Quilter Bundle

Who Does Quilter Serve?

In the ever-changing financial landscape, understanding the Quilter SWOT Analysis is more critical than ever. Quilter Company, a key player in wealth management, has strategically refined its focus. This deep dive explores the customer demographics and target market of Quilter, revealing the core segments driving its success.

This analysis will dissect Quilter's approach to market segmentation, identifying its ideal customer and building detailed buyer persona profiles. By examining the company's evolution and recent performance, including its 2024 achievements, we'll uncover how Quilter adapts to meet its clients' financial aspirations, ensuring a brighter financial future for every generation it serves.

Who Are Quilter’s Main Customers?

The primary customer segments for the company are High Net Worth (HNW) and Affluent individuals. These segments are served through a Business-to-Consumer (B2C) model, utilizing financial advice, investment platforms, and solutions. The company's distribution model includes both its restricted financial planners and Independent Financial Advisers (IFAs), ensuring a broad reach across various client types.

Understanding the customer demographics and target market is crucial for the company's success. The company uses market segmentation, informed by independent third-party research, to understand the financial behaviors, characteristics, needs, and potential vulnerabilities of its UK consumers. This approach helps tailor services and strategies effectively.

The company's strategic refresh in 2024, focusing on 'brighter financial futures for every generation,' reflects an ongoing adaptation to serve these diverse segments effectively. This customer-centric approach is key to maintaining and growing its market share.

The High Net Worth segment held £29.5 billion in Assets under Management (AuM) as of December 31, 2024, marking a 9% increase. This segment showed strong performance, with gross flows of £3.1 billion in 2024, a 42% increase from the previous year. Asset retention remained robust at 91% in 2024.

The Affluent segment held £88.5 billion in AuMA as of December 31, 2024, reflecting a 14% increase. The company's Investment Platform is a core component, representing about 69% of the group's AuMA as of September 30, 2023. Gross inflows from IFAs increased by 66% to £8.8 billion in 2024, with asset retention at 89%.

Customer Segmentation and Strategic Focus

The company employs a detailed market segmentation model to understand its customer base better. This includes segments like 'Starting Savings Journey,' 'Money Makers,' and 'Golden Age,' each with distinct financial behaviors and needs. The Growth Strategy of Quilter highlights the company's commitment to adapting to these diverse segments.

- 'Starting Savings Journey': Younger households with good incomes but high costs.

- 'Money Makers': High-income households accumulating assets despite high expenditure.

- 'Golden Age': Fortunate elders with pensions and financial choices.

- Focus on 'brighter financial futures for every generation' reflects a customer-centric approach.

