Shift4 Bundle

How Does Shift4 Company Thrive in the Fintech Arena?

Shift4 Payments (NYSE:FOUR) is making waves in the financial technology sector, and its recent performance is nothing short of impressive. With soaring revenue and significant payment volume increases, Shift4 is a force to be reckoned with. But how does this payment processing giant actually work, and what drives its continued success?

This deep dive into Shift4 will explore its core operations, from its payment processing capabilities and POS systems to its strategic advantages in the merchant services industry. Understanding the intricacies of Shift4 SWOT Analysis is crucial for anyone looking to understand the competitive landscape and the company's potential for future growth. We'll examine the company's diverse revenue streams, its leadership in key industries like hospitality and retail, and the factors that contribute to its resilience in a dynamic market.

What Are the Key Operations Driving Shift4’s Success?

The core operations of Shift4, a leading payment processing company, are centered around providing a comprehensive platform. This platform integrates hardware, software, and payment processing capabilities. This end-to-end solution aims to streamline commerce for businesses across various sectors and geographies.

Shift4 Payments delivers value through its integrated technology platform. This platform simplifies payment processing and business management. The company primarily serves merchants in hospitality, retail, and sports and entertainment.

The value proposition of Shift4 focuses on simplifying commerce. This is achieved through an integrated platform that combines hardware, software, and payment processing. This approach reduces complexity and costs for merchants, offering a one-stop solution for their payment and business management needs.

Shift4 provides a range of services, including a proprietary payment gateway, point-of-sale (POS) systems, and venue payments. The company also offers cross-border e-commerce acquiring. These services are designed to meet the diverse needs of merchants.

Shift4 primarily targets merchants in the hospitality, retail, and sports and entertainment industries. This includes hotels, restaurants, stadiums, and theme parks. The company tailors its solutions to meet the specific needs of each sector.

Shift4's operational processes include technology development for card acceptance and fraud prevention. The company has focused on software feature enhancements to attract a higher-end merchant base. Its direct distribution channel improves profit margins.

Shift4's vertically integrated approach, particularly in its restaurant and hospitality software, sets it apart. The 'SkyTab' bundle offers software, hardware, payments, and installation. This integrated platform reduces complexity and costs for merchants.

Key Features and Benefits

Shift4's integrated platform provides a one-stop shop for payment and business management. It offers robust security features to protect transactions. The company's focus on innovation and customer service enhances its value proposition.

- Integrated Payment Solutions: A comprehensive platform that combines hardware, software, and payment processing.

- Enhanced Security: Features like EMV encryption and tokenization to protect transactions and data.

- Cost Reduction: The integrated approach reduces the need for multiple vendors, lowering costs for merchants.

- Simplified Operations: A unified system streamlines payment processing and business management.

