Credito Real Bundle

What Caused Crédito Real's Downfall?

The liquidation of Crédito Real, a major Mexican non-bank financial institution, signals a critical moment for understanding the dynamics of specialized lending. This event shines a light on the competitive landscape, exposing the vulnerabilities and risks within the financial services sector catering to underserved communities. Exploring the factors that led to Crédito Real's challenges offers crucial insights into the broader market.

This article provides a deep dive into the Credito Real SWOT Analysis, examining its Credito Real competitive landscape and the strategies employed by its rivals. We'll dissect the Credito Real competitors, analyze their strengths and weaknesses, and assess the impact of the regulatory environment. This Credito Real market analysis will reveal the pressures faced by NBFIs and the factors influencing their Credito Real financial performance within the Credito Real industry analysis, offering a comprehensive view of their Credito Real business strategy and the broader financial ecosystem.

Where Does Credito Real’ Stand in the Current Market?

Prior to its liquidation, the company held a significant position within Mexico's non-bank financial institution sector. While specific market share figures for 2024-2025 aren't applicable due to its liquidation, historical data indicates its presence in payroll lending and microfinance. This targeted individuals and small businesses often excluded from traditional banking services. The company's primary offerings included payroll loans, microloans, and small business loans, alongside financing for autos and durable goods.

The firm's geographic focus was primarily within Mexico. It served a broad demographic, including government employees and small entrepreneurs. Over time, the company attempted to diversify its offerings and broaden its client base. However, its financial health deteriorated significantly leading up to its insolvency. The company's strategic shifts and financial woes significantly impacted its market standing.

In 2022, the company reported a net loss of 2.15 billion Mexican pesos, a stark contrast to its earlier growth phases. Its debt obligations became unsustainable, leading to a default on a bond payment in February 2022 and subsequent bankruptcy proceedings. This marked a dramatic shift from its earlier standing, where it was considered a key provider of credit to underserved segments. The company's weak financial position, marked by high leverage and a challenging macroeconomic environment, ultimately undermined its market standing and led to its collapse. For a deeper understanding, explore the Revenue Streams & Business Model of Credito Real.

The company's primary market was Mexico, focusing on payroll lending, microloans, and small business loans. It served a broad demographic, including government employees and small entrepreneurs. The company's focus was on providing financial services to underserved segments of the population.

Key product lines included payroll loans, microloans, and small business loans. It also offered financing for autos and durable goods. These offerings were designed to cater to the financial needs of individuals and small businesses.

The company experienced a significant downturn, reporting a net loss of 2.15 billion Mexican pesos in 2022. This financial strain led to unsustainable debt obligations and eventual bankruptcy. The decline in financial health undermined its market position.

The company attempted to diversify its offerings and reach a wider client base. However, these efforts were not enough to offset the deteriorating financial conditions. These strategic moves were insufficient to prevent the company's collapse.

Credito Real Competitive Landscape Analysis

The company's competitive landscape was significantly impacted by its financial struggles and eventual liquidation. The Credito Real competitive landscape shifted dramatically. Key competitors in the financial services industry have likely absorbed its former market share.

- The Credito Real competitors include other non-bank financial institutions and traditional banks.

- Its Credito Real market analysis reveals the impact of its failure on the financial services sector.

- The company's Credito Real key competitors 2024 are those that have gained market share.

- The Credito Real financial services industry rivals have adjusted strategies.

