Blue Ridge Bank Bundle

Who Does Blue Ridge Bank Serve?

In today's fast-paced financial world, understanding the heart of any successful bank lies in its customers. For Blue Ridge Bank, navigating the evolving needs of its Blue Ridge Bank SWOT Analysis is paramount. This analysis dives deep into the bank's customer demographics and target market, revealing crucial insights for strategic decision-making. Discover how Blue Ridge Bank adapts to meet the demands of its diverse customer base.

This exploration into Blue Ridge Bank's customer demographics and target market is essential for anyone seeking to understand the bank's growth potential. We'll examine the Bank customers profile, including their age range, income levels, and geographic location. This market analysis will also provide valuable insights into Blue Ridge Bank's ability to deliver effective financial services and capture its ideal customer.

Who Are Blue Ridge Bank’s Main Customers?

Understanding the primary customer segments is crucial for any financial institution. For Blue Ridge Bank, this involves a dual focus on both consumers and businesses. Analyzing the customer demographics and target market allows for tailored financial services and effective market analysis.

The bank's strategy centers on serving a diverse range of customers. This includes individuals seeking traditional banking services, as well as small to medium-sized businesses (SMBs). This approach ensures a comprehensive financial partnership within its operational areas. The customer segmentation strategy is designed to meet the varied financial needs of its community.

By catering to both consumer and business segments, the bank aims to create a balanced portfolio. This strategy helps in building a strong local economy. The bank's focus on customer needs is a key driver of its market research and customer acquisition strategy.

The consumer segment of the bank includes individuals from various age groups. These individuals often seek traditional banking services with convenient digital access. The bank's customer profile typically includes local residents, families, retirees, and working professionals. These customers value personalized service and local branch accessibility.

The business segment focuses on small to medium-sized businesses (SMBs). These SMBs span various industries, including retail, services, light manufacturing, and real estate. They require commercial deposit products, loan products, and potentially treasury management services. The decision-makers are typically local entrepreneurs and business owners.

Key Demographics and Needs

The bank's target audience is diverse, reflecting the communities it serves. Customer demographics include a wide range of ages, income levels, and occupations. The bank's customer needs vary, from everyday banking to specialized business financing.

- Age Range: Spans all age groups, with a focus on those seeking long-term financial partnerships.

- Income Levels: Caters to a broad spectrum, aiming to provide services for all income brackets.

- Geographic Location: Primarily serves local residents and businesses within its operational footprint.

- Customer Needs: Offers a range of services, including checking and savings accounts, loans, and business financing.

