Freddie Mac Bundle

Unveiling Freddie Mac: How Does It Shape Your Financial World?

Ever wondered how millions of Americans secure home loans? Freddie Mac, a pivotal player in the U.S. housing finance system, plays a crucial role. Established in 1970, this Freddie Mac SWOT Analysis can provide further insights into its strategic position. Understanding Freddie Mac is essential for anyone involved in the housing market.

Freddie Mac's operations are complex, yet its impact is clear: providing liquidity and stability to the mortgage market. As a Government-sponsored enterprise, it purchases mortgages from lenders, transforming them into mortgage-backed securities, influencing Freddie Mac mortgage rates and overall housing affordability. Exploring the intricacies of Freddie Mac's role, from its impact on homeownership to its risk management, is key to grasping the broader financial landscape.

What Are the Key Operations Driving Freddie Mac’s Success?

The core of Freddie Mac's operations centers on its commitment to injecting liquidity, stability, and affordability into the U.S. housing market. This is primarily achieved through its role in the secondary mortgage market, where it buys conforming mortgages from lenders. These mortgages must meet specific criteria set by Freddie Mac and the Federal Housing Finance Agency (FHFA), including adhering to loan-to-value ratios and loan limits. For instance, in 2024, the conforming loan limit for a single-unit property in most areas of the U.S. is set at $766,550.

The company's primary activity involves acquiring these mortgages, pooling them, and then securitizing them into mortgage-backed securities (MBS). These MBS are subsequently sold to a diverse group of investors globally, including pension funds, insurance companies, and foreign central banks. This process allows lenders to replenish their funds, enabling them to offer more mortgages and thereby increasing the availability of housing finance. Freddie Mac provides a guarantee on the timely payment of principal and interest to MBS investors, mitigating investor risk and making these securities an attractive investment.

The operational uniqueness of Freddie Mac lies in its ability to standardize a wide array of individual mortgages into uniform, tradable securities, effectively linking mortgage originators with capital market investors. Its advanced risk management frameworks and technology platforms facilitate the efficient processing and securitization of large volumes of mortgage data. Partnerships with a broad network of lenders and a strong distribution network for its MBS ensure that its core capabilities translate into readily available mortgage credit for consumers and reliable investment opportunities for institutions, ultimately benefiting the entire housing ecosystem.

Freddie Mac buys conforming mortgages from lenders, providing them with cash to offer more loans. These mortgages are then pooled and transformed into mortgage-backed securities (MBS). This process allows for a continuous flow of funds in the housing market.

Freddie Mac guarantees the timely payment of principal and interest to MBS investors, even if borrowers default. This guarantee reduces investor risk, making MBS attractive. Sophisticated risk management frameworks are crucial for maintaining stability.

MBS are sold to a wide array of global investors, including pension funds and insurance companies. This attracts capital into the housing market, supporting mortgage availability. Freddie Mac's operations significantly influence mortgage interest rates and overall market stability.

Freddie Mac uses advanced technology and standardized processes to efficiently handle large volumes of mortgages. This operational efficiency allows them to streamline the securitization process and support the housing market. The company's technology platforms are key to its success.

Key Aspects of Freddie Mac's Operations

Freddie Mac's role in the housing market is multifaceted, involving mortgage purchases, securitization, and guaranteeing payments. Its operations directly impact the availability and cost of mortgage credit, influencing homeownership rates and overall economic stability. The company's influence extends to mortgage rates and the broader financial system.

- Liquidity Provision: Freddie Mac provides liquidity to mortgage lenders by purchasing their loans.

- Risk Mitigation: The guarantee on MBS reduces investor risk, making mortgage investments more attractive.

- Market Stability: Freddie Mac's activities help stabilize the housing market, especially during economic downturns.

- Affordability Initiatives: The company supports affordable housing initiatives, promoting homeownership.

