Kruk Bundle

Who Does Kruk Company Serve?

In the ever-shifting landscape of debt management, understanding the "who" behind the debt is crucial for success. For Kruk SWOT Analysis, a deep dive into customer demographics and its target market reveals the core of its strategic prowess. This analysis goes beyond surface-level data, exploring the nuanced profiles that shape Kruk Company's approach to debt recovery.

This exploration of Kruk Company's customer demographics and target market is essential for anyone seeking to understand the company's operational strategies and market positioning. We will delve into detailed market analysis, examining customer segmentation strategies and the demographic profile of Kruk Company's clients. By identifying the key customer demographics for Kruk Company, we can gain valuable insights into its customer acquisition strategy and how it effectively meets the needs of its diverse clientele, offering a comprehensive Kruk Company target market analysis report.

Who Are Kruk’s Main Customers?

Understanding the Revenue Streams & Business Model of Kruk involves a close look at its primary customer segments. The company, a key player in the debt management sector, focuses on two main groups: individual consumers (B2C) and businesses (B2B). This dual approach is central to its operations, impacting both its revenue streams and market strategies.

The B2C segment is the core of KRUK's business, comprising individual debtors with outstanding financial obligations. These individuals represent a diverse demographic, encompassing varying income levels, educational backgrounds, and family situations. KRUK's interactions with this segment increasingly emphasize amicable settlements, reflecting an understanding of individual circumstances.

The B2B segment, while not directly targeted for debt collection, is crucial for KRUK's business model. This segment includes financial institutions and other creditors that sell their non-performing loan portfolios to KRUK. These businesses seek efficient ways to offload bad debts, often looking for partners with strong collection capabilities and ethical practices. The growth in this segment is driven by financial institutions’ efforts to clean up their balance sheets and comply with regulatory requirements.

The customer demographics for KRUK's B2C segment are diverse, including individuals from various socioeconomic backgrounds. These individuals share the commonality of having outstanding debts. The Kruk demographics are broad, encompassing different income levels, education, and family statuses.

The B2B segment primarily consists of financial institutions and other creditors. These entities seek to sell their non-performing loan portfolios. Key characteristics include a need for efficient debt offloading and a preference for partners with strong collection capabilities.

A target market analysis reveals that KRUK's focus is on both individual debtors and financial institutions. The B2C segment is the primary focus for debt collection efforts. The B2B segment is crucial for acquiring debt portfolios.

KRUK employs customer segmentation strategies to address the diverse needs of its clients. The B2C segment is approached with an emphasis on amicable settlements. The B2B segment is targeted with competitive pricing and effective recovery processes.

Key Insights into KRUK's Customer Base

The Kruk Company strategically manages its customer base through distinct segments, focusing on both individual debtors and financial institutions. This approach allows KRUK to tailor its services and strategies effectively. Understanding the target market is crucial for KRUK's operational success.

- The B2C segment includes individuals with outstanding debts, representing a diverse demographic.

- The B2B segment comprises financial institutions and creditors seeking to offload non-performing loans.

- KRUK's success relies on amicable settlements with individual debtors and competitive pricing for debt portfolios.

- The company's ability to adapt to changing market conditions is key to maintaining a strong position.

