CFO Bundle

Who Really Owns CFOS?

Unraveling the ownership structure of a company is the first step toward understanding its strategic direction and financial health. In the dynamic vocational training sector, where government reforms and market growth reshape the landscape, knowing who owns CFOS—Centro de Formação Oliveira de São—is more critical than ever. This knowledge provides a crucial lens through which to view its operations, accountability, and long-term viability.

This exploration into CFO SWOT Analysis will delve into the ownership of CFOS, examining its founder's initial stakes, key investors, and any shifts in its structure. Understanding the CFO company ownership is essential for anyone conducting due diligence on CFO company ownership, or assessing CFO company investment opportunities, especially within a sector projected for significant growth. The analysis will also touch upon the CFO company legal structure and the influence of the CFO company board of directors.

Who Founded CFO?

Determining the specific founders and initial ownership structure of a company like Centro de Formação Oliveira de São (CFOS) requires looking at the vocational training sector. Information on the founders and the exact equity split at the start of CFOS isn't publicly available. However, understanding how similar organizations are formed can offer insights into the potential early ownership dynamics.

In the vocational training field, the formation often involves individuals or groups focused on skills development and professional advancement. For instance, CFAE AVCOA, established in 2008, resulted from consolidating existing training centers. This suggests that CFOS might have been created through a similar restructuring or merger of existing educational initiatives, rather than a single founding event with a clear equity distribution among individuals. Understanding the background of the founding team is key to understanding the company's vision and direction.

Early backing for vocational training centers can come from various sources, including government funding and private investment. The U.S. government, for example, allocated $1,470.0 million in FY 2024 for career and technical education. Private centers, which make up the majority, often rely on private investment.

Founders

The founders of a CFO company are typically individuals with expertise in CFO services, financial management, and corporate finance. They may have backgrounds in accounting, finance, or business management. Identifying the founder of a CFO company can be crucial for due diligence on CFO company ownership.

Early Ownership

Early ownership in a CFO company often involves the founders and possibly angel investors or early backers. The initial equity split is determined based on the contributions of each party. Agreements like vesting schedules and buy-sell clauses are common in private company formations to manage ownership.

Investment

CFO company investment can come from various sources, including private equity ownership of CFO firms. Understanding the investment history can provide insights into the company's financial stability and growth potential. Identifying the CEO of a CFO company is crucial for understanding the leadership structure.

Legal Structure

The CFO company's legal structure, such as a sole proprietorship, partnership, or corporation, determines the ownership and liability. The legal structure impacts how the company is managed and how profits are distributed. Due diligence on CFO company ownership includes examining the legal structure.

Board of Directors

The CFO company's board of directors oversees the management and strategic direction of the company. The board's composition and expertise can significantly impact the company's performance. Understanding the board of directors provides insights into the company's governance.

Management Team

The CFO company's management team, including the CEO, CFO, and other executives, plays a crucial role in the company's operations and success. The management team's experience and track record are essential for assessing the company's potential. Analyzing the CFO company management team is part of the due diligence process.

Early ownership agreements often include clauses like vesting schedules and buy-sell agreements. These help manage ownership and control, especially during the company's initial growth. The founding team's vision, even if not explicitly detailed for CFOS, would typically be reflected in the initial curriculum and target audience, aiming to address specific skill gaps and employability needs, a core objective of vocational training. To learn more about the strategic direction of a CFO company, you can explore the Growth Strategy of CFO.

Key Considerations

Understanding the ownership structure of a CFO company involves several key elements.

- Identifying the founders and their backgrounds.

- Examining the initial equity split and any subsequent changes.

- Assessing the legal structure of the company.

- Reviewing the board of directors and management team.

- Understanding the investment history and potential private equity ownership.

