S&U Bundle

How Does S&U Company Navigate the UK Lending Arena?

The UK specialist lending market is a battlefield of innovation and adaptation, and S&U PLC has been a key player since 1938. From its humble beginnings as a clothing retailer, S&U has strategically transformed, showcasing remarkable resilience in the face of evolving consumer needs and technological advancements. This journey highlights the company's ability to identify and capitalize on emerging opportunities within the financial services sector.

To truly understand S&U's position, we must delve into its S&U SWOT Analysis and the broader competitive landscape. This comprehensive market analysis will reveal key rivals, distinct competitive advantages, and the strategies S&U employs to navigate industry trends. Examining the competitive landscape analysis of S&U Company is crucial for any investor or strategist seeking to understand the dynamics of the UK lending market, including its market share and future growth opportunities.

Where Does S&U’ Stand in the Current Market?

S&U PLC carves out a specialized market position within the UK's non-prime motor finance and property bridging sectors. The company's core operations are divided between Advantage Finance, which offers hire purchase finance for used cars, and Aspen Bridging, which provides short-term secured loans for property transactions. This dual focus allows S&U to cater to distinct customer segments, providing financial solutions to those who may not qualify for mainstream lending and property professionals requiring quick funding.

The value proposition of S&U lies in its ability to serve niche markets effectively. Advantage Finance provides accessible finance options for used car purchases, while Aspen Bridging offers flexible, short-term funding for property projects. This specialization enables S&U to develop expertise in underwriting and risk management tailored to these specific segments, differentiating it from larger, more generalized lenders. The company's focus on these niches allows it to maintain a strong position where it has developed significant expertise and a loyal customer base.

In the latest financial update for the year ended January 31, 2024, S&U reported a pre-tax profit of £35.6 million, with Advantage Finance playing a key role. This financial performance underscores the company's robust market position. The Growth Strategy of S&U has been instrumental in its success.

Advantage Finance focuses on providing hire purchase finance for used cars. It caters to customers who may not meet the criteria of mainstream lenders. The division's loan book indicates substantial activity in the non-prime motor finance segment, driving significant contributions to S&U's overall profitability.

Aspen Bridging provides short-term, secured loans for property transactions. This segment focuses on property developers and investors needing quick funding. While smaller than motor finance, it offers diversification and taps into a different customer base, showing growth in its loan book.

S&U concentrates its operations within the United Kingdom. It leverages its established network and local market understanding. The company's customer segments are distinct, serving individuals seeking used car finance and property professionals needing short-term funding.

S&U has demonstrated an ability to adapt its positioning, moving away from broader retail credit to focus on these specialized lending niches. This strategic shift has allowed it to build expertise and tailored underwriting processes that differentiate it from larger, more generalized lenders. S&U's consistent profitability and loan book growth in both Advantage Finance and Aspen Bridging underscore its strong and resilient position in these targeted UK markets.