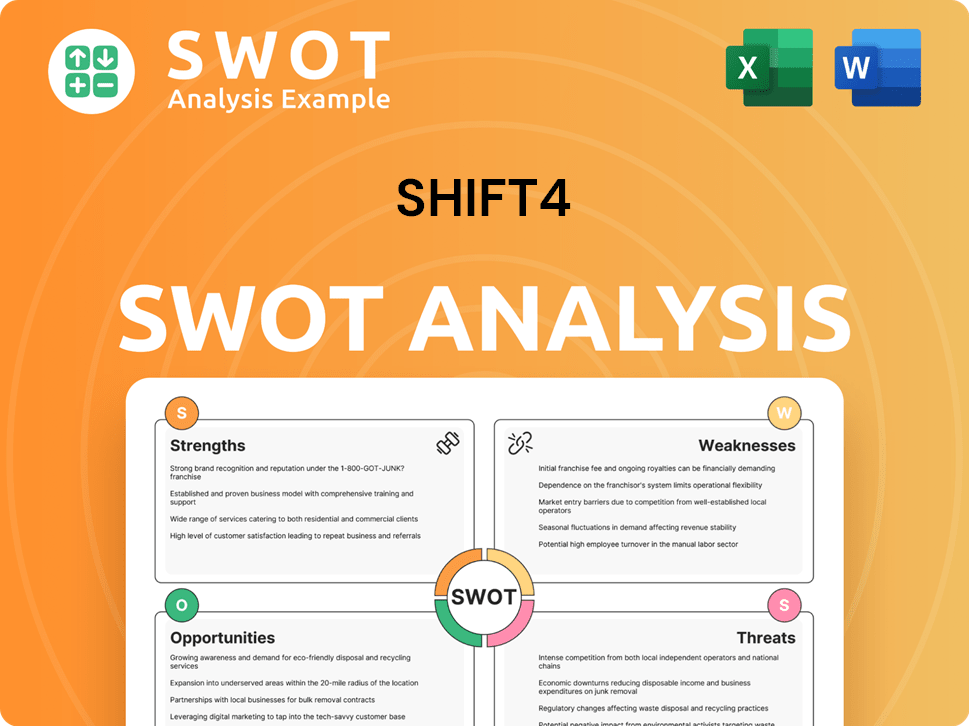

Shift4 SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Shift4 Make Money?

The revenue streams and monetization strategies of the company are primarily centered around payment processing and subscription services. The company, known for its comprehensive merchant services, generates revenue through transaction fees and recurring subscription charges.

The company's financial model is designed to maximize revenue through a combination of transaction-based fees and recurring subscription revenue, ensuring a diversified and sustainable income stream. This approach allows the company to cater to a wide range of merchants, from restaurants to retail businesses, with a focus on providing integrated solutions.

The company's approach to revenue generation is multifaceted, with a strong emphasis on both transaction volume and the value-added services offered to merchants. This strategy allows the company to maintain a competitive edge in the payment processing industry while providing merchants with comprehensive solutions.

Payments-Based Revenue

Payments-based revenue is the largest revenue stream, driven by payment processing fees. This revenue stream is directly tied to the end-to-end payment volume processed.

Subscription and Other Revenues

Subscription and other revenues come from recurring fees for technology deployed to merchants. These include point-of-sale software, hardware leases, and support services.

Monetization Strategies

The company employs platform fees, bundled services, and cross-selling to boost revenue. The company focuses on converting its core gateway business to end-to-end processing.

End-to-End Payment Volume

End-to-end payment volume is a key metric for the company. In Q4 2024, it increased by 49.2% year-over-year to $47.9 billion. In Q1 2025, payment volumes reached $45 billion, a 35% year-over-year increase.

SkyTab and Bundled Services

The company's SkyTab offerings allow it to bundle software, hardware, and payment processing. This provides a comprehensive solution, reducing costs for merchants.

Strategic Acquisitions

Strategic acquisitions, such as Global Blue, are expected to provide significant cross-selling opportunities. These opportunities include services like dynamic currency conversion (DCC) and VAT tax refunds.

Key Financial Data

The company's financial performance is driven by its payment processing volume and subscription services. The company's revenue streams are diversified to ensure financial stability and growth. To understand how the company compares to its competitors, consider the Competitors Landscape of the company.

- In Q1 2025, payments-based revenue reached $755.7 million.

- For the full year 2024, payments-based revenue was nearly $3 billion, making up approximately 90% of total revenue.

- In Q1 2025, subscription and other revenues amounted to $92.6 million, a 77% year-over-year growth.

- For the full year 2024, subscriptions added about $340 million to revenue.