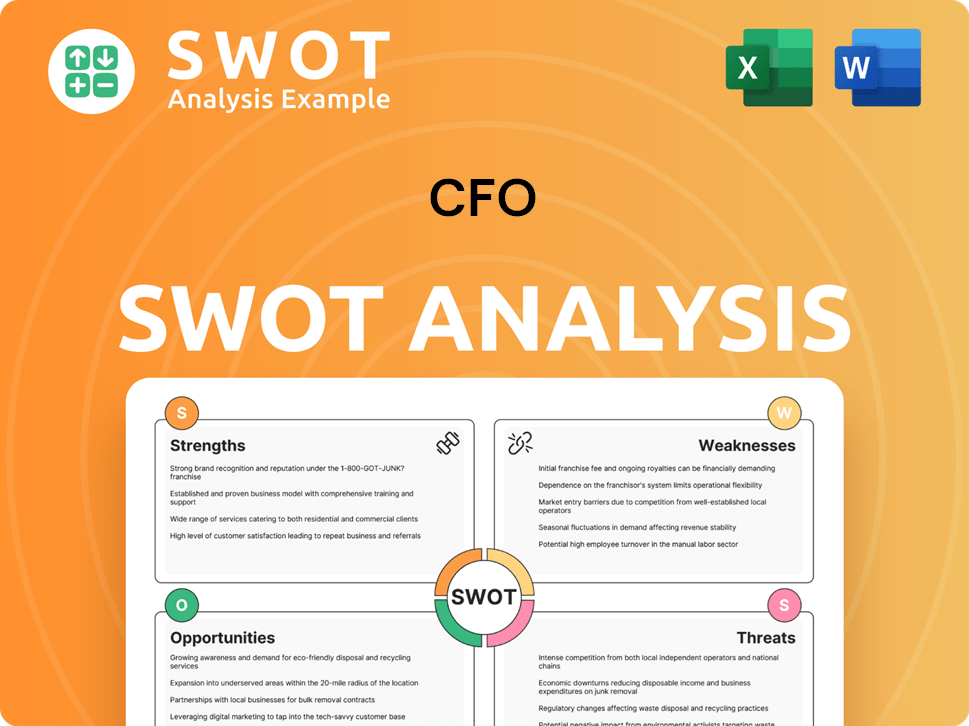

CFO SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Has CFO’s Ownership Changed Over Time?

While specific details on the ownership evolution of Centro de Formação Oliveira de São (CFOS) aren't available in the search results, we can analyze general trends in the vocational training sector to understand potential ownership structures. The vocational training market is substantial, valued at approximately US$388.1 billion in 2024. This growth is projected to reach US$648.9 billion by 2030, indicating significant investment opportunities. This expansion often leads to changes in ownership as companies seek to capitalize on market growth and adapt to evolving industry needs. Key stakeholders include private entities, and investment from private equity firms is common, especially in private vocational training centers, which make up a large portion of the market.

The vocational education market's private segment is anticipated to grow at a Compound Annual Growth Rate (CAGR) of about 12.25% from 2024 to 2032. This growth is driven by the demand for specialized and industry-aligned training. These shifts can lead to changes in equity allocation as new investors or partners come on board to support strategic growth or technological integration. Understanding the ownership structure of a CFO company, or any vocational training center, often involves looking at the influence of various stakeholders, including private equity firms, individual shareholders, and potentially, in some cases, the impact of mergers and acquisitions. For more insights on the target market, consider reading about the Target Market of CFO.

| Stakeholder Type | Typical Involvement | Impact on Ownership |

|---|---|---|

| Private Equity Firms | Investment, strategic guidance, operational improvements | Significant equity stakes, potential for mergers and acquisitions |

| Individual Shareholders | Founders, key executives, early investors | Control through direct ownership, influence on strategic direction |

| Government and Regulatory Bodies | Setting standards, providing funding, overseeing compliance | Indirect influence through regulations and funding requirements |

Changes in the ownership of a CFO company or a vocational training center are often influenced by the need to adapt to evolving workforce demands and technological advancements. Increased employer ownership and responsibility for skills development are also driving changes, with a focus on aligning skills investment with business strategy. The legal structure of the CFO company, whether it's a private entity or potentially part of a larger corporate structure, will also impact the ownership dynamics and the roles of the board of directors and management team. Due diligence on a CFO company's ownership structure is critical for understanding its strategic direction and financial stability.