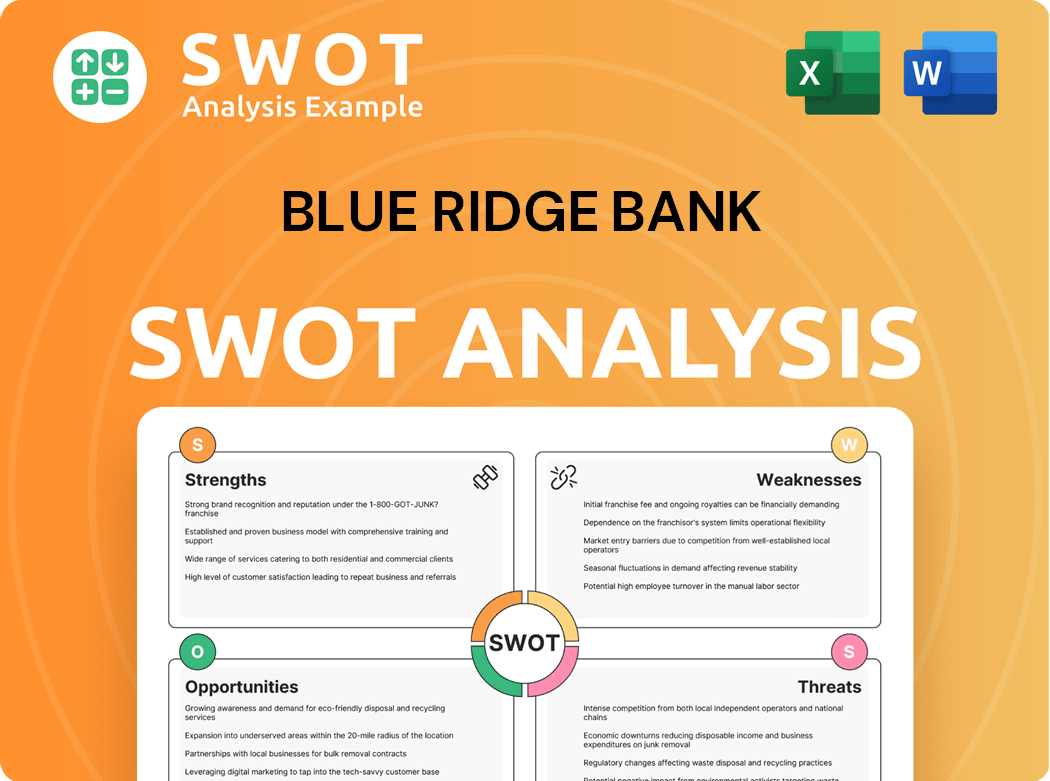

Blue Ridge Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do Blue Ridge Bank’s Customers Want?

Understanding the needs and preferences of its customer demographics is crucial for success. This involves a deep dive into the target market, analyzing what drives their financial decisions and how the bank can best meet those needs. By focusing on these elements, the bank can refine its services and maintain a competitive edge in the financial services sector.

For Blue Ridge Bank, this means providing solutions that resonate with both individual and business clients. The goal is to build lasting relationships by addressing their unique requirements, whether it's convenient banking options or tailored financial strategies. This customer-centric approach is essential for driving growth and ensuring customer loyalty.

The bank's success hinges on its ability to adapt and innovate, staying ahead of evolving customer expectations and market trends. This proactive stance ensures it remains relevant and continues to meet the diverse needs of its customer base.

Individual Customer Needs

Individual bank customers seek convenience, competitive rates, and user-friendly digital platforms. They value trust, reputation, and responsive customer service. Product usage includes checking, savings, and credit products.

Key Motivations

Customers are motivated by financial security and a local banking relationship. Practical drivers involve competitive rates and accessible services. The desire is for accessible credit and secure financial management.

Pain Points Addressed

The bank addresses pain points such as the need for accessible credit, secure financial management, and personalized financial advice. This is achieved through user-friendly digital solutions and personalized services.

Business Customer Needs

Business clients require efficient cash management, flexible lending, and specialized advice. Decision-making is influenced by industry understanding and loan approval speed. Products include business accounts and lines of credit.

Loyalty Factors

Loyalty for businesses is built on strong relationships and proactive problem-solving. The bank supports growth through tailored solutions. This includes dedicated relationship managers and customized loan options.

Adaptation and Innovation

Market analysis and customer feedback drive product development. This leads to improved online and mobile banking. The bank adapts to the increasing demand for digital solutions.

The bank's ability to understand its customer demographics and tailor its services accordingly is a key factor in its success. For example, in 2024, digital banking adoption rates among adults in the U.S. reached approximately 60%, highlighting the need for robust digital platforms. Furthermore, according to a 2024 report by the American Bankers Association, customer satisfaction with online banking services remains high, with an average satisfaction score of 80%. To learn more about the financial aspects of the bank, you can read about the Revenue Streams & Business Model of Blue Ridge Bank.

Key Strategies

The bank focuses on personalized services and digital enhancements to meet customer needs. This includes offering tailored loan solutions and developing user-friendly digital tools.

- Dedicated relationship managers for businesses.

- Customized loan solutions.

- Digital tools for commercial clients, such as online bill pay.

- Robust treasury management platforms.

