Inter&Co Bundle

How Does Inter&Co Thrive in Brazil's Digital Banking Arena?

Inter&Co, a leading Brazilian digital bank, is making waves with its impressive growth, recently announcing record-breaking Q1 2025 results. With net income soaring and a rapidly expanding customer base, this financial powerhouse is reshaping the industry. But how does Inter&Co SWOT Analysis help this company stand out in a competitive market?

Founded in 1994, Inter&Co transformed into Brazil's first fully digital bank in 2015, setting the stage for its current success. Understanding how Inter&Co works, from its comprehensive suite of Inter&Co services to its innovative approach, is crucial for anyone looking to understand the future of finance. This in-depth Inter&Co review will explore its operational model, revenue streams, and the key Inter&Co features driving its remarkable growth, providing insights into its sustained market leadership.

What Are the Key Operations Driving Inter&Co’s Success?

The Inter&Co company operates as a financial super app, providing a wide array of financial and non-financial services. This digital platform caters to both individuals and businesses, primarily in Brazil and expanding into the United States. The core of its operations involves offering traditional banking products alongside investment solutions, insurance brokerage, and foreign exchange transactions. This comprehensive approach aims to simplify users' financial lives.

The operational model of Inter&Co is entirely digital, emphasizing a low-cost, scalable distribution strategy. The company was a pioneer in launching Brazil's first 100% digital checking account in 2015, which is fee-free. They leverage cloud capabilities and are incorporating AI to personalize user experiences and enhance decision-making. This digital-first approach allows for efficient customer engagement through its super app.

The company's integrated ecosystem, supported by a banking license, sets it apart from many fintechs, enabling it to offer loans and deposits. This provides a competitive advantage. Inter&Co's low funding cost, at 60% of Brazil's CDI rate, further supports its competitiveness. This operational efficiency translates into significant customer benefits, making financial services more accessible and often fee-free. By Q1 2025, the company had attracted and retained a large client base, with active clients growing to 21.6 million.

The Inter&Co app offers a wide range of financial services. These include checking accounts, debit and credit cards, deposits, and various loan options. Investment solutions, insurance brokerage, and foreign exchange transactions are also available, creating a one-stop financial shop for users.

The platform is entirely digital, leveraging cloud capabilities and AI. This enables hyper-personalization of the user experience. The digital-first approach allows Inter&Co to maintain a low-cost, scalable distribution model, enhancing efficiency and customer engagement.

Beyond financial services, Inter&Co offers a marketplace for e-commerce. This includes shopping discounts, cashback rewards, and access to events. This integrated approach provides users with a comprehensive financial and lifestyle platform, increasing user engagement and loyalty.

The company's banking license allows it to offer loans and deposits, which is a key advantage. Its low funding costs further support competitiveness. This model has enabled Inter&Co to attract and retain a large client base, with active clients reaching 21.6 million by Q1 2025.

Key Benefits and Features

Inter&Co simplifies financial lives by offering a one-stop shop for diverse needs. The platform provides accessible, often fee-free services, enhancing customer satisfaction. The company's focus on digital innovation and customer experience has driven significant growth.

- Comprehensive financial services integrated into a single app.

- Fee-free digital checking accounts.

- A marketplace with shopping discounts and cashback rewards.

- Strong customer growth, with 21.6 million active clients by Q1 2025.

For more information about the ownership and stakeholders, you can read this article: Owners & Shareholders of Inter&Co.