CFO Company Ownership Insights

Understanding CFO company ownership involves identifying key stakeholders and their influence.

- Private equity firms often invest in CFO services.

- Individual shareholders can include founders and key executives.

- The legal structure of the company impacts ownership dynamics.

- Due diligence is crucial for assessing ownership.

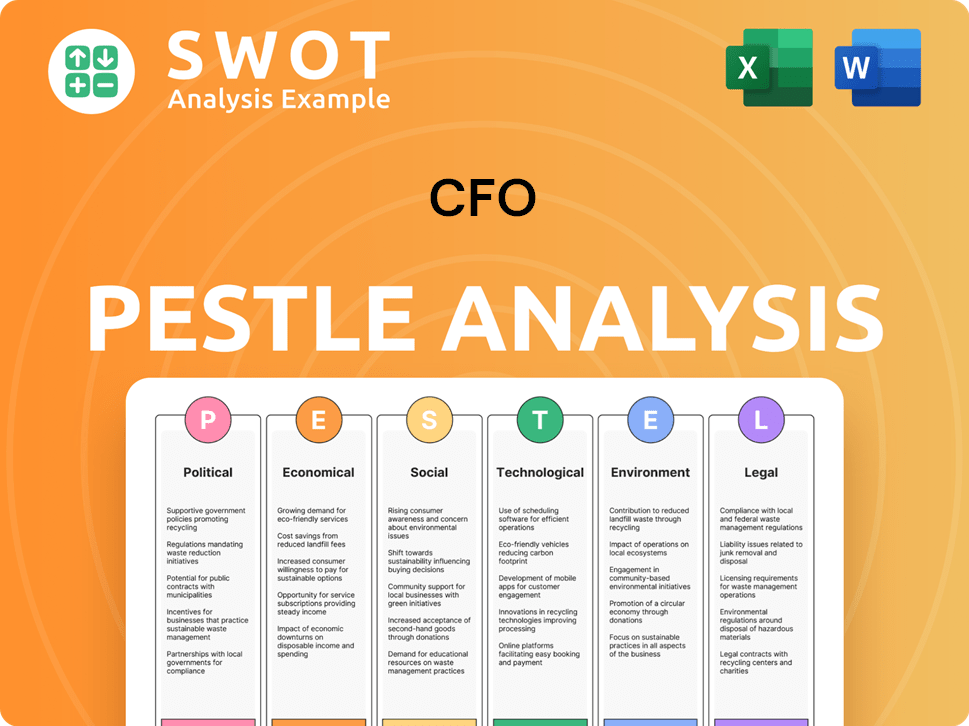

CFO PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Who Sits on CFO’s Board?

Specific information about the current board of directors of Centro de Formação Oliveira de São (CFOS) is not publicly available. Generally, in the context of educational institutions and vocational training centers, the board of directors is responsible for strategic oversight and governance. Board members often include representatives from various stakeholders, such as educational professionals, industry experts, and potentially government liaisons, reflecting the collaborative nature of the vocational education ecosystem.

The board's role is crucial for ensuring the center's alignment with its mission and the needs of its stakeholders. Effective board leadership, risk management, and ethical decision-making are essential for the success of any organization, including vocational training centers. The increasing focus on corporate governance in the broader business world highlights the importance of these aspects.

| Aspect | Details | Relevance to CFOS |

|---|---|---|

| Board Composition | Typically includes educational professionals, industry experts, and government representatives. | Ensures diverse perspectives and relevant expertise for strategic decision-making. |

| Governance Structure | Often involves a division of responsibility and decision-making power. | Influences how CFOS is managed and how decisions are made. |

| Stakeholder Representation | Reflects the collaborative nature of the vocational education ecosystem. | Ensures that the interests of all stakeholders are considered. |

Voting structures typically involve one-share-one-vote for most companies. Governance controversies can arise in any organization, particularly concerning strategic direction or financial management. The emphasis on 'co-ownership' of learning and development between HR and business units underscores the importance of shared accountability in achieving organizational capability and business strategy alignment within training contexts.

