Jana Bank Bundle

How Does Jana Bank Navigate the Competitive Financial Waters?

Jana Small Finance Bank, a prominent player in India's financial sector, has rapidly evolved since its 2018 launch. From its microfinance roots, the bank has expanded its reach, aiming to serve the urban underserved population. Its impressive growth, marked by significant financial gains, has positioned it as a key contender in a dynamic market.

Understanding the Jana Bank SWOT Analysis is crucial for investors and strategists alike. This analysis will explore the Jana Bank competitive landscape, providing a detailed Jana Bank market analysis to assess its position against its Jana Bank competitors. We'll examine Jana Bank financial performance and Jana Bank industry analysis to understand its Jana Bank business strategy and its impact on its Jana Bank market share analysis India.

Where Does Jana Bank’ Stand in the Current Market?

Jana Small Finance Bank has carved a significant niche in the Indian financial sector, particularly by focusing on the urban underserved market. It is recognized as the fourth-largest Small Finance Bank based on Assets Under Management (AUM). The bank offers a range of financial products and services, including savings accounts, loans, and fixed deposits, tailored to meet the needs of its target demographic. This strategic positioning allows it to capitalize on the growing demand for accessible financial solutions.

The bank's business model is built on providing financial services to a diverse customer base, with a strong emphasis on secured lending. This approach helps manage risk and supports sustainable growth. Jana Small Finance Bank's extensive distribution network, comprising numerous banking outlets across multiple states and union territories, ensures broad market reach and accessibility for its customers. The bank's focus on both lending and deposit-taking activities is crucial for its financial stability and expansion.

As of March 31, 2025, Jana Small Finance Bank's AUM stood at ₹29,545 crore, reflecting a 19% year-on-year growth. Secured assets constitute a significant portion of the AUM, at 70%, indicating a strategic shift toward secured lending. The bank's total deposits reached ₹29,120 crore, demonstrating a 29% year-on-year growth. This growth highlights the bank's strong market presence and customer trust.

Jana Small Finance Bank reported a net profit of ₹123.47 crore for Q4 FY25, despite a 62% year-on-year decrease. The interest income for the same period rose by nearly 8% to ₹1,999.27 crore. The bank's capital adequacy ratio (CAR) improved to 20.7% in Q4 FY25, with a Tier-1 CRAR of 19.8% as of March 31, 2025. These figures reflect the bank's financial health and its ability to manage its capital effectively.

Loan AUM grew to ₹24,746 crore in FY24, a 24.9% increase year-on-year. The bank serves customers through a network of 771 banking outlets across 22 states and two union territories. The bank's diverse loan products include secured business loans, microloans against property, MSME loans, and affordable housing loans. The bank's extensive distribution network is crucial for reaching its target market.

The Gross Non-Performing Assets (GNPA) ratio increased to 2.71% in Q4 FY25, while Net NPA rose to 0.94%. As of December 31, 2024, the bank's liquidity coverage ratio was healthy at 279% against the regulatory requirement of 100.0%. The bank's asset quality and liquidity positions are key indicators of its financial stability and ability to manage risks effectively.

Competitive Advantages and Strategy

Jana Small Finance Bank's competitive advantage lies in its focus on the urban underserved segment and its diversified product portfolio. The bank’s strategy includes increasing the share of secured assets and expanding its distribution network. For a deeper understanding of the bank's target market, consider reading about the Target Market of Jana Bank.

- Focus on urban underserved segment.

- Diversified product portfolio.

- Strategic shift towards secured lending.

- Extensive distribution network.

