Weihai City Commercial Bank Bundle

How Does Weihai Bank Thrive in China's Banking Sector?

Weihai City Commercial Bank, now known as Weihai Bank (WCCB), is making waves in the Chinese financial landscape. This regional powerhouse, officially rebranded in February 2025, has a rich history of serving local communities and businesses. Its strategic expansion and commitment to digital transformation offer a compelling case study for investors and industry analysts alike.

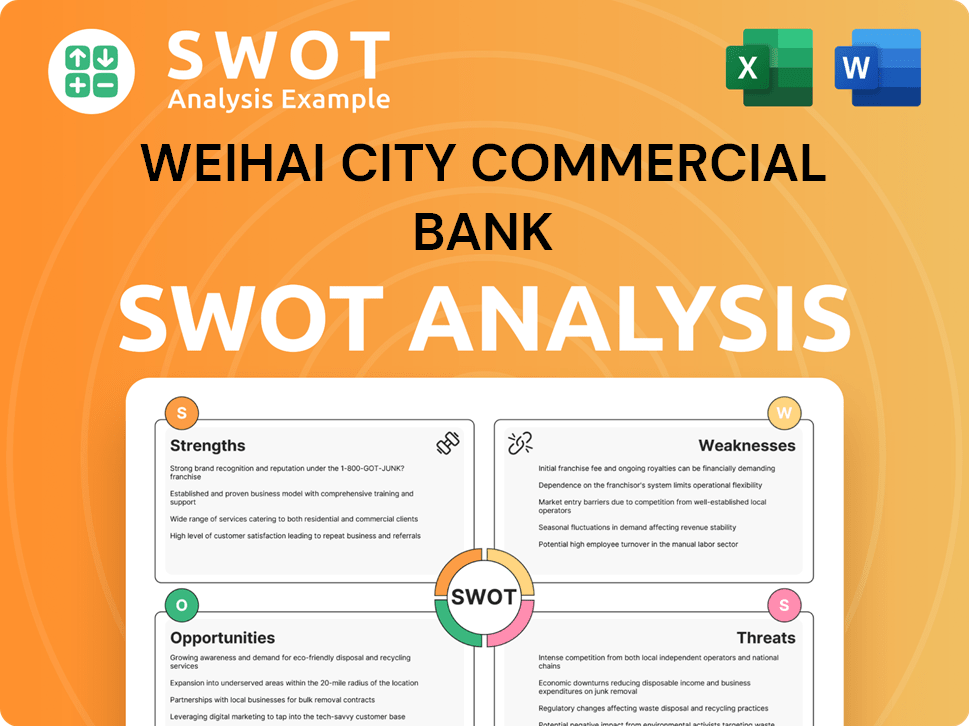

With its roots firmly planted in Shandong province since 1997, Weihai Bank has grown significantly. The bank's successful IPO on the Hong Kong Stock Exchange in 2020 further solidified its position. To gain a deeper understanding of its strengths, consider exploring the Weihai City Commercial Bank SWOT Analysis, which provides valuable insights into its competitive advantages and areas for improvement within the commercial banking sector.

What Are the Key Operations Driving Weihai City Commercial Bank’s Success?

Weihai City Commercial Bank (WCCB), also known as Weihai Bank, delivers value through a wide range of banking and financial services. Its primary focus is on serving individuals, businesses, and institutions within Shandong province and beyond. The bank's operations are strategically segmented to cater to diverse financial needs, ensuring comprehensive service delivery across various customer segments.

The core of Weihai Bank's operations is divided into three main segments: Corporate Banking, Retail Banking, and Financial Markets. Each segment is designed to offer specialized products and services tailored to the specific needs of its clientele. Through these segments, WCCB aims to provide a full spectrum of financial solutions, fostering strong customer relationships and supporting regional economic growth.

The bank emphasizes technological advancements and digital transformation to enhance operational efficiency and customer experience. This strategic direction, coupled with a robust branch network, positions Weihai Bank to effectively serve its customers and contribute to the financial landscape of the region. Partnerships and innovative financial products further enhance its value proposition.

Weihai Bank provides financial products and services to corporations, government agencies, and financial institutions. These include corporate loans, trade financing, deposit-taking, agency services, and wealth management. The bank focuses on supply chain finance and green finance innovations.

