Pepper Bundle

Who are Pepper Money's customers, and how does it target them?

In the competitive landscape of non-bank lending, understanding the Pepper SWOT Analysis is crucial for success. Pepper Money's impressive financial performance, including a A$140.2 million net profit after tax in 2023, highlights the importance of knowing its customer base. This success is a direct result of the company’s ability to identify and serve specific segments often overlooked by traditional banks.

Pepper Money, a specialist lender since 2000, initially focused on customers outside mainstream banking criteria. This market analysis reveals the evolution of its target market, moving beyond niche segments to include a wider range of financial products. Today, we delve into the customer demographics, exploring their needs, locations, and how Pepper Money adapts its strategies in the ever-changing financial ecosystem, including the consumer profile and customer segmentation.

Who Are Pepper’s Main Customers?

Understanding the customer demographics and target market is crucial for the success of any financial institution. For the company, this involves identifying who they serve and how they tailor their products to meet specific needs. The company primarily focuses on the Australian and New Zealand markets, providing financial solutions to both consumers and businesses.

This focus on specialized lending allows the company to serve segments often overlooked by traditional banks. Their customer base includes individuals and businesses that may not fit standard lending criteria. This includes self-employed individuals, those with variable income, or those with less-than-perfect credit histories. The company's ability to cater to these niches is a key aspect of their business model.

The company's target market is diverse, encompassing both consumers (B2C) and businesses (B2B). This dual approach allows for a wider reach and a more comprehensive financial service offering. Analyzing the customer profile helps tailor products and marketing efforts effectively. A deep dive into the Marketing Strategy of Pepper can provide further insights into how they approach their target markets.

The B2C segment includes a broad age range, particularly those seeking residential mortgages or auto loans. This often includes first-time homebuyers and individuals looking to refinance existing loans. While specific age breakdowns aren't publicly detailed, the focus is on working-age adults. The company's products are designed to meet the needs of individuals seeking financial solutions for personal needs.

The B2B segment primarily serves small and medium-sized enterprises (SMEs). These businesses seek commercial real estate loans or asset finance to support growth. This segment requires flexible funding solutions that traditional banks may not offer. This allows businesses to secure capital for expansion, equipment, or property investments.

Market Analysis and Customer Segmentation

The company's market analysis reveals consistent demand for non-conforming loans, indicating a significant portion of the population requires alternative lending options. In 2023, the company reported a mortgage loan book of A$14.8 billion, demonstrating the substantial contribution of this segment to its revenue. The company's ability to adapt product offerings and risk assessment models has enabled it to maintain a competitive edge.

- Customer Segmentation: The company segments its market based on the need for specialized financial products, such as non-conforming mortgages and commercial real estate loans.

- Geographic Focus: The primary geographic focus is Australia and New Zealand, where the company has established a strong presence.

- Income Levels: The target market includes individuals and businesses with varying income levels, particularly those who may not meet the stringent requirements of traditional lenders.

- Loan Book: The company's mortgage loan book of A$14.8 billion in 2023 reflects the success of its customer segmentation and market strategies.

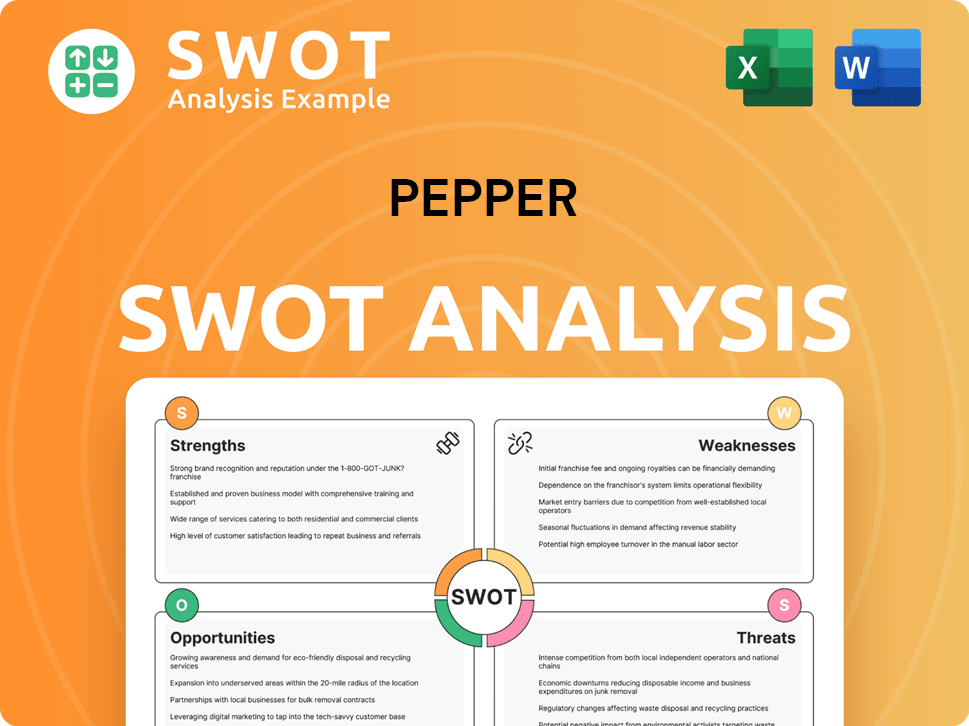

Pepper SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do Pepper’s Customers Want?

