Freddie Mac Bundle

What's the Story Behind Freddie Mac?

Dive into the fascinating Freddie Mac SWOT Analysis, a cornerstone of the U.S. housing market, and uncover its pivotal role in shaping homeownership. Established in 1970, the Federal Home Loan Mortgage Corporation (Freddie Mac) revolutionized the mortgage industry. Explore how this government-sponsored enterprise (GSE) continues to impact the financial institutions and the housing market today.

This exploration into Freddie Mac's history will reveal its critical contributions to the mortgage industry. From its inception to its present-day operations, understanding the evolution of Freddie Mac is crucial for anyone interested in the housing market and the role of financial institutions. Learn about the brief history of Freddie Mac's founding and its ongoing mission to support affordable housing and stabilize the market, making it a key player in the financial landscape.

What is the Freddie Mac Founding Story?

The Federal Home Loan Mortgage Corporation, now known as Freddie Mac, was established on July 24, 1970. Its creation was a strategic move to strengthen the secondary mortgage market. This aimed to help savings and loan associations sell mortgages, freeing up capital for new loans, and addressing liquidity issues in the mortgage industry.

Freddie Mac's initial mission was to buy mortgages from lenders, mainly savings and loan associations. It then packaged these mortgages into mortgage-backed securities (MBS) for investors. This process, known as securitization, shifted risks and increased the flow of funds into the housing market.

The introduction of the participation certificate (PC) marked a significant innovation. It offered a standardized investment vehicle representing an interest in conventional mortgages. This attracted a broader investor base to the mortgage market, facilitating the growth of the mortgage industry.

Key Events in Freddie Mac's Founding

Freddie Mac was founded to address liquidity issues in the mortgage market and support financial institutions.

- Established on July 24, 1970, as the Federal Home Loan Mortgage Corporation.

- Created to enhance the secondary mortgage market.

- Initially purchased mortgages from lenders, especially savings and loan associations.

- Securitized mortgages into mortgage-backed securities (MBS).

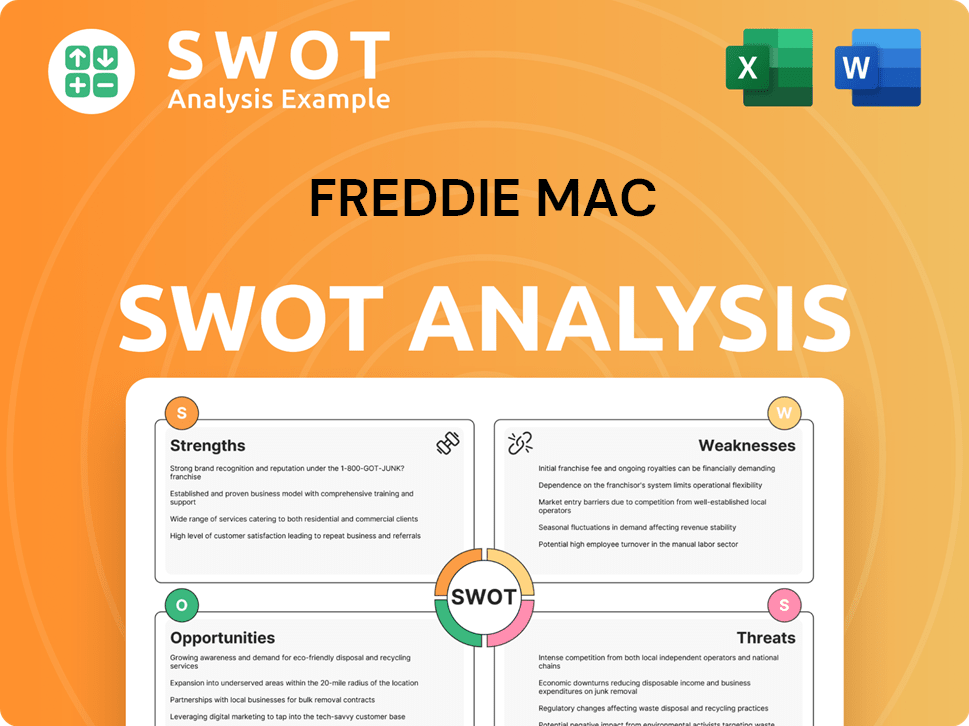

Freddie Mac SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of Freddie Mac?

