Consumer Portfolio Services Bundle

How Does Consumer Portfolio Services Thrive in the Auto Loan Market?

Consumer Portfolio Services (CPS) is a key player in subprime auto lending, a sector vital for vehicle ownership among those with less-than-perfect credit. Its strategic partnerships with dealerships and focus on Consumer Portfolio Services SWOT Analysis highlights its significance in consumer finance. Understanding CPS is crucial for investors, customers, and industry analysts alike.

CPS's business model revolves around purchasing and servicing CPS loans, primarily through dealerships. With the subprime auto loan market constantly shifting, including factors like interest rates, understanding CPS auto financing is critical. This analysis will explore how CPS operates, generates revenue, and manages risk within the dynamic landscape of subprime auto loans, offering insights into its value proposition and strategic positioning. Considering questions like "How does Consumer Portfolio Services approve loans?" and analyzing Consumer Portfolio Services customer reviews can provide a deeper understanding of their approach to car financing.

What Are the Key Operations Driving Consumer Portfolio Services’s Success?

Consumer Portfolio Services (CPS) operates as a financial intermediary, specializing in subprime auto loans. Their core business revolves around purchasing and servicing these loans, primarily through partnerships with auto dealerships across the United States. This approach allows CPS to cater to a specific market segment: consumers with less-than-perfect credit histories who may struggle to secure financing elsewhere.

The value proposition of CPS lies in its ability to provide auto financing to individuals often excluded by traditional lenders. By focusing on subprime auto loans, CPS fills a critical gap in the market, enabling access to vehicles for a broader range of consumers. This is achieved through a streamlined process that leverages a network of dealers and a proprietary underwriting system.

The operational model of CPS is built on indirect lending, where loan applications originate from dealerships. CPS then assesses each applicant's creditworthiness using its proprietary system, considering factors beyond traditional credit scores. Once a loan is approved, CPS handles the servicing, including payment collection and delinquency management. This specialized expertise in subprime lending and efficient loan servicing differentiates CPS from other lenders.

CPS partners with auto dealers to originate CPS loans. Dealers submit loan applications on behalf of customers. This indirect lending model is a key part of their operational strategy.

CPS uses a proprietary credit underwriting system. The system assesses risk and determines loan terms. This system considers factors beyond traditional credit scores.

Once a loan is approved, CPS handles all servicing responsibilities. This includes collecting payments and managing delinquencies. Efficient loan servicing is crucial for profitability.

CPS offers car financing to consumers with subprime credit. This provides access to transportation for those who might be denied by other lenders. The company's value is in serving this specific market.

Key Differentiators

CPS distinguishes itself through its specialized expertise in subprime credit assessment and robust loan servicing. Their established dealer relationships provide a consistent flow of business. This focus allows them to serve a market segment often overlooked by traditional lenders.

- Specialized in subprime auto loans.

- Strong dealer network for loan origination.

- Proprietary underwriting system for risk assessment.

- Efficient loan servicing capabilities.

