Consumer Portfolio Services Bundle

Can Consumer Portfolio Services Thrive in the Evolving Auto Finance Landscape?

The subprime auto lending sector is a dynamic arena, presenting both hurdles and opportunities for companies like Consumer Portfolio Services (CPS). Understanding a company's Consumer Portfolio Services SWOT Analysis is crucial to grasping its ability to adapt and expand. This analysis explores CPS's journey from its inception in 1991 to its current market position, highlighting its unique approach to serving the underserved market.

This in-depth market analysis will examine the growth strategy of Consumer Portfolio Services, delving into its future prospects within the competitive financial services industry. We'll explore how CPS plans to navigate the complexities of subprime auto loans, focusing on its expansion plans, technological advancements, and financial strategies. Furthermore, we will assess the potential impact of economic factors and other challenges on CPS's trajectory, providing a comprehensive outlook on its investment potential.

How Is Consumer Portfolio Services Expanding Its Reach?

The Growth strategy of Consumer Portfolio Services (CPS) centers on expanding its reach and enhancing its offerings within the subprime auto lending market. CPS aims to strengthen its market position by focusing on several key initiatives. These include deepening its presence in existing markets and exploring opportunities to diversify its product offerings.

CPS's approach involves a strategic focus on both organic growth and potential acquisitions. The company is actively working to optimize its dealer relationships and operational efficiency. These efforts are crucial for supporting increased loan originations and maintaining credit quality, especially considering economic uncertainties.

Understanding the Future prospects of CPS requires an examination of its expansion plans and market dynamics. CPS is navigating the subprime auto loan sector with a focus on sustainable growth and strategic diversification. This approach is designed to enhance its long-term value and competitiveness.

CPS concentrates on expanding within its current operational states. This strategy leverages existing infrastructure and regulatory knowledge. The company is focused on increasing its network of franchise and independent auto dealers.

CPS explores offering related financial products, such as vehicle service contracts. These products are offered through its dealer network. This diversification aims to increase revenue per customer and enhance customer retention.

CPS continuously evaluates potential mergers and acquisitions within the specialty finance space. These opportunities must align with its core competencies and strategic objectives. This approach helps CPS access new customer segments and diversify revenue streams.

CPS focuses on optimizing its dealer relationships to support increased loan originations. Enhancing operational efficiency is another key area of focus. These efforts help maintain credit quality amidst economic fluctuations.

The company's ability to adapt to changing market conditions is critical for its long-term success. For a deeper dive into how CPS approaches its marketing efforts, consider reading about the Marketing Strategy of Consumer Portfolio Services.

Key Expansion Initiatives

CPS's expansion strategy is multifaceted, involving geographical growth, product diversification, and strategic acquisitions. These initiatives are designed to enhance its market position and revenue streams. The company is focused on sustainable growth and adapting to industry changes.

- Deepening market penetration within existing geographical areas.

- Expanding product offerings to include related financial products.

- Evaluating potential mergers and acquisitions in the specialty finance sector.

- Optimizing dealer relationships and operational efficiency.