The Retail Banking segment serves individual customers with personal loans, deposit-taking, wealth management, and remittance services. Weihai Bank aims to improve customer experience through mobile, scenario-based, and intelligent transformations, enhancing accessibility and convenience for retail clients.

This segment involves inter-bank money market transactions, repurchases, investment, and debt securities trading. Weihai Bank actively participates in financial markets to manage its liquidity and investment portfolios, contributing to the stability and efficiency of the financial system.

Weihai Bank is implementing a 'smart digital bank' strategy to improve customer experience. Collaborations with FinTech firms, such as the 2023 partnership with Ant Group, aim to streamline operations. These initiatives are expected to reduce operational expenses by approximately 15% by 2024.

Key Advantages and Customer Benefits

Weihai Bank's operational strengths translate into tangible benefits for its customers, including tailored financial products and competitive interest rates. The bank's commitment to customer loyalty is also a key part of its value proposition.

- Tailored financial products designed to meet specific customer needs.

- Competitive interest rates, such as 4.5% for SME loans, approximately 0.5% lower than the industry average.

- A strong emphasis on customer loyalty programs to foster long-term relationships.

- Extensive branch network of nearly 130 branches across Shandong and presence in Tianjin.

Weihai City Commercial Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Weihai City Commercial Bank Make Money?

Weihai City Commercial Bank (WCCB), also known as Weihai Bank, generates revenue through its core business segments: Corporate Banking, Retail Banking, and Financial Markets. The bank's financial performance reflects its strategic focus on these areas, with a consistent increase in operating income driven primarily by net interest income.

In the first half of 2024, Weihai Bank's operating income rose by approximately 4.76% to around RMB4.56 billion. For the full year 2023, operating income reached approximately RMB8.74 billion, marking a 5.36% increase from RMB8.29 billion in 2022. These figures highlight the bank's ability to grow its revenue streams through effective management of its core banking activities.

The bank's monetization strategies encompass traditional banking services and innovative approaches. These initiatives aim to enhance customer loyalty, expand digital offerings, and diversify financial products. The bank's commitment to digital transformation and expansion into new financial products further strengthens its revenue generation capabilities.

Corporate Banking

In 2020, corporate banking contributed approximately 56% of the bank's operating income. This segment focuses on providing financial services to businesses, including loans, credit facilities, and other corporate banking products. The success of this segment is crucial for the overall financial health of Weihai Bank.

Retail Banking

Retail banking provides services to individual customers, including savings accounts, loans, and other retail financial products. The bank has implemented strategies to increase deposits and customer loyalty. The bank aims to increase online account openings to 50% by the end of 2024.

Financial Markets

Financial markets accounted for 20% of the operating income in 2020. This segment involves trading activities, including investments in bonds and other financial instruments. The bank's performance in this area is influenced by market conditions and its trading strategies.

Interest Income and Fees

Weihai Bank generates interest income from loans and advances, as well as fees from various services. The bank's ability to manage interest rates and service charges directly impacts its profitability. The bank's strategies include tiered savings accounts and preferential loan rates.

Digital Initiatives

Weihai Bank is leveraging digital platforms to reduce operational costs. By the end of 2024, the bank aims to reduce operational costs by 20%. This focus on digital transformation is crucial for efficiency and customer service. The bank's mobile banking app is a key component of its digital strategy.

New Financial Products

The bank has expanded into new financial products, such as green loan initiatives launched in 2022, with a target issuance of ¥1 billion in green financing. Weihai Bank is also aiming for ¥5 billion in assets under management (AUM) in wealth management services by the end of 2023. The bank's diverse offerings help attract a wider customer base.

Key Monetization Strategies

Weihai Bank employs several key strategies to generate revenue and enhance its financial performance. These strategies include leveraging digital platforms, expanding into new financial products, and forming strategic partnerships. The bank's focus on customer loyalty and operational efficiency further supports its revenue growth.

- Customer Loyalty Programs: The introduction of tiered savings accounts and preferential loan rates for loyal customers has led to a 15% increase in deposits from existing clients over the past year, managing over ¥50 billion in retail deposits.

- Digital Transformation: The bank aims to increase online account openings to 50% by the end of 2024, leveraging digital platforms to reduce operational costs by 20%.