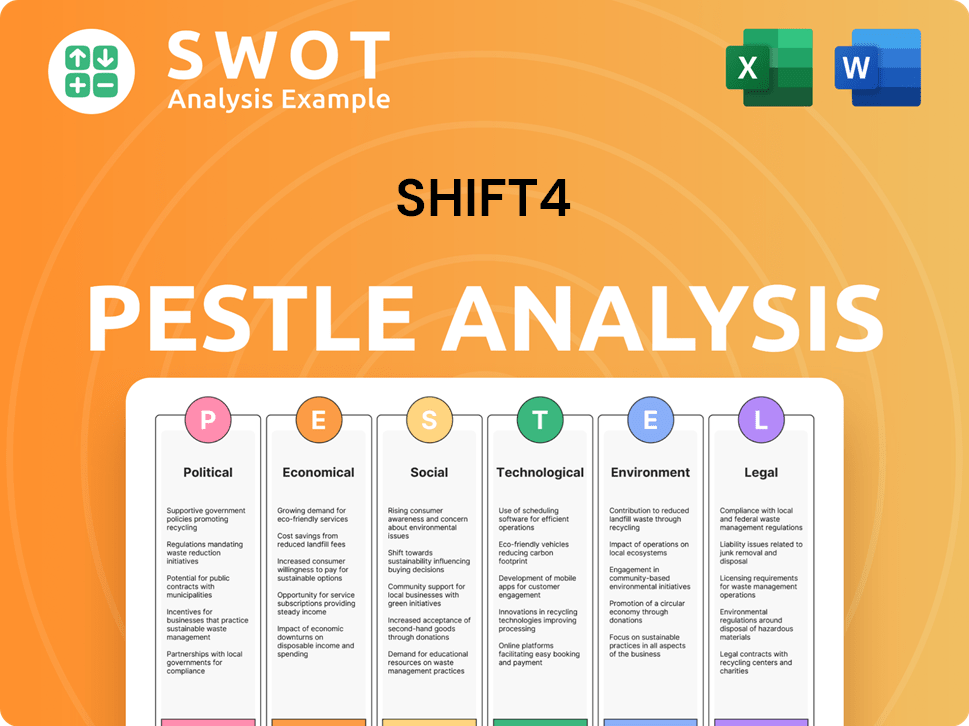

Shift4 PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Shift4’s Business Model?

The following details the key milestones, strategic moves, and competitive advantages of the company. The company has strategically expanded its operations through acquisitions and technological advancements. These moves have positioned the company for growth in the payment processing and merchant services sectors.

A significant aspect of the company's strategy involves expanding its global footprint and enhancing its service offerings. The company has also focused on integrating its technology to provide comprehensive solutions for merchants, particularly in the hospitality and entertainment industries. These efforts aim to improve operational efficiency and provide a competitive edge in the market.

The company's commitment to innovation is evident in its development of new payment solutions and its focus on customer service. By continuously improving its technology and expanding its market reach, the company strives to maintain its position as a leader in the payment processing industry, as detailed in the Growth Strategy of Shift4.

The company's growth has been marked by significant acquisitions and technological advancements. The acquisition of Global Blue in February 2025 for $2.5 billion is a major milestone. The launch of SkyTab Air in Q1 2025 also represents a key development in its POS solutions.

The company's strategic moves include an aggressive acquisition strategy to expand into new markets. Converting its core gateway business to end-to-end processing is another key strategic focus. The introduction of 'Pay With Crypto' in October 2024 highlights its innovative approach to payment processing.

The company's vertically integrated platform and large library of integrations provide a competitive advantage. Its strong presence in hospitality and entertainment allows for tailored solutions. The ability to drive high growth rates while expanding margins, with adjusted EBITDA margins of 51.3% in Q3 2024, further highlights its operational efficiency.

The company's financial performance includes converting $5 billion of its payment volume backlog in Q3 2024 and adding an additional $13 billion. The Global Blue acquisition is expected to add $80 million in revenue. The company's adjusted EBITDA margins of 51.3% in Q3 2024 demonstrate strong profitability.

Key Strategic Initiatives

The company's strategic initiatives include expanding its global footprint through acquisitions, such as the Global Blue deal. The company is also focused on converting its core gateway business to end-to-end processing to drive volume growth. Furthermore, the company is enhancing its SkyTab POS solutions and introducing innovative features like 'Pay With Crypto'.