During its early growth, the Federal Home Loan Mortgage Corporation, or Freddie Mac, focused on expanding the secondary mortgage market. This was achieved by increasing the volume of mortgages it purchased and securitized. The company established standardized underwriting guidelines and documentation requirements, making mortgages more attractive to investors. As the company grew, it broadened its reach beyond savings and loan associations, contributing to a more diversified mortgage market.

Key developments included the introduction of new types of mortgage-backed securities and the expansion of its programs to support various segments of the housing market. For instance, in 2024, Freddie Mac's multifamily production volume reached $66 billion, a 34% increase over 2023, supporting over 507,000 affordable rental units. The company also reported $1 billion in Low-Income Housing Tax Credit (LIHTC) equity investments in 2024.

In the first quarter of 2025, new business activity totaled $78 billion, an increase from $62 billion in the first quarter of 2024, with both home purchase and refinance activity increasing due to expanded market coverage and higher conforming loan limits. Freddie Mac financed 224,000 mortgages in Q1 2025, with 51% of eligible loans being affordable to low- to moderate-income families, and 52% of single-family loan purchases supporting first-time homebuyers.

The company also financed 89,000 rental units, with 92% being affordable to low- to moderate-income families. These efforts demonstrate a continuous evolution in its product offerings and market reach, adapting to the changing needs of the housing landscape and maintaining its mission of promoting housing affordability and stability. To learn more about the history of Freddie Mac, you can read more about it [here](0).

Freddie Mac's growth reflects its ongoing efforts to support the mortgage industry and housing market. Its ability to adapt to economic changes and expand its services has been crucial. The company's focus on affordable housing and its response to market needs highlight its role in the financial institutions landscape.

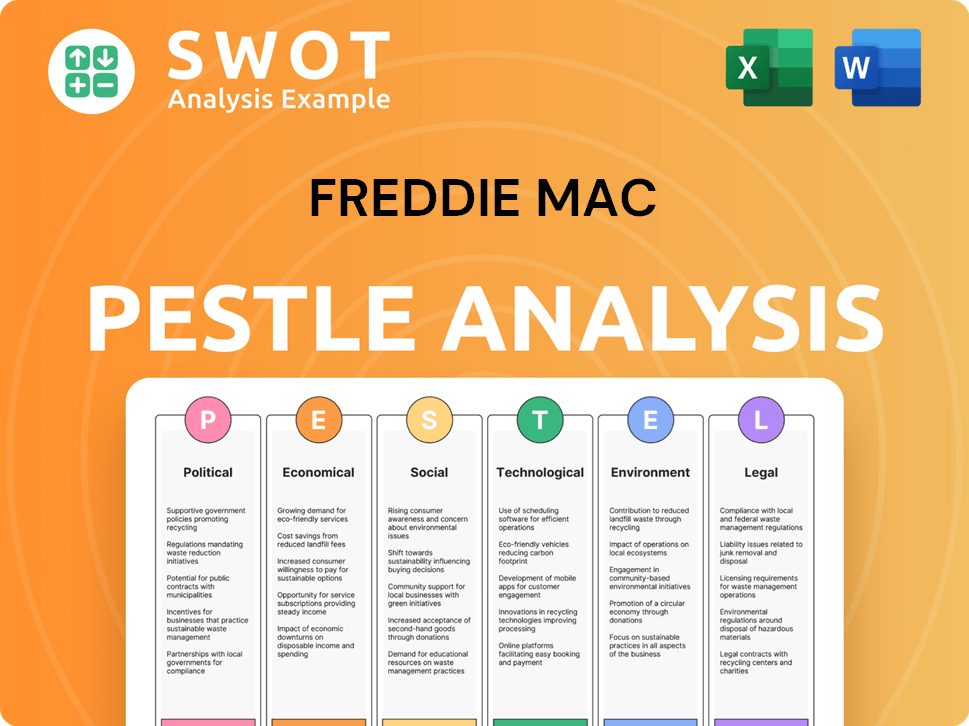

Freddie Mac PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in Freddie Mac history?

