Credito Real Bundle

What Went Wrong at Credito Real?

Crédito Real, a once-dominant force in Mexican finance, offered crucial Credito Real SWOT Analysis financial services to underserved populations. This non-bank financial institution (NBFI) provided specialized Credito Real loans, including payroll, micro, and small business loans, aiming to bridge the gap left by traditional banks. Understanding the inner workings of the Credito Real company is essential, especially given its eventual liquidation and the implications for investors and the broader financial landscape.

The story of Credito Real Mexico is a cautionary tale, highlighting the importance of rigorous risk management and adaptability. Analyzing its business model reveals critical lessons for anyone involved in Credito Real investment or interested in the dynamics of specialized lending. Exploring Credito Real financial services offers insights into the challenges and opportunities within the NBFI sector, impacting everything from Credito Real financial products to Credito Real loan interest rates.

What Are the Key Operations Driving Credito Real’s Success?

The core operations of the Credito Real company revolved around providing various financial products, mainly targeting specific customer segments in Mexico. Their offerings were tailored to meet the financial needs of individuals and small businesses, which included payroll loans, microloans, and small business loans. They also offered auto loans and durable goods loans, expanding their financial services to a broader consumer base.

Credito Real's value proposition centered on accessibility and speed, offering a viable alternative to traditional banking and informal lending. The company focused on understanding and mitigating the unique risks associated with its target segments. This allowed them to provide financial solutions where others couldn't, contributing to local economic development.

The operational processes behind these offerings involved a robust credit assessment framework. This framework was designed to evaluate the creditworthiness of individuals and small businesses that might not have extensive credit histories with traditional banks. The company used a network of branches and partnerships to reach its target demographic, utilizing direct sales forces and collaborations with employers for payroll loan distribution.

Credito Real offered a range of financial products. These included payroll loans, microloans, small business loans, auto loans, and durable goods loans. These products aimed to meet diverse financial needs within Mexico.

The company used a robust credit assessment framework. This framework evaluated the creditworthiness of individuals and small businesses. They used alternative data and personalized client interactions to assess risk.

Credito Real focused on accessibility and speed of loan disbursement. It served as an alternative to informal lending sources. This approach catered to urgent financial needs, making it a valuable option for many.

The primary target market for Credito Real was in Mexico. It specifically catered to underserved customer segments. This included individuals and small businesses with limited access to traditional financial services.

Key Features of Credito Real

Credito Real's operations were designed to provide accessible financial solutions. They focused on meeting the needs of underserved markets in Mexico. Their approach included tailored financial products, efficient credit assessments, and a wide distribution network.

- Payroll Loans: Offered based on salary, with direct deductions to reduce risk.

- Microloans and Small Business Loans: Provided capital for growth and operational needs.

- Auto and Durable Goods Loans: Enabled consumers to acquire vehicles and essential items.

- Credit Assessment: Used alternative data and personalized interactions.

