S&U Bundle

Can S&U Company Continue Its Impressive Growth Trajectory?

In the dynamic world of specialist lending, understanding a company's growth strategy is crucial for informed decision-making. S&U Company, a prominent player in the UK's financial sector, offers a compelling case study. This analysis delves into S&U's strategic planning and future prospects, exploring its evolution from its founding in 1938 to its current market position.

With a solid foundation built on a history of providing financial solutions, S&U Company's commitment to innovation and strategic planning is evident. To further understand its position, consider a detailed S&U SWOT Analysis. This exploration of S&U's growth strategy will examine its expansion plans and future growth opportunities, providing valuable insights for investors and business strategists alike, including a market analysis of its future prospects.

How Is S&U Expanding Its Reach?

The Growth strategy of S&U Company centers on strategic expansion initiatives primarily through its two core businesses: Advantage Finance and Aspen Bridging. These divisions are crucial for driving business development and enhancing the company's market presence. This approach is supported by robust financial management and a focus on organic growth within established markets. For a deeper understanding of the company's customer base, consider reading about the Target Market of S&U.

Advantage Finance, the motor finance division, focuses on the used car market, adapting to evolving consumer needs and regulatory changes. Aspen Bridging, on the other hand, specializes in short-term, secured bridging loans, a segment experiencing increasing demand. Both divisions leverage S&U's strong financial foundation to support their expansion efforts.

The company's strategic planning includes refining credit underwriting models and enhancing digital application processes. This is aimed at improving customer accessibility and operational efficiency. The commitment to maintaining a strong balance sheet and liquidity provides the necessary capital for these expansion plans.

Advantage Finance continues to focus on the used car market. The company aims to further penetrate this market by refining its credit underwriting models. They are also enhancing digital application processes to improve customer accessibility and efficiency.

Aspen Bridging is expanding within the property sector, focusing on short-term bridging loans. The company is exploring opportunities to broaden its product offerings. This could include more diverse property types or larger loan facilities.

As of January 31, 2024, motor finance receivables reached £320.1 million, indicating sustained activity. Aspen Bridging's loan book reached £60.9 million during the same period. These figures highlight the company's capacity for continued organic growth.

S&U Company's market analysis indicates a strong position in its core markets. The future prospects are positive, underpinned by its strategic focus on organic growth. The company leverages its expertise and customer relationships to secure future business.

Key Expansion Strategies

S&U's expansion strategies are focused on organic growth within its established markets. They are leveraging their expertise and strong customer relationships to secure future business. This approach includes refining credit models and enhancing digital platforms.

- Refining credit underwriting models to improve efficiency.

- Enhancing digital application processes for better customer access.

- Broadening product offerings within bridging finance.

- Focusing on organic growth within established markets.