The Federal Home Loan Mortgage Corporation, or Freddie Mac, has a rich Freddie Mac history, marked by significant milestones that have shaped the mortgage industry. From its inception, the company has played a crucial role in the secondary mortgage market, influencing how financial institutions operate and how people access home financing.

| Year | Milestone |

|---|---|

| 1970 | Freddie Mac was established to provide a secondary market for mortgages, increasing the availability of funds for home loans. |

| 1980s | Freddie Mac introduced the participation certificate (PC), revolutionizing the secondary mortgage market by creating a liquid and standardized investment in mortgages. |

| 2008 | Freddie Mac was placed into conservatorship during the financial crisis, a pivotal moment in its history. |

| 2019-2024 | Freddie Mac issued $24 billion in total Impact Bond issuances, with $4.3 billion issued in 2024 alone, supporting affordable housing. |

| 2024 | Freddie Mac continued to innovate with various risk transfer offerings, such as its K-Deals in the multifamily sector, which transferred $27.7 billion. |

Freddie Mac has consistently introduced innovations to improve the efficiency and stability of the mortgage market. These innovations include risk transfer offerings and initiatives to support affordable housing, demonstrating its commitment to adapting to market needs.

Participation Certificates (PCs)

The introduction of PCs created a liquid market for mortgages, allowing financial institutions to free up capital and make more loans. This innovation standardized mortgage investments, making them more accessible to a wider range of investors.

K-Deals

Freddie Mac's K-Deals in the multifamily sector transferred $27.7 billion in risk in 2024. These risk transfer offerings help manage Freddie Mac's exposure to market fluctuations.

Multifamily Giant PCs and Q-Deals

In 2024, Freddie Mac introduced Multifamily Giant PCs and multi-sponsor Q-Deals to enhance its securitization platform. These innovations aim to improve the efficiency and attractiveness of mortgage-backed securities.

Impact Bonds

Freddie Mac has issued a total of $24 billion in Impact Bonds since 2019, with $4.3 billion issued in 2024. These bonds support affordable housing initiatives, demonstrating a commitment to social responsibility.

Despite its successes, Freddie Mac has faced significant challenges, particularly in the context of the housing market. The company's ability to navigate these challenges is critical to its long-term success and its mission to support the mortgage industry.

2008 Financial Crisis

The 2008 financial crisis led to Freddie Mac being placed into conservatorship, a major challenge that continues to impact its operations. The crisis highlighted the risks associated with the mortgage market and the need for robust risk management.

Housing Market Challenges

Ongoing challenges in the housing market, including high mortgage rates and limited inventory, have affected Freddie Mac's performance. The company initially predicted a 2.8% increase in home prices for 2024, but revised this forecast to just 0.5% annually.

Interest Rate Lock-in Effect

The average interest rate lock-in effect for conventional mortgage borrowers was estimated at $47,800 in November 2024. This reflects the impact of rising interest rates on borrowers and the market.

Multifamily Market Dynamics

In the multifamily sector, record-high supply in 2024 led to muted market fundamentals and increased vacancy rates, reaching 8.9% in Q4 2024. This indicates challenges in maintaining occupancy and profitability.

Low Mortgage Rates

In 2024, only 0.52% of Freddie Mac's loans had rates below 4%, a stark contrast to 79.67% in 2020. This shift reflects the impact of rising interest rates on the mortgage market.