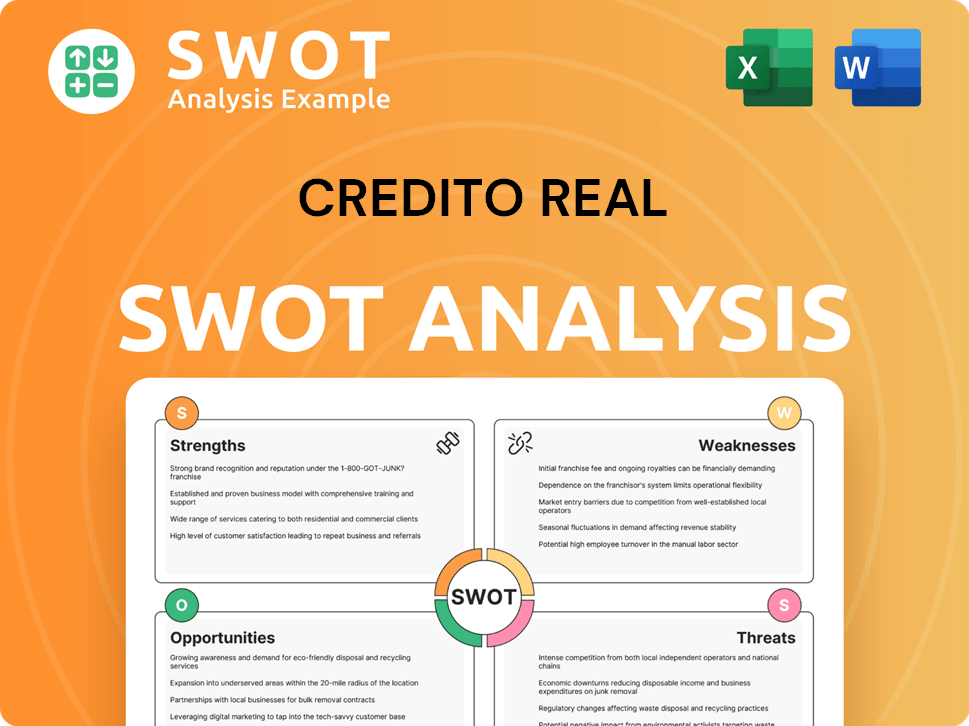

Credito Real SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

Who Are the Main Competitors Challenging Credito Real?

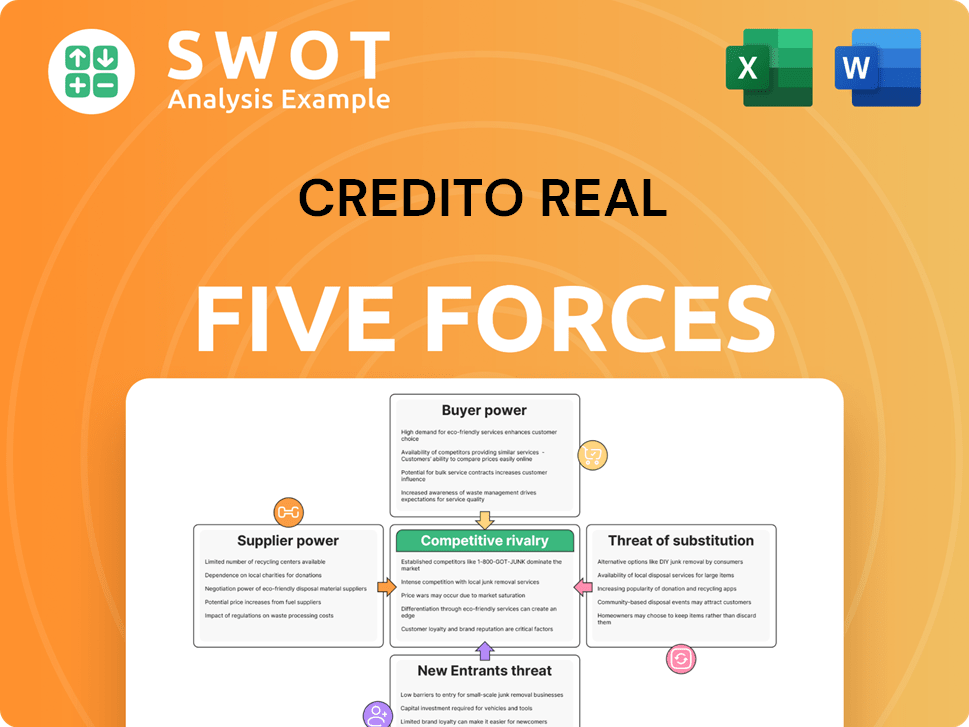

The Credito Real competitive landscape was defined by a mix of specialized non-bank financial institutions (NBFIs), fintech companies, and, to a lesser extent, traditional banks. This environment was particularly dynamic, with various players vying for market share in the underserved lending segments that Crédito Real targeted. Understanding the key competitors and their strategies is essential for a thorough Crédito Real market analysis.