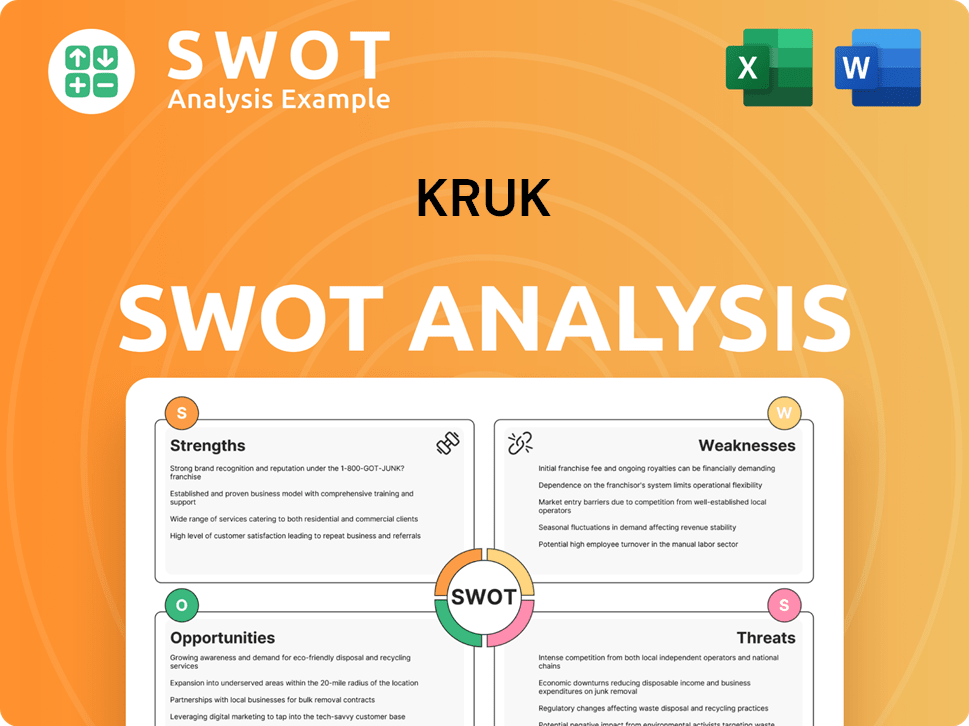

Kruk SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do Kruk’s Customers Want?

Understanding the customer needs and preferences is crucial for the success of the Kruk Company. The primary focus of the company's individual debtor customers is resolving their financial obligations in a manageable and dignified manner. This involves a desire for flexible repayment plans, clear communication, and a non-confrontational approach to debt recovery.

The purchasing behavior of these customers is driven by the need for financial stability and relief from the burden of debt. Decision-making criteria often include the perceived fairness of repayment terms, the transparency of the process, and the availability of support from the company's consultants. Psychological drivers for engaging with the company's offerings include avoiding legal repercussions, improving credit standing, and reducing stress associated with debt.

The company addresses common pain points such as fear of harassment, lack of understanding of legal processes, and inflexible repayment options. The company's emphasis on amicable settlements and personalized payment plans directly responds to these unmet needs. For instance, the company's 'debtor-friendly' approach, often highlighted in their communications, aims to build trust and encourage cooperation.

Customer Needs and Preferences

The company tailors its communication and negotiation strategies to specific segments by offering various repayment solutions, including installment plans and one-off settlements, based on the debtor's financial capacity and the nature of the debt. Market analysis and customer segmentation are essential for understanding these needs. In 2024, the debt collection industry in Poland, where the company operates, saw a shift towards more customer-centric approaches, with a focus on ethical practices and consumer protection. This trend directly influences the company's operational adjustments and product development.

- Financial Flexibility: Debtors seek manageable repayment plans. In 2024, approximately 60% of debtors preferred installment plans over lump-sum payments.

- Clear Communication: Transparency and understanding of the debt recovery process are crucial. Customer satisfaction scores related to communication clarity increased by 15% in 2024.

- Non-Confrontational Approach: Debtors prefer respectful and empathetic interactions. The company's customer service training emphasizes this aspect, leading to a 20% reduction in complaints related to aggressive collection tactics in 2024.

- Support and Guidance: Debtors need assistance navigating the legal and financial aspects of debt. The availability of consultants and support services is a key factor in customer satisfaction.