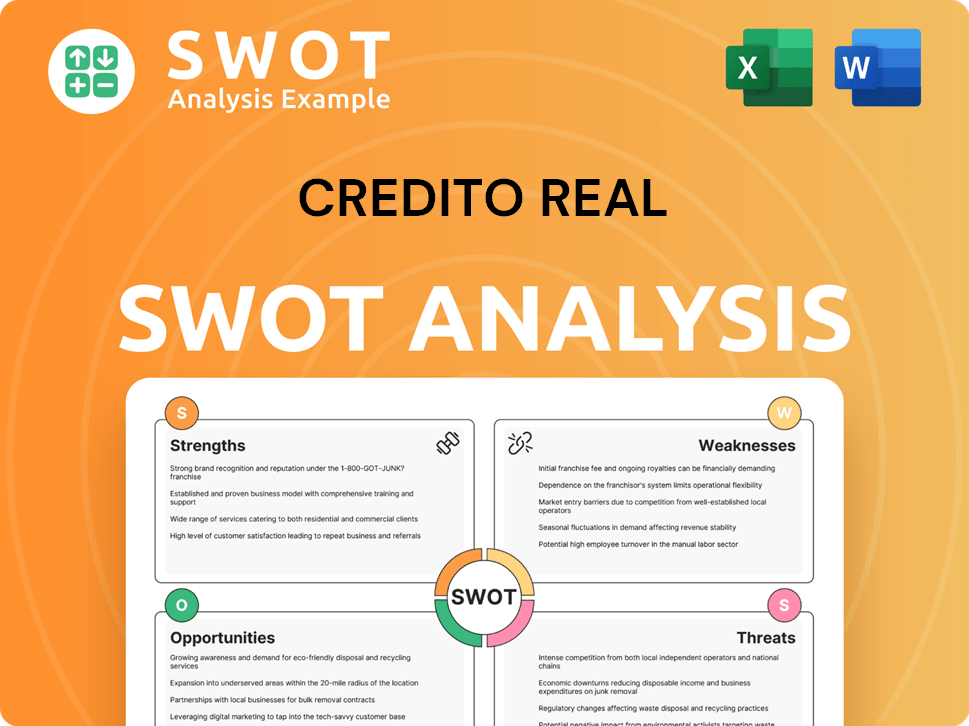

Credito Real SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Credito Real Make Money?

The Credito Real company, which offered financial services, primarily generated revenue through interest income derived from its loan portfolio. This revenue stream was the cornerstone of its financial model, encompassing a variety of loan products tailored to different market segments. The company's ability to effectively manage and monetize its loan portfolio was critical to its overall financial performance.

Credito Real's monetization strategy focused on maximizing interest income from its diverse loan offerings. These included payroll loans, microloans, small business loans, auto loans, and loans for durable goods. The company aimed to serve a broad customer base, often catering to underserved segments with higher perceived risk, which allowed for higher interest rates compared to traditional bank loans.

The company's revenue model was designed to capitalize on the demand for accessible credit solutions within its target markets. Although specific recent financial data isn't available due to the company's liquidation status, historical financial reports would have highlighted the significance of interest income as the dominant revenue source. This approach, combined with additional fees, supported the company's financial operations.

Interest Income

The primary revenue source for Credito Real was interest earned on its loan portfolio. This income stream was generated from various loan products, including payroll loans, microloans, and auto loans.

Loan Origination and Service Fees

Besides interest, Credito Real also charged origination fees, late payment penalties, and other service charges. While the exact contribution of these fees to total revenue isn't specified, they supplemented the primary income stream.

Risk-Based Pricing

Interest rates were adjusted based on the risk profile of borrowers and the loan type. This approach allowed Credito Real to manage risk and optimize profitability across different market segments.

Market Focus

Credito Real targeted underserved markets, which allowed for higher interest rates. This focus was a key element of the company's monetization strategy, enabling it to generate revenue from a customer base that might not have access to traditional banking services.

Loan Portfolio Diversification

The company diversified its loan offerings to manage risk and cater to a wide range of customer needs. This diversification helped stabilize revenue streams and mitigate the impact of defaults in any single loan category.

Volume and Efficiency

Credito Real aimed to offset higher individual loan risks by efficiently managing a large volume of loans. This strategy required effective risk assessment and streamlined operational processes to maintain profitability.

The company's ability to generate revenue was closely tied to its loan portfolio's performance and the economic conditions affecting its target markets. For more details about the company's stakeholders, you can read about the Owners & Shareholders of Credito Real.

Key Revenue Streams and Strategies

Credito Real's revenue model was primarily driven by interest income, supplemented by fees and charges. The company's strategy involved risk-based pricing, market focus, and portfolio diversification to maximize revenue generation.

- Interest Income: The core revenue source, derived from interest charged on loans.

- Fees and Charges: Origination fees, late payment penalties, and service charges added to revenue.

- Risk-Based Pricing: Interest rates varied based on borrower risk and loan type.

- Market Focus: Targeting underserved markets allowed for higher interest rates.

- Loan Portfolio Diversification: Offered various loan products to manage risk.

- Volume and Efficiency: Aimed to manage a large loan volume efficiently.