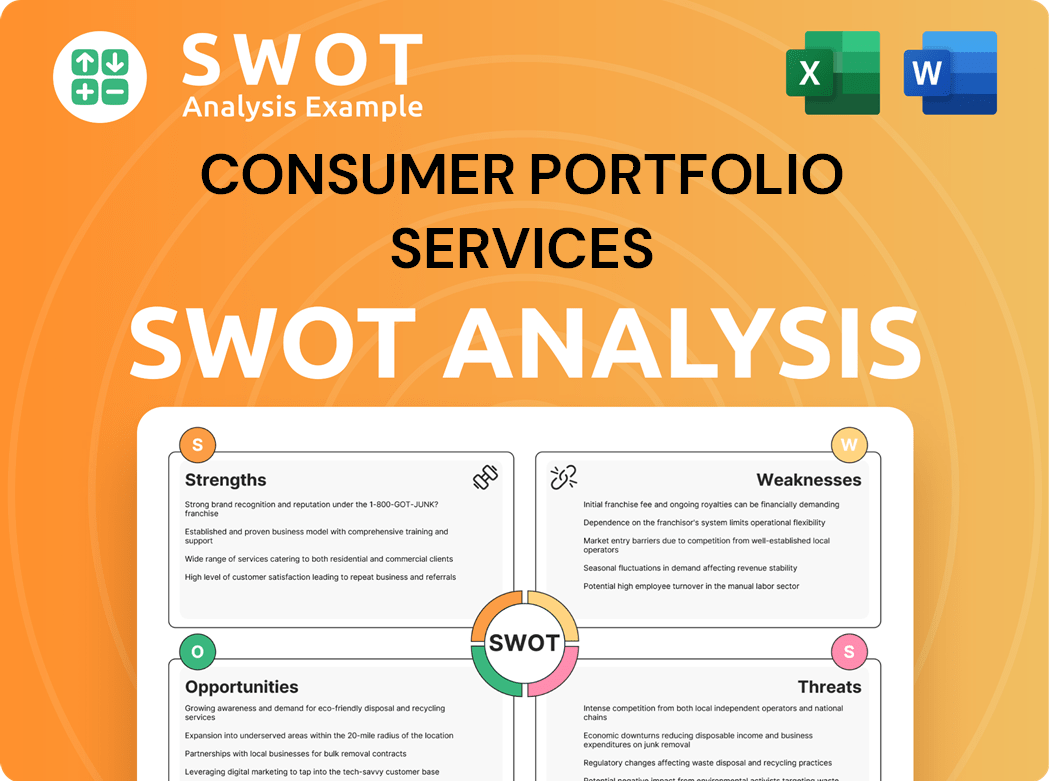

Consumer Portfolio Services SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Consumer Portfolio Services Invest in Innovation?

Consumer Portfolio Services (CPS) is strategically leveraging technology and innovation to foster sustainable growth, particularly within the subprime auto lending sector. Their approach to digital transformation focuses on streamlining both loan origination and servicing, aiming to enhance the experiences for both customers and dealerships. This commitment includes continuous investments in their proprietary loan management systems and the integration of advanced data analytics capabilities.

By enhancing its data infrastructure, CPS aims to refine its credit scoring models, enabling more precise risk assessment and potentially expanding its lending criteria while maintaining portfolio quality. This focus on technological advancement is crucial for navigating the dynamic landscape of the financial services industry and ensuring long-term viability. The company's ability to adapt and integrate new technologies directly impacts its competitive edge and operational efficiency.

The company's growth strategy is heavily influenced by its ability to adapt to technological advancements. This is particularly important in the subprime auto loans market, where data-driven decisions and efficient operations are critical. CPS's commitment to technological innovation is a key factor in its ability to compete and grow.

Data Analytics and Credit Scoring

CPS is enhancing its data infrastructure to refine credit scoring models. This allows for more precise risk assessment. Improved models could lead to expanded lending criteria while preserving portfolio quality.

Operational Automation

CPS focuses on in-house automation, particularly in back-office operations. This includes payment processing and customer service interactions. Automation aims to improve efficiency and reduce operational costs.

AI and ML Integration

The company is exploring the use of AI and ML technologies. These technologies are being considered to optimize underwriting decisions. They are also used to identify fraud and personalize customer communications.

Focus on Core Business

CPS prioritizes technological applications that directly support its core business. The core business is purchasing and servicing auto loans. This focus ensures that technology investments align with strategic objectives.

Competitive Advantage

Continuous efforts to enhance the technological infrastructure contribute to the company's growth objectives. These efforts improve operational scalability and reduce costs. This enhances the competitive edge in a data-driven industry.

Digital Transformation Strategy

CPS's digital transformation strategy focuses on streamlining loan origination and servicing processes. This improves the customer and dealer experience. These improvements are essential for maintaining market competitiveness.