The Mexican financial sector's competitive dynamics have been significantly shaped by the rise of fintech and the strategic responses of established players. While specific 2024-2025 data on the exact market shares of competitors relative to Crédito Real is difficult to ascertain due to its liquidation, the historical context provides valuable insights into the competitive pressures it faced. Crédito Real's business strategy was constantly challenged by the actions of its rivals.

Direct competitors of Crédito Real included other payroll lenders and microfinance institutions, which focused on similar underserved customer segments. These entities often utilized aggressive pricing, localized distribution networks, and tailored credit products to compete. Indirect competition came from the burgeoning fintech sector, which offered digital lending solutions, including personal loans, small business financing, and buy-now-pay-later (BNPL) services.

Direct Competitors

Key direct competitors included other payroll lenders and microfinance institutions. These institutions targeted similar customer segments as Crédito Real, often competing on price and product customization.

Indirect Competitors

Fintech companies offering digital lending solutions provided indirect competition. Traditional banks, though less focused on the same segments, also posed a competitive threat through their smaller credit offerings.

Market Dynamics

The competitive landscape was influenced by new entrants, mergers, and alliances. The Mexican NBFI sector has seen consolidation due to financial difficulties rather than strategic expansion in recent years.

Competitive Strategies

Competitors employed strategies like aggressive pricing, localized distribution, and tailored credit products. Fintech companies leveraged technology for faster approvals and convenient access to funds.

Regulatory Environment

The regulatory environment impacted competitors, influencing their operational strategies and financial performance. The sector's regulatory framework plays a crucial role.

Economic Impact

Economic downturns significantly impacted competitors, affecting their loan portfolios and profitability. These challenges are critical for understanding the financial services industry rivals.

Key Competitive Factors

The competitive landscape was shaped by several key factors. These factors influenced the Credito Real market analysis and the overall industry dynamics. Understanding these factors is crucial for assessing the competitive advantages and disadvantages of each player.

- Pricing Strategies: Competitors often used aggressive pricing to attract customers.

- Distribution Networks: Localized distribution networks enabled competitors to reach specific customer segments.

- Product Customization: Tailored credit products met the unique needs of different customer groups.

- Technological Innovation: Fintech companies offered faster approval processes and convenient access to funds.

- Regulatory Compliance: Adherence to the regulatory environment was essential for all players.