Competitive Advantages

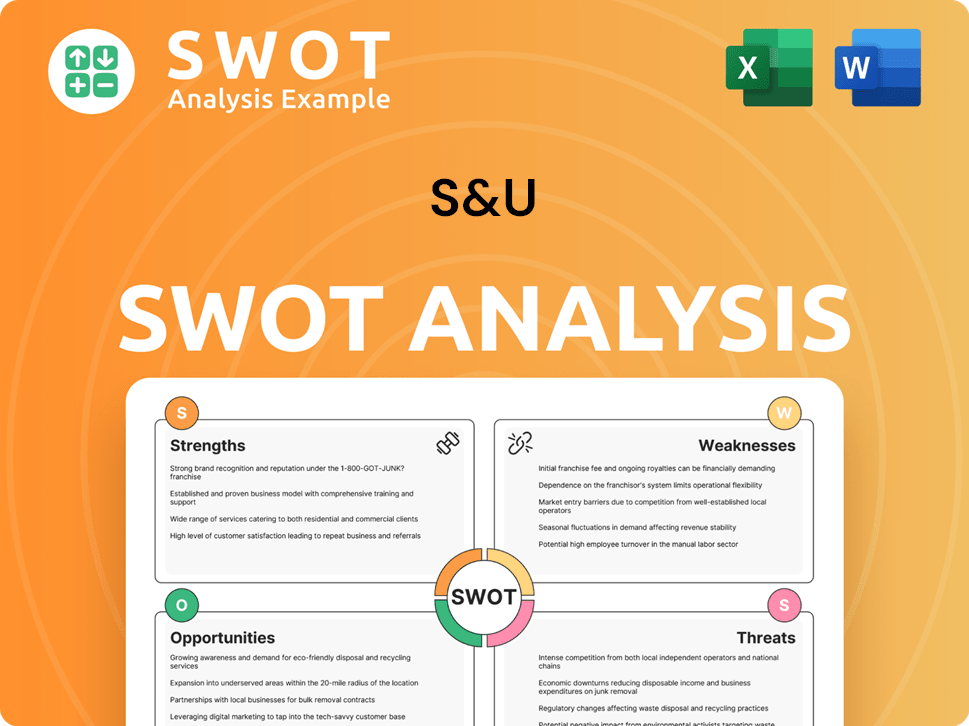

S&U's competitive advantages stem from its specialization in non-prime motor finance and property bridging. The company's tailored underwriting processes and deep understanding of these niche markets allow it to manage risk effectively and serve customers underserved by mainstream lenders. This focus enables S&U to maintain a strong market position.

- Specialized expertise in non-prime lending.

- Tailored underwriting processes.

- Strong relationships with customers and partners.

- Consistent financial performance.

S&U SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

Who Are the Main Competitors Challenging S&U?

The Owners & Shareholders of S&U face a dynamic competitive landscape across its primary business segments: motor finance and property bridging. A thorough market analysis reveals the key players and strategies shaping the industry. Understanding the competitive landscape is crucial for developing effective business strategies and maintaining a competitive advantage.

In the non-prime motor finance sector, S&U PLC competes with a mix of specialist lenders and challenger banks. The property bridging loan market also presents a complex competitive environment, with numerous specialist lenders and private funds vying for market share. This industry analysis provides insights into the key competitors and the strategies they employ.

The competitive landscape analysis for S&U Company involves examining its key competitors and their respective market positions. This includes assessing their strengths, weaknesses, opportunities, and threats (SWOT analysis) to understand their competitive strategies and market share. The following sections detail the key competitors in each of S&U's primary business segments.

Motor Finance Competitors

In the non-prime motor finance sector, S&U PLC competes with various specialist lenders and challenger banks. Key direct competitors include companies like Close Brothers Group PLC, particularly its motor finance division. These competitors challenge S&U through pricing, underwriting criteria, and dealer relationships.

Close Brothers Group PLC

Close Brothers Group PLC, a significant competitor, caters to a broad spectrum of credit profiles, including non-prime customers. They compete through their established dealer networks and competitive interest rates. In 2024, Close Brothers reported that its motor finance division saw a slight decrease in lending volumes, reflecting the overall market trends.

Provident Financial Group (Vanquis Banking Group)

Provident Financial Group (now Vanquis Banking Group) historically held a strong presence in the non-standard lending market. Although their focus has shifted, they remain a competitor. Vanquis Banking Group's 2024 financial reports show a strategic shift towards digital lending solutions.

Other Motor Finance Providers

Smaller, independent motor finance providers also present competition, often specializing in particular niches or geographic regions. These providers compete by offering specialized services and tailored financial products. The market share of these providers varies, with some experiencing growth in specific segments.

Competitive Strategies in Motor Finance

Competitors challenge S&U primarily through pricing strategies, flexible underwriting criteria, and dealer relationships. Some offer lower interest rates or more lenient terms. The competitive landscape is further influenced by technological advancements and the emergence of FinTech companies.

Market Dynamics

The motor finance market is influenced by economic conditions, regulatory changes, and consumer behavior. For instance, interest rate fluctuations and changes in credit availability directly impact the competitive environment. The Financial Conduct Authority (FCA) continues to play a significant role in regulating the sector.