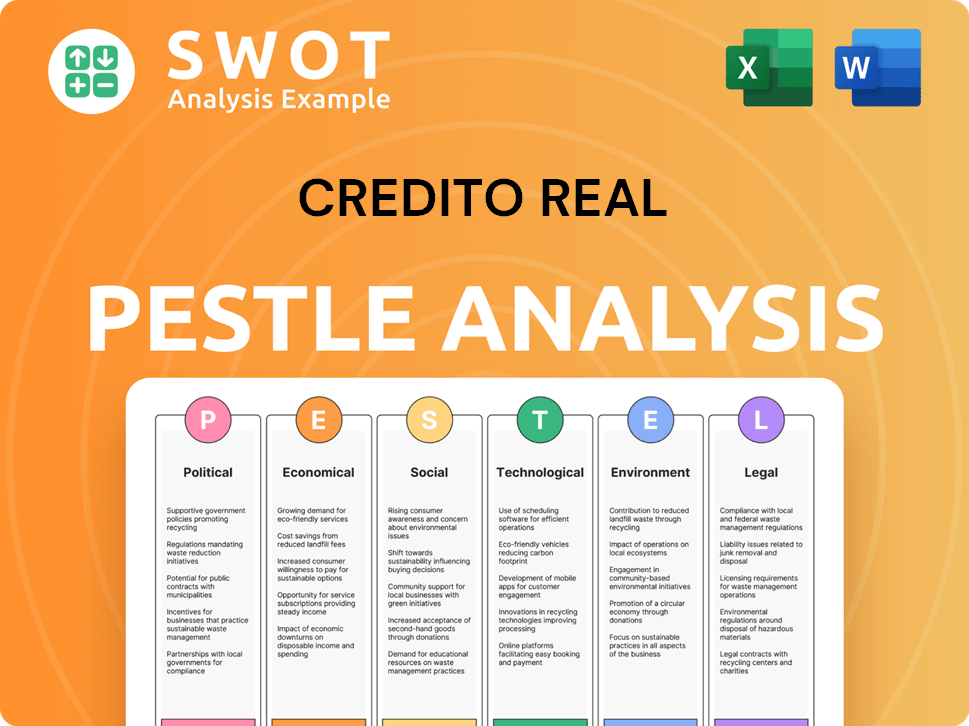

Credito Real PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Credito Real’s Business Model?

The trajectory of the Credito Real company, a prominent player in Mexico's non-bank lending sector, was marked by significant expansion and strategic shifts. Initially, the company focused on payroll lending, a strategy that provided a relatively stable revenue stream due to the direct deduction of loan repayments from borrowers' salaries. This approach, combined with strategic partnerships and a growing branch network, enabled the company to penetrate underserved communities and establish a strong market presence.

Key milestones included expanding its loan portfolio and geographic footprint. The company aimed to meet the financial needs of a broad customer base. However, the company faced substantial challenges, including regulatory hurdles, economic downturns that impacted borrowers' ability to repay, and heightened competition within the financial services industry. These factors, coupled with increasing debt and potentially inadequate risk management, ultimately led to its financial distress and liquidation.

The competitive edge of Credito Real, initially rooted in its specialization and access to underserved markets, was gradually eroded. Escalating debt, unfavorable market conditions, and potentially inadequate risk management in a highly sensitive lending environment contributed to its decline. The company's attempts to adapt to new trends and competitive threats were ultimately insufficient to overcome its financial difficulties, leading to a significant business model pivot towards asset liquidation rather than continued operations.

Early expansion focused on payroll lending, providing a stable revenue stream. Strategic partnerships and branch network expansion increased its reach into underserved communities. Faced challenges like regulatory hurdles and economic downturns impacting loan repayments.

Focused on payroll lending for stable revenue. Expanded its reach through partnerships and branch networks. Attempted to adapt to new trends but failed to overcome financial difficulties. Shifted towards asset liquidation due to financial distress.

Initially specialized in payroll lending and access to underserved markets. Eroded by escalating debt and unfavorable market conditions. Inadequate risk management contributed to its decline. The inability to meet debt obligations signaled operational distress.