The company's approach is not just about adopting new technologies but integrating them strategically to support its core business model. This approach, combined with a focus on data-driven decision-making, positions CPS to navigate the challenges and opportunities within the subprime auto loan market. Further insights into the company's mission and values can be found in this article: Mission, Vision & Core Values of Consumer Portfolio Services.

Technological Investments and Future Prospects

The future prospects for CPS are closely tied to its ability to leverage technology effectively. Continued investment in data analytics, automation, and AI/ML capabilities is crucial for maintaining its competitive edge and achieving sustainable growth. While specific financial figures for 2024 and 2025 are not yet available, the company's strategic focus on technology suggests a commitment to long-term value creation.

- Enhancements in data analytics will likely improve risk assessment.

- Automation in back-office operations will likely reduce operational costs.

- The strategic use of AI and ML could lead to better underwriting decisions.

- These advancements will help CPS to adapt to market changes.

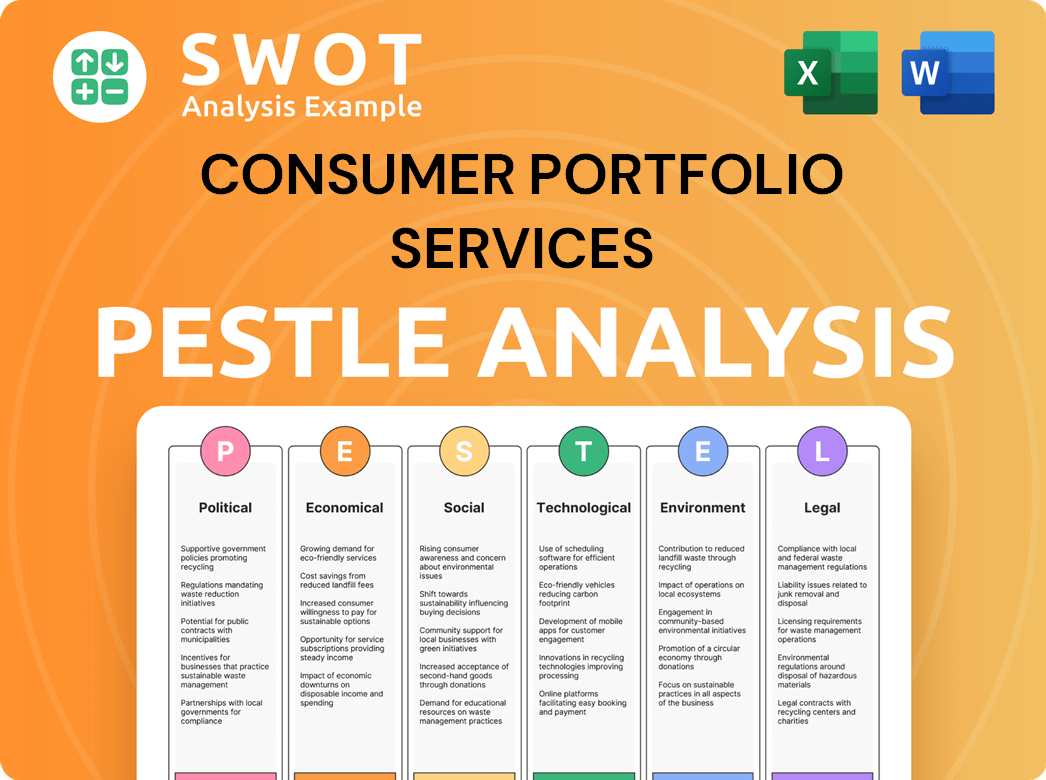

Consumer Portfolio Services PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Consumer Portfolio Services’s Growth Forecast?

The financial outlook for Consumer Portfolio Services (CPS) is significantly influenced by the subprime auto lending market's performance. The company's ability to manage credit risk and operational efficiency directly impacts its revenue and profit margins. Key factors such as interest rate fluctuations, credit losses, and loan origination volume play crucial roles in shaping its financial results.

