordable financial solutions.

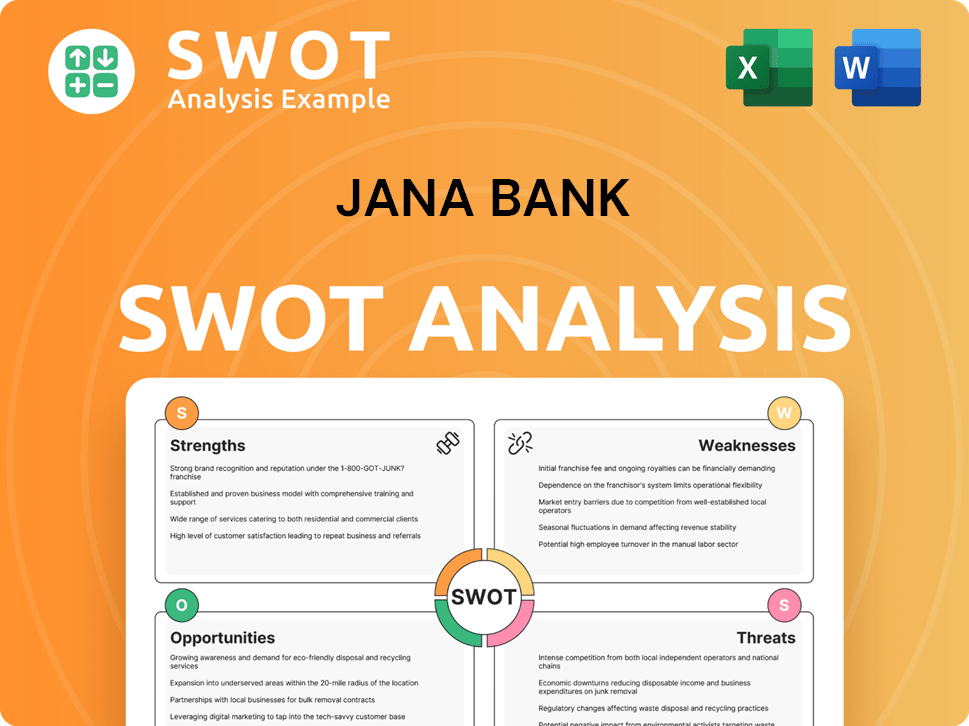

Jana Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Jana Bank Make Money?

Jana Small Finance Bank, or Jana Bank, strategically generates revenue through a diverse range of financial products and services. The bank's primary focus is on interest income derived from its lending activities, which include various loan products tailored to different customer segments.

In addition to loans, Jana Bank also earns revenue from deposit accounts, such as savings accounts and fixed deposits, providing a stable funding base. Furthermore, the bank expands its income streams through fee-based services and strategic partnerships, enhancing its overall financial performance.

For the fiscal year ending March 31, 2025, Jana Bank's financial performance showed significant growth. The bank's total income rose by 11.02% to ₹1,433.16 crore in Q4 FY25 compared to the same period the previous year.

Revenue Streams in Detail

The main revenue streams for Jana Bank include interest from loans and income from deposits. Jana Bank's interest income for the January to March quarter of FY25 rose by nearly 8% to ₹1,999.27 crore. The bank's net interest income grew to ₹2,127 crore, a 28.1% year-on-year increase from ₹1,660 crore in FY24.

- Loans: Secured business loans, microloans against property (M-LAP), MSME loans, affordable housing loans, two-wheeler loans, gold loans, and agricultural and group loans.

- Deposits: Savings accounts and fixed deposits.

- Fee-Based Income: Corporate agent for third-party insurance products, Point of Sale (POS) terminals, and payment gateway services. The bank aims to further diversify its fee and non-interest-based revenues by cross-selling products such as mutual funds.