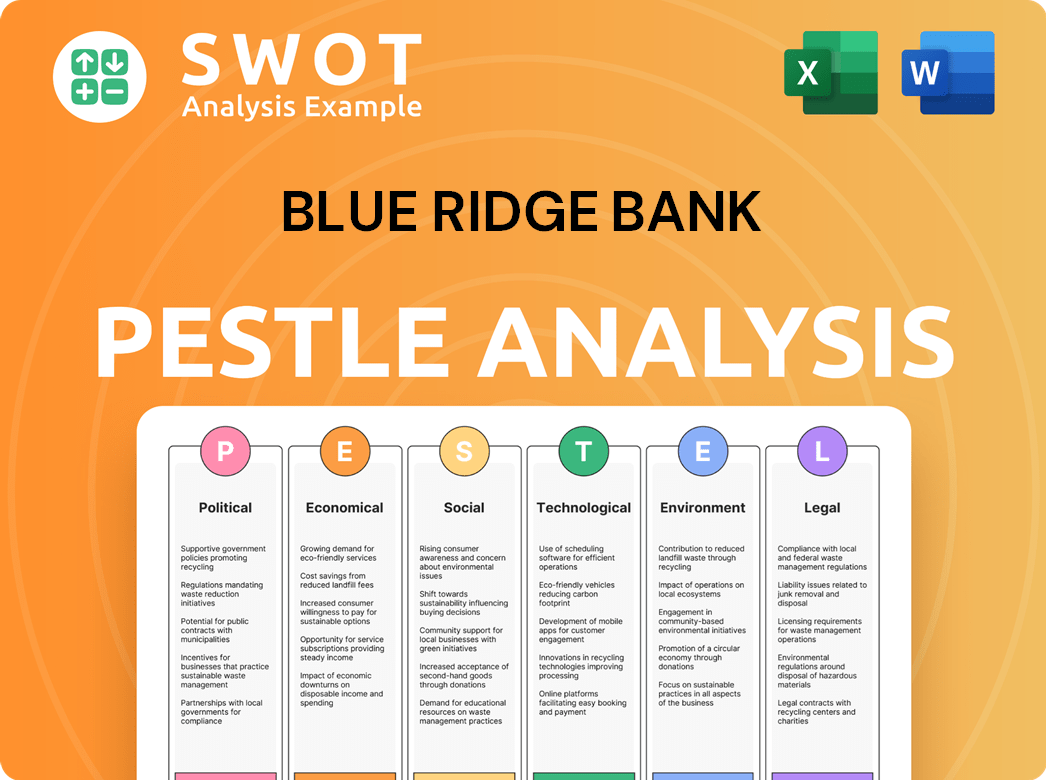

Blue Ridge Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does Blue Ridge Bank operate?

The geographical market presence of the [Company Name] centers on specific regions within the United States, with a focus on establishing a strong local presence. As a community bank, its primary market share and brand recognition are typically strongest in the counties and towns where its branches are located. This often includes areas within Virginia and potentially neighboring states where it has expanded its footprint. The bank's strategic decisions regarding branch locations and service areas are driven by market opportunities and growth initiatives.

Understanding the nuances of the local market is crucial for [Company Name]. This involves tailoring products and services to the specific economic activities and demographics of each community. For instance, rural areas may have a higher demand for agricultural loans, while suburban or urban areas might see greater demand for mortgage lending or small business loans. This localized approach allows the bank to better serve its customer demographics and meet the financial needs of each region.

The bank's target market is defined by its geographic footprint and the specific needs of the communities it serves. This includes offering specialized loan programs for local industries, participating in community events, and employing local staff who understand the regional market. Any recent expansions or strategic withdrawals are driven by market opportunity, competitive landscape, and the bank's strategic growth initiatives. The geographic distribution of sales and growth directly correlates with the economic vitality and population density of its primary service areas. For more details, you can refer to the Marketing Strategy of Blue Ridge Bank.

Customer Segmentation

The bank likely segments its customer base based on geographic location, income levels, and financial needs. This allows for the creation of targeted marketing campaigns and product offerings. Understanding Blue Ridge Bank customer profile is key to effective market penetration.