Recent financial reports indicate a dynamic economic environment for CPS. For the fiscal year ending December 31, 2024, the company reported a net income of $1.1 million. This is a considerable decrease from the $66.1 million reported the previous year. This decline was primarily due to increased provisions for credit losses and higher interest expenses. Total revenue for the same period was $327.3 million, down from $376.1 million in 2023.

Looking ahead, analysts and company guidance emphasize the importance of maintaining strong asset quality and managing delinquency rates. These factors are crucial for ensuring profitability. CPS's long-term financial goals likely involve sustainable loan portfolio growth while optimizing its cost of funds and operational expenses. Access to capital markets for securitization and other funding avenues is essential for supporting loan origination volumes. In 2024, CPS completed several securitizations, including a $250 million transaction in March, which supported new loan originations. The financial strategy centers on prudent risk management and disciplined growth, aiming for consistent returns in a specialized market segment.

CPS's revenue for 2024 was $327.3 million, a decrease from $376.1 million in 2023. Net income for 2024 was $1.1 million, significantly lower than the $66.1 million reported in the prior year. These figures highlight the impact of increased credit loss provisions and higher interest expenses on profitability.

The company relies on securitization to fund its loan originations. In March 2024, CPS completed a $250 million securitization transaction. This funding mechanism is crucial for supporting the continued growth of the loan portfolio. The ability to secure funding is vital for the growth strategy.

Managing credit risk is a critical aspect of CPS's financial performance. The increase in provisions for credit losses in 2024 indicates the challenges in the subprime auto lending market. Effective risk management strategies are essential to mitigate potential losses.

The future prospects of CPS are closely tied to the overall health of the subprime auto loan market. Factors such as interest rates, economic conditions, and consumer credit behavior significantly influence the company's financial outcomes. Understanding these dynamics is key to assessing Consumer Portfolio Services's long-term potential.

Key Financial Metrics

The financial performance of CPS is closely monitored through several key metrics. These metrics provide insights into the company's operational efficiency, credit quality, and overall financial health. Understanding these metrics is crucial for evaluating the Consumer Portfolio Services company growth strategy.

- Net Income: $1.1 million (2024), $66.1 million (2023)

- Total Revenue: $327.3 million (2024), $376.1 million (2023)

- Securitization: $250 million transaction (March 2024)