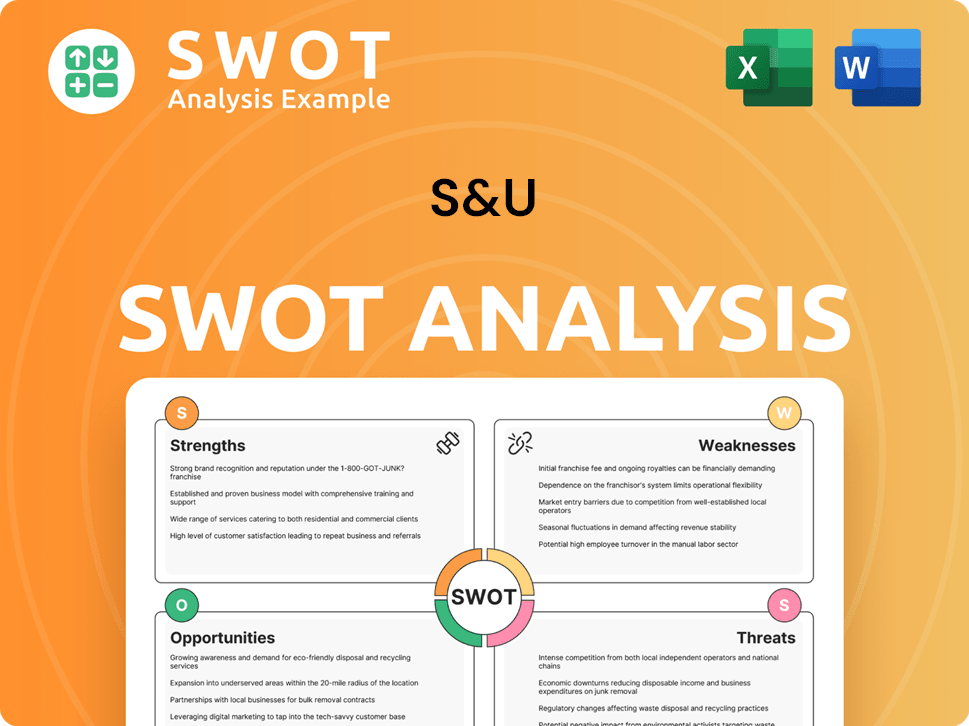

S&U SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does S&U Invest in Innovation?

The innovation and technology strategy of S&U Company is crucial for its sustained growth, especially in boosting operational efficiency and enhancing customer experience. The company consistently invests in digital transformation across its Advantage Finance and Aspen Bridging divisions. This strategic focus supports S&U's overall growth objectives by increasing its capacity to process more applications and manage a larger loan book efficiently.

S&U Company leverages technological advancements to streamline processes and improve service delivery. This includes the development of advanced online application portals and sophisticated credit assessment algorithms. These technological integrations are designed to reduce turnaround times and improve the overall customer journey, making financial services more accessible and user-friendly.

In the property bridging sector, Aspen Bridging utilizes technology to expedite due diligence and valuation processes. This is particularly important in the fast-paced nature of bridging loans. While specific details on R&D investments or patents are not publicly detailed, S&U's operational improvements demonstrate a clear commitment to technological integration and innovation.

Digital Transformation

S&U Company is actively engaged in digital transformation across its Advantage Finance and Aspen Bridging divisions. This involves the implementation of advanced online application portals and sophisticated credit assessment algorithms.

Operational Efficiency

The company's focus on digital solutions enhances internal efficiencies. This leads to reduced turnaround times and improved operational capabilities. These improvements are crucial for managing a larger loan book effectively.

Customer Experience

Technological advancements improve the customer journey, making financial services more accessible and user-friendly. This customer-centric approach supports the company's growth strategy.

Data Analytics

Advanced data analytics allows Advantage Finance to better assess credit risk and tailor financial products. This reduces defaults and improves portfolio quality, contributing to the Competitors Landscape of S&U.

Bridging Loans

In the property bridging sector, technology expedites due diligence and valuation processes. This is crucial for the fast-paced nature of bridging loans, supporting the company's expansion plans.

R&D and Patents

While specific details on R&D investments or patents are not publicly detailed, S&U's operational improvements demonstrate a commitment to technological integration and innovation, supporting the future prospects.

Key Technological Strategies

S&U Company's innovation strategy focuses on enhancing operational efficiency and improving customer experience through digital transformation. This strategy includes the development of advanced online portals and sophisticated credit assessment tools.

- Digital Application Portals: Streamline the lending process, reducing manual effort and processing times.

- Credit Assessment Algorithms: Improve risk assessment and tailor financial products to meet individual customer needs.

- Data Analytics: Enhance the ability to assess credit risk, reduce defaults, and improve portfolio quality.

- Automation: Automate processes such as due diligence and valuation in the bridging sector, increasing efficiency.