- Aggressive acquisition strategy to expand into new verticals and geographies.

- Conversion of core gateway business to end-to-end processing.

- Development and global distribution of SkyTab software-integrated POS solutions.

- Introduction of innovative payment features like 'Pay With Crypto'.

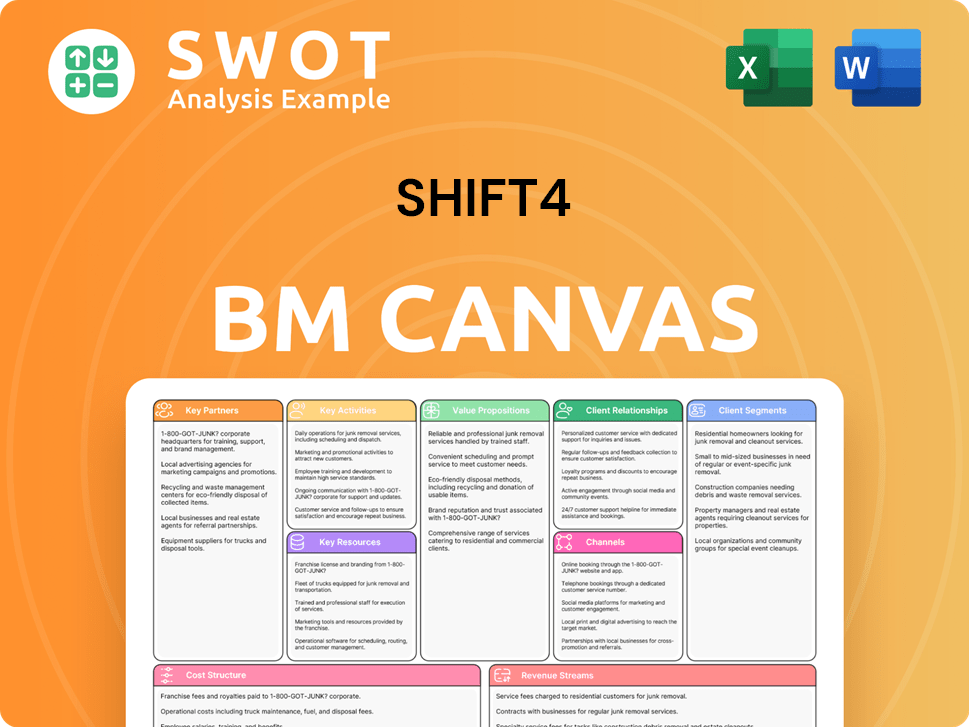

Shift4 Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Shift4 Positioning Itself for Continued Success?

The position of Shift4 Payments in the payment processing sector is notably strong, especially within its key markets. It is estimated that the Shift4 company serves around one-third of all table-service restaurants and roughly 40% of U.S. hotels. The company has a significant presence in sports and entertainment, handling approximately 75% of U.S. professional sports venues, which allows it to capitalize on recurring revenue streams from ticketing and concessions.

Despite its strengths, Shift4 faces several risks. Macroeconomic factors, such as reduced consumer spending and inflation, could affect transaction volumes. Competition from global players and fintech disruptors poses a threat to maintaining take rates. Regulatory challenges in new international markets and integration issues from recent acquisitions also present risks. Additionally, the company's substantial debt load could strain cash flow.

Shift4 is a leading independent provider in the U.S. based on payment volume processed. The company handles billions annually for over 200,000 merchants. As of May 2025, Shift4 operates in over 50 countries, significantly expanding its global footprint from just one country 18 months earlier.

Macroeconomic headwinds, such as softening consumer spending, inflation, and economic uncertainties, can impact transaction volumes and revenue. Increased competition and regulatory challenges in international markets also pose risks. Integration challenges from acquisitions and a substantial debt load could strain cash flow.