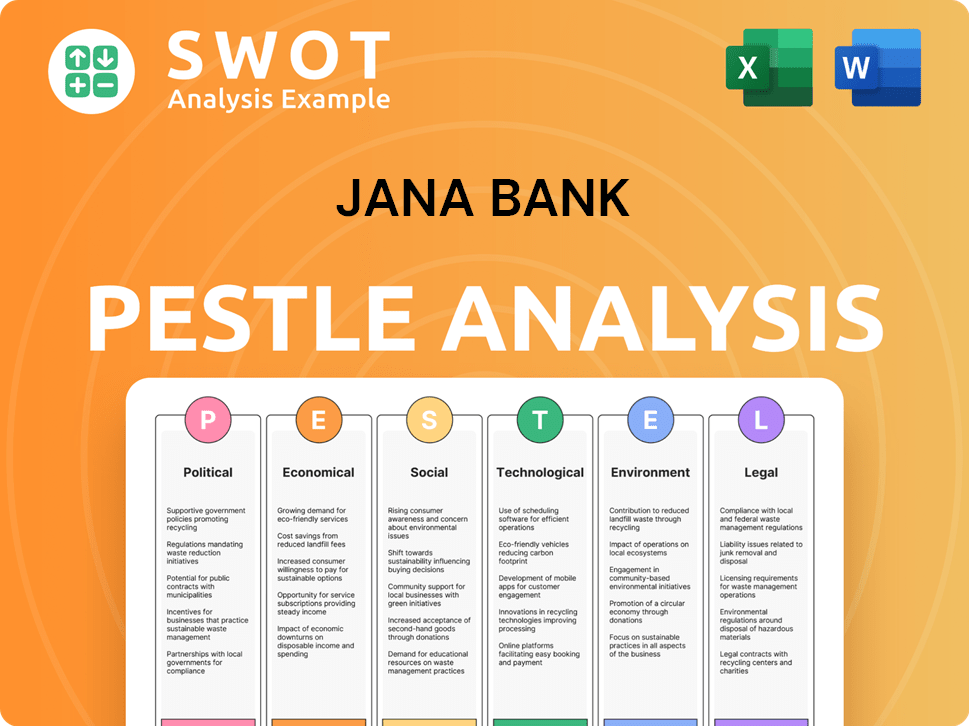

Jana Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Jana Bank’s Business Model?

The journey of Jana Small Finance Bank (Jana SFB) is marked by significant milestones and strategic shifts. Initially, it operated as Janalakshmi Financial Services Private Limited, later obtaining an NBFC registration and transitioning to an NBFC-MFI. A crucial turning point was the acquisition of the Small Finance Bank license in 2015, followed by the commencement of banking operations in March 2018, establishing it as a Scheduled Commercial Bank.

Key product launches have included two-wheeler loans, digital account opening and KYC processes, gold loans, and affordable housing loans. The bank's Asset Under Management (AUM) has shown substantial growth, exceeding both ₹150,000 Million and ₹200,000 Million. Jana SFB has also expanded its branch network, surpassing 750 open branches. A notable strategic move was its Initial Public Offering (IPO) in February 2024, which raised ₹462 crore, strengthening its capital adequacy.

Jana SFB's operational landscape has included challenges, particularly industry-wide stress within the Microfinance Institution (MFI) segment, which led to increased delinquencies in its microfinance portfolio. In response, Jana SFB has strategically pivoted towards a more secured loan portfolio, aiming for secured loans to constitute 70% of its AUM by March 31, 2025, a rise from 60% in March 2024, thereby enhancing risk management and asset quality.

Jana SFB started as Janalakshmi Financial Services Private Limited. It received its Small Finance Bank license in 2015. Banking operations began in March 2018.

The bank launched two-wheeler loans and digital account opening. It expanded its branch network and had an IPO in February 2024. Jana SFB is shifting towards a more secured loan portfolio.

AUM has surpassed ₹150,000 Million and ₹200,000 Million. The IPO in February 2024 raised ₹462 crore. Secured loans are targeted to be 70% of AUM by March 31, 2025.

Jana SFB has an established track record in lending. It focuses on customer-centric approach. The bank offers digital banking and has a wide branch network. The bank has strong capitalization levels.

