Fairfax Bundle

Who Are Fairfax Company's Customers?

In the complex world of insurance and reinsurance, understanding the Fairfax SWOT Analysis is crucial for any investor or strategist. Knowing the customer demographics and target market is not just an exercise; it's the cornerstone of sustainable growth for a company like Fairfax Financial Holdings Limited. This analysis dives deep into the customer base of Fairfax Company, revealing the strategies behind its success.

This exploration of Fairfax Company's customer demographics and target market will provide valuable insights for audience analysis. We'll examine the diverse customer segments served by Fairfax's subsidiaries, from geographic locations to customer buying behavior. Discover how Fairfax uses market segmentation strategies to meet the needs and wants of its customers and how to research Fairfax Company's target market.

Who Are Fairfax’s Main Customers?

Understanding the customer demographics and target market of the Fairfax Company is crucial for grasping its business model. The company primarily focuses on serving businesses (B2B) through its insurance and reinsurance subsidiaries. This strategic focus shapes its customer profile and market segmentation.

The core of Fairfax's operations revolves around its property and casualty insurance and reinsurance businesses. These entities, including Crum & Forster, Odyssey Group, and others, provide services to a wide array of commercial clients. This B2B approach is a defining characteristic of Fairfax's target market.

While primarily B2B, Fairfax has expanded into consumer markets through acquisitions like Sleep Country Canada Holdings Inc. This diversification indicates a dual approach, with a significant presence in commercial insurance and a growing, though smaller, footprint in retail and food services. This evolution is important for a comprehensive Fairfax Company target market analysis.

The primary customer segment is businesses seeking property and casualty insurance and reinsurance services. These clients span various industries and sizes, reflecting a broad commercial focus. The company's subsidiaries cater to diverse needs within this segment.

Fairfax also serves consumers through its investments in retail (Sleep Country) and food services (Recipe Unlimited). These segments represent a smaller portion of the overall business but indicate diversification into B2C markets. This diversification is a key aspect of understanding the company's customer demographics.

The company operates globally, with a significant presence in North America, particularly in the United States and Canada. Its subsidiaries like Northbridge Financial focus on the Canadian market, while others like Allied World have a global reach. This geographic diversity is crucial for understanding where Fairfax Company gets its customers from.

In 2024, Fairfax's property and casualty insurance and reinsurance operations achieved a record underwriting profit of $1.8 billion and generated $32.5 billion in gross premiums written. Net premiums written grew by 11.6% in 2024. These figures highlight the continued strength and growth in its core insurance and reinsurance segments.

Key Takeaways

Fairfax's primary target market consists of businesses requiring insurance and reinsurance solutions, with a secondary focus on consumer markets through strategic acquisitions. The company's revenue is largely driven by its insurance operations, with a strong performance in 2024. Understanding these segments is essential for a comprehensive Fairfax Company customer profile examples.

- The majority of Fairfax's customer base is B2B, focusing on insurance and reinsurance services.

- The company is diversifying into consumer markets through acquisitions.

- Geographic focus includes North America and global markets.

- Strong financial performance in the insurance sector drives overall growth.