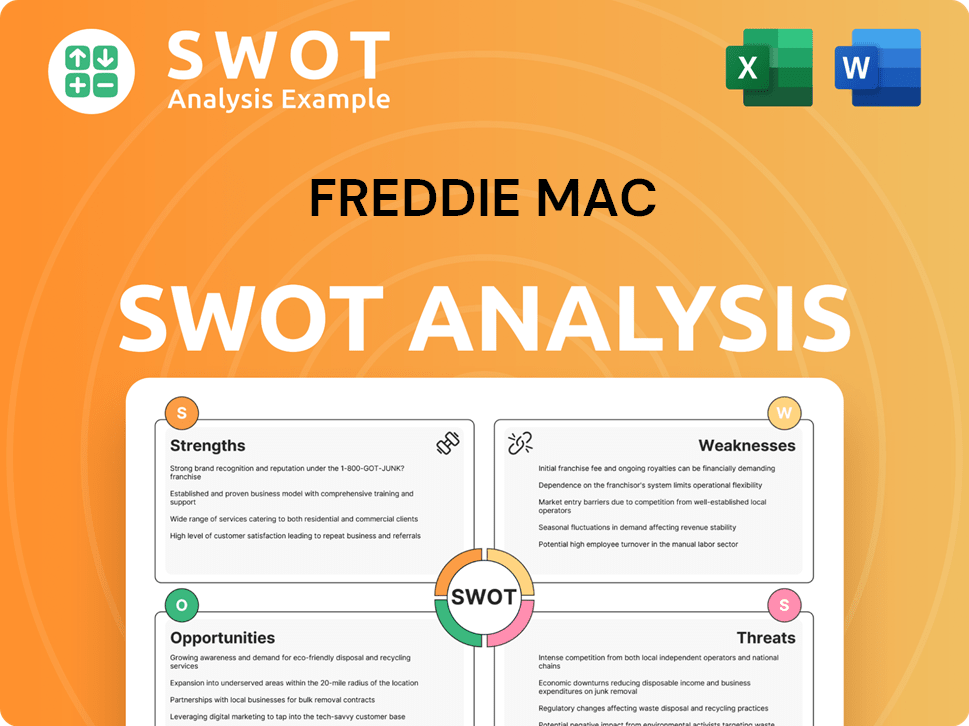

Freddie Mac SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Freddie Mac Make Money?

The primary revenue streams for Freddie Mac, a government-sponsored enterprise, are guarantee fees and net interest income. These revenue sources are central to its financial stability and operational capacity within the housing market. Understanding how Freddie Mac generates revenue is crucial for grasping its role in the U.S. mortgage system.

Guarantee fees are charged to lenders for the credit enhancement provided on mortgage-backed securities (MBS) issued by Freddie Mac. This fee compensates the company for assuming the credit risk associated with the underlying mortgages, ensuring investors receive timely payments. Net interest income stems from its retained portfolio of mortgages and MBS, representing the difference between interest earned and the cost of funding these assets.

In 2023, guarantee fee income was a significant contributor to Freddie Mac's financial performance. Furthermore, the company reported a net interest income of $9.7 billion for the full year 2023, highlighting the importance of its retained portfolio. These revenue streams are vital for supporting Freddie Mac's mission to provide liquidity and stability in the housing market.

Monetization Strategies

Freddie Mac's monetization strategy focuses on its public mission to reduce mortgage credit costs and make mortgage investments attractive. This is achieved by guaranteeing mortgage payments and fostering a liquid secondary market. The company's operations directly influence mortgage interest rates and homeownership opportunities.

- Guarantee Fees: Earned by providing credit enhancement on MBS.

- Net Interest Income: Generated from the retained mortgage portfolio.

- Secondary Market Liquidity: Facilitating the buying and selling of mortgages.

- Investment Income: Additional revenue from investments.

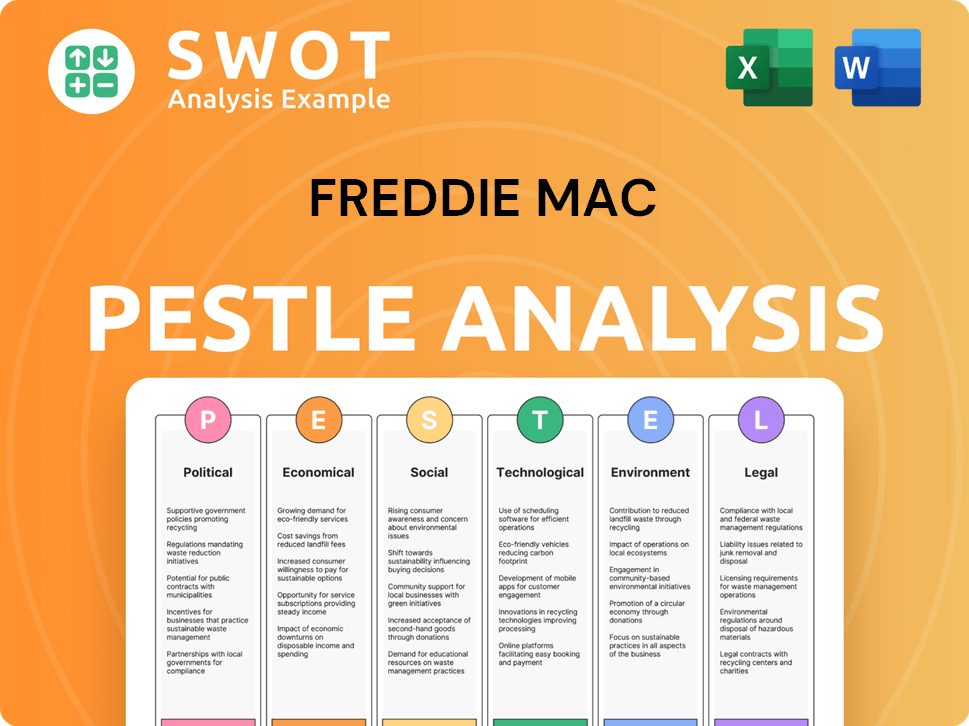

Freddie Mac PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Freddie Mac’s Business Model?