Geographic Focus

The bank's primary focus is on communities within Virginia and potentially neighboring states. This geographic concentration allows for better relationship-building and understanding of local market dynamics. The Blue Ridge Bank geographic location is a key factor in its success.

Market Analysis

Regular market analysis is essential to identify opportunities and adapt to changing customer needs. This includes assessing the competitive landscape and understanding the economic trends within its service areas. This helps define the Best target market for Blue Ridge Bank.

Product and Service Tailoring

The bank tailors its products and services to meet the specific needs of each community it serves. This could involve offering specialized loan programs for local industries or providing financial education resources. This ensures that Blue Ridge Bank customer needs are met effectively.

Customer Acquisition

The bank likely employs a customer acquisition strategy that focuses on building relationships within the community. This includes participating in local events, supporting community initiatives, and leveraging the knowledge of its local staff. This helps in identifying the Blue Ridge Bank ideal customer.

Economic Indicators

The bank's geographic distribution of sales and growth directly correlates with the economic vitality and population density of its primary service areas. This means that areas with stronger economic indicators will likely see greater growth for the bank. Analyzing Demographic data for Blue Ridge Bank is key.

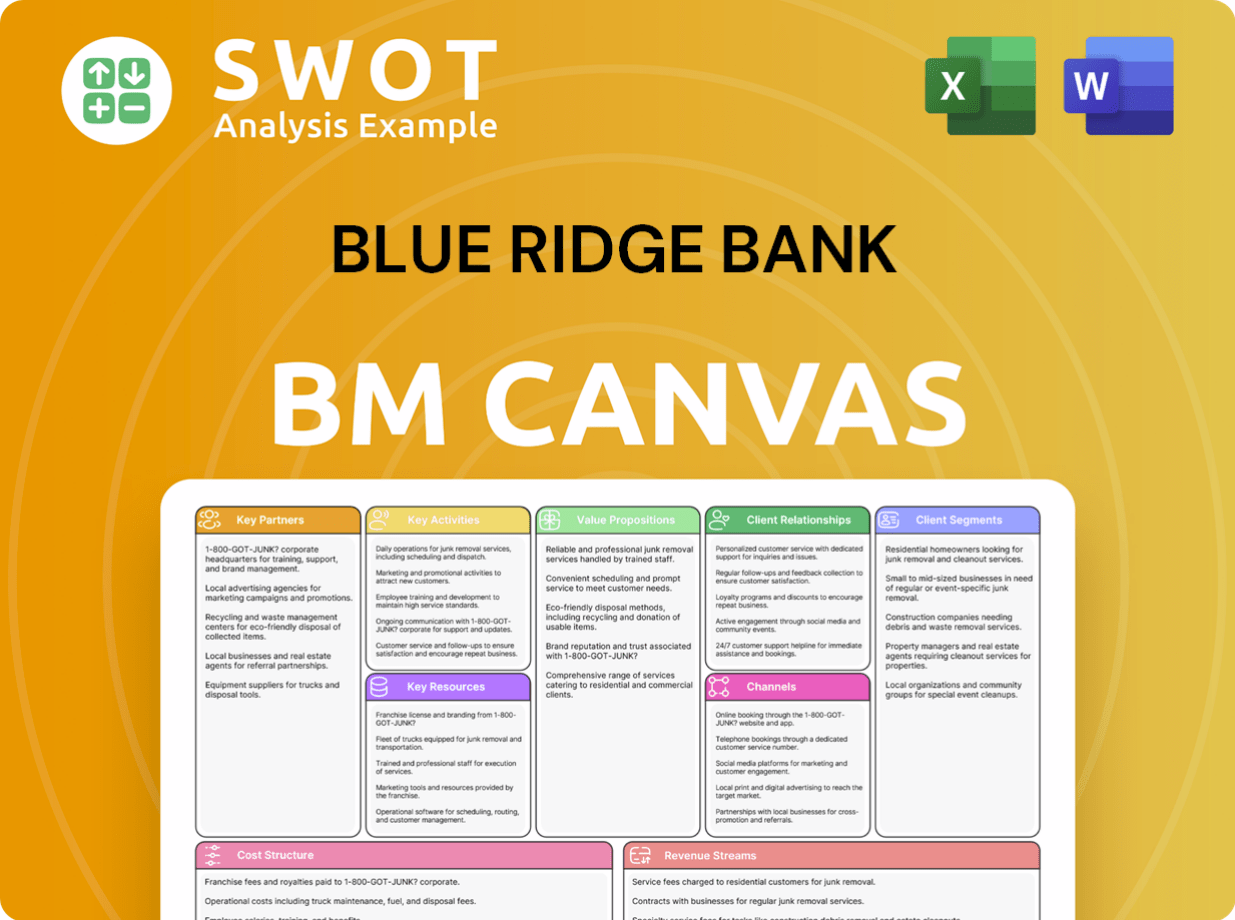

Blue Ridge Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does Blue Ridge Bank Win & Keep Customers?

Acquiring and retaining customers is crucial for the success of any financial institution, including community banks. The bank employs a multifaceted strategy to attract new customers and keep existing ones. These strategies blend traditional methods with digital approaches to reach a wide audience and build strong, lasting relationships. This approach is vital for ensuring the bank's sustained growth in a competitive market.

The acquisition strategy focuses on both local and digital channels. Traditional marketing includes local advertising through community newspapers, radio, and sponsorships of local events. Digitally, the bank uses search engine optimization (SEO), pay-per-click (PPC) advertising, and social media marketing. Referral programs are also a key tactic, leveraging customer trust. Sales tactics involve relationship banking, where representatives engage with potential customers to understand their needs and offer tailored solutions. The goal is to attract a diverse customer base and build a strong presence in the community.