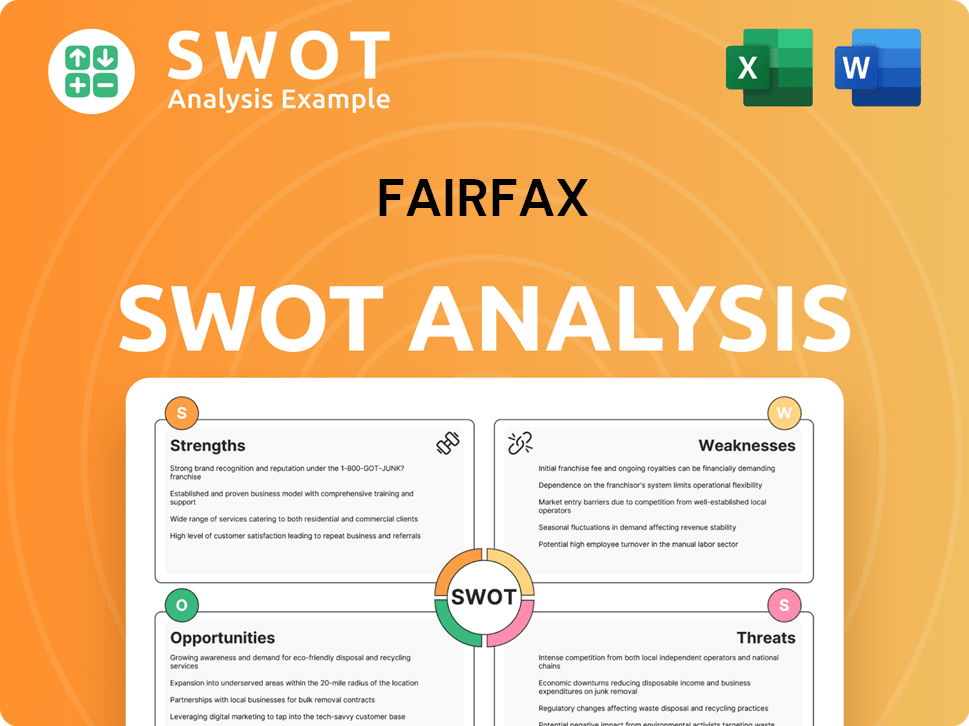

Fairfax SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do Fairfax’s Customers Want?

Understanding the customer needs and preferences is crucial for businesses like Fairfax Financial. Their core customers, primarily businesses, seek property and casualty insurance and reinsurance solutions. These clients are driven by essential needs related to risk mitigation, financial stability, and reliable claims handling.

The purchasing behaviors of the target market are shaped by several factors. These include the scope of coverage offered, the financial strength and reputation of the insurer, competitive pricing, and the efficiency of policy issuance and claims processing. For instance, clients prioritize robust underwriting and timely payouts to ensure business continuity and minimize financial disruptions.

Fairfax's decentralized model, with autonomous operating subsidiaries, allows for tailoring offerings to specific industry needs and risk profiles. This approach enables the company to better meet the diverse needs of its customer base, enhancing its market position and customer satisfaction.

Psychological Drivers

Psychological drivers for choosing Fairfax revolve around trust and security. This is particularly important given the long-term nature of insurance contracts and the potential for large claims. Customers need to feel confident in their insurer's ability to provide support when needed.

Practical Drivers

Practical drivers include comprehensive policy terms, efficient administrative processes, and access to specialized expertise in complex risk areas. These practical elements ensure that the insurance solutions are user-friendly and meet the specific needs of the clients.

Aspirational Drivers

Aspirational drivers involve partnering with a financially sound and reputable insurer that can support their growth and expansion. Clients seek insurers that can be long-term partners, providing stability and support as their businesses evolve.

Financial Strength

Fairfax's strong financial position, with $2.5 billion in cash and marketable securities at the holding company level at the end of 2024, and total portfolio investments of $62.9 billion held by its insurance and reinsurance companies, reinforces this trust. This financial stability reassures clients.

Customer Pain Points

Common pain points that Fairfax's subsidiaries address include the complexity of navigating diverse regulatory environments, the need for customized coverage for unique risks, and the desire for responsive customer service during critical periods. Addressing these issues enhances customer satisfaction.

Underwriting Performance

Fairfax's emphasis on 'disciplined underwriting' and 'strong underwriting performance' suggests a focus on providing effective and sustainable insurance solutions. The company's consistent underwriting profit, which reached a record $1.8 billion in 2024 despite absorbing $1.1 billion in catastrophe losses, indicates its ability to manage risks effectively.