- Interest Expense: Increased in 2024

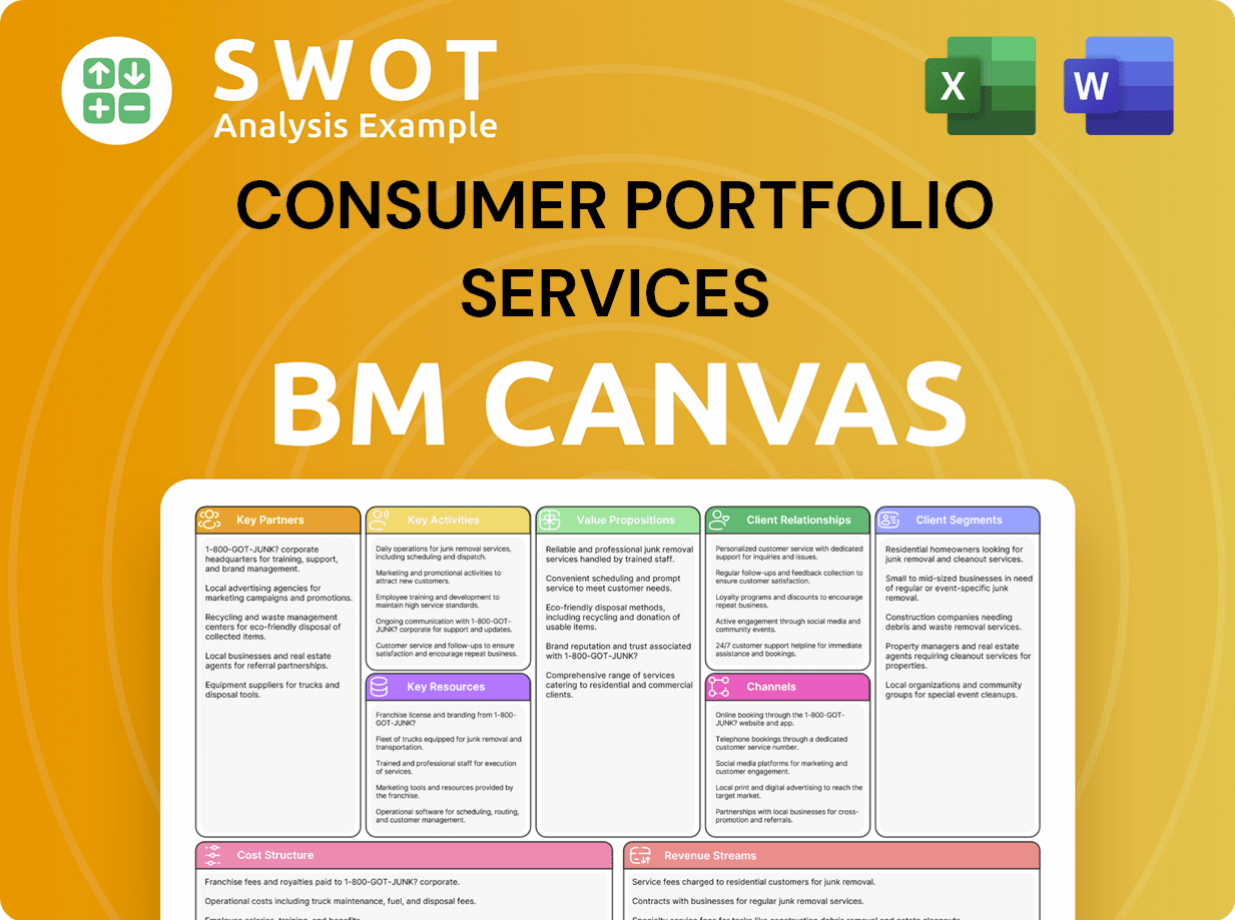

Consumer Portfolio Services Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Consumer Portfolio Services’s Growth?

The subprime auto lending sector presents several potential risks and obstacles for companies like Consumer Portfolio Services (CPS) as they pursue their growth strategy. The competitive landscape, regulatory changes, and technological advancements all pose significant challenges. Understanding and proactively addressing these factors is crucial for navigating the future prospects of the company.

Market competition remains a primary concern, with numerous financial services providers vying for market share in the subprime auto loans segment. Regulatory scrutiny, especially from bodies like the Consumer Financial Protection Bureau (CFPB), can lead to increased compliance costs and operational adjustments. Additionally, the company must contend with supply chain vulnerabilities and internal resource limitations.

Technological disruption and cybersecurity threats also present risks that could impact the company's performance. To mitigate these challenges, CPS employs robust risk management frameworks, including sophisticated credit underwriting models and diversified funding sources. The ability to adapt to economic downturns and fluctuating interest rates will be key to the company's long-term success.

Market Competition

The subprime auto loan market is highly competitive, with both established and new players vying for market share. This can lead to price wars and reduced profit margins. Companies must differentiate themselves through superior service, technology, or niche offerings to succeed in this environment.

Regulatory Changes

The subprime auto lending industry is subject to evolving consumer protection laws and financial regulations. Increased scrutiny from agencies such as the CFPB can lead to higher compliance costs and potential restrictions on lending practices. Staying ahead of these changes is critical.

Supply Chain Vulnerabilities

Disruptions in the automotive supply chain can indirectly affect the demand for auto loans. Vehicle availability and pricing fluctuations can impact loan volumes and profitability. Monitoring these trends and adapting to market changes is essential.

Technological Disruption

Failing to keep pace with advancements in credit scoring, digital lending platforms, and cybersecurity can lead to competitive disadvantages. Investing in technology and data analytics is crucial for maintaining a competitive edge and mitigating risks. The Target Market of Consumer Portfolio Services article provides additional insights.