- Green Financing and Wealth Management: Launching green loan initiatives in 2022 with a target issuance of ¥1 billion and aiming for ¥5 billion in assets under management (AUM) in wealth management services by the end of 2023.

- Fintech Partnerships: Enhancing payment solutions through partnerships with fintech platforms, resulting in a 50% increase in mobile payment transactions in the first half of 2023, totaling over ¥3 billion.

- Capital Market Activities: In November 2024, the bank successfully issued RMB2.9 billion worth of perpetual capital bonds in the national inter-bank bond market.

For a deeper understanding of the bank's strategic direction, consider reading about the Growth Strategy of Weihai City Commercial Bank.

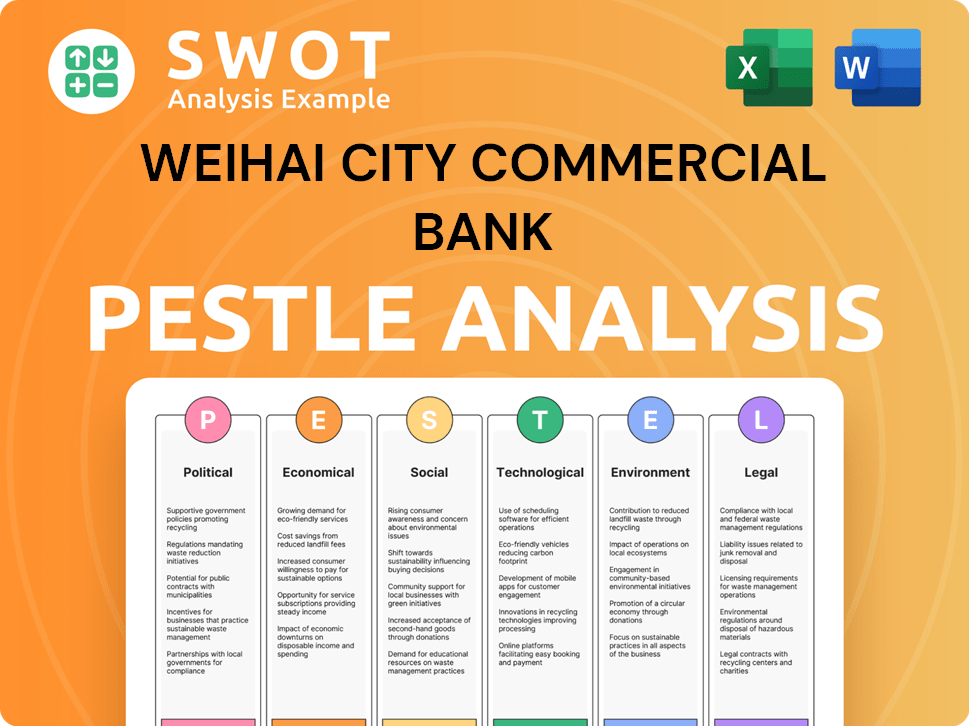

Weihai City Commercial Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Weihai City Commercial Bank’s Business Model?

Weihai Bank, formerly known as Weihai City Commercial Bank (WCCB), has marked significant milestones that have shaped its trajectory in the financial sector. Its listing on the Hong Kong Stock Exchange in October 2020 was a pivotal event, enhancing its profile and access to capital markets. The bank's strategic moves, including its early adoption of financial leasing and commitment to environmental and social responsibility, have further defined its operational approach.

The bank's evolution is also evident in its name change, officially transitioning to Weihai Bank on February 26, 2025, which reflects its evolving brand identity. This, coupled with its adherence to the 'Equator Principle' since 2021, underscores its commitment to sustainable banking practices. These initiatives highlight the bank's proactive approach to adapting to industry trends and regulatory changes.

Weihai Bank's competitive edge is rooted in its strategic initiatives and robust operational framework. Its comprehensive network across Shandong Province and presence in Tianjin provides a strong regional advantage, supported by a quality shareholder structure. The bank’s focus on digital transformation and customer-centric strategies further enhances its market position, as detailed in Growth Strategy of Weihai City Commercial Bank.

Weihai Bank listed on the Main Board of the Hong Kong Stock Exchange on October 12, 2020. It was the first financial institution in Shandong Province to establish a financial leasing company in 2016. The bank officially changed its name to Weihai Bank on February 26, 2025.