The customer needs and preferences for Fairfax's business are centered on long-term value creation. This is reflected in the company's focus on long-term growth in book value per share, aligning with the long-term risk management needs of its clients. The company's ability to maintain profitability and provide valuable coverage, even in the face of significant catastrophe losses, highlights its commitment to meeting customer needs.

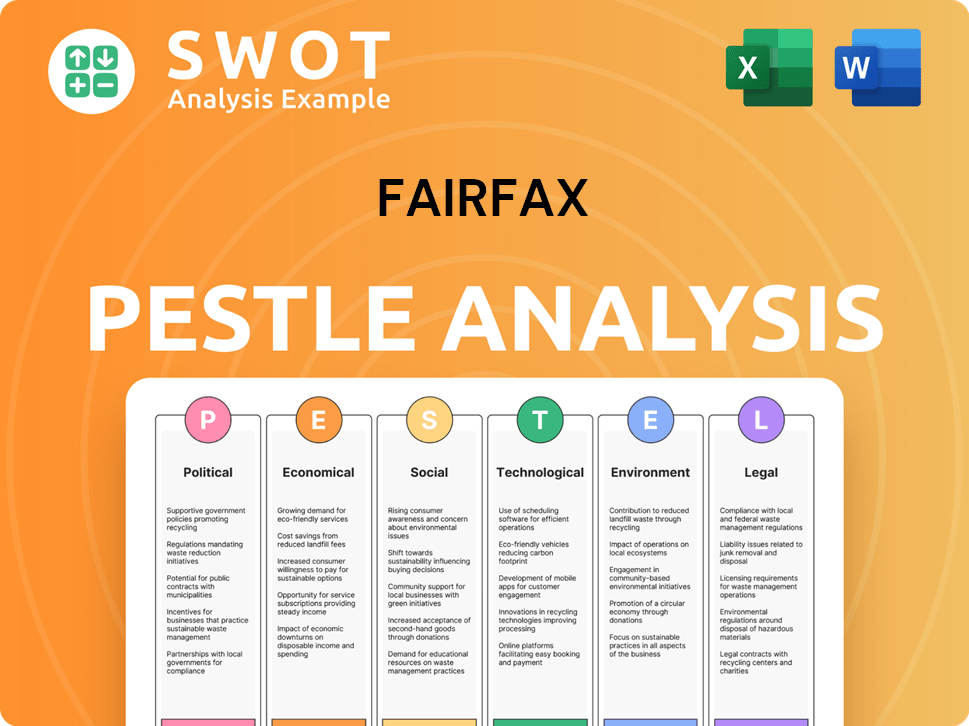

Fairfax PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does Fairfax operate?

The geographical market presence of the company is extensive, with operations spanning North America, Europe, Asia, and Latin America. This global footprint is supported by a network of subsidiaries strategically located to serve diverse regional markets. The company's reach is further expanded through strategic acquisitions and investments, solidifying its position in key markets worldwide.

The company's operations are decentralized, empowering subsidiaries to adapt to local market conditions. This approach allows for a tailored response to the varied customer demographics and preferences across different regions. The company's structure allows it to capitalize on local market opportunities and address the specific needs of its customers in each geographic area.

The company's commitment to international expansion is evident through its strategic acquisitions and investments. These moves have strengthened its presence in key markets, with a focus on long-term growth. For instance, in 2023, the acquisition of Gulf Insurance Group boosted gross premiums written by $2.7 billion. Moreover, the increased ownership in Brit in December 2024, reinforced its position in the Lloyd's of London market, and the recent acquisition of Sleep Country Canada Holdings Inc. in October 2024, highlights its commitment to expanding its reach.

The company has a strong presence in North America, particularly in Canada and the United States. Northbridge Financial is a key player in the Canadian property and casualty insurance market. In the U.S., Crum & Forster and Zenith National are prominent in commercial property and casualty and workers' compensation insurance, respectively. These subsidiaries cater to specific customer needs within the region.