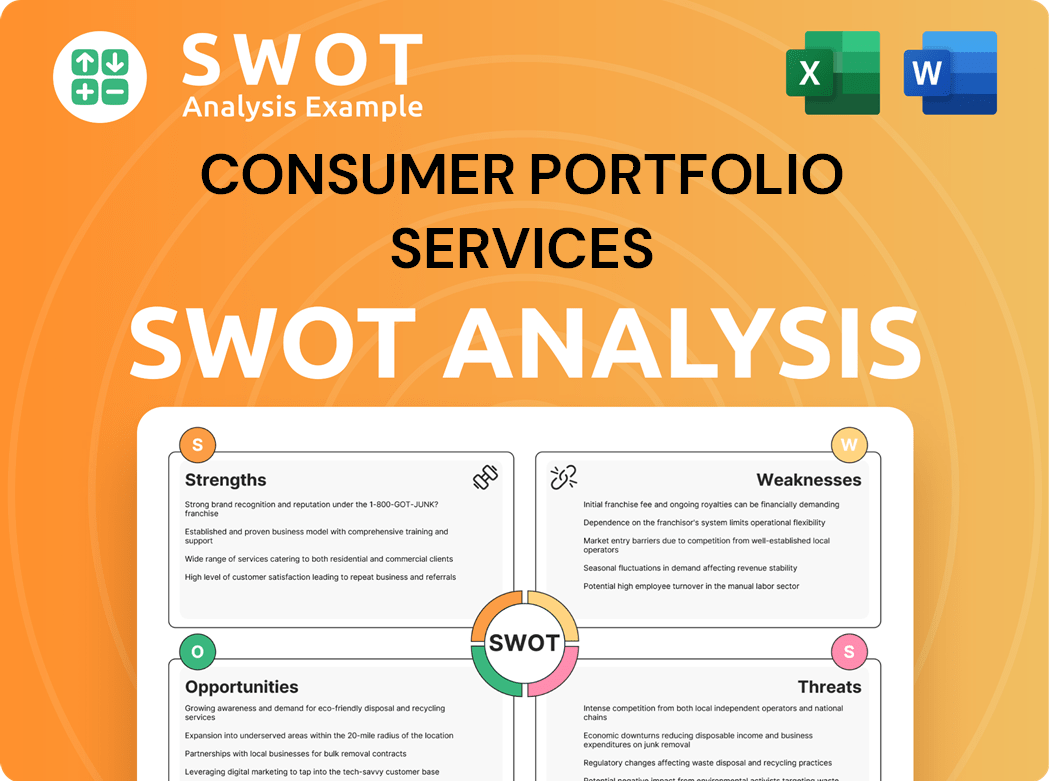

Consumer Portfolio Services SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Consumer Portfolio Services Make Money?

The revenue streams and monetization strategies of Consumer Portfolio Services (CPS) are centered around its core business of providing and servicing auto loans, particularly to subprime borrowers. This approach allows the company to generate income through various channels, with a primary focus on finance charges and interest income.

The primary revenue stream for CPS is derived from the finance charges applied to the auto loans it purchases and services. These charges reflect the interest paid by borrowers over the life of their loans. Additionally, CPS generates revenue from late fees and the sale of repossessed vehicles.

In the fiscal year ending December 31, 2023, CPS reported total revenues of approximately $264.4 million, with net interest income being a significant contributor. This demonstrates the company's reliance on interest income from its portfolio of CPS loans.

Key Revenue Streams and Monetization Strategies

CPS strategically employs a risk-based pricing model to generate revenue. This approach involves assessing the credit risk of each borrower and adjusting loan terms accordingly. This allows CPS to manage the higher risk associated with subprime auto loans effectively. The company also focuses on efficient loan servicing and effective collection strategies to maximize revenue and minimize losses.

- Finance Charges: These are the primary source of revenue, representing interest paid by borrowers on CPS loans.

- Late Fees: Assessed when borrowers fail to make timely payments, contributing to overall income.

- Sale of Repossessed Vehicles: Revenue generated from selling vehicles that have been repossessed due to loan defaults, helping to mitigate losses.

- Risk-Based Pricing: CPS uses this strategy to price loans according to the borrower's credit risk, ensuring that expected returns compensate for the increased risk of default, which is a common aspect of subprime auto loans.

- Effective Loan Servicing: Efficient management of loan portfolios, including collection strategies, to maximize revenue and minimize losses.