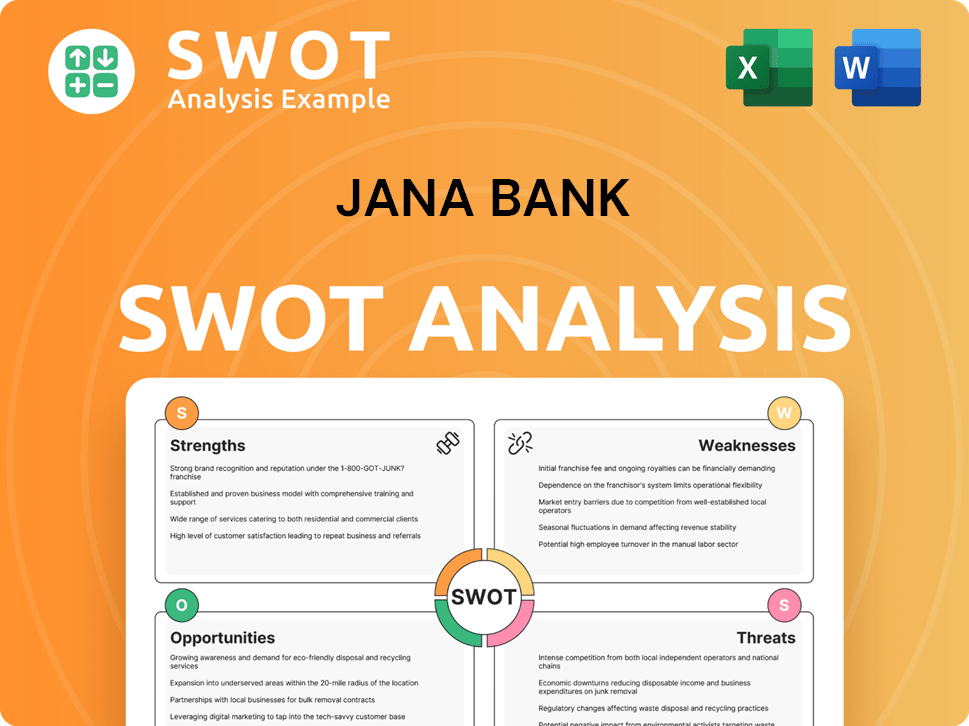

Jana Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

Who Are the Main Competitors Challenging Jana Bank?

The competitive landscape for Jana Small Finance Bank is complex, encompassing a variety of financial institutions vying for market share in India. Understanding the dynamics of this landscape is crucial for assessing the bank's Growth Strategy of Jana Bank and overall financial performance. This analysis considers the key players and their strategies, providing insights into the challenges and opportunities Jana Small Finance Bank faces.

Jana Small Finance Bank operates within a market characterized by intense competition. The bank competes with other small finance banks, non-banking financial companies (NBFCs), traditional banks, payment banks, and fintech companies. Each type of competitor brings its own strengths and strategies, creating a multifaceted competitive environment.

The bank's ability to navigate this landscape is critical for its success. The strategies of its competitors, market trends, and regulatory changes all influence Jana Small Finance Bank's performance and future prospects. This competitive analysis provides a comprehensive overview of the key players and their impact on Jana Small Finance Bank.

Other Small Finance Banks

Direct competitors include other small finance banks (SFBs) that target similar customer segments. These SFBs offer comparable products and services, competing for the same customer base. The competition often revolves around interest rates, service quality, and branch network.

Non-Banking Financial Companies (NBFCs)

NBFCs specializing in microfinance, small business loans, and affordable housing loans also compete with Jana Small Finance Bank. They often have a strong presence in the urban underserved markets. NBFCs may offer specialized financial products tailored to specific customer needs.

Traditional Banks

Major traditional banks like State Bank of India, HDFC Bank, and ICICI Bank compete with Jana Small Finance Bank by offering a wide range of banking products. These banks have established customer bases and extensive networks. Traditional banks often have a broader product portfolio.

Payment Banks

Payment banks, such as Paytm Payments Bank and India Post Payments Bank, compete by focusing on basic banking services like deposits and remittances. They target customers who may not have access to traditional banking services. Payment banks often leverage technology to offer convenient services.

Fintech Companies

Fintech companies are disrupting the financial services industry with innovative digital solutions. They challenge traditional banking models through technology-driven services. Fintech companies often compete on the basis of technological innovation and lower operational costs.

Competitive Dynamics and Strategies

The competitive landscape is dynamic, with various factors influencing the strategies of each player. SFBs may focus on higher interest rates or expanding their branch networks. Traditional banks leverage their extensive customer base and diversified offerings. Fintech companies emphasize technological innovation and digital experiences.

- Interest Rates: SFBs often compete on interest rates for loans and deposits.

- Branch Network: The size and reach of the branch network impact customer accessibility.

- Digital Services: Fintech companies and traditional banks are investing in digital banking.

- Customer Base: Traditional banks have a large customer base.

- Product Diversification: Traditional banks offer a wide range of financial products.