Retention strategies center on building strong customer relationships and delivering exceptional service. Loyalty programs, personalized experiences, and after-sales service are key components. The bank focuses on responsive customer support through various channels, including in-branch, phone, and digital messaging. This comprehensive approach aims to enhance customer loyalty, increase lifetime value, and reduce churn rates, ultimately driving sustainable growth for the bank.

The bank uses a mix of traditional and digital channels. This includes local advertising, search engine optimization (SEO), pay-per-click (PPC) advertising, and social media marketing. Referral programs and relationship banking are also key elements of their acquisition strategy. These diverse channels help reach a broad audience.

Relationship banking involves bank representatives actively engaging with potential customers. The goal is to understand their financial needs and offer tailored solutions. This approach fosters trust and builds long-term relationships. It is particularly effective for attracting and retaining customers.

Retention strategies focus on building strong customer relationships. This includes loyalty programs, personalized experiences, and after-sales service. Customer Relationship Management (CRM) systems are used to track customer interactions and preferences. The bank aims to provide responsive customer support across multiple channels.

Investment in mobile banking apps and online account opening capabilities is a key trend. These digital initiatives improve customer experience and streamline processes. They also help the bank stay competitive in the evolving financial landscape. Digital banking is essential for both acquisition and retention.

The evolution of the bank's strategy over time reflects the changing financial landscape. An increased focus on mobile banking apps and online account opening capabilities signals a shift towards digital acquisition and retention. Successful acquisition campaigns highlight the bank's local advantage and personalized service. Innovative retention initiatives include financial literacy programs or specialized advisory services for small businesses. These strategies directly impact customer loyalty, lifetime value, and churn rate, fostering long-term relationships. For more insights, you can check out the Competitors Landscape of Blue Ridge Bank.

Local Advertising

The bank uses local advertising through community newspapers and radio. Sponsorships of local events also play a role. This approach helps the bank connect with its community and build brand recognition. It is a cost-effective way to reach the target market.

Digital Marketing

Digital marketing includes SEO, PPC advertising, and social media marketing. These channels are used to reach a broader audience and attract digitally-savvy customers. Effective digital marketing helps drive online traffic and generate leads. The bank likely allocates a significant portion of its marketing budget to digital channels.