Understanding the customer needs and preferences is crucial for the success of any financial institution. For the company, the focus is on providing accessible and flexible financial solutions, especially for those who may not fit the traditional banking mold. This approach helps the company cater to a specific segment of the market, ensuring its services meet the unique needs of its customers.

The primary drivers for the company's customers are the need for financial products that are accessible and flexible. These customers often seek options when traditional banks are not an option. They value lenders who consider individual circumstances beyond standard credit scores, such as self-employment or a history of minor credit issues. This customer profile is a key element in the company's market analysis and customer segmentation strategies.

The decision-making process for these customers prioritizes factors such as loan approval speed, personalized service, and competitive interest rates. While the interest rates might be slightly higher than prime rates, the increased accessibility is a significant draw. This focus on customer needs helps define the company's target market and identify the ideal customer for its financial products.

Purchasing Behaviors

Customers often seek lenders who consider individual circumstances beyond standard credit scores. They look for options when traditional banking avenues are not viable.

Decision-Making Criteria

Factors like loan approval speed, personalized service, and competitive interest rates are heavily weighed. Accessibility is a key factor, even if it means slightly higher interest rates.

Product Usage

Customers use the company's services for significant life purchases like homeownership and vehicle acquisition. They also utilize them for business expansion.

Loyalty Factors

Positive experiences with the application process, support, and flexible loan terms drive customer loyalty. These factors are crucial for retaining customers.

Psychological Drivers

Aspiration for financial independence and stability drives customer decisions. This is a key psychological factor in their choices.

Practical Drivers

Securing necessary funds for personal or business growth motivates customers. This is a practical need that the company addresses.

The company addresses common pain points such as rigid credit assessments and slow approval processes. By offering tailored solutions and a more human-centric approach to lending, they meet the needs of their target market. This is further supported by the company's marketing, which often showcases success stories of individuals or businesses that have achieved their goals through the company's flexible lending options. This approach helps in analyzing consumer behavior and defining the company's target market. For more insights, you can read about the Growth Strategy of Pepper.

Market Trends and Adaptations

The company continuously refines its offerings to meet the evolving needs of its diverse customer base. This includes adapting to the increasing demand for specialist lending in regions like Australia and New Zealand.

- The company tailors its marketing messages to emphasize its understanding of unique financial situations.

- They highlight their commitment to finding solutions where others might not.

- Product features and customer experiences are adapted to specific segments.

- The company's approach is designed to meet the demands of its customer demographics.