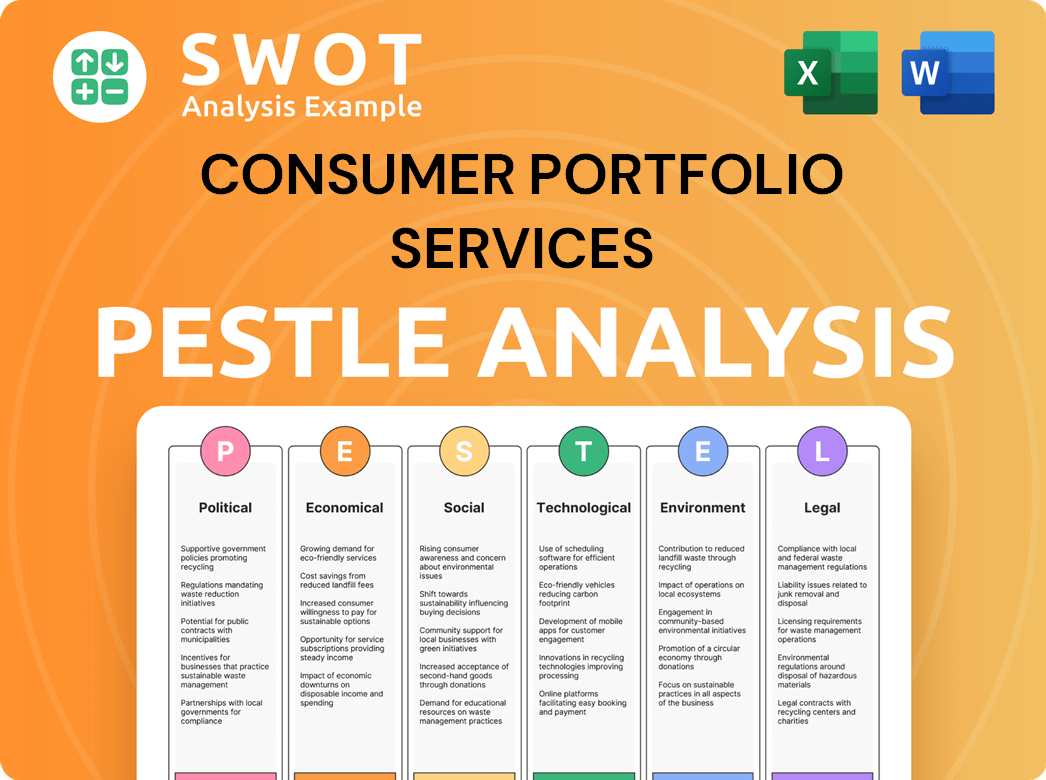

Consumer Portfolio Services PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Consumer Portfolio Services’s Business Model?

Consumer Portfolio Services (CPS) has established itself as a key player in the subprime auto lending market. Its operational strategy revolves around indirect lending, heavily relying on relationships with thousands of auto dealers across the United States. This dealer network serves as the primary source for loan originations, allowing CPS to reach a wide customer base and scale its operations effectively. The company's focus remains on purchasing and servicing auto loans, continuously refining its credit underwriting models and loan servicing technologies.

The company's strategic adjustments are often driven by economic cycles and shifts in consumer credit behavior. For example, rising interest rates can increase funding costs and impact borrowers' ability to repay loans, potentially leading to higher delinquency rates. CPS responds by adjusting underwriting criteria, refining collection strategies, and managing funding costs through securitization and credit facilities. These proactive measures are crucial for maintaining portfolio performance.

CPS's competitive edge stems from its specialized expertise in subprime credit risk assessment and management. Unlike traditional lenders, CPS has the infrastructure and analytical capabilities to accurately evaluate and service loans for borrowers with less-than-perfect credit. This niche focus, combined with its extensive dealer network, creates a barrier to entry for new competitors. Furthermore, its experience in securitizing auto loan receivables provides access to capital markets, enabling it to fund its loan originations. The company continuously adapts to new trends by monitoring credit quality metrics and adjusting its lending parameters to reflect current market conditions and regulatory changes, ensuring the sustainability of its business model.

CPS has consistently focused on indirect lending through its extensive network of auto dealers. This approach has been a cornerstone of its growth, enabling the company to reach a broad customer base. The company has refined its credit underwriting models and loan servicing technologies to manage risk effectively.

CPS adapts to economic challenges by adjusting underwriting criteria and refining collection strategies. This includes managing funding costs through securitization and credit facilities. The company's ability to adapt to macroeconomic shifts is critical for maintaining portfolio performance.

CPS specializes in subprime credit risk assessment and management, setting it apart from traditional lenders. Its extensive dealer network and experience in securitizing auto loan receivables are significant advantages. The company continuously monitors credit quality and adjusts lending parameters to stay competitive.

CPS monitors credit quality metrics and adjusts lending parameters to reflect current market conditions and regulatory changes. This ensures the sustainability of its business model. The company's ability to adapt to changes in the target market of Consumer Portfolio Services is crucial.

Key Operational Data and Metrics

CPS's success is closely tied to its ability to manage risk and adapt to market changes. The company's performance is influenced by factors such as interest rates, credit scores, and economic conditions. Understanding these elements is essential for evaluating CPS's financial health.

- Dealer Network: CPS maintains relationships with thousands of auto dealers, providing a steady stream of loan originations.

- Credit Underwriting: The company uses sophisticated models to assess the creditworthiness of borrowers.

- Loan Servicing: CPS manages its loan portfolio, including collections and customer service.

- Securitization: CPS securitizes auto loan receivables to access capital markets and fund its operations.