Internal Resource Constraints

The availability of skilled personnel for underwriting and servicing can present ongoing management challenges. Attracting and retaining qualified staff is essential for maintaining operational efficiency and managing credit risk. Continuous training and development are vital.

Economic Downturns and Interest Rates

Fluctuating interest rates and economic downturns can significantly impact the subprime auto loan market. Elevated credit losses and decreased loan demand are common during these periods. Scenario planning and flexible underwriting criteria are crucial for managing these risks.

Elevated credit losses are a continuous concern, requiring constant adjustments to underwriting criteria. Enhancing collection strategies and closely monitoring loan performance are essential. In 2024, the industry saw a slight increase in charge-off rates, emphasizing the need for proactive risk management.

Data breaches and cyberattacks pose a significant risk to financial institutions. Investing in robust cybersecurity measures and data protection protocols is essential. The cost of data breaches in the financial sector has increased by approximately 15% in the last year.

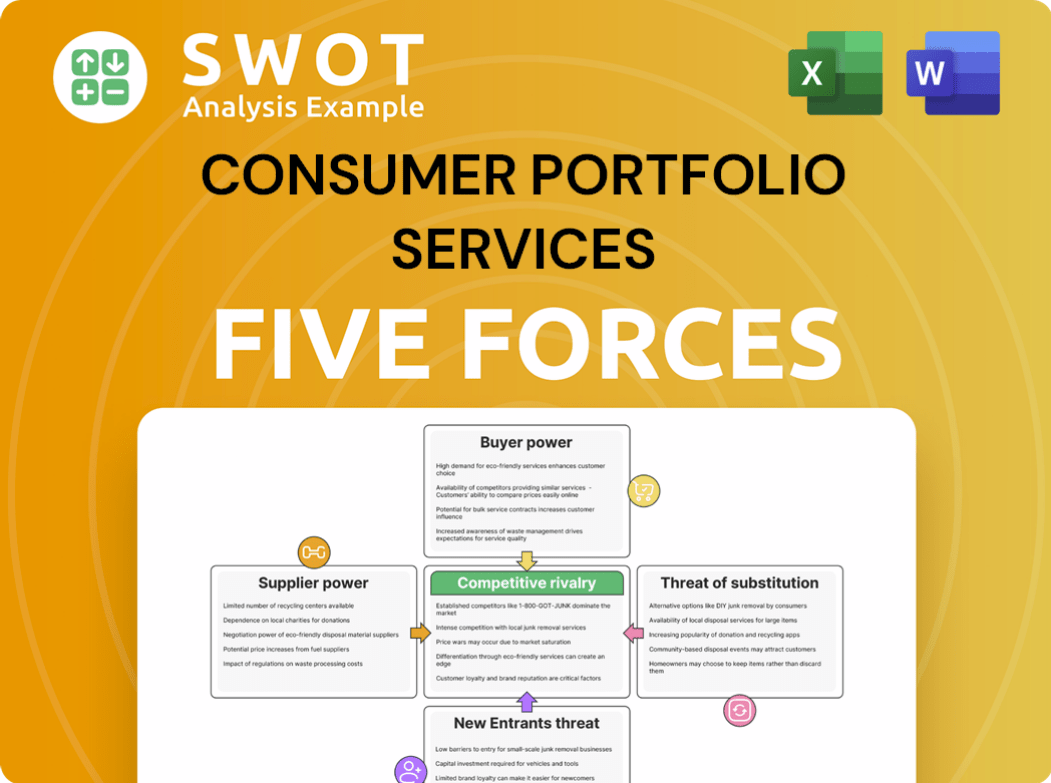

Consumer Portfolio Services Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Consumer Portfolio Services Company?

- What is Competitive Landscape of Consumer Portfolio Services Company?

- How Does Consumer Portfolio Services Company Work?

- What is Sales and Marketing Strategy of Consumer Portfolio Services Company?

- What is Brief History of Consumer Portfolio Services Company?

- Who Owns Consumer Portfolio Services Company?

- What is Customer Demographics and Target Market of Consumer Portfolio Services Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.