Brit, a market-leading global Lloyd's of London specialty insurer and reinsurer, is based in London, England. The company's operations in Europe are focused on specialty insurance and reinsurance, serving a diverse customer base. The strategic location in London allows access to the Lloyd's market and international clients.

The company is optimistic about long-term growth in Asia, where premiums rose by 16% in Q1 2025. This region presents significant opportunities for expansion and diversification. The company's focus on Asia reflects its strategic vision for future growth.

Odyssey Group, headquartered in Stamford, Connecticut, underwrites reinsurance and specialty insurance with principal locations in Latin America. This presence supports the company's global reach and ability to serve diverse markets. The Latin American market contributes to the company's overall revenue.

Decentralized Operations

The company operates on a decentralized basis, allowing subsidiaries to adapt to local market conditions. This structure enables them to make decisions that resonate with their regional customer bases. This approach is crucial for effectively targeting the diverse customer demographics.

Key Subsidiaries

Key subsidiaries like Northbridge Financial, Crum & Forster, Zenith National, Odyssey Group, and Brit contribute significantly to the company's geographical presence. These entities provide a range of insurance and reinsurance solutions. The success of these subsidiaries is critical to the company's overall performance.

Financial Performance

In 2024, Odyssey Group's net premiums written were US$5,895.0 million, Brit's were US$3,156.8 million, Allied World's were US$5,049.1 million, Crum & Forster's were US$4,233.7 million, Zenith National's were US$741.6 million, and Northbridge's were Cdn$3,049.5 million (approximately US$2,226 million). These figures highlight the financial strength and market penetration of the company's subsidiaries.

Strategic Acquisitions

The company's acquisitions, such as Gulf Insurance Group in 2023 and the increased ownership in Brit in December 2024, have expanded its geographical footprint. These strategic moves have significantly boosted gross and net premiums written. These acquisitions enhance the company's ability to serve its target market.

Market Segmentation

The company's subsidiaries focus on different segments within the insurance and reinsurance markets. This approach allows for a targeted strategy to reach the right customer demographics. This segmentation strategy helps the company tailor its offerings to specific customer needs.

Customer Needs

The company's decentralized structure enables its subsidiaries to address the specific needs and preferences of their local customer bases. This localized approach ensures that products and services are relevant to each region. Understanding customer needs is essential for the company's success.

Market Analysis

The company's geographical distribution of sales indicates a strong presence in North America, with significant contributions from its Canadian and U.S. insurance operations. The company is also expanding its international presence through global reinsurance and specialty insurance providers. For more information on the company's structure, you can review Owners & Shareholders of Fairfax.

- The company's operations are spread across North America, Europe, Asia, and Latin America.

- Strategic acquisitions and investments have solidified its presence in key markets.

- The decentralized structure allows subsidiaries to adapt to local market conditions.

- The company's financial performance is supported by key subsidiaries.