Understanding Board of Directors and Voting Power

The board of directors plays a crucial role in the governance of CFOS, overseeing strategic direction and ensuring accountability. The voting structure within the organization determines how decisions are made and who has the power to influence them. Understanding these aspects is vital for anyone interested in the CFO company ownership.

- Board members often include representatives from various stakeholders.

- Voting structures can vary, impacting decision-making power.

- Governance controversies can arise, highlighting the importance of effective oversight.

- Shared accountability is key for achieving organizational goals.

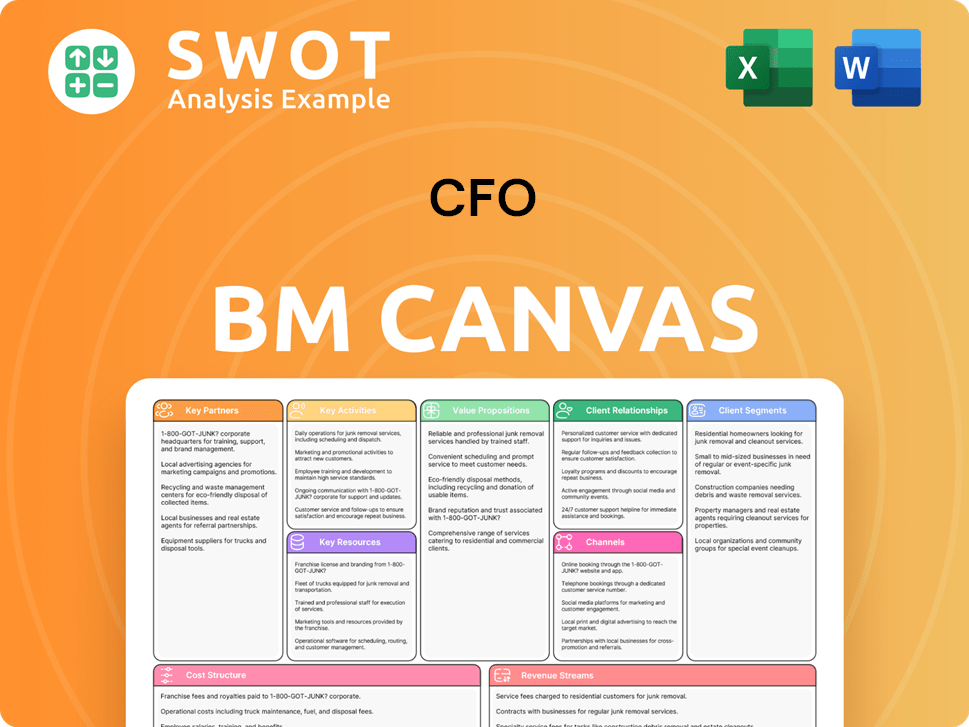

CFO Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Recent Changes Have Shaped CFO’s Ownership Landscape?

Recent developments in the vocational training sector, which directly impact the ownership of companies providing CFO services, are driven by technological advancements and evolving workforce needs. The global vocational training market is projected to grow from USD 42.87 billion in 2024 to USD 119.91 billion by 2033, with a compound annual growth rate (CAGR) of 12% from 2025 to 2033. This expansion is fueled by the increasing demand for specialized skills, such as those in automation and data analysis, leading to greater investment from both public and private sectors. This growth trend influences the Revenue Streams & Business Model of CFO companies, especially those offering financial management services.