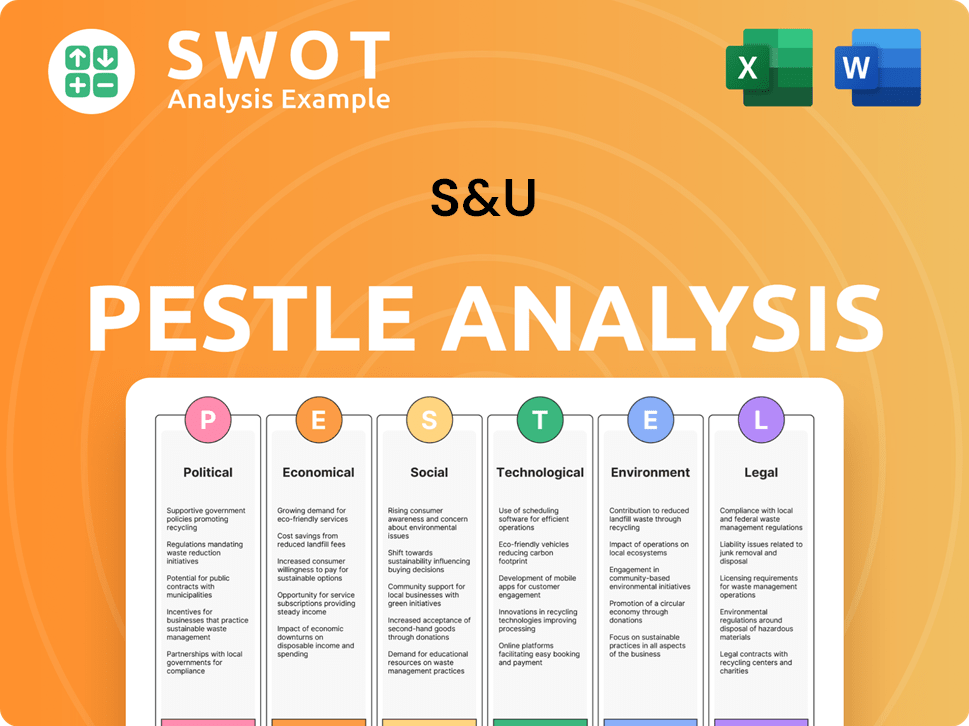

S&U PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is S&U’s Growth Forecast?

The financial outlook for S&U Company (S&U) appears promising, supported by consistent profitability and strategic capital management. The company's financial health is a key factor in its growth strategy and future plans. The focus on maintaining a strong balance sheet is crucial for funding future initiatives.

For the financial year ending January 31, 2024, S&U reported a pre-tax profit of £39.8 million. While this was slightly down from the previous year's £40.7 million, it still demonstrates resilience in a fluctuating market. This financial stability is a cornerstone for business development and expansion. The net asset value is robust at £200 million, which supports its lending activities.

The company's financial strategy emphasizes maintaining a healthy balance sheet and strong liquidity, which enables it to fund future growth organically and through potential strategic acquisitions. The company's dividend policy also reflects its financial stability, with a proposed final dividend of 28p per share for 2024, bringing the total dividend to 56p per share. S&U's financial performance is a key indicator of its potential. Analyst forecasts and company guidance suggest a continued focus on sustainable growth, driven by disciplined lending practices and effective risk management. The company’s ability to generate significant cash flow from operations further strengthens its capacity for reinvestment and expansion without excessive reliance on external financing.

S&U's motor finance arm, Advantage Finance, generated £320.1 million in receivables, showing strong performance in its lending operations. The company's ability to manage and grow its loan portfolio is a key aspect of its financial strategy.

Aspen Bridging's loan book grew to £60.9 million, indicating expansion in its bridging finance segment. This growth contributes to the overall market analysis of S&U's diversified financial services.

The proposed final dividend of 28p per share for 2024, bringing the total dividend to 56p per share, reflects the company's commitment to shareholder returns. This is a key indicator of financial health.

Analyst forecasts suggest a continued focus on sustainable growth, driven by disciplined lending practices and effective risk management. This outlook supports the future prospects of S&U.