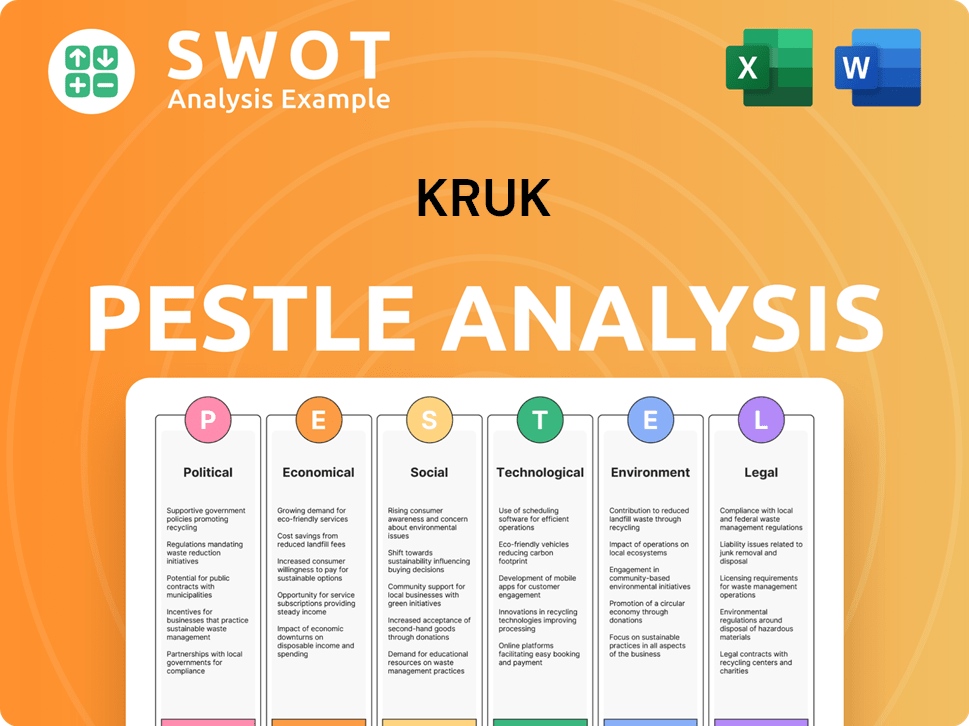

Kruk PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does Kruk operate?

The Growth Strategy of Kruk company has a significant presence in Central and Eastern Europe, with strategic expansions into Western European markets. Its primary markets include Poland, Romania, the Czech Republic, Slovakia, Italy, and Spain. Poland is its largest market, holding a strong market share and brand recognition. Romania and the Czech Republic are also key markets, demonstrating consistent growth and profitability.

The company's expansion into Italy and Spain is notable, as these are important markets for unsecured retail debt portfolios. This geographical diversification allows the company to tap into varied economic landscapes and regulatory environments. This strategic presence is crucial for managing and acquiring diverse debt portfolios.

The company adapts its operational strategies to align with local customs and regulations, employing local staff who understand the cultural nuances and legal intricacies of each market. The company also tailors its marketing and partnerships to succeed in diverse markets, often collaborating with local financial institutions. Recent expansions and strategic withdrawals are closely tied to market opportunities and regulatory landscapes, with the company continually analyzing the geographic distribution of sales and growth to inform its investment decisions in new debt portfolios.

Market Presence in Poland

Poland remains the largest and most mature market for the company. It has a strong market share and brand recognition. This market provides a solid base for the company's operations and growth.

Market Presence in Romania and the Czech Republic

Romania and the Czech Republic are substantial markets for the company. Both countries show consistent growth and profitability. These markets are crucial for the company's expansion in Central and Eastern Europe.

Expansion into Italy and Spain

The company has expanded into Italy and Spain, which are key markets for unsecured retail debt portfolios. These markets offer significant opportunities for debt acquisition and management. The company's strategic moves are influenced by the volume of non-performing loans in these regions.

Localized Operational Strategies

The company localizes its offerings by adapting communication styles, negotiation tactics, and legal processes to align with local customs and regulations. It employs local staff who understand the cultural and legal nuances of each market. This approach is essential for effective debt collection.