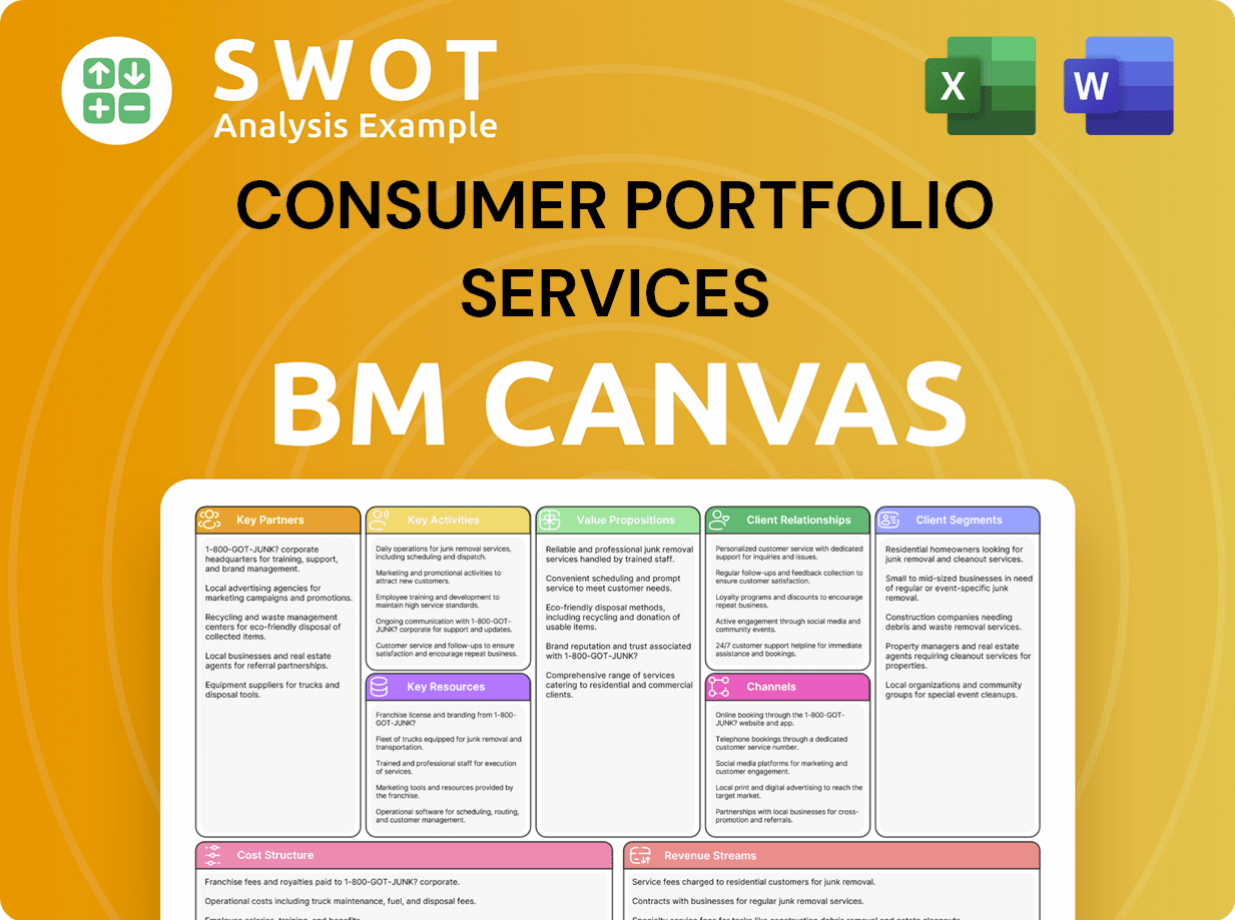

Consumer Portfolio Services Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Consumer Portfolio Services Positioning Itself for Continued Success?

Within the subprime auto finance sector, Consumer Portfolio Services (CPS) holds a significant position. CPS specializes in offering CPS loans, distinguishing itself from mainstream auto lenders. Its business model hinges on collaborations with dealerships nationwide, focusing on CPS auto financing for individuals with less-than-perfect credit histories. The company's market share is primarily within the subprime segment, where it competes with other specialized lenders.

The company faces several key risks, including fluctuations in interest rates, economic downturns, and regulatory changes. Rising interest rates can increase the cost of funds, impacting profitability, and economic downturns can lead to higher default rates on CPS loans. Regulatory changes and the emergence of fintech competitors also pose challenges. Despite these risks, CPS aims to maintain its market position by optimizing its lending practices and managing its loan portfolio effectively. Read more about the Owners & Shareholders of Consumer Portfolio Services.

Consumer Portfolio Services is a prominent player in the subprime auto lending market. It carves out a niche by offering CPS auto financing to borrowers who may not qualify for prime loans. The company's strategy involves partnerships with auto dealerships to reach its target demographic.