Conservatorship

Freddie Mac is still working to exit conservatorship, a process that requires significant operational and financial adjustments. This ongoing process influences the company's strategic decisions and market activities.

For more insights into the ownership structure, you can read about the Owners & Shareholders of Freddie Mac.

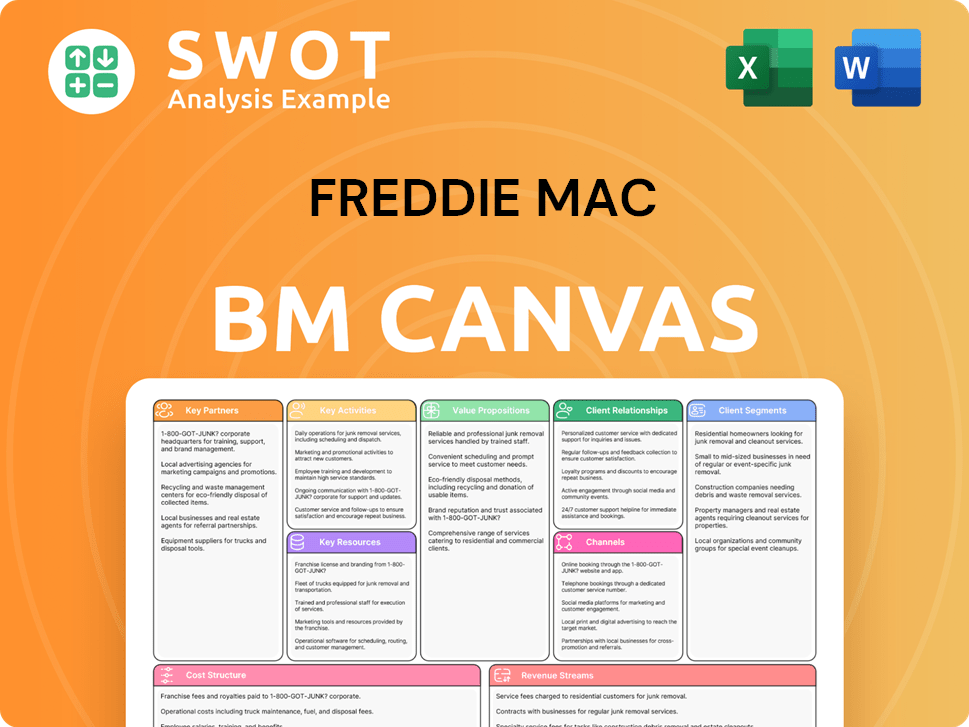

Freddie Mac Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for Freddie Mac?

The history of Freddie Mac, officially known as the Federal Home Loan Mortgage Corporation, is marked by significant milestones that have shaped the mortgage industry. Founded in 1970, it has played a critical role in the housing market. The company's journey includes periods of substantial growth and challenges, notably the 2008 financial crisis, which led to government conservatorship. Freddie Mac has since navigated through these turbulent times, adapting to evolving economic landscapes and regulatory changes while striving to fulfill its mission.

| Year | Key Event |

|---|---|

| 1970 | Founded as the Federal Home Loan Mortgage Corporation, marking the beginning of its role in the mortgage industry. |

| 2008 | Placed into conservatorship by the U.S. government during the financial crisis. |

| 2019 | FHFA published a new Strategic Plan for the conservatorships of Fannie Mae and Freddie Mac, aiming for a competitive, liquid, efficient, and resilient housing finance system. |

| 2024 Q3 | Real Gross Domestic Product (GDP) grew at 3.1%. |

| 2024 Q4 | Reported a net income of $3.2 billion, with full-year net income reaching $11.9 billion, up 13% from 2023. |

| 2024 | Multifamily production volume reached $66 billion, a 34% increase over 2023. |

| November 2024 | The Federal Housing Finance Agency (FHFA) announced a 5.2% increase in conforming loan limits for mortgages purchased by Freddie Mac and Fannie Mae for 2025, with the new limit for a one-unit home set at $806,500. |

| December 2024 | FHFA released the 2025 Scorecard for Fannie Mae and Freddie Mac, outlining objectives for safe and sound operations, risk management, and support for housing supply and affordability. |

| 2025 Q1 | Reported a net income of $2.8 billion, up 1% year-over-year. |

| 2025 | Multifamily loan purchase cap is set at $73 billion. |

Freddie Mac anticipates a moderate pace of economic growth in 2025. The company projects a modest increase in home sales. Refinance volumes are expected to rise due to slightly lower interest rates compared to 2024.