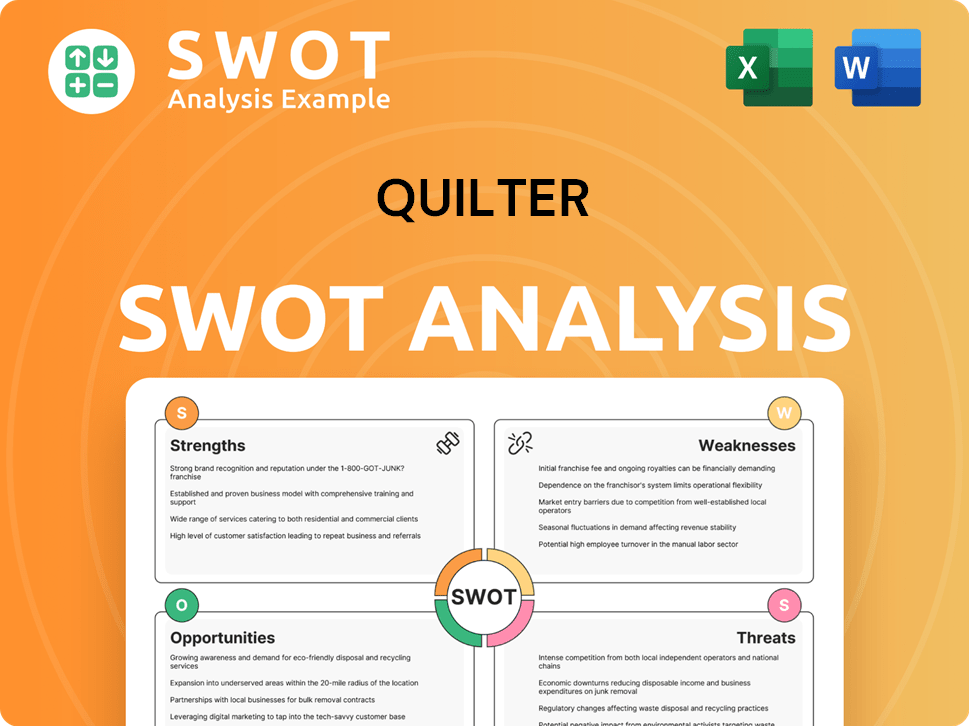

Quilter SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do Quilter’s Customers Want?

The customer needs and preferences for the financial services offered by the Quilter company are centered around comprehensive financial advice, robust investment platforms, and tailored investment solutions. Customers are looking for clarity and a deep understanding of their financial documentation. This is a key aspect of their decision-making process.

Purchasing behaviors are influenced by the need for secure custody arrangements and confidence in the firm's financial strength. Clients and financial advisors value direct contact with a dedicated investment manager and the convenience of multiple office locations, which enhances accessibility and personal service.

Quilter addresses common pain points by simplifying operational processes, particularly for the Affluent segment, to reduce duplication and complexity. The firm also focuses on providing value-added tools and services to enhance the customer experience.

Customer Trust and Satisfaction

Quilter Cheviot has a strong reputation, reflected in a Trustpilot score of 4.5 stars in 2024, indicating high levels of customer satisfaction. This positive feedback is crucial for building and maintaining customer trust and loyalty.

Financial Strength and Security

As of December 31, 2024, Quilter Cheviot managed over £119.4 billion in client investments. This significant amount underscores the company's financial strength and its ability to provide secure investment solutions.

Accessibility and Convenience

Quilter's network of 11 offices across the UK provides convenient access for clients and financial advisors. This accessibility is a key factor in meeting customer needs and preferences for personalized service.

Value-Added Services

Quilter offers value-added services such as family linking pricing, faster payment services, and its CashHub cash management offering. These services are designed to enhance the overall proposition for customers.

Digital Innovation

The acquisition of NuWealth in September 2024 is a strategic move to enhance digital capabilities. This allows Quilter to onboard clients directly, supporting advisors and creating additional growth opportunities.

Tailored Investment Solutions

Quilter tailors its offerings to specific segments, such as the WealthSelect offering, which has surpassed £18 billion in assets. The 'Positive Change' strategy caters to clients seeking ESG investments.

Key Customer Preferences

Understanding the needs and preferences of the target market is crucial for the success of the Quilter company. Quilter's approach to meeting customer needs includes providing comprehensive financial advice, a robust investment platform, and tailored investment solutions. Understanding the Marketing Strategy of Quilter can also provide insights into how the company addresses these preferences.

- Comprehensive Financial Advice: Customers value expert guidance to achieve their financial goals.

- Robust Investment Platforms: Clients seek reliable and efficient platforms for managing their investments.

- Tailored Investment Solutions: Personalized investment strategies that align with individual financial objectives.

- Clarity and Understanding: Customers need clear and easy-to-understand financial documentation.

- Secure Custody Arrangements: Clients prioritize the safety and security of their investments.

- Direct Contact: Access to dedicated investment managers for personalized service.