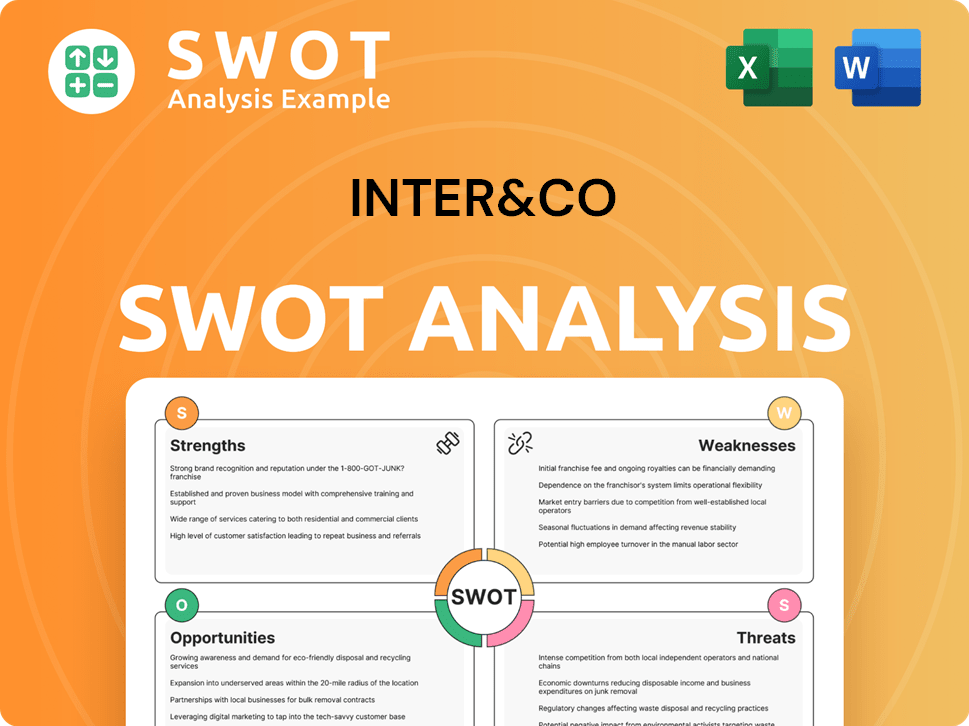

Inter&Co SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Inter&Co Make Money?

The digital super app, generates revenue through a variety of streams. These include net interest income from its loan portfolio and net fee revenues. The company has implemented innovative monetization strategies to boost engagement across its platform.

The company's approach focuses on cross-selling and engagement, which is evident in its peer-to-peer payments system and Loop loyalty program. These initiatives drive recurring revenue and encourage users to engage with more products. Tiered pricing and bundled services within its investment and insurance offerings also contribute to revenue generation.

In Q1 2025, total gross revenue was R$3.16 billion ($526.7 million), reflecting a 38% year-over-year increase, driven by strong credit and transaction growth. The company's net interest margin improved to 8.8% in Q1 2025. The average monthly revenue per active customer grew by 11% to BRL 33.6 in 2024, while the cost of service increased by only 4%, leading to a 16% increase in margin per customer.

Revenue Streams

The primary revenue streams for include net interest income and net fee revenues. Net interest income from its loan portfolio expanded by 21.2% to R$37.39 billion ($6.23 billion) by Q1 2025. Net fee revenues exceeded R$2.0 billion in 2024, showing a 31% year-over-year growth.

Monetization Strategies

Monetization strategies include the peer-to-peer payments system, Pix, and the Loop loyalty program. Pix contributes significantly to fee income with minimal credit risk, accounting for 8.4% of all transactions in Q1 2025. The Loop loyalty program, with 12.4 million active users as of Q1 2025, drives recurring revenue.

Financial Performance

In Q1 2025, total gross revenue was R$3.16 billion ($526.7 million), a 38% year-over-year increase. For the full year 2024, total gross revenues surpassed R$10 billion. The net interest margin improved to 8.8% in Q1 2025, supported by optimized credit origination.

Customer Engagement

The average monthly revenue per active customer grew by 11% to BRL 33.6 in 2024. The cost of service increased by only 4%, leading to a 16% increase in margin per customer. Loop clients use 2.3 times more products than non-members.

Key Takeaways

The company's revenue model is built on a foundation of diverse income streams and strategic monetization efforts. These strategies are designed to boost user engagement and increase profitability. For more detailed information, you can explore the Competitors Landscape of Inter&Co.

- Net interest income and net fee revenues are key revenue drivers.

- The peer-to-peer payments system and Loop loyalty program enhance monetization.

- Strong financial performance, including revenue and margin growth, demonstrates effective strategies.

- Customer engagement and cross-selling efforts are central to the company's success.