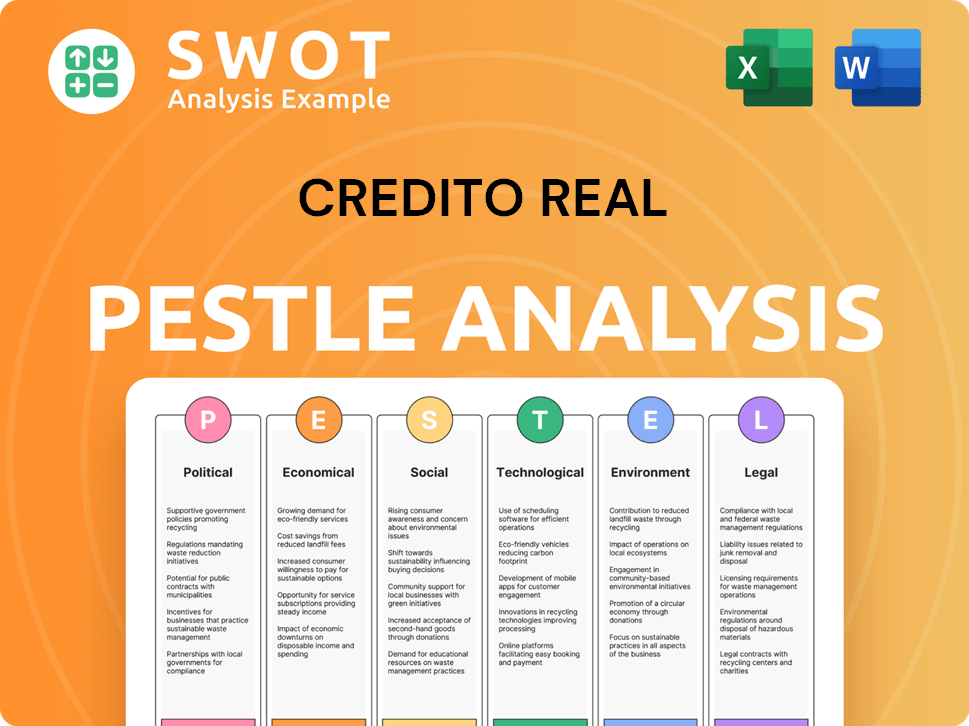

Credito Real PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Gives Credito Real a Competitive Edge Over Its Rivals?

Prior to its insolvency, the company, aimed to establish several competitive advantages. A key strategy involved focusing on underserved segments of the Mexican population, offering tailored financial products such as payroll loans, microloans, and small business loans. This specialization, combined with a network of branches and partnerships, aimed to provide accessibility to its target customers. The company also sought to build customer loyalty through personalized service and a streamlined application process.

Historically, the ability to assess risk within its specific customer base, using alternative data points for credit scoring, could have been considered an advantage. The company invested in technology to improve operational efficiencies and customer experience. However, these efforts proved insufficient to overcome macroeconomic headwinds, increasing competition, and internal financial vulnerabilities. The brand equity built over nearly three decades was eroded by financial distress and negative publicity.

The company's advantages, while present, were not robust enough to withstand significant market shifts and internal financial pressures, ultimately proving unsustainable in the face of mounting debt and a changing regulatory environment. A thorough Credito Real market analysis reveals the challenges faced in maintaining a competitive edge.

The company focused on providing financial products like payroll loans, microloans, and small business loans tailored to the underserved segments of the Mexican population. This specialization allowed it to cater to a niche market that traditional banks often overlooked. This strategy was a key element in its initial competitive approach.

The company utilized a network of branches and strategic partnerships to enhance accessibility to its target customers. This distribution strategy was crucial in reaching the specific demographic it aimed to serve. The network's effectiveness was essential for customer acquisition and service delivery.

The company aimed to build customer loyalty through personalized service and a streamlined application process. This approach was designed to differentiate it from larger financial institutions. The focus on customer experience was intended to improve customer retention.

The company developed the ability to assess risk within its specific customer base, utilizing alternative data points for credit scoring. This capability was intended to provide an advantage in lending decisions. Risk assessment played a crucial role in its financial performance.

Challenges and Unsustainability

Despite these initial advantages, the company faced significant challenges that ultimately led to its downfall. Macroeconomic headwinds, increasing competition, and internal financial vulnerabilities eroded its competitive position. The company's financial distress and negative publicity further damaged its brand equity.

- Economic Downturn: The impact of economic downturns significantly affected the company's loan portfolio and repayment rates.

- Increased Competition: The financial services industry in Mexico became increasingly competitive, putting pressure on margins and market share.

- Regulatory Environment: Changes in the regulatory environment added to the challenges, impacting the company's operations.

- Financial Vulnerabilities: Internal financial issues, including mounting debt, proved unsustainable.