Property Bridging Loan Competitors

In the property bridging loan market, S&U PLC faces competition from numerous specialist bridging lenders, private funds, and smaller banks. These competitors differentiate themselves through loan-to-value ratios, speed of execution, and flexibility in loan terms. The bridging finance market is highly competitive.

- United Trust Bank: Offers competitive bridging loans and is a significant player in the market. They focus on providing quick and efficient services.

- Shawbrook Bank: Another key competitor, Shawbrook Bank, provides a range of bridging finance options. They focus on a variety of property types and offer flexible terms.

- Tuscan Capital: A private bridging loan provider known for its specialized services and tailored financial solutions. They often focus on specific property asset classes.

- Octane Capital: Competes by offering innovative and technology-driven bridging loan products. They focus on speed and efficiency in their processes.

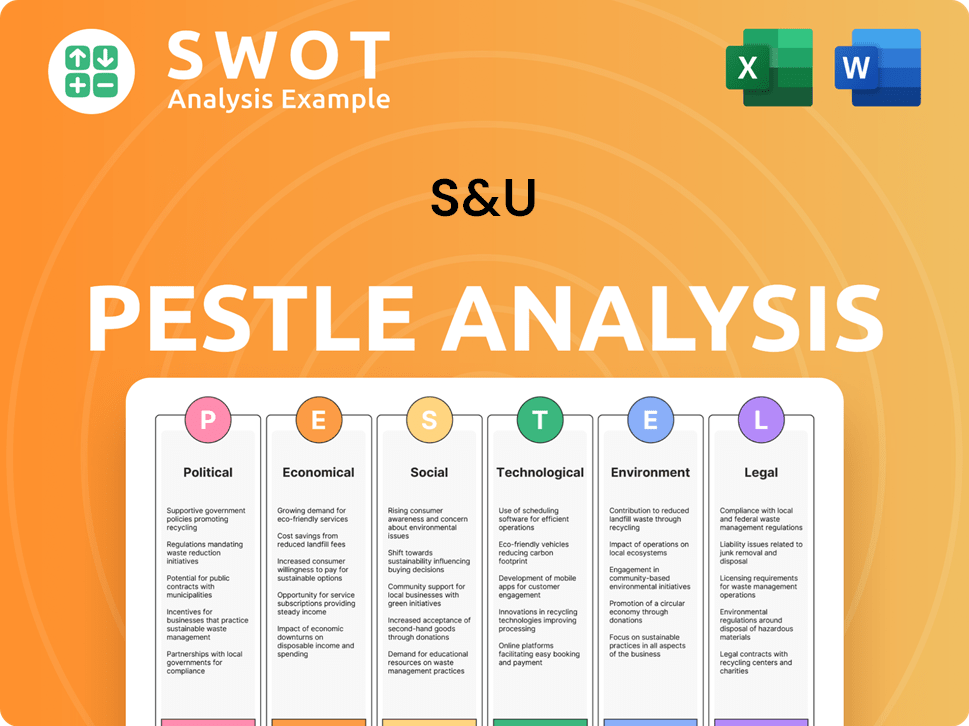

S&U PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Gives S&U a Competitive Edge Over Its Rivals?

The core competitive advantages of S&U PLC are rooted in its specialized focus, deep market expertise, and robust operational frameworks. The company has cultivated significant strengths in both motor finance and property bridging. This strategic focus allows S&U to develop and refine its capabilities, providing a strong foundation for sustained success in the competitive landscape.

A key advantage for Advantage Finance lies in its established presence and expertise within the non-prime used car finance market. This has enabled the company to build sophisticated underwriting models and risk assessment capabilities. These models are specifically tailored to this customer segment. This proprietary knowledge, developed over decades, serves as a substantial barrier to entry for new competitors. For a comprehensive understanding of S&U's financial operations, consider reviewing the Revenue Streams & Business Model of S&U.

In the property bridging sector, Aspen Bridging benefits from its agile and relationship-driven approach. Its ability to offer quick decisions and flexible lending solutions appeals to developers and investors needing rapid access to capital. The company's streamlined processes and direct access to decision-makers enhance its responsiveness, a critical factor in the fast-paced bridging market. The company's ability to navigate complex property deals provides a distinct edge.