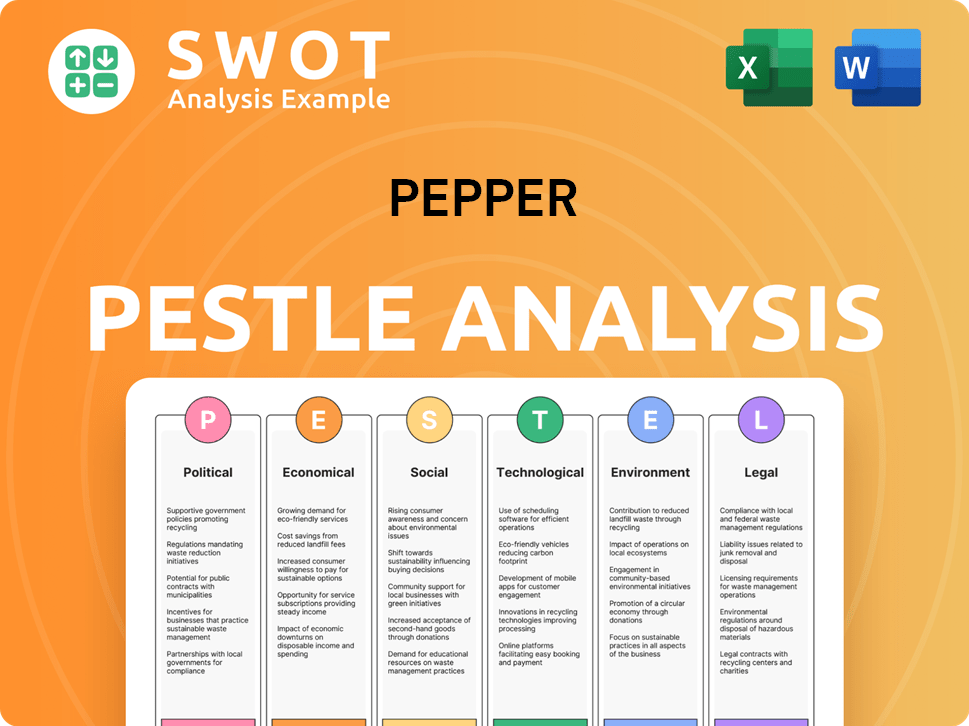

Pepper PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does Pepper operate?

The geographical market presence of the company is primarily concentrated in Australia and New Zealand. These two countries serve as the core markets, where the company has built a strong reputation within the non-bank lending sector. The focus is on providing financial solutions, including residential mortgages, commercial real estate loans, and asset finance, to a diverse clientele.

Within Australia and New Zealand, the company has established a significant market share, especially in specialist lending segments. This includes catering to borrowers who may not meet the traditional lending criteria of mainstream banks. The company’s strategic approach involves understanding and adapting to the specific market dynamics of each region.

The company's success in these markets is demonstrated by its financial performance. For example, the company's loan book grew to A$18.9 billion in 2023, reflecting strong performance across its operational geographies. The geographic distribution of sales and growth is heavily concentrated within Australia and New Zealand, where the company continues to solidify its position as a leading non-bank lender. For more insights into the company's structure, you can read about Owners & Shareholders of Pepper.

The company's primary focus is on the Australian and New Zealand markets. These regions are key to its business strategy, with a strong emphasis on residential mortgages and commercial real estate loans. The company tailors its services to meet the specific needs of borrowers in these areas.

The company serves a diverse range of customers, including self-employed individuals and those with non-traditional income streams. It caters to borrowers who may not fit the standard criteria of traditional banks. This approach allows it to capture a significant portion of the specialist lending market.

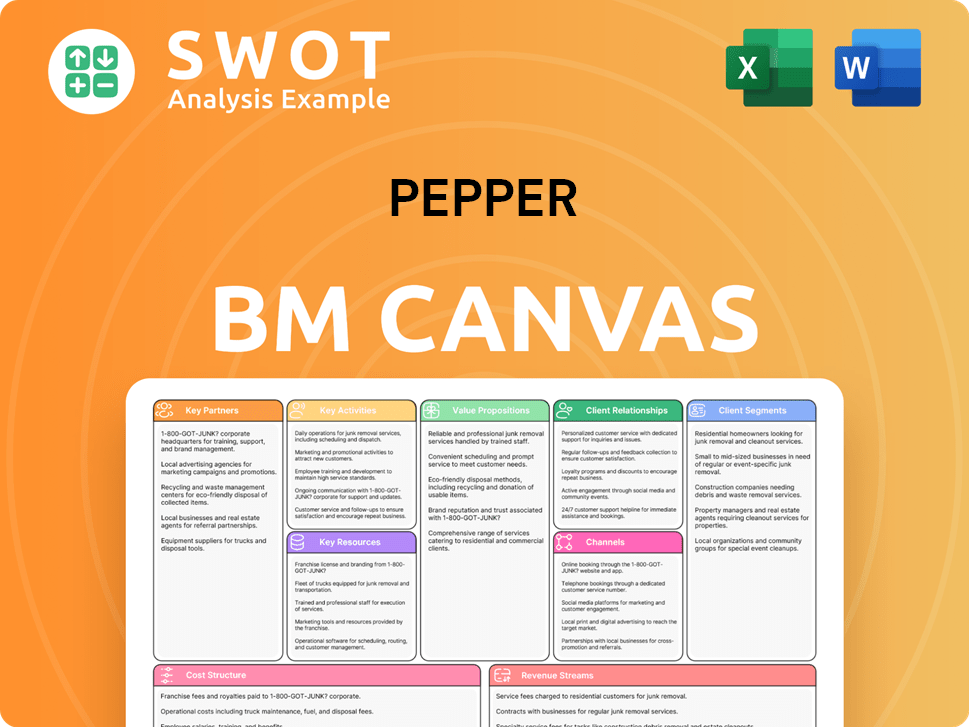

Pepper Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does Pepper Win & Keep Customers?

Customer acquisition and retention strategies at the [Company Name] are multifaceted, focusing on both digital and traditional approaches. A substantial portion of their new business comes through mortgage brokers and introducers, highlighting the importance of B2B relationships in reaching borrowers needing specialist lending solutions. Digital marketing, including targeted online campaigns and SEO, also plays a crucial role in directly attracting potential customers.