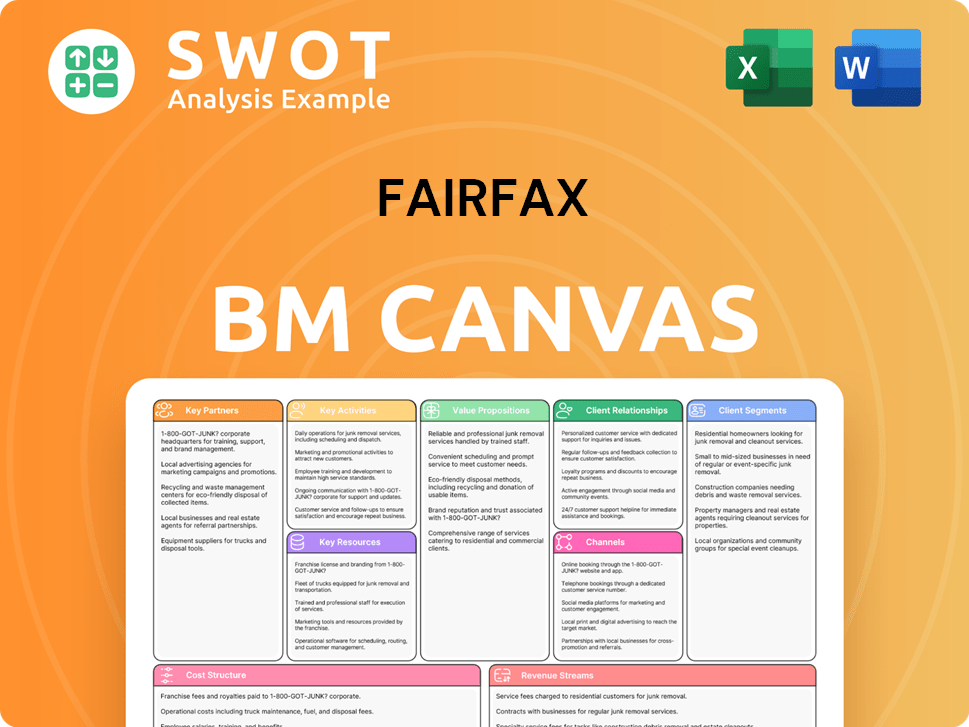

Fairfax Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does Fairfax Win & Keep Customers?

The customer acquisition and retention strategies of Fairfax Financial Holdings Limited are primarily executed at the subsidiary level due to its decentralized operational model. This approach allows each subsidiary to tailor its strategies to its specific customer base and market conditions. A key element of their strategy, especially in property and casualty insurance and reinsurance, is built on strong underwriting performance and financial stability, which are attractive to businesses seeking reliable risk partners.

Fairfax's success in customer acquisition is evident in its strategic acquisitions and disciplined underwriting. The company's record underwriting profit of $1.8 billion in 2024 and a consolidated combined ratio of 92.7% demonstrate its commitment to profitable underwriting. This financial strength and operational efficiency are crucial for attracting and retaining customers in the competitive insurance and reinsurance markets. The company also focuses on expanding its client base and ensuring profitable growth from existing clients.

Retention strategies focus on providing consistent service, maintaining strong reserves, and ensuring favorable claims development. The company's commitment to 'soundly financed' operations and 'prudent reserving practices' helps build long-term trust and loyalty with its clients. Fairfax reported favorable reserve development of $594 million in 2024, further indicating its ability to meet future obligations. While specific loyalty programs are not typically highlighted in public reports for its B2B insurance operations, the decentralized nature allows each subsidiary to foster relationships and tailor service to its specific customer needs.

Key Acquisition Strategies

Fairfax employs several strategies to acquire customers, especially in its insurance and reinsurance businesses. These include direct sales forces and brokers, as well as building strong relationships with large corporate clients. Acquisitions also play a crucial role in expanding the customer base, as demonstrated by the 2023 acquisition of Gulf Insurance and the 2024 acquisition of Sleep Country Canada.

- Direct Sales and Broker Networks: Utilize direct sales teams and broker networks to reach potential clients.

- Strategic Acquisitions: Acquire companies to expand customer base and market presence.

- Focus on Underwriting Performance: Maintain strong underwriting to attract and retain clients.

- Expand Client Base: Focus on both expanding its client base and ensuring profitable growth from existing clients.

Financial Stability

Fairfax’s financial stability is a cornerstone of its customer retention strategy. The company's strong financial performance, including a record underwriting profit of $1.8 billion in 2024, instills confidence in its clients. This financial health is further supported by prudent reserving practices and favorable claims development.

Decentralized Approach

The decentralized operating model allows each subsidiary to tailor its customer acquisition and retention strategies. This flexibility enables them to respond effectively to the specific needs of their customer base. This approach allows for more personalized service and relationship management.