Ownership trends show a rise in institutional ownership and potential founder dilution as companies seek larger investments for expansion and technological integration. The private segment of the technical and vocational education market is expected to grow at a CAGR of about 12.25% from 2024-2032, driven by the demand for specialized, industry-aligned training that private institutions can offer. Such shifts can lead to mergers and acquisitions, as the market consolidates to achieve greater scale and efficiency. Government reforms, like those in New Zealand where new Industry Skills Boards are being established, can also significantly alter the ownership and operational control of training providers, impacting the CFO company owner and financial structures.

From January 1, 2025, education and vocational training provided by private schools in the UK became subject to a standard 20% VAT rate, which can impact their financial models and potentially their ownership structures. The increasing integration of digitized skills into educational programs, including AI and VR systems, also influences investment and strategic partnerships within the sector, which affects the CFO company leadership structure and the need for specialized financial services.

Institutional ownership is increasing as CFO companies seek larger investments. Private equity ownership of CFO firms is growing, driven by market expansion. Mergers and acquisitions are becoming more prevalent to achieve greater scale.

Government initiatives, such as those in New Zealand, can significantly alter ownership. Tax changes, like the VAT in the UK, impact financial models. Reforms influence the CFO company's legal structure and financial planning.

Digitized skills and AI are influencing investment. Strategic partnerships are forming within the sector. These changes affect the CFO company's management team and operations.

Changes in ownership affect CFO services demand. The demand for financial management is increasing. Due diligence on CFO company ownership is becoming more critical.

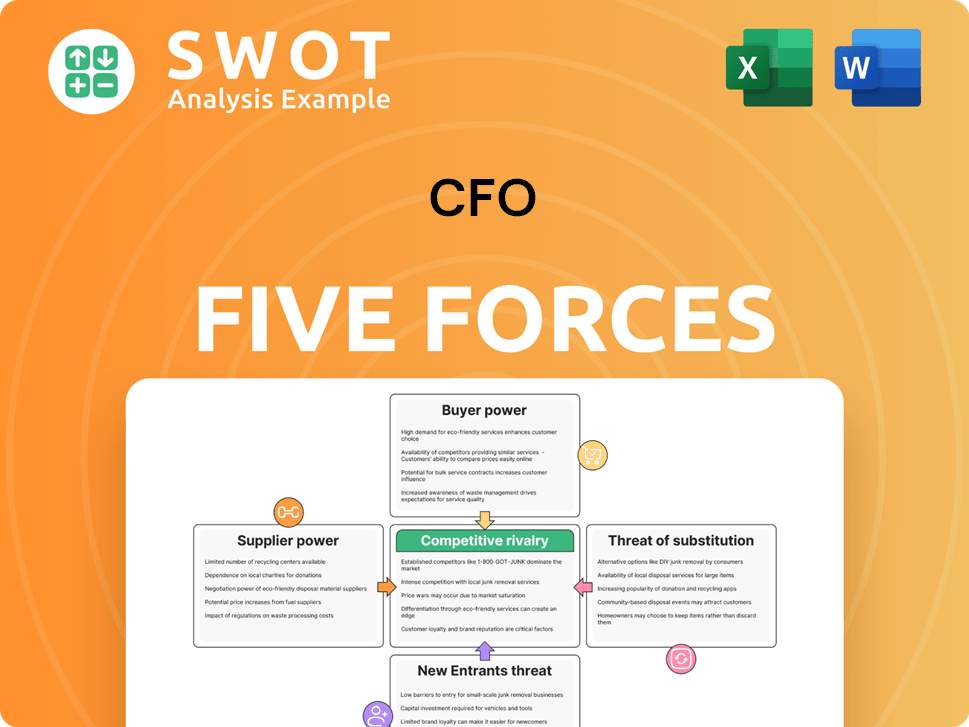

CFO Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of CFO Company?

- What is Competitive Landscape of CFO Company?

- What is Growth Strategy and Future Prospects of CFO Company?

- How Does CFO Company Work?

- What is Sales and Marketing Strategy of CFO Company?

- What is Brief History of CFO Company?

- What is Customer Demographics and Target Market of CFO Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.