The bank adopted the 'Equator Principle' in 2021, demonstrating its commitment to environmental and social responsibility. It invested RMB 100 million in digital initiatives by 2024. The bank is also using AI for risk assessment and customer service.

A comprehensive network layout with nearly 130 branches and sub-branches across Shandong Province and in Tianjin. The bank has a quality shareholder structure. It has a featured product portfolio, particularly in corporate banking, and a 'Bi-Focus Retail Banking' strategy.

Weihai Bank invested RMB 100 million in digital initiatives by 2024. The bank is adopting AI for risk assessment and customer service. Blockchain technology is used for secure transactions.

Key Advantages

Weihai Bank's competitive strengths include its extensive branch network and strong shareholder backing. The bank's focus on corporate banking, supply chain finance, and green finance enhances its market position. Customer loyalty programs have led to an 85% retention rate.

- Extensive Branch Network: Nearly 130 branches and sub-branches.

- Strong Shareholder Support: Backing from Shandong Hi-Speed Group Company and Weihai Municipal Finance Bureau.

- Customer Retention: An 85% retention rate among existing clients.

- Digital Initiatives: Investment in AI and blockchain technologies.

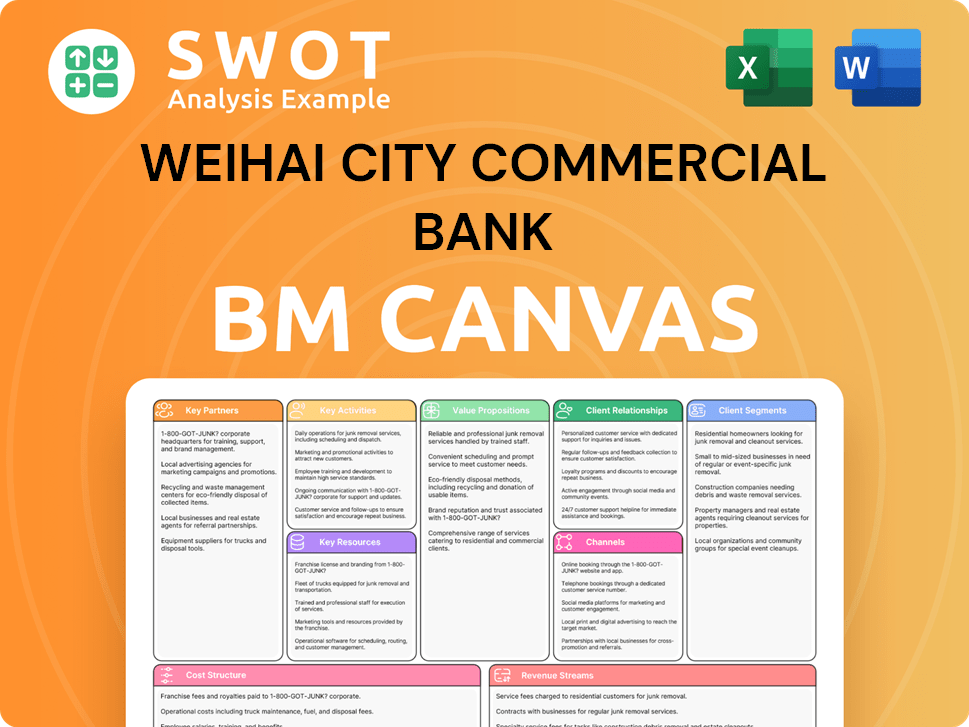

Weihai City Commercial Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Weihai City Commercial Bank Positioning Itself for Continued Success?

Weihai City Commercial Bank (WCCB) holds a significant position within the regional banking sector in China, particularly in Shandong Province. As of December 31, 2019, it was the third-largest city commercial bank in Shandong based on total assets, total deposits, and total loans. The bank has been working to increase its market share within the local banking sector.

Like all financial institutions, WCCB faces various risks, including credit risk, market risk, operational risk, and compliance risk. The broader Chinese banking industry also faces challenges such as contracting profitability and macroeconomic uncertainty. The plummeting real estate market has also put pressure on small and medium-sized banks, increasing risk-weighted assets and capital needs.

Weihai Bank is a key player in Shandong's banking sector. As of Q3 2023, it held approximately 3.5% of the total market share among local banks in Shandong. The bank's extensive branch network and focus on local economic development contribute to strong customer loyalty. As of the end of 2024, Weihai Bank's total assets reached RMB441.464 billion.