Strategic Initiatives

S&U's financial strategy includes several key elements that support its long-term vision. These initiatives are crucial for its strategic planning and overall success.

- Maintaining a healthy balance sheet.

- Focusing on strong liquidity.

- Funding future growth organically.

- Considering strategic acquisitions.

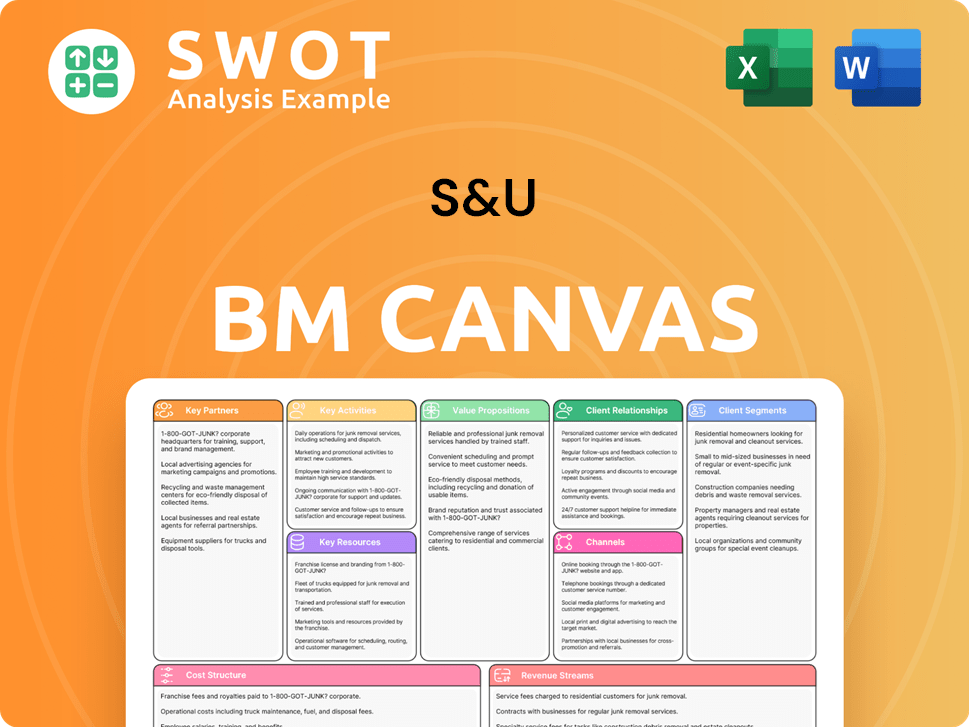

S&U Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow S&U’s Growth?

The S&U Company faces potential risks and obstacles that could impact its growth strategy and future prospects. These challenges primarily stem from market dynamics, regulatory changes, and broader economic conditions. Understanding these risks is crucial for informed decision-making and effective strategic planning.

In the motor finance and property bridging sectors, the company operates within competitive landscapes. The company's success hinges on its ability to navigate these challenges effectively. Robust risk management and a strong financial position are essential to mitigate potential adverse impacts and ensure sustained business development.

The motor finance sector, where S&U Company operates, is intensely competitive. Specialist lenders and mainstream banks compete for market share, potentially compressing profit margins. Economic downturns, marked by rising interest rates and inflation, could reduce consumer affordability, increasing loan default rates. This directly impacts profitability, requiring proactive measures to manage credit risk and maintain financial stability. For instance, in 2024, the average interest rate on new car loans in the UK was around 6.5%, reflecting the impact of economic conditions on the sector.

Market Competition

Intense competition from other specialist lenders and mainstream banks. This could compress margins and limit market share growth.

Economic Downturns

Rising interest rates and inflation could impact consumer affordability. Also, it may increase default rates on loans, directly affecting profitability.

Property Market Fluctuations

Fluctuations in the housing market and changes in property values can affect the security of loans. This could impact the property bridging market.