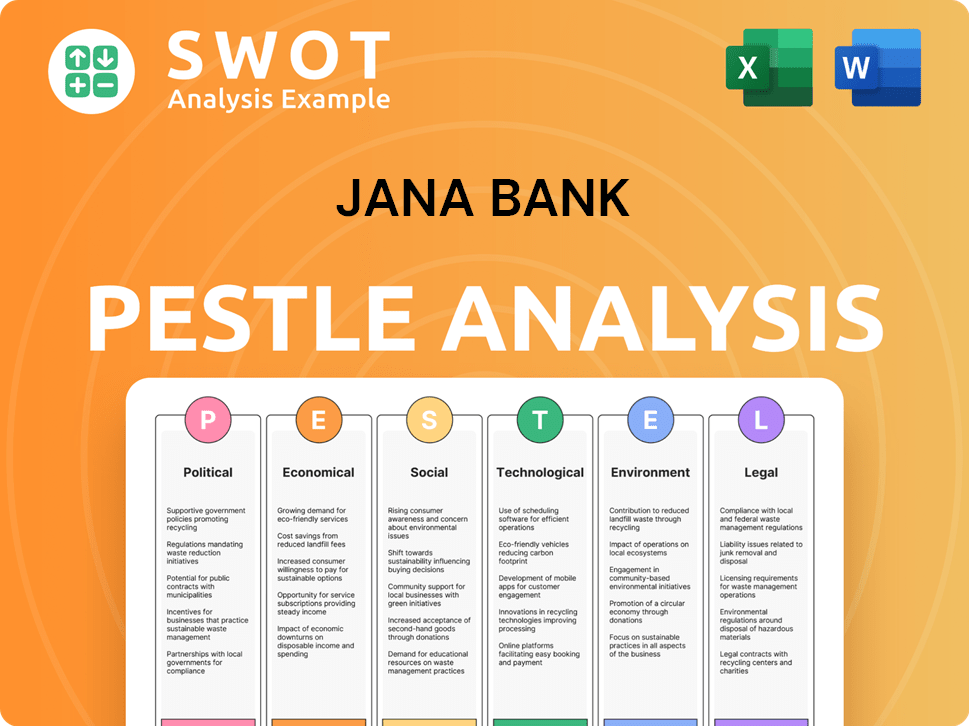

Jana Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Gives Jana Bank a Competitive Edge Over Its Rivals?

The competitive landscape for Jana Small Finance Bank is shaped by its strategic focus on financial inclusion and its evolution from a microfinance institution. Key milestones include its transformation into a small finance bank, allowing it to offer a wider range of financial products and services. This strategic shift has positioned it to tap into the underserved urban market, differentiating it from competitors and driving its growth strategy.

Jana Small Finance Bank's competitive edge is rooted in its customer-centric approach and technological advancements. The bank has invested heavily in digital banking solutions to provide a seamless experience for its customers. This focus on technology, combined with a robust distribution network and a diversified product portfolio, has enabled it to build a strong customer base and maintain a competitive position in the market. For a deeper understanding of the bank's ownership structure, you can refer to Owners & Shareholders of Jana Bank.

The bank's ability to adapt to changing market dynamics and its commitment to serving the urban underserved population are crucial factors in its continued success. By focusing on these areas, Jana Small Finance Bank aims to strengthen its position in the Jana Bank competitive landscape.

Jana Small Finance Bank prioritizes serving the urban underserved population, offering tailored products and services. This customer-centric approach builds strong relationships and fosters loyalty. Their offerings include lower minimum balance requirements and competitive interest rates, directly benefiting small businesses and individuals, which is a key aspect of the Jana Bank market analysis.

The bank offers a wide array of financial products, including savings accounts and various loan types, such as secured business loans and affordable housing loans. This diversification reduces reliance on a single offering and caters to diverse customer needs. A strategic shift towards secured lending enhances risk management, with secured assets comprising 68% of AUM as of December 2024.

Jana Small Finance Bank has invested heavily in digital banking solutions, providing a seamless digital experience. This includes adopting an integrated risk management approach and leveraging technology for efficient operations. Digitization enhances customer service through chatbots, email marketing automation, and mobile banking apps, which is a critical element in the Jana Bank digital banking services.

The bank has built a robust distribution network with a presence in key urban centers and a widespread branch network. This extensive network makes banking services easily accessible to a wide customer base. As of February 28, 2025, the bank employed 26,320 people, demonstrating its commitment to physical presence and customer service, which is crucial for the Jana Bank branch network locations.

Strong Risk Management

Jana Small Finance Bank has robust risk management practices to ensure the safety of customer funds. The shift towards secured assets is a strategic move to bolster the risk profile. This focus on risk management is essential for sustainable growth and maintaining customer trust.