Freddie Mac's journey has been marked by significant milestones and strategic adaptations, particularly in response to market dynamics and regulatory shifts. Established in 1970, the company was created to provide competition and expand the secondary market for conventional mortgages. Its operations have been crucial in shaping the housing market.

The 2008 financial crisis presented an unprecedented challenge, leading to Freddie Mac being placed into conservatorship under the Federal Housing Finance Agency (FHFA). This strategic move was critical to stabilize the housing market. Since then, Freddie Mac has operated under the direction of the FHFA, with a focus on risk management and supporting housing affordability. Understanding Freddie Mac operations is key to grasping its impact on the housing sector.

Operational challenges have included navigating fluctuating interest rates and adapting to technological advancements. In response, Freddie Mac has continuously refined its credit underwriting standards and invested in technology to enhance its securitization platform and data analytics capabilities. The company's role in the housing market is significant.

Freddie Mac's competitive edge stems from its government-sponsored enterprise (GSE) status, which provides an implicit federal backing. This allows it to access capital markets at lower rates than private entities. This advantage is crucial in the mortgage market.

Freddie Mac continuously refines its credit underwriting standards and invests in technology. These strategic moves are essential for adapting to market changes. The company's focus remains on risk management and supporting housing affordability.

The establishment of Freddie Mac in 1970 to compete with Fannie Mae was a pivotal moment. The 2008 financial crisis led to conservatorship under the FHFA. These milestones have shaped the company's trajectory.

Freddie Mac continues to adapt to new trends, such as the increasing demand for affordable housing. It also integrates sustainable finance principles into its operations. This includes green financing initiatives.

Impact and Influence

Freddie Mac's influence is significant in the mortgage market. Its role in providing liquidity and guaranteeing mortgages has a broad impact. Understanding Freddie Mac mortgage operations is key to grasping its influence.

- Freddie Mac's guarantee of mortgage payments provides stability.

- It supports affordable housing initiatives.

- The company's actions influence mortgage interest rates.

- Freddie Mac's vast scale creates economies of scale.

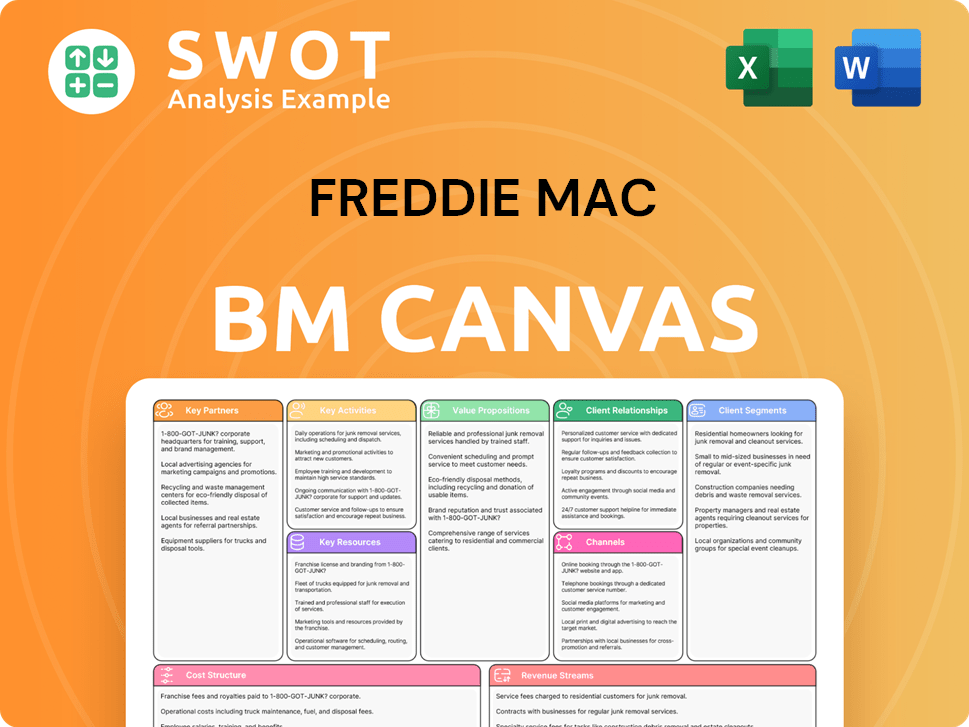

Freddie Mac Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Freddie Mac Positioning Itself for Continued Success?