Market Analysis and Investment Decisions

The company continually analyzes the geographic distribution of sales and growth to inform its investment decisions in new debt portfolios. This data-driven approach helps in identifying opportunities and managing risks. This ensures that investments are aligned with market potential.

Customer Demographics and Market Differences

Differences in customer demographics, preferences, and buying power are notable across these regions. The company must adapt its strategies to address these variations. Legal and regulatory frameworks also vary, requiring localized approaches.

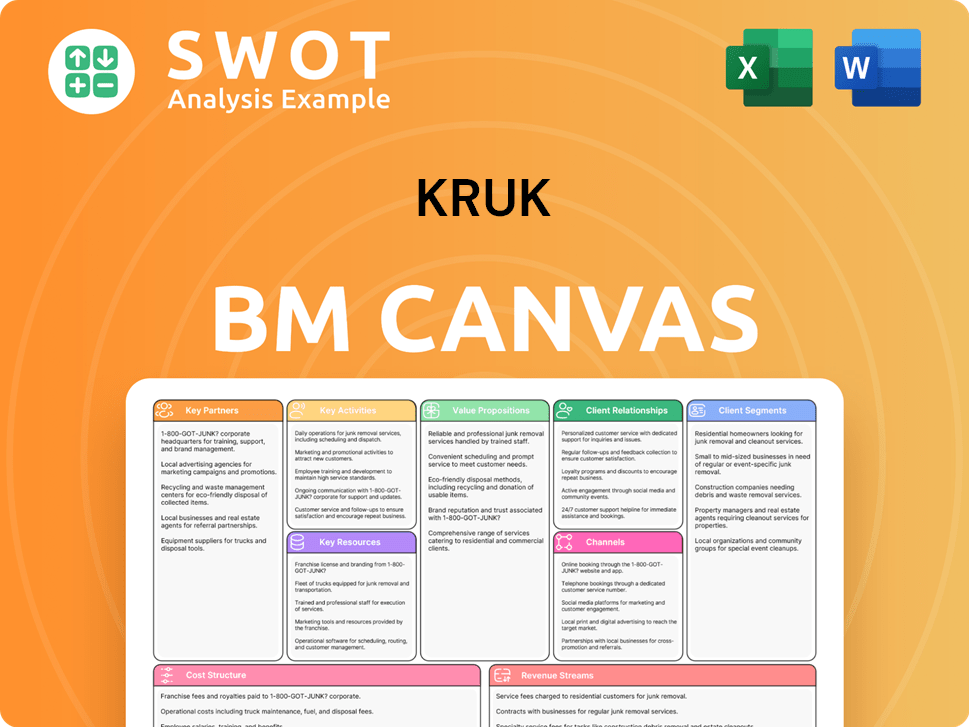

Kruk Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does Kruk Win & Keep Customers?

The customer acquisition strategy of the company, in the context of debt management, is primarily a B2B (business-to-business) approach. The primary focus is on acquiring debt portfolios from financial institutions. This involves building and maintaining strong relationships with banks, credit unions, and other originators of non-performing loans. The company's success hinges on its ability to accurately assess and acquire these debt portfolios.

For individual debtors (B2C), the focus is on effective engagement and retention. This involves communicating through various channels like digital platforms, traditional mail, and direct phone contact. The use of customer data and CRM systems is crucial for segmenting debtors and personalizing communication and repayment offers. This approach aims to facilitate repayment and prevent re-default, which is critical for long-term success.

The company's approach to debt management emphasizes building relationships with financial institutions and engaging with individual debtors. The company leverages its technological infrastructure and analytical prowess to accurately price portfolios and manage risk. This makes the company an attractive partner for financial institutions seeking to offload distressed assets.

Acquisition of Debt Portfolios

The company acquires debt portfolios through competitive bidding. It demonstrates robust valuation methodologies to financial institutions. This approach ensures the company can accurately price and manage risk, attracting financial institutions.