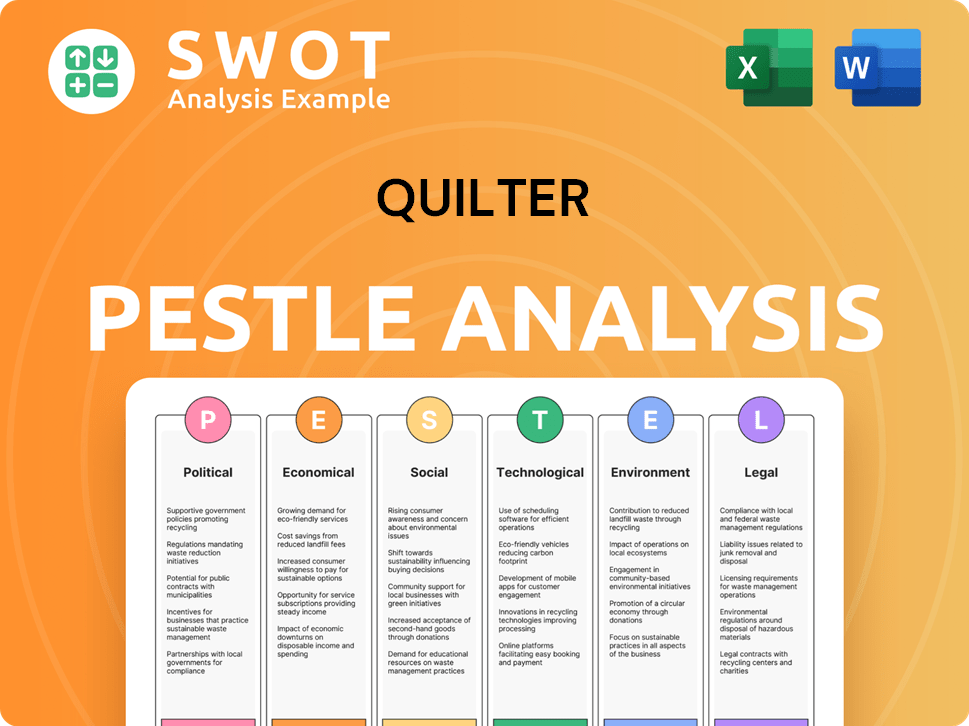

Quilter PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does Quilter operate?

The geographical market presence of the company is primarily focused on the UK and South Africa. As of December 31, 2024, the company managed a substantial £119.4 billion in customer investments, demonstrating its significant footprint in these regions. The company's strategic focus on these areas is reinforced by its listings on the London Stock Exchange (LSE) and the Johannesburg Stock Exchange (JSE).

In the UK, the company is recognized as the largest and fastest-growing retail advised platform provider. This underscores the company’s strong position in the UK market. The platform business is a key driver of growth, particularly with increased market share in gross inflows, especially from independent financial advisors.

The company's strategy involves localizing its offerings to succeed in diverse markets. The dual distribution strategy ensures that products and services are accessible to both internal and independent financial advisors. The acquisition of NuWealth in September 2024 is a strategic move to enhance digital capabilities and broaden offerings, including a direct-to-consumer channel, adaptable to various market needs.

The UK is the core market, with the company being the largest and fastest-growing retail advised platform provider. The company has a significant presence with 11 offices across the UK, facilitating direct client engagement.

The company also maintains a presence in South Africa. Executive Committee members were scheduled to host South African investors in June 2025, organized by UBS. Shareholders on the Johannesburg Stock Exchange have specific trading procedures.

Dual Distribution Strategy

The company employs a dual distribution strategy. This approach ensures its products and services are available to both internal and independent financial advisors. This broadens market penetration and accessibility for the company.

Strategic Acquisitions

The acquisition of NuWealth in September 2024 is aimed at accelerating digital capabilities. This move broadens the company's offerings, including a direct-to-consumer channel. This channel is adaptable to meet various market needs.

Market Share Growth

The company has gained market share in gross inflows, particularly from independent financial advisors. This growth highlights the company's increasing influence within the financial advisory sector. This is further detailed in the article Owners & Shareholders of Quilter.