Competitive Advantages of Jana SFB

Jana SFB's competitive edge comes from its long-standing experience and customer-focused approach. The bank leverages technology for a seamless banking experience and has a broad physical presence. Furthermore, the bank maintains robust financial health, including a Capital Adequacy Ratio (CAR) of 20.7% and a Tier-1 CRAR of 19.8% as of March 31, 2025, and a strong Liquidity Coverage Ratio (LCR) of 253%.

- Customer-Centric Approach: Offers personalized services and dedicated relationship managers.

- Technology Integration: Provides free digital transactions and mobile banking solutions.

- Extensive Branch Network: Over 770 banking outlets, including in unbanked rural areas.

- Capital Adequacy: Strong CAR and Tier-1 CRAR as of March 31, 2025.

- Liquidity: High LCR of 253% as of March 31, 2025.

- Strategic Shift: Diversifying advances by accelerating secured loan growth.

For a deeper understanding of the bank's growth trajectory and strategic initiatives, consider reading about the Growth Strategy of Jana Bank.

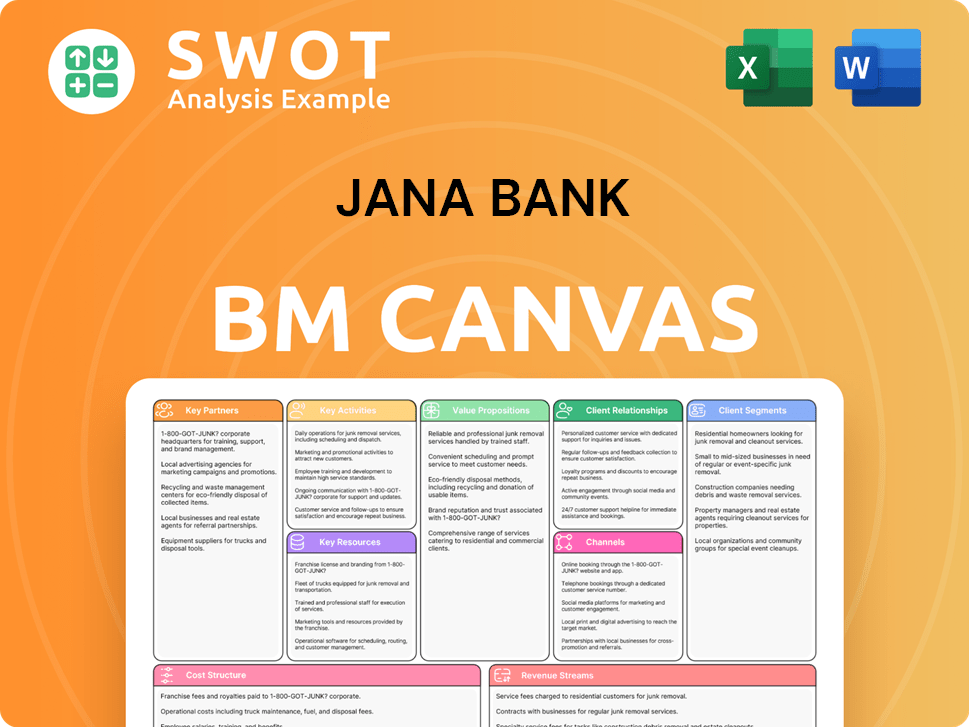

Jana Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Jana Bank Positioning Itself for Continued Success?

As of September 30, 2023, Jana Small Finance Bank held a significant position in the Indian small finance bank sector, ranking fourth largest in terms of Asset Under Management (AUM) and deposit size. The bank strategically focuses on financial inclusion, particularly serving the urban underserved segment. It fosters customer loyalty through tailored products and a customer-centric approach, solidifying its market position.

As of December 31, 2024, the bank's deposits were ₹25,865 crore and advances were ₹27,984 crore, with a network of 778 branches. This financial institution's operations are geared towards expanding its reach and impact within the banking services landscape.

The bank faces risks due to its high retail exposure, making it vulnerable to economic downturns. Regulatory changes from the RBI could also impact its growth. While diversifying, Jana Bank's CASA ratio was at 18.43% as of December 31, 2024, and a high Credit-Deposit (CD) ratio of 102.5% at the same time, indicating reliance on higher-cost deposits.