Regulatory hurdles and economic downturns impacted loan repayments. Increased competition within the financial services industry. Escalating debt and potentially inadequate risk management. Ultimately, the company faced liquidation due to its inability to meet debt obligations.

Financial Distress and Liquidation

The ultimate failure of Credito Real stemmed from its inability to manage its debt obligations, leading to its liquidation. This failure highlights the risks associated with high debt levels and the importance of effective risk management, especially in the non-bank lending sector. The company's experience serves as a cautionary tale about the impact of economic downturns and increased competition on financial institutions.

- Inability to meet debt obligations.

- Inadequate risk management practices.

- Impact of economic downturns on borrowers.

- Increased competition in the lending market.

For a deeper understanding of the strategic decisions and market dynamics that influenced Credito Real's performance, further analysis is available in the Growth Strategy of Credito Real.

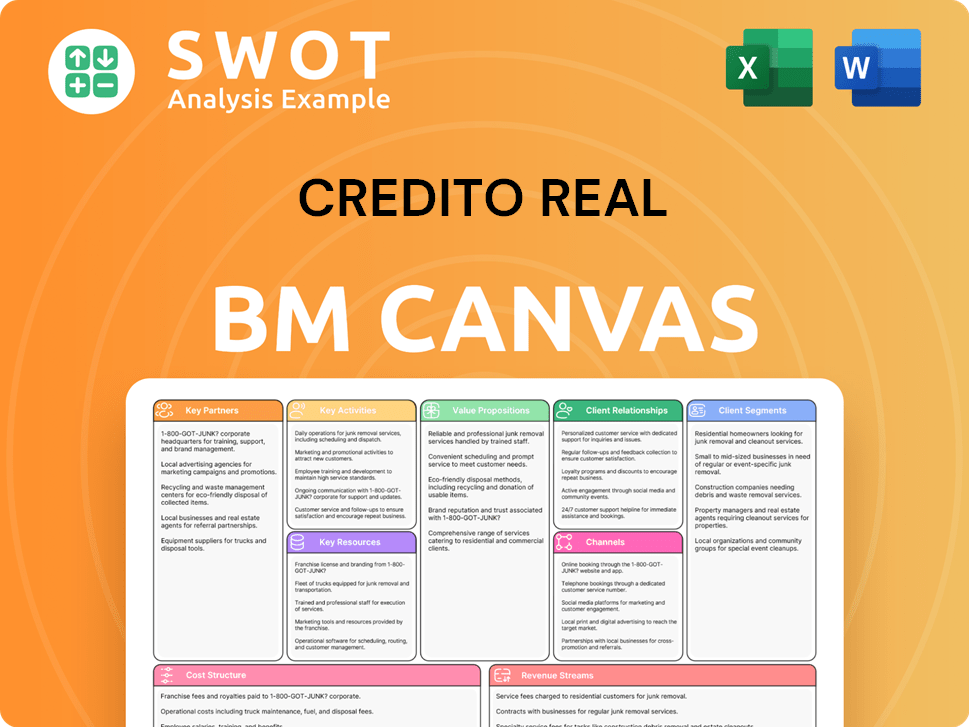

Credito Real Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Credito Real Positioning Itself for Continued Success?

Before its liquidation, the Credito Real company held a prominent position in Mexico's non-bank financial institution sector. It offered specialized loans to groups often overlooked by larger banks. The company's market share was concentrated in niche areas like payroll lending and microfinance, making it a significant player in these segments. However, this position was built on a foundation that proved unsustainable.

The Credito Real loans business faced considerable risks, including credit risk from its borrowers, interest rate risk, and refinancing risk due to its reliance on wholesale funding. Regulatory changes and increasing competition from traditional banks and other NBFIs also posed ongoing threats. Ultimately, these risks led to the company's downfall, as it was unable to service its debt, resulting in default and liquidation.

Credito Real Mexico specialized in providing financial services, particularly focusing on payroll lending and microfinance. This focus allowed the company to capture a specific market segment within the broader financial landscape. However, its position was vulnerable due to the nature of its target borrowers and funding sources.