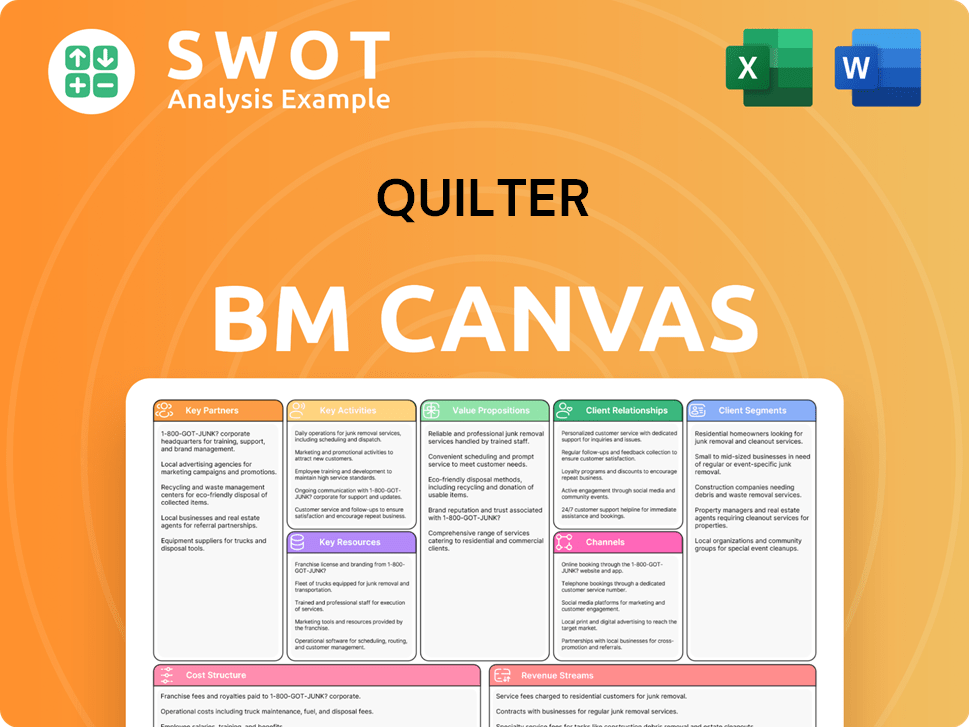

Quilter Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does Quilter Win & Keep Customers?

The company utilizes a dual-distribution strategy to acquire and retain customers, focusing on both its restricted financial planners and Independent Financial Advisers (IFAs). This approach has significantly boosted gross and net inflows across both channels. This dual approach allows for a broader reach within its target market, catering to various customer segments and their preferences.

In 2024, core net inflows reached £5.2 billion, a marked increase from £800 million in 2023, demonstrating robust acquisition momentum. Marketing efforts include direct engagement via financial advisors and increasing digital capabilities. The acquisition of NuWealth in September 2024 is a strategic move to accelerate digital onboarding, supporting advisors and potentially creating future growth pipelines.

Sales tactics include enhancing adviser productivity; for instance, annual gross flow per adviser increased by 14% to £3.2 million in 2024. These strategies are crucial for maintaining a competitive edge in the financial services sector and ensuring long-term customer relationships.

The company employs a dual-distribution strategy involving restricted financial planners (Quilter channel) and IFAs (IFA channel). This approach is designed to maximize market penetration and cater to a diverse customer base. This strategy helps reach a wider segment of the customer demographics and expand the target market.

The acquisition of NuWealth in September 2024 is a strategic move to accelerate digital onboarding. This enhances the efficiency of client onboarding and supports advisors in nurturing early-stage clients. Digital onboarding is a key component of the company’s strategy to improve customer experience and streamline processes.

Enhancements in adviser productivity are a key sales tactic. In 2024, annual gross flow per adviser increased by 14% to £3.2 million. This focus on productivity improvements directly contributes to increased net inflows and overall business growth.

Retention is supported by the value offered through the company's platform and investment solutions. Asset retention for the High Net Worth segment remained at 91% in 2024, and for the Affluent segment, it was stable at 89%. These strategies are essential for building long-term customer relationships and ensuring sustainable business performance.

Focus on Efficiency

The company is implementing simplification programs to enhance efficiency and improve its proposition. The goal is to achieve £50 million in cost savings by the end of 2025, with £35 million delivered by the end of 2024. These initiatives support sustainable operations and contribute to customer loyalty.