Freddie Mac holds a pivotal position in the U.S. housing finance sector, functioning as a government-sponsored enterprise (GSE) alongside Fannie Mae. Together, they are fundamental to the mortgage market, setting standards for conforming loans and ensuring liquidity. Freddie Mac's consistent presence and standardized processes are vital, fostering customer loyalty among lenders. Its role in the secondary mortgage market is substantial, even though specific market share figures fluctuate.

Despite its strong standing, Freddie Mac faces challenges such as regulatory changes and economic fluctuations that impact mortgage originations and default rates. The future outlook for Freddie Mac involves adapting to housing market demands, managing risks, and navigating the ongoing debate surrounding its conservatorship. The company also focuses on technological advancements to streamline operations and enhance data analytics.

Freddie Mac is a key player in the U.S. housing market, acting as a GSE. It sets standards for conforming loans and provides crucial liquidity to the market. The company's influence extends to mortgage-backed securities and overall housing market stability.

Freddie Mac faces risks from regulatory changes and economic downturns, impacting mortgage originations and default rates. The company's operations are also subject to interest rate fluctuations. The emergence of fintech poses potential competitive challenges.

The future outlook involves adapting to evolving market demands and managing risks. Freddie Mac will continue to leverage its unique position to foster a robust mortgage finance system. It also focuses on responsible risk management and supporting underserved markets.

Freddie Mac operations involve purchasing mortgages from lenders and packaging them into mortgage-backed securities (MBS). The company guarantees these MBS, providing assurance to investors. This process ensures a continuous flow of funds for home loans.

Key Aspects of Freddie Mac

Freddie Mac's role in the housing market is significant, impacting mortgage rates and homeownership. It securitizes mortgages, ensuring liquidity in the market. For further insights, consider the Competitors Landscape of Freddie Mac.

- Guarantees mortgage payments to investors, mitigating risk.

- Sets standards for conforming loans, influencing mortgage rates.

- Supports affordable housing initiatives and underserved markets.

- Operates with a focus on risk management and financial stability.

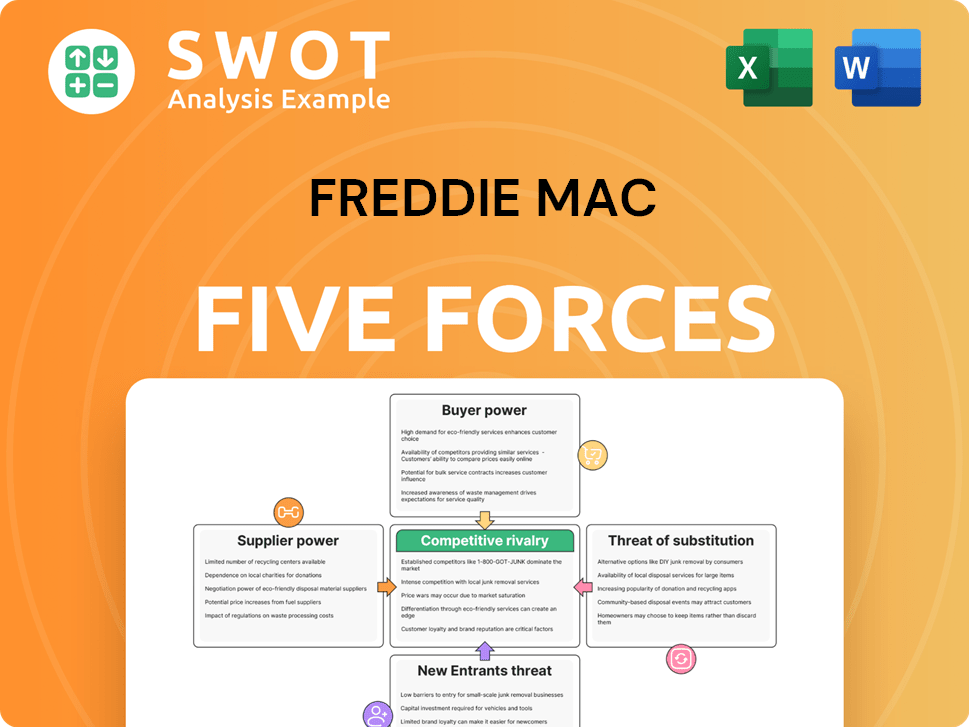

Freddie Mac Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Freddie Mac Company?

- What is Competitive Landscape of Freddie Mac Company?

- What is Growth Strategy and Future Prospects of Freddie Mac Company?

- What is Sales and Marketing Strategy of Freddie Mac Company?

- What is Brief History of Freddie Mac Company?

- Who Owns Freddie Mac Company?

- What is Customer Demographics and Target Market of Freddie Mac Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.