Shift4 aims for sustained growth through international expansion and product innovation. Management projects sustained growth through 2025. The company plans to enter 30+ countries within 18 months. The company's focus on cross-selling payment processing services and offering dynamic currency conversion are key revenue opportunities.

For 2025, Shift4 projects gross revenue less network fees between $1.65 billion and $1.72 billion, indicating a 22% to 27% increase. Adjusted EBITDA is projected to be between $830 million and $855 million. The anticipated end-to-end payment volume is set between $200 billion and $220 billion for 2025. The company aims to achieve a $1 billion annual free cash flow run rate by 2027.

Strategic Initiatives and Leadership

Shift4's strategic initiatives focus on international expansion and product innovation. The company plans to enter 30+ countries within 18 months, supported by surging international application submissions. Leadership transition, with Taylor Lauber becoming CEO and Jared Isaacman moving to Executive Chairman, is a strategic move. The company's ability to successfully integrate acquisitions, manage its debt, and navigate economic fluctuations will be critical to sustaining its growth trajectory. Read more about the company's payment processing capabilities in this article about 0.

- Focus on cross-selling payment processing services to acquired customer bases.

- Offering dynamic currency conversion for hotels.

- Aiming to achieve a $1 billion annual free cash flow run rate by 2027.

- The ability to successfully integrate acquisitions, manage its debt, and navigate economic fluctuations.

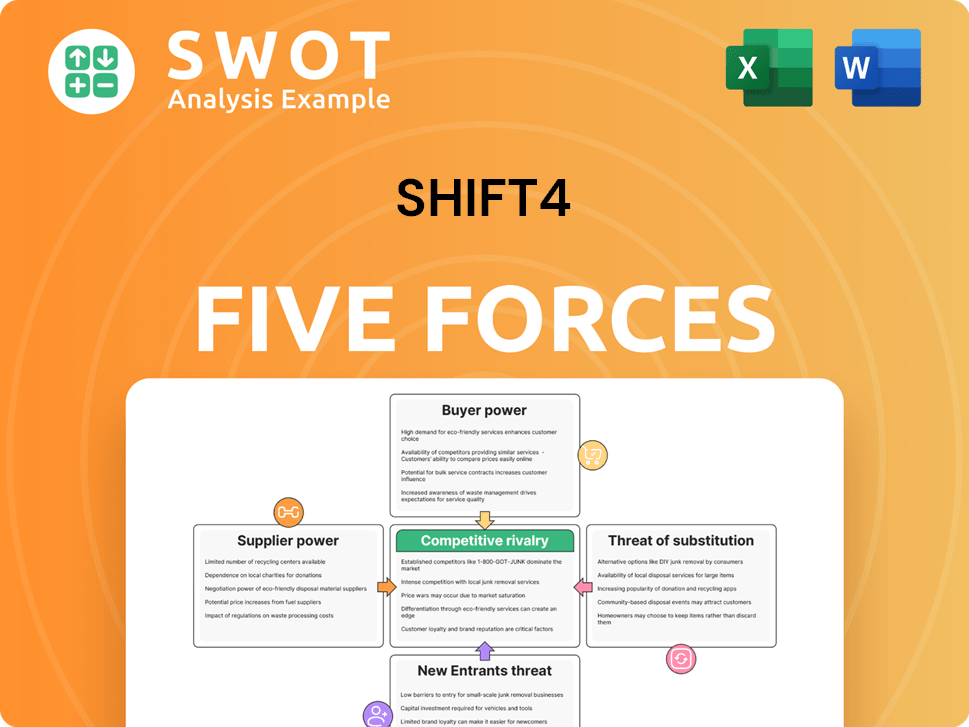

Shift4 Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Shift4 Company?

- What is Competitive Landscape of Shift4 Company?

- What is Growth Strategy and Future Prospects of Shift4 Company?

- What is Sales and Marketing Strategy of Shift4 Company?

- What is Brief History of Shift4 Company?

- Who Owns Shift4 Company?

- What is Customer Demographics and Target Market of Shift4 Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.