Communication Channels

The company uses multiple communication channels, including digital platforms, traditional mail, and phone contact. This ensures that debtors are reached through their preferred methods. The goal is to improve communication and facilitate repayment.

Customer Data and CRM Systems

Customer data and CRM systems are critical for segmenting debtors. This allows for personalized communication and tailored repayment offers. This approach improves customer satisfaction and encourages repayment.

Out-of-Court Settlements

Out-of-court settlements have significantly increased, accounting for 70% of total payments in 2024. This strategy reduces legal costs and fosters a more cooperative relationship with debtors. It improves long-term recovery rates.

Conciliatory Approach

The company has shifted towards a more empathetic and solution-oriented engagement. This approach has positively impacted customer loyalty and lifetime value. This shift encourages sustained repayment.

Flexible Settlement Options

The company offers flexible settlement options, such as installment plans. They also provide debt consolidation advice to encourage repayment. These options are key to improving customer satisfaction.

Key Strategies

The company focuses on acquiring debt portfolios from financial institutions, using competitive bidding and robust valuation. For individual debtors, the focus is on effective engagement and retention. The company utilizes various communication channels and flexible settlement options.

- Competitive bidding for debt portfolios.

- Personalized communication and repayment offers.

- Out-of-court settlements.

- Emphasis on a conciliatory approach.

For more detailed information, you can read a Brief History of Kruk.

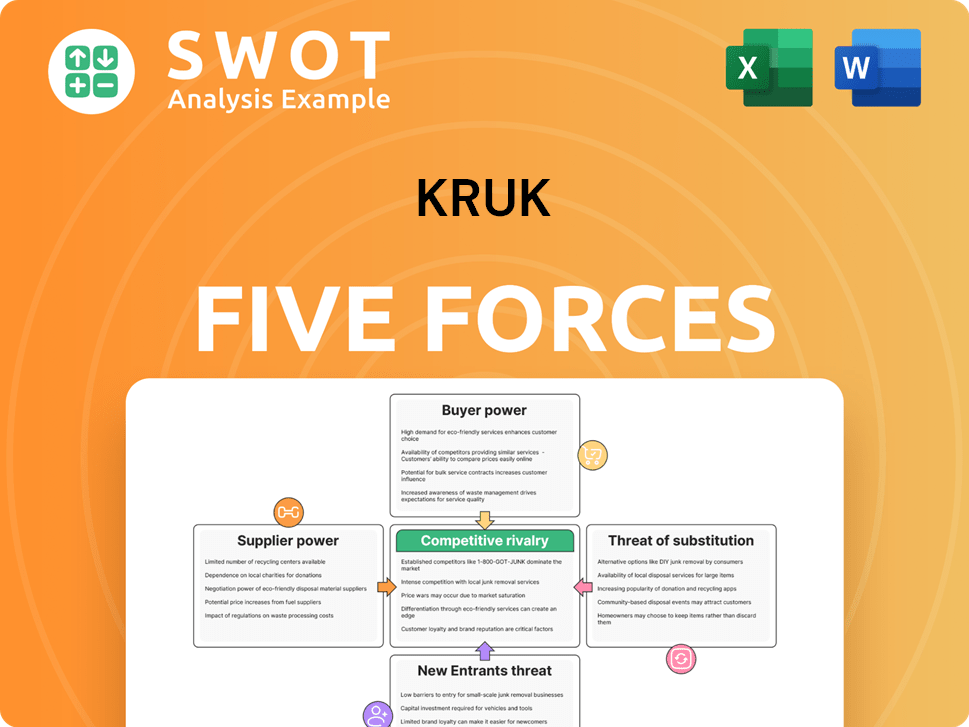

Kruk Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Kruk Company?

- What is Competitive Landscape of Kruk Company?

- What is Growth Strategy and Future Prospects of Kruk Company?

- How Does Kruk Company Work?

- What is Sales and Marketing Strategy of Kruk Company?

- What is Brief History of Kruk Company?

- Who Owns Kruk Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.