Interest rate changes and economic downturns are significant risks for CPS loans. Higher interest rates can increase borrowing costs, while economic downturns can lead to increased defaults. Regulatory changes and competition from fintech companies also pose challenges.

The company's future depends on its ability to adapt to market changes and manage risks. Consumer Portfolio Services will likely continue to focus on prudent risk management and optimizing its lending practices. The company's performance is closely tied to the health of the subprime auto market.

Consumer Portfolio Services likely focuses on optimizing its credit models and loan servicing. Maintaining strong dealer relationships and efficient access to capital markets are also crucial. The company aims to identify and underwrite creditworthy subprime borrowers.

Factors Influencing Consumer Portfolio Services

Several factors influence the performance of Consumer Portfolio Services, including interest rate fluctuations, economic conditions, and regulatory changes. The company's ability to manage its loan portfolio and adapt to market dynamics is crucial. The subprime auto loan market is subject to volatility, and CPS auto financing is affected by these broader trends.

- Interest Rate Sensitivity: Changes in interest rates directly impact the cost of funds and loan affordability.

- Economic Cycles: Economic downturns increase the risk of loan defaults.

- Regulatory Environment: Compliance with lending regulations affects operational costs and practices.

- Competitive Landscape: Competition from other subprime lenders and fintech companies.

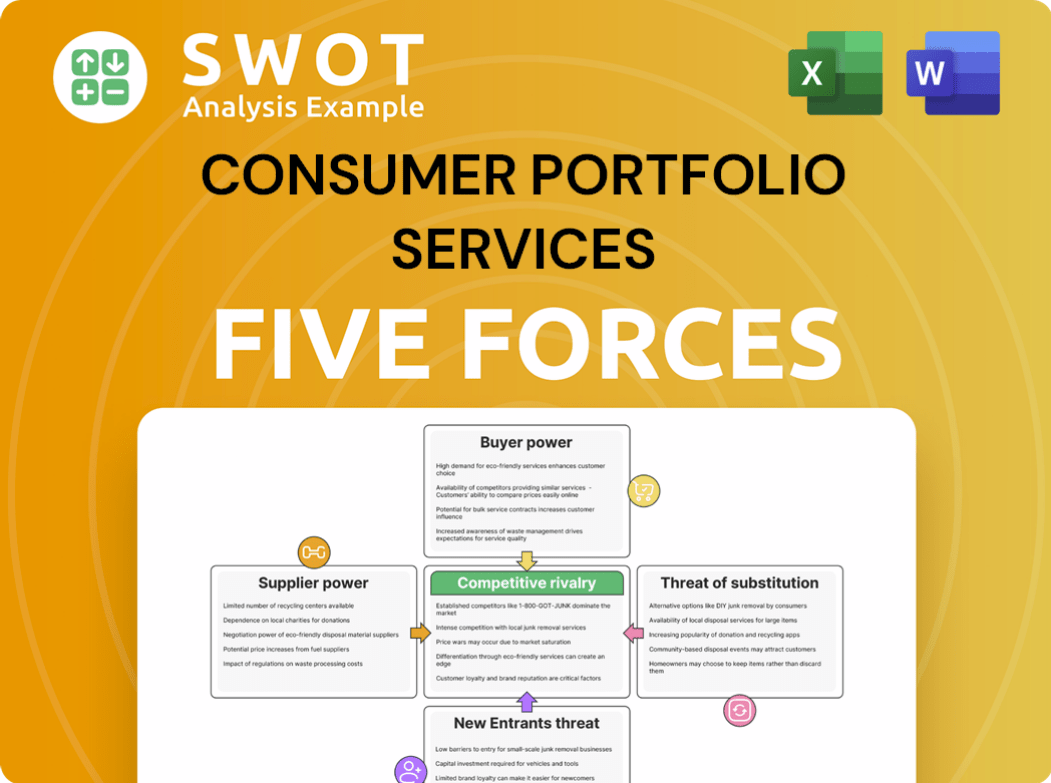

Consumer Portfolio Services Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Consumer Portfolio Services Company?

- What is Competitive Landscape of Consumer Portfolio Services Company?

- What is Growth Strategy and Future Prospects of Consumer Portfolio Services Company?

- What is Sales and Marketing Strategy of Consumer Portfolio Services Company?

- What is Brief History of Consumer Portfolio Services Company?

- Who Owns Consumer Portfolio Services Company?

- What is Customer Demographics and Target Market of Consumer Portfolio Services Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.