WCCB faces risks common to all financial institutions, including credit, market, operational, and compliance risks. The bank is also affected by broader industry challenges such as macroeconomic uncertainty and stricter regulatory scrutiny. The real estate market downturn adds further pressure on smaller banks.

The bank focuses on strategic initiatives to sustain and expand profitability, including a technology-driven 'Bi-Focus Retail Banking' model. It aims to enhance its strengths in supply chain finance and green finance while accelerating digital transformation in retail banking. Weihai Bank plans to allocate at least 1% of its annual profit to community development and corporate social responsibility.

Key strategies include developing a 'Bi-Focus Retail Banking' model, enhancing differentiated strengths, and promoting intensive management. The bank aims to solidify its advantages in supply chain finance and green finance and accelerate digital transformation in retail banking. Furthermore, WCCB aims to enhance the application of advanced FinTech, promoting digital model transformation to build a 'smart digital bank' with a 'first-class customer experience.'

Growth and Targets

Weihai Bank aims for sustained growth. It projects to achieve a sustained annual growth rate of 10% in total assets and a 15% increase in net profit by the end of 2024, with a target of 90% customer satisfaction. For more information on the bank's ownership structure, see Owners & Shareholders of Weihai City Commercial Bank.

- Focus on technology-driven banking.

- Emphasis on digital transformation.

- Commitment to community development.

- Targets for asset and profit growth.

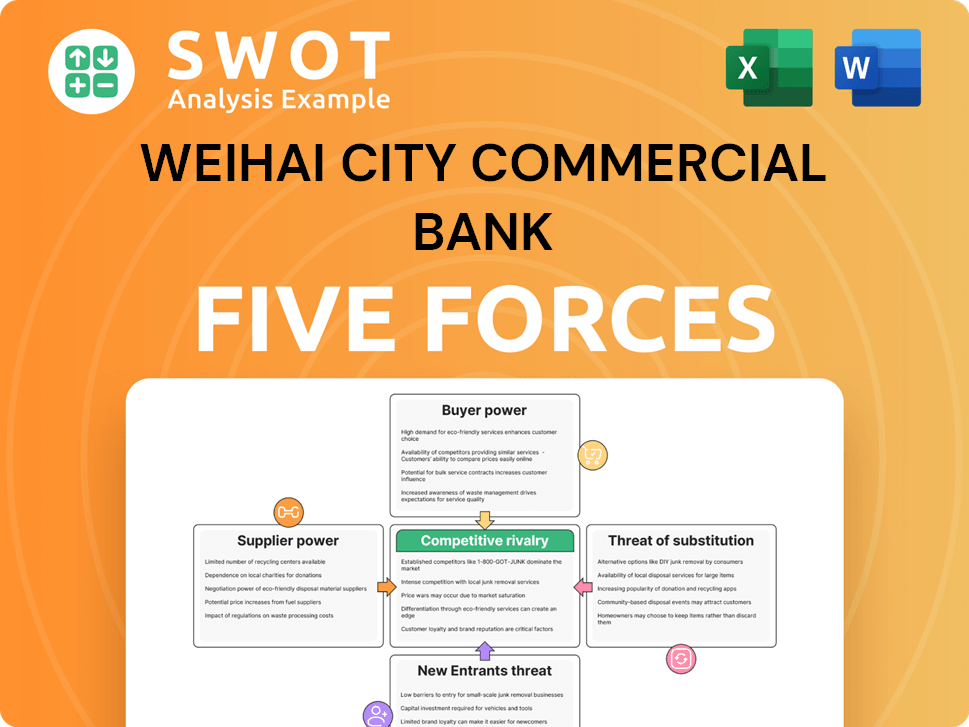

Weihai City Commercial Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Weihai City Commercial Bank Company?

- What is Competitive Landscape of Weihai City Commercial Bank Company?

- What is Growth Strategy and Future Prospects of Weihai City Commercial Bank Company?

- What is Sales and Marketing Strategy of Weihai City Commercial Bank Company?

- What is Brief History of Weihai City Commercial Bank Company?

- Who Owns Weihai City Commercial Bank Company?

- What is Customer Demographics and Target Market of Weihai City Commercial Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.