Advantage Finance's long-standing presence allows for sophisticated underwriting models. These models are specifically designed for the non-prime used car finance market. This expertise enables accurate risk pricing and maintains healthy loan book performance. This specialized knowledge creates a significant barrier to entry.

Aspen Bridging offers quick decisions and flexible lending options. This caters to developers needing rapid capital access for property transactions. The company's streamlined processes and direct access to decision-makers enhance responsiveness. This is a critical factor in the fast-paced bridging market.

S&U benefits from a strong balance sheet and prudent financial management. This allows it to maintain a stable funding base and absorb potential market shocks. The company's reputation for reliable lending fosters customer loyalty. This leads to repeat business and positive referrals.

Strong relationships with a network of used car dealerships across the UK provide a consistent business pipeline. These relationships reinforce the company's market position. Targeted marketing and ongoing investment in underwriting technology further support these advantages.

Key Competitive Advantages

S&U's competitive advantages are multifaceted, including specialized market focus, deep expertise, and robust operational frameworks. These advantages are supported by a strong balance sheet and prudent financial management. The company's brand equity, built on reliable lending practices, fosters customer loyalty.

- Specialized focus in non-prime used car finance and property bridging.

- Sophisticated underwriting models and risk assessment capabilities.

- Agile and relationship-driven approach in property bridging.

- Strong balance sheet and prudent financial management.

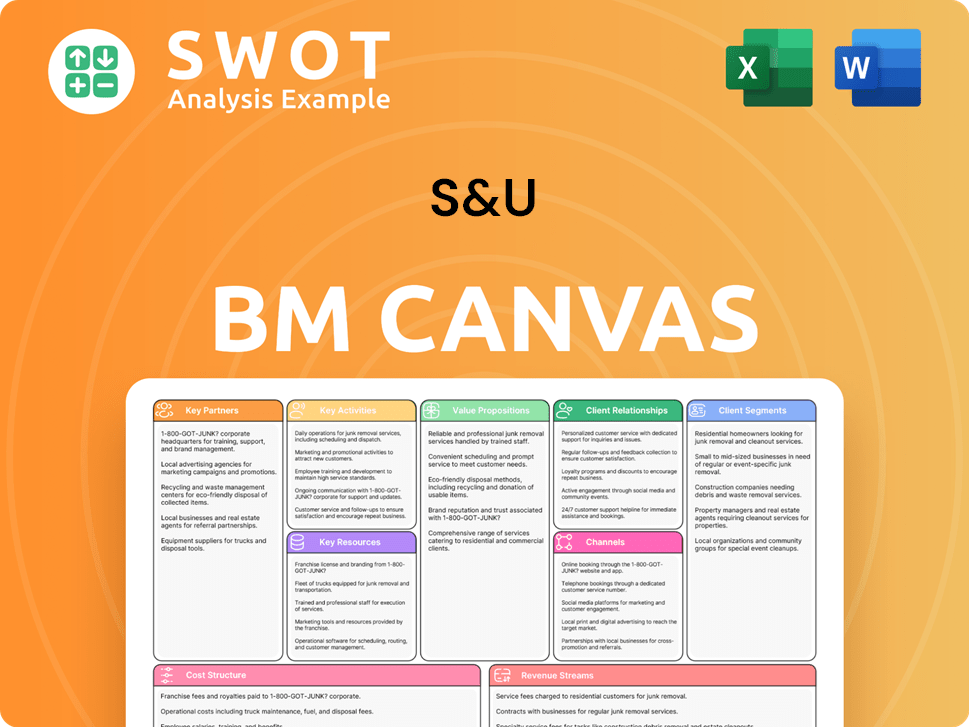

S&U Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Industry Trends Are Reshaping S&U’s Competitive Landscape?

The UK specialist lending industry, where S&U PLC operates, is currently experiencing significant shifts. These changes are driven by technological advancements, evolving regulatory landscapes, and changing consumer preferences. A thorough competitive landscape analysis is essential for understanding the company's position and formulating effective business strategy.