Regulatory Changes

New legislation or stricter enforcement by bodies like the Financial Conduct Authority (FCA) could necessitate operational adjustments. It can also increase compliance costs or restrict lending practices.

Credit Regulations

Changes in consumer credit regulations could impact the business model. This may require adjustments to lending practices.

Risk Management

The company mitigates these risks through robust internal risk management frameworks. It includes diversified lending portfolios and stringent credit underwriting standards.

The property bridging market is susceptible to fluctuations in the housing market and property values, potentially affecting loan security. Regulatory changes in the UK's financial services industry pose another significant risk. New legislation or stricter enforcement by the Financial Conduct Authority (FCA) could necessitate operational adjustments and increase compliance costs. For example, changes in consumer credit regulations could impact the business model. S&U Company addresses these risks through robust internal risk management frameworks, including diversified lending portfolios and stringent credit underwriting standards. The company's strong capital position provides a buffer against unexpected economic shocks. For more details on the company's revenue streams and business model, see: Revenue Streams & Business Model of S&U.

Diversified lending portfolios to spread risk across different sectors. Stringent credit underwriting standards to minimize loan defaults. Continuous monitoring of market and regulatory landscapes for proactive adaptation.

A strong capital position provides a buffer against economic shocks. This allows the company to absorb potential losses and maintain operational continuity. This is crucial for long-term S&U Company's future prospects.

The motor finance sector faces intense competition from specialist lenders and mainstream banks. This could compress margins and limit market share growth. Market analysis is essential.

Economic downturns, characterized by rising interest rates and inflation, could impact consumer affordability. This will increase default rates, directly affecting profitability. In 2024, the UK's inflation rate was around 4%.

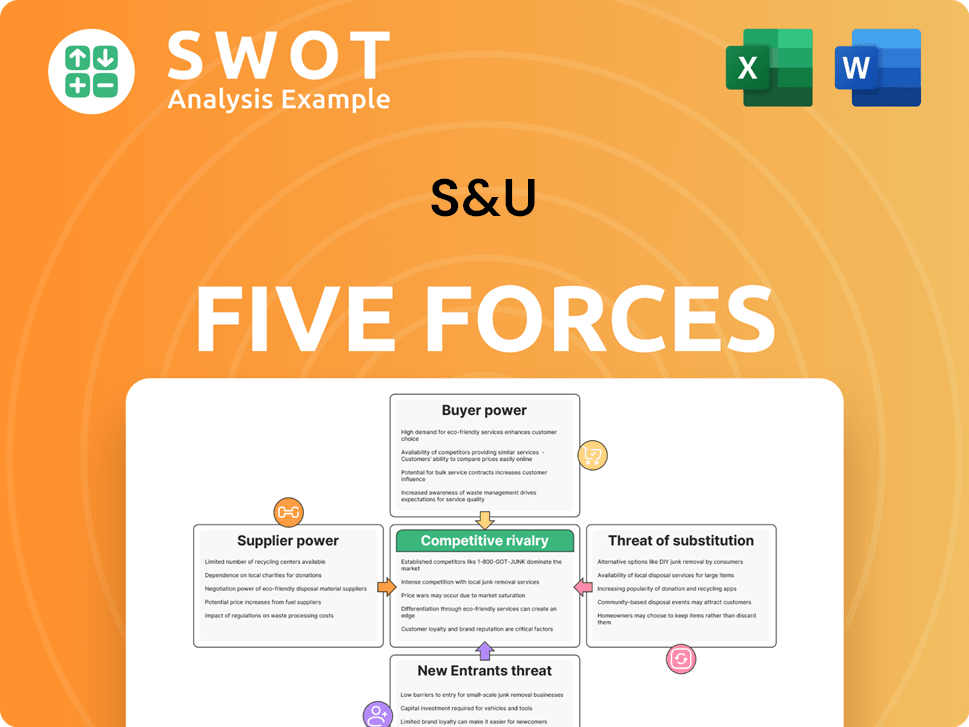

S&U Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.