The company emphasizes personalized customer experiences and efficient after-sales service to retain customers. This includes streamlined loan processes, responsive customer support, and ongoing communication. Data analytics and CRM systems are used to segment customers and tailor offerings, which enhances loyalty. Broker remuneration structures and potential preferential rates for existing customers are likely integrated into loyalty programs.

The evolution of these strategies has focused on enhancing the broker experience and boosting digital engagement. The growth of their loan book, reaching A$18.9 billion in 2023, indicates effective acquisition and retention, contributing to a higher customer lifetime value and reduced churn rates. Adapting strategies to market conditions and customer feedback has been key to maintaining a competitive edge in the specialist lending market. To learn more about the company's background, you can read Brief History of Pepper.

The company leverages an extensive network of mortgage brokers and introducers. These brokers are crucial for connecting the company with borrowers who require specialist lending solutions. This B2B approach is a primary channel for customer acquisition, as brokers often serve as the initial point of contact for potential customers.

Digital marketing includes targeted online campaigns, search engine optimization (SEO), and social media presence. The goal is to reach potential customers directly. Digital strategies likely highlight flexible lending criteria and diverse product offerings to differentiate the company from traditional banks.

The company focuses on personalized customer experiences and efficient after-sales service. This includes streamlined loan application processes and responsive customer support. Ongoing communication is also a key component of enhancing customer satisfaction and retention.

Investment in technology and data analytics, including CRM systems, helps in customer segmentation. This allows for tailored communication and product offerings, enhancing customer loyalty. The use of data-driven insights supports the company's customer-centric approach.

Key Strategies

The company's strategies focus on enhancing the broker experience and improving digital engagement. These efforts have contributed to the growth of the loan book and increased customer lifetime value. The company's ability to adapt to market conditions is crucial for maintaining its competitive edge.

- Emphasis on broker relationships for customer acquisition.

- Targeted digital marketing campaigns to reach potential customers.

- Personalized customer experiences and efficient after-sales service.

- Use of data analytics and CRM for customer segmentation.

- Adaptation of strategies to market conditions and customer feedback.

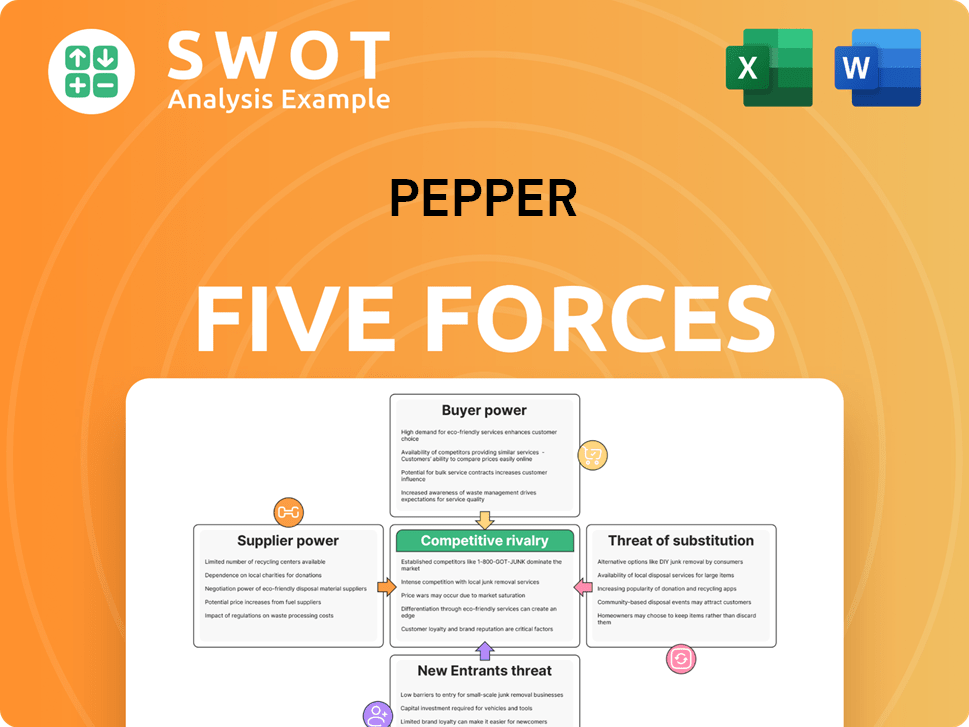

Pepper Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Pepper Company?

- What is Competitive Landscape of Pepper Company?

- What is Growth Strategy and Future Prospects of Pepper Company?

- How Does Pepper Company Work?

- What is Sales and Marketing Strategy of Pepper Company?

- What is Brief History of Pepper Company?

- Who Owns Pepper Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.