Value-Added Services

The company enhances its proposition through value-added tools and services, such as family linking pricing, faster payment services, and its CashHub cash management offering. These services help in differentiating the company's offerings and improving customer satisfaction. These services add value for the ideal customer.

Platform and Adviser Relationships

The company focuses on deepening relationships with existing advisers on its Platform and reducing outflow pressure from consolidators. This approach is crucial for retaining assets and maintaining strong relationships within the IFA channel. Deepening relationships is key to understanding and meeting the needs of the buyer persona.

Channel-Specific Performance

The Quilter channel saw a 46% increase in net inflows to £2.9 billion in 2024. For the IFA channel, gross inflows onto the company Platform increased by 66% to £8.8 billion in 2024, reflecting improved market share. These figures demonstrate the effectiveness of the company's channel-specific strategies.

Cost Savings and Operating Margin

The company is aiming to operate sustainably above a 30% operating margin. The cost-saving initiatives support this ambition. These efforts contribute to customer loyalty and lifetime value by ensuring competitive and efficient service delivery, which is crucial for the Quilter company.

Market Share and Growth

The company's strategies have led to significant growth in both gross and net inflows. The strong performance in the IFA channel, with a 66% increase in gross inflows, indicates improved market share and the effectiveness of the company's distribution strategy. This approach is designed to maximize market penetration and cater to a diverse customer base.

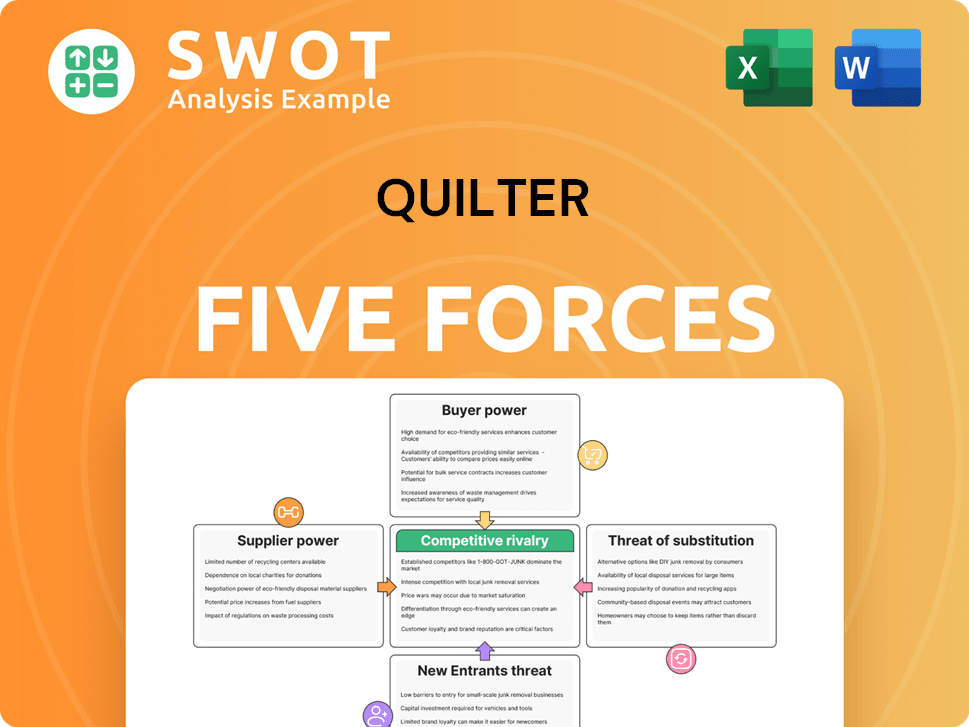

Quilter Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Quilter Company?

- What is Competitive Landscape of Quilter Company?

- What is Growth Strategy and Future Prospects of Quilter Company?

- How Does Quilter Company Work?

- What is Sales and Marketing Strategy of Quilter Company?

- What is Brief History of Quilter Company?

- Who Owns Quilter Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.