- Focus on secured lending to enhance asset quality.

- Implementation of advanced risk assessment models.

- Regular monitoring and review of lending practices.

- Compliance with regulatory guidelines and standards.

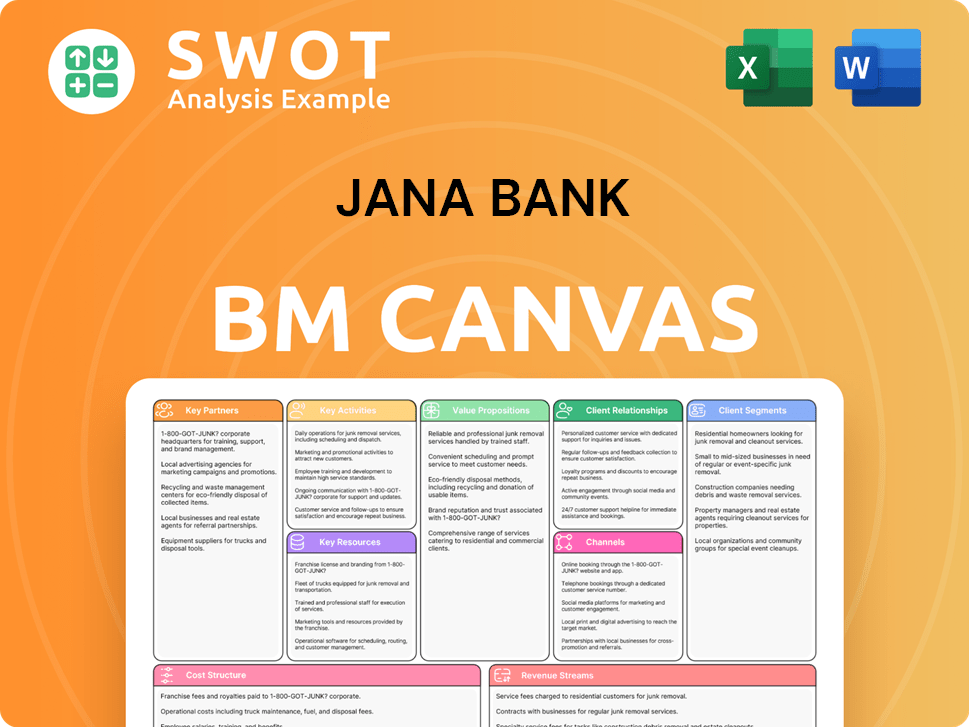

Jana Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Industry Trends Are Reshaping Jana Bank’s Competitive Landscape?

The Indian banking sector, particularly for Small Finance Banks (SFBs), is experiencing significant shifts that impact the Jana Bank competitive landscape. These changes create both opportunities and challenges for institutions like Jana Small Finance Bank. Understanding these dynamics is crucial for assessing its future prospects and formulating effective Jana Bank business strategy.

Jana Bank industry analysis reveals a sector undergoing rapid technological advancements, evolving consumer preferences, and stringent regulatory changes. The bank's ability to adapt to these trends, manage risks, and capitalize on emerging opportunities will determine its success. This analysis also considers the Jana Bank financial performance in the context of its competitors and market position.

The banking sector is rapidly digitizing, with a strong preference for online and mobile banking. This shift is powered by innovations like AI and data science, enabling personalized marketing and improved customer service. Jana Bank leverages technology for efficient operations and digital transformation. The bank's focus on digital banking services is crucial for remaining competitive.

The government's financial inclusion initiatives provide a strong impetus for SFBs. However, this also brings increased regulatory scrutiny, especially regarding digital lending. Jana Bank, meeting GNPA < 3% and NNPA < 1% as of March 31, 2025, is eligible for a Universal Banking License, potentially altering its operational scope. This could significantly impact the Jana Bank competitive landscape.

Consumers increasingly demand accessible, affordable, and tailored financial products. This customer-centric approach is key for Jana Bank, but it also requires continuous product innovation. Understanding Jana Bank customer base demographics is critical for product development and marketing strategies.

There's a trend towards increasing secured loan portfolios to enhance risk management and asset quality. Jana Bank actively participates in this, with secured assets comprising 70% of its AUM as of March 31, 2025, aiming for 80% in the coming years. This strategic shift impacts the bank's risk profile.