The company faced substantial risks, including credit risk, interest rate risk, and refinancing risk. Credit risk stemmed from the potential inability of borrowers to repay their loans. Interest rate risk arose from fluctuations in interest rates, impacting profitability. Refinancing risk was a major concern given its reliance on wholesale funding. The Competitors Landscape of Credito Real shows how market dynamics influenced its performance.

Given its liquidation, the future outlook for Credito Real as an operating entity is nonexistent. The focus has shifted to the orderly winding down of its assets to repay creditors. This situation highlights the vulnerabilities within the specialized lending sector, particularly for institutions with high leverage and exposure to economically sensitive borrower segments.

Prior to its financial difficulties, the company's financial performance showed periods of growth, but also increasing debt levels. Specific financial data regarding its performance, such as quarterly reports and annual reports, would provide a complete view of its financial health before its collapse. The company's financial performance in previous years showed varying levels of profitability and debt.

Key Takeaways

The collapse of Credito Real serves as a cautionary tale for investors and financial institutions. The company's failure underscores the importance of prudent risk management and the dangers of over-reliance on wholesale funding.

- The company's business model, focusing on specialized lending, was not inherently flawed, but its execution and risk management were insufficient.

- The reliance on wholesale funding made it vulnerable to market fluctuations and refinancing risks.

- Regulatory changes and increased competition added to the challenges the company faced.

- The liquidation process aims to recover value for creditors, but the ultimate recovery rate is uncertain.

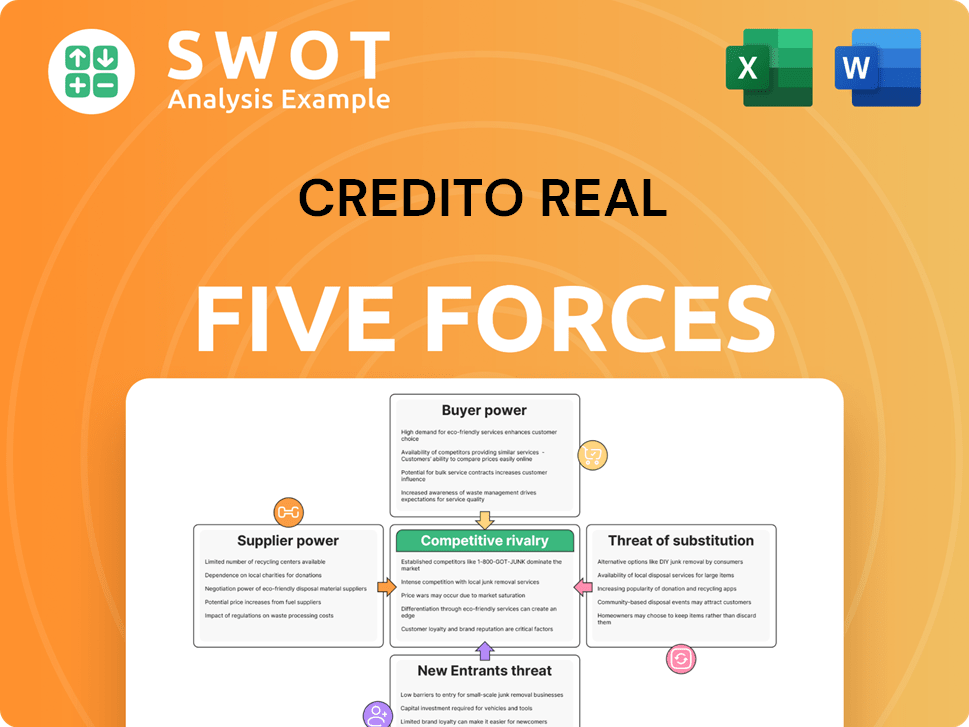

Credito Real Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Credito Real Company?

- What is Competitive Landscape of Credito Real Company?

- What is Growth Strategy and Future Prospects of Credito Real Company?

- What is Sales and Marketing Strategy of Credito Real Company?

- What is Brief History of Credito Real Company?

- Who Owns Credito Real Company?

- What is Customer Demographics and Target Market of Credito Real Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.