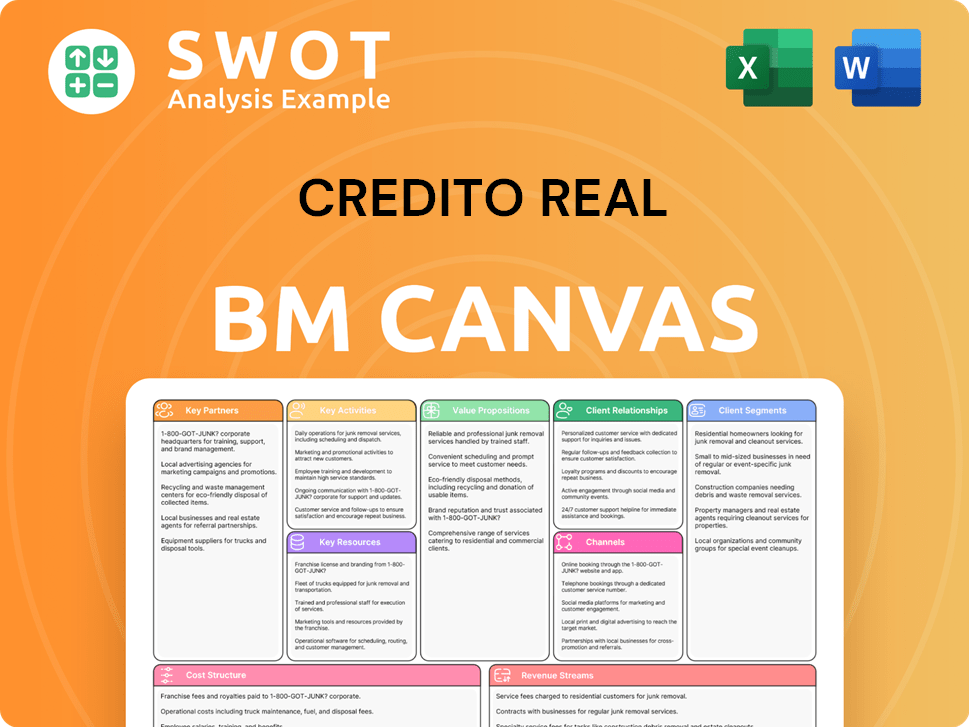

Credito Real Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Industry Trends Are Reshaping Credito Real’s Competitive Landscape?

The non-bank financial institution (NBFI) sector in Mexico, including the space once occupied by Crédito Real, is currently shaped by significant industry trends. These trends include technological advancements, changes in the regulatory landscape, and shifts in consumer preferences. A thorough Credito Real market analysis reveals the sector's dynamic nature. The rise of fintech platforms continues to disrupt traditional lending models, offering faster, more convenient, and often more personalized financial services. This creates both challenges and opportunities, requiring NBFIs to invest in digital transformation while expanding their reach to a digitally-savvy customer base.

Regulatory changes, particularly those aimed at strengthening financial stability and consumer protection, pose ongoing challenges. These changes necessitate that NBFIs adapt their compliance frameworks and operational practices. Understanding the Credito Real competitive landscape involves assessing these factors. The experience of Crédito Real serves as a reminder of the potential for rapid financial deterioration if these challenges are not effectively managed. The competitive landscape now also includes fintech companies offering similar services.

Technological advancements, especially in fintech, are reshaping lending. The regulatory landscape is evolving to enhance financial stability and consumer protection. Consumer preferences are shifting towards digital and personalized financial services. These trends significantly impact the Credito Real competitors and the broader market.

Managing credit risk in volatile economic conditions is a key challenge. Securing adequate funding and navigating stringent regulatory oversight are also significant hurdles. The ability to adapt to rapid changes in the market and maintain financial health is crucial. These challenges are central to the Credito Real industry analysis.

Expanding financial inclusion through innovative product offerings is a major opportunity. Leveraging data analytics for more precise credit assessments can improve efficiency. Forming strategic partnerships with fintech companies can enhance reach and capabilities. These opportunities are vital for the future of surviving NBFIs.

The competitive position of surviving NBFIs hinges on digital transformation and robust risk management. Swift adaptation to market and regulatory dynamics is essential for success. Understanding Credito Real financial performance and its impact on the market is critical. The sector's future is about resilience and innovation.

Key Factors for Success

The ability to embrace digital transformation is crucial for NBFIs. Maintaining robust risk management practices is essential for financial stability. Adapting swiftly to evolving market and regulatory dynamics is key to long-term success. For more context on the company's history, consider reading Brief History of Credito Real.

- Digital Transformation: Investing in technology to offer online services and improve customer experience.

- Risk Management: Implementing strong credit assessment and monitoring processes.

- Regulatory Compliance: Staying updated with changes in financial regulations.

- Strategic Partnerships: Collaborating with fintech companies or larger financial institutions.

Credito Real Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Credito Real Company?

- What is Growth Strategy and Future Prospects of Credito Real Company?

- How Does Credito Real Company Work?

- What is Sales and Marketing Strategy of Credito Real Company?

- What is Brief History of Credito Real Company?

- Who Owns Credito Real Company?

- What is Customer Demographics and Target Market of Credito Real Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.