Future Challenges

Jana Bank faces several challenges. Asset quality risks, particularly in affordable housing and loans against property, are a concern, with GNPAs increasing in December 2024. Intense competition from various financial institutions, including traditional banks and fintech companies, is another significant hurdle. Managing and improving the deposit profile, especially the CASA ratio, which declined to 18% as of December 2024 from 20% in March 2024, is a continuous challenge. Changes in RBI directives can also impact operations.

- Asset Quality Risks: Maintaining asset quality is crucial for future growth.

- Intense Competition: The competitive landscape is fierce, with new and existing players vying for market share.

- Maintaining Deposit Profile: Improving CASA ratio is a continuous challenge.

- Regulatory Compliance: Compliance failures can lead to penalties and reputational damage.

Opportunities

Jana Bank has several opportunities for growth. Expansion in emerging markets and underserved segments offers substantial potential. Product innovations, such as digital-first offerings, can attract new customers. Strategic partnerships with microfinance institutions and fintech companies can expand reach. The potential for a universal banking license could allow Jana Bank to operate on a larger scale. Increasing the share of secured assets will also strengthen the bank's risk profile. Exploring Jana Bank investment opportunities is crucial for stakeholders.

- Expansion in Emerging Markets: Focus on underserved and underbanked areas.

- Product Innovations: Develop tailored financial products.

- Strategic Partnerships: Collaborate with other institutions.

- Universal Banking License: Expand services and operations.

- Increased Secured Lending: Strengthen the bank's risk profile.

The future outlook for Jana Bank points towards a stronger, more diversified financial institution, with an increased focus on secured assets and a robust digital presence. The bank's strategies focus on customer-centricity, technological innovation, and strategic partnerships. Successfully navigating regulatory changes and continuously improving asset quality and deposit granularity will be key to sustained growth and profitability. For a deeper dive into the competitive dynamics, consider analyzing the Jana Bank vs other small finance banks and reviewing the latest Jana Bank latest news and updates.

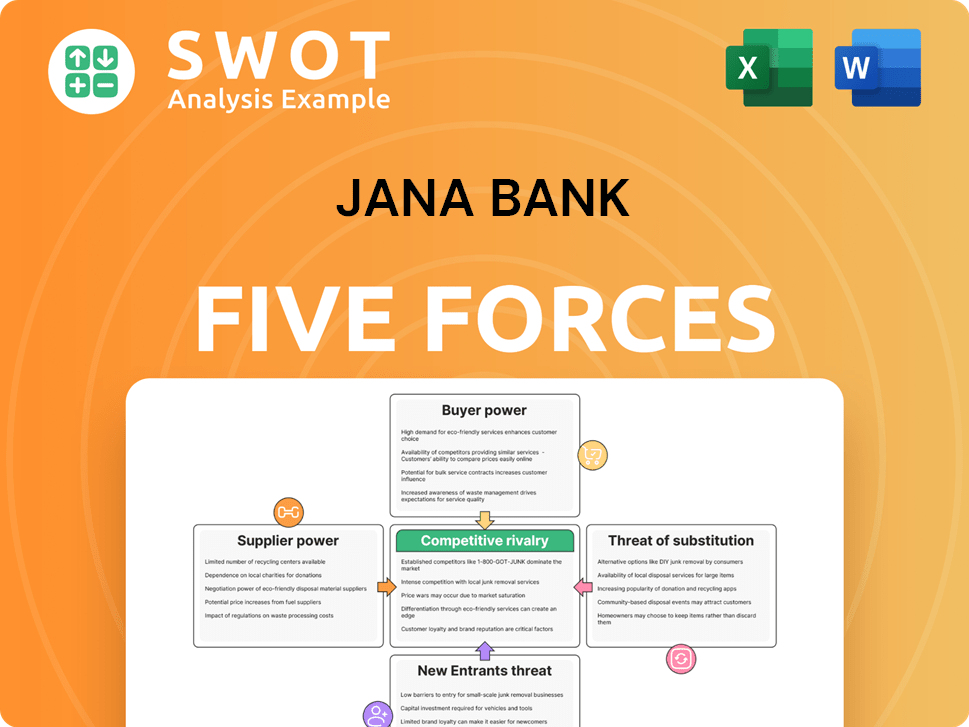

Jana Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Jana Bank Company?

- What is Growth Strategy and Future Prospects of Jana Bank Company?

- How Does Jana Bank Company Work?

- What is Sales and Marketing Strategy of Jana Bank Company?

- What is Brief History of Jana Bank Company?

- Who Owns Jana Bank Company?

- What is Customer Demographics and Target Market of Jana Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.