The company anticipates a moderation in the pace of house price appreciation, projecting a rate of 0.5% in 2025. Multifamily originations are expected to increase. Modest rent growth and slight increases in vacancy rates are also expected.

Freddie Mac plans to continue streamlining operations and reducing costs. The company aims to support mortgage affordability and maintain a safer and sounder financial position. The liquidation preference of its senior preferred stock is projected to increase to $135.1 billion by June 30, 2025.

In Q1 2025, Freddie Mac reported a net income of $2.8 billion, up 1% year-over-year. Net revenues for the same period were $5.9 billion, a 2% increase. The mortgage portfolio reached $3.1 trillion, up 2% year-over-year.

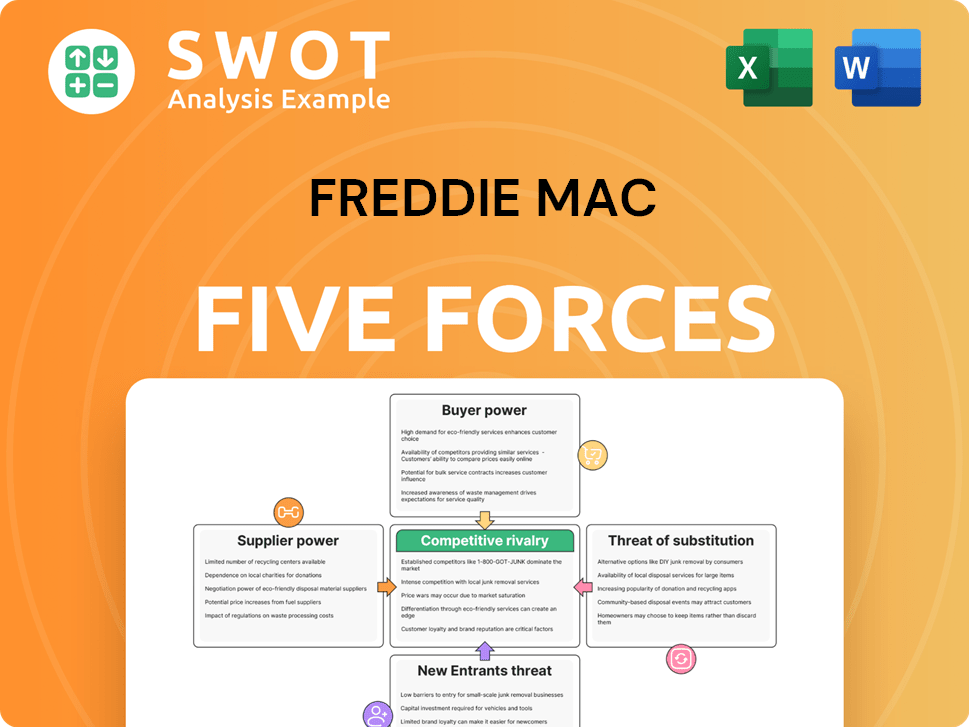

Freddie Mac Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of Freddie Mac Company?

- What is Growth Strategy and Future Prospects of Freddie Mac Company?

- How Does Freddie Mac Company Work?

- What is Sales and Marketing Strategy of Freddie Mac Company?

- What is Brief History of Freddie Mac Company?

- Who Owns Freddie Mac Company?

- What is Customer Demographics and Target Market of Freddie Mac Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.