The future outlook for S&U hinges on its ability to adapt to these trends while navigating potential risks. The company must leverage opportunities for growth, such as expanding into underserved markets and innovating its product offerings. Understanding the market analysis and anticipating future challenges is crucial for maintaining a competitive advantage.

Technological advancements, particularly in data analytics and AI, are transforming credit assessment and operational efficiency. Regulatory changes, focused on consumer protection and responsible lending, are ongoing. Consumer preferences are shifting towards digital and seamless application processes, especially among younger demographics.

Intensified competition from fintech lenders with innovative models poses a threat. Economic downturns or declines in used car demand could negatively impact the market. Increased regulation around non-prime lending might restrict lending volumes or increase compliance burdens.

Emerging markets within the UK, such as regional property developments, offer expansion avenues. Product innovations, like flexible loan structures, can differentiate S&U. Strategic partnerships with tech providers or financial institutions could unlock new capabilities and market access.

S&U's strategy will likely involve continued investment in digital transformation. Cautious expansion into adjacent market niches is expected, along with a commitment to prudent risk management. The company will need to adapt to maintain its position in the competitive landscape.

Key Considerations

The specialist lending market is dynamic, with both risks and opportunities. S&U must balance technological advancements with regulatory compliance. Understanding consumer preferences and economic conditions is crucial for success.

- Competitive Landscape Analysis: Evaluate fintech entrants and their impact.

- Market Positioning: Differentiate through product innovation and customer service.

- Risk Management: Maintain strong underwriting standards and compliance.

- Growth Strategies: Explore new markets and partnerships.

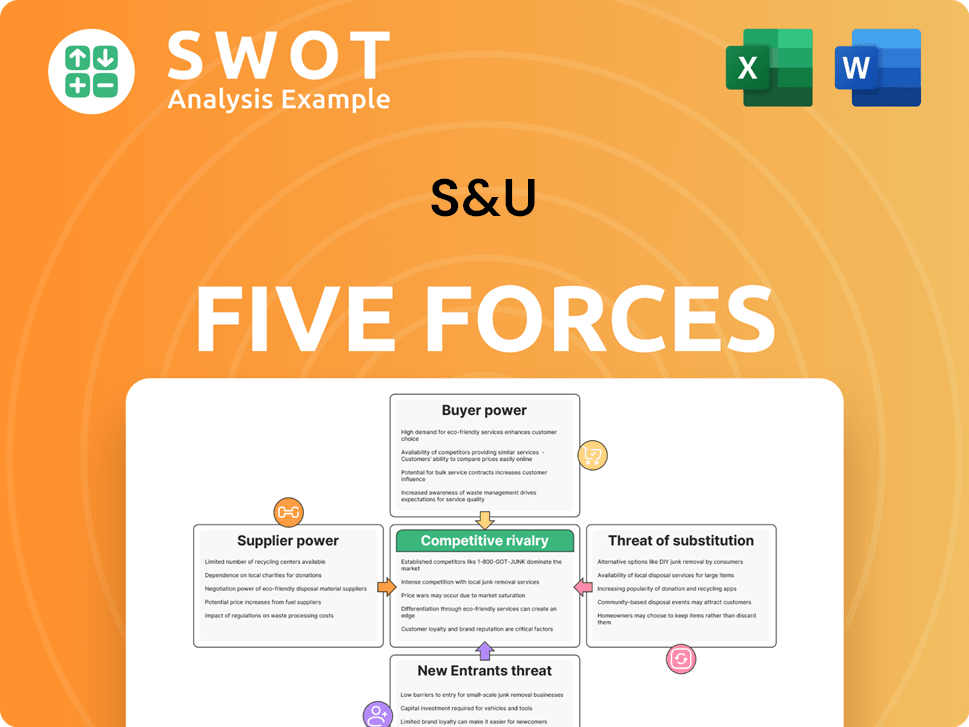

S&U Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of S&U Company?

- What is Growth Strategy and Future Prospects of S&U Company?

- How Does S&U Company Work?

- What is Sales and Marketing Strategy of S&U Company?

- What is Brief History of S&U Company?

- Who Owns S&U Company?

- What is Customer Demographics and Target Market of S&U Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.