Referral Programs

Referral programs incentivize existing customers to bring in new ones. This tactic leverages trust and word-of-mouth marketing. Satisfied customers are a valuable source of new business. These programs are often highly effective for community banks.

Customer Relationship Management (CRM)

CRM systems are used to track customer interactions, preferences, and financial needs. This data enables targeted communication and proactive service. CRM helps the bank personalize the customer experience. Effective CRM improves customer satisfaction and loyalty.

After-Sales Service

After-sales service, particularly for loan products, involves ongoing support and communication. This ensures customer satisfaction and builds long-term relationships. Providing excellent after-sales service reduces churn. It is a key component of the bank's retention strategy.

Financial Literacy Programs

Financial literacy programs can be part of the bank's retention strategy. These programs educate customers and build trust. They help customers make informed financial decisions. Such programs can enhance customer loyalty.

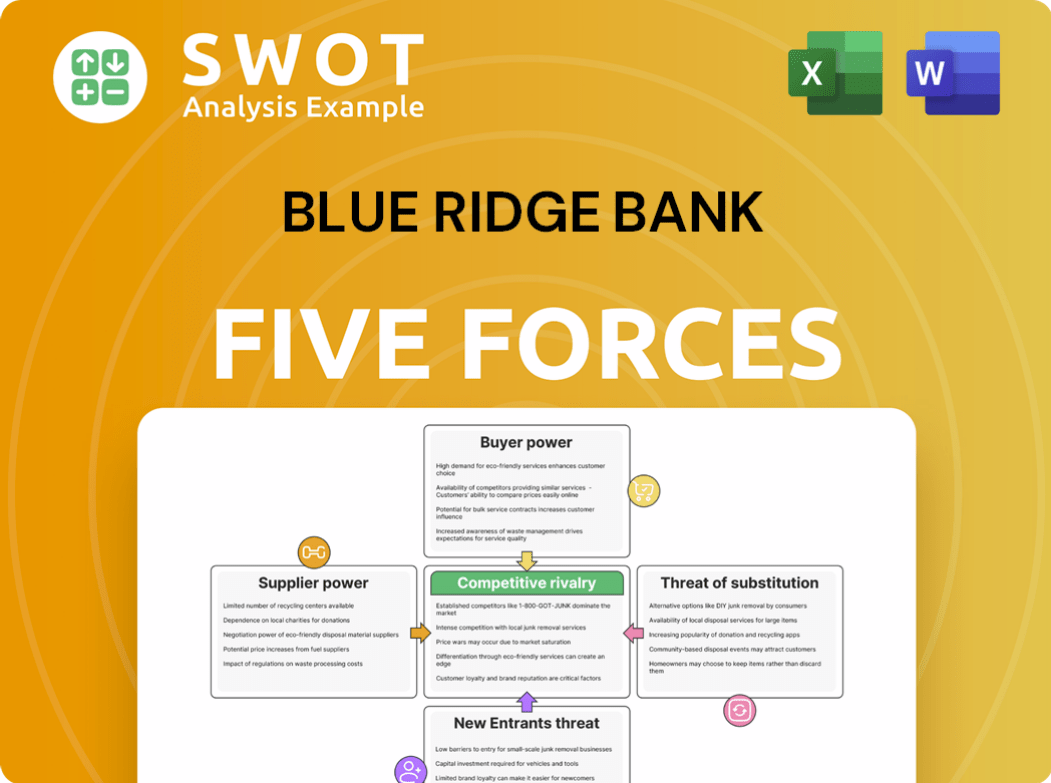

Blue Ridge Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Blue Ridge Bank Company?

- What is Competitive Landscape of Blue Ridge Bank Company?

- What is Growth Strategy and Future Prospects of Blue Ridge Bank Company?

- How Does Blue Ridge Bank Company Work?

- What is Sales and Marketing Strategy of Blue Ridge Bank Company?

- What is Brief History of Blue Ridge Bank Company?

- Who Owns Blue Ridge Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.