Customer Data and CRM Systems

Customer data and CRM systems are implied in the operations of its various subsidiaries. This helps in managing policyholder information and claims. However, specific details on their utilization for targeted campaigns or segmentation are not publicly detailed.

Long-Term Value Creation

Fairfax’s overall strategy emphasizes long-term value creation and disciplined underwriting. This approach inherently supports customer retention by providing a stable and reliable partner in risk management. The company's ongoing focus on increasing interest and dividend income, which reached $2.5 billion in 2024, also contributes to its financial strength.

Shareholder Value

Share buybacks, such as the purchase of 1,346,953 subordinate voting shares for cancellation in 2024 for approximately $1.6 billion, enhance shareholder value. This aligns with Fairfax’s long-term objectives and financial stability, indirectly benefiting customers.

Focus on Underwriting Profitability

Fairfax aims to maintain a combined ratio in the mid-90s, demonstrating its commitment to profitable underwriting. This focus on profitability ensures the company can meet its obligations to policyholders and maintain a strong financial position, which is crucial for customer retention. The company's record underwriting profit of $1.8 billion in 2024 is a testament to this strategy.

For more detailed insights into the company's financial performance and strategic initiatives, you can refer to a comprehensive analysis of Fairfax's business model.

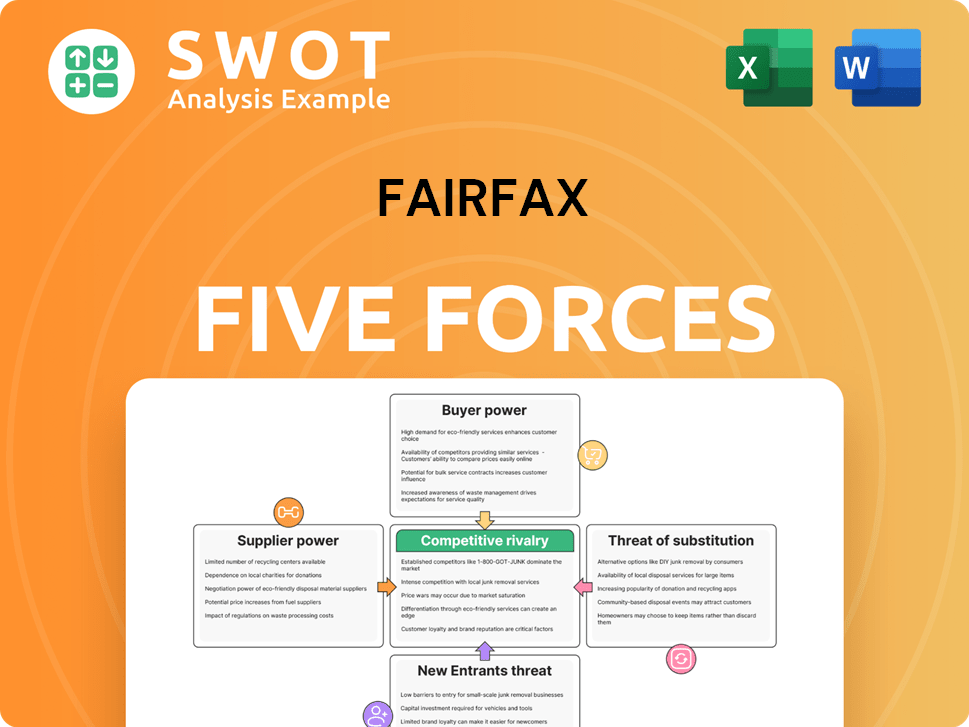

Fairfax Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Fairfax Company?

- What is Competitive Landscape of Fairfax Company?

- What is Growth Strategy and Future Prospects of Fairfax Company?

- How Does Fairfax Company Work?

- What is Sales and Marketing Strategy of Fairfax Company?

- What is Brief History of Fairfax Company?

- Who Owns Fairfax Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.