Jana Bank aims to improve its deposit profile by increasing granular and retail deposits. The bank plans to increase its secured loan book to around 80% in the coming years. On June 9, 2025, Jana Small Finance Bank submitted an application to the Reserve Bank of India (RBI) for a voluntary transition from a small finance bank to a universal bank.

Jana Bank is focusing on enhancing its deposit profile and increasing secured loans. The bank aims to enhance its financial performance through these strategic moves. This approach aligns with the bank's goal to become an 'Anchor Bank to a Rising and Atmanirbhar India.' Learn more about the Marketing Strategy of Jana Bank.

Asset quality, with a Gross Non-Performing Assets (GNPA) of 2.5% and Net Non-Performing Assets (NNPA) of 0.9% as of March 31, 2025, is a key area to monitor. The bank's capital adequacy (CAR) was at 20.7% as of March 31, 2025, suggesting a strong financial position.

Transition to Universal Bank

The application to become a universal bank is a strategic move for Jana Bank, enabling it to offer a broader range of services. To qualify, the bank needs to meet criteria such as a net worth of at least ₹1,000 crore, being listed, and maintaining a gross NPA ratio of less than 3% for two consecutive fiscal years.

- Expanding service offerings.

- Enhancing financial inclusion efforts.

- Meeting regulatory requirements.

- Improving asset quality.

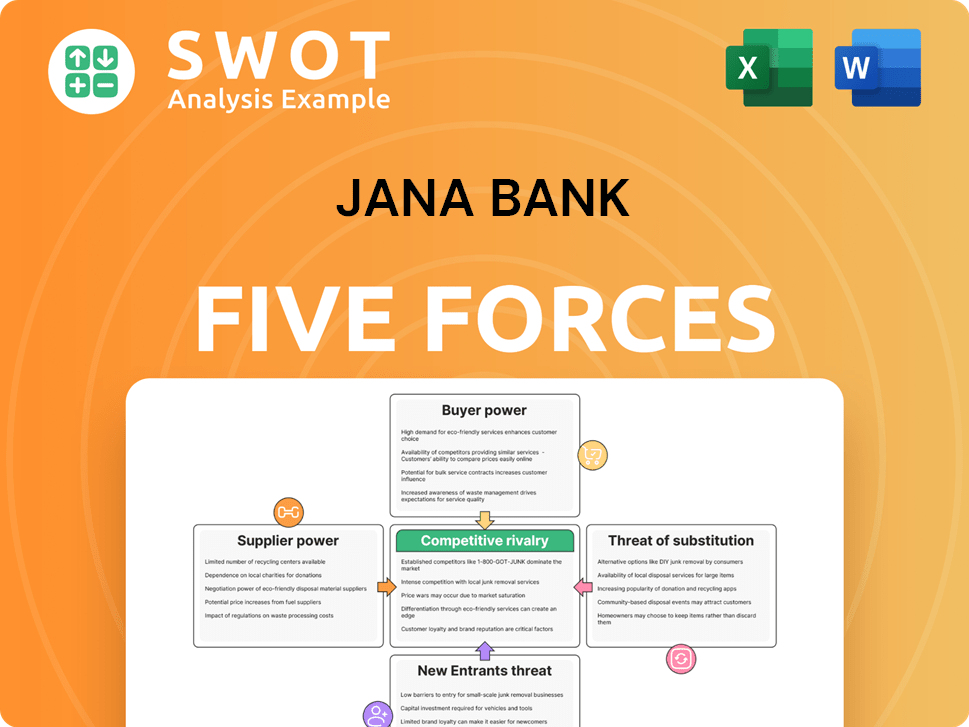

Jana Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Jana Bank Company?

- What is Competitive Landscape of Jana Bank Company?

- What is Growth Strategy and Future Prospects of Jana Bank Company?

- What is Sales and Marketing Strategy of Jana Bank Company?

- What is Brief History of Jana Bank Company?

- Who Owns Jana Bank Company?

- What is Customer Demographics and Target Market of Jana Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.