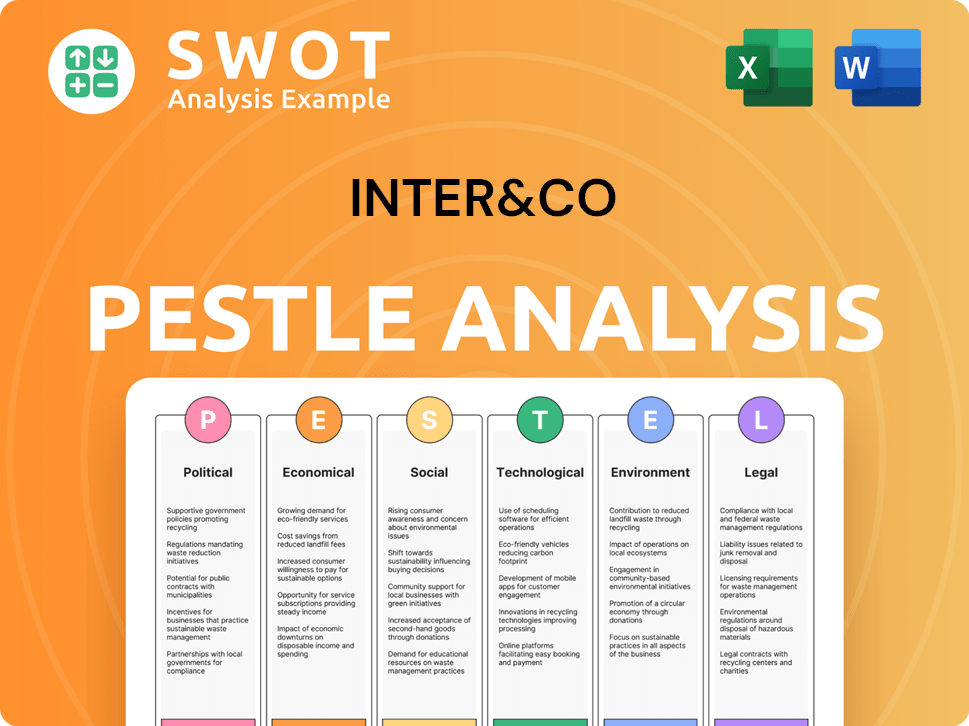

Inter&Co PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Inter&Co’s Business Model?

The journey of Inter&Co has been marked by significant milestones and strategic initiatives that have shaped its operations and financial performance. A pivotal moment was its transformation into Brazil's first fully digital bank in 2015. This move set the stage for its subsequent growth and expansion in the financial sector.

Further milestones include its IPO on the Brazilian stock exchange in 2018 and its listing on Nasdaq in June 2022. This made Inter&Co the first Brazilian company to upgrade its primary listing to the U.S. These strategic moves highlight the company's ambition to broaden its investor base and increase its global presence. The launch of its 'financial super app' in 2020, integrating banking, investments, insurance, and e-commerce, was a significant innovation that expanded its product offering and fostered cross-selling.

The company's strategic focus on partnerships and acquisitions, such as the acquisition of Granito in 2024, has enhanced its operations. Furthermore, the naming rights sponsorship of the Inter&Co Stadium in Orlando has solidified its U.S. presence, offering unique benefits through its loyalty program. For more details, you can read about the Brief History of Inter&Co.

In 2015, Inter&Co became Brazil's first fully digital bank. The IPO on the Brazilian stock exchange in 2018 and the Nasdaq listing in June 2022 were critical for expansion. The launch of the financial super app in 2020 integrated various financial services.

The acquisition of Granito in 2024 enhanced U.S. operations. The naming rights for the Inter&Co Stadium in Orlando boosted its U.S. presence. The launch of new products like private payroll loans in Q1 2025, which quickly reached R$197 million ($32.8 million) in originations, shows rapid growth.

Its fully digital business model with a banking license sets it apart. The super app ecosystem drives customer loyalty. It uses cloud capabilities and AI for hyper-personalization. Low funding costs and improving asset quality, with non-performing loans (NPLs) dropping to 4.1% in Q1 2025, strengthen its position.

Inter&Co focuses on its '60-30-30 plan' – targeting 60 million clients, 30% efficiency, and 30% ROE by 2027. Continuous integration of new technologies and portfolio expansion is key. Adapting to macroeconomic challenges, such as the high Selic rate in Brazil, is crucial.

Operational and Financial Highlights

Despite macroeconomic challenges, Inter&Co has shown resilience. The company's focus on collateralized loans and disciplined growth has helped manage the high Selic rate environment. The drop in non-performing loans (NPLs) to 4.1% in Q1 2025 indicates improving asset quality.

- The launch of private payroll loans in Q1 2025 reached R$197 million ($32.8 million) in originations.

- The '60-30-30 plan' aims for 60 million clients, 30% efficiency, and 30% ROE by 2027.

- Technological advancements, including cloud capabilities and AI, drive hyper-personalization.

- The super app ecosystem fosters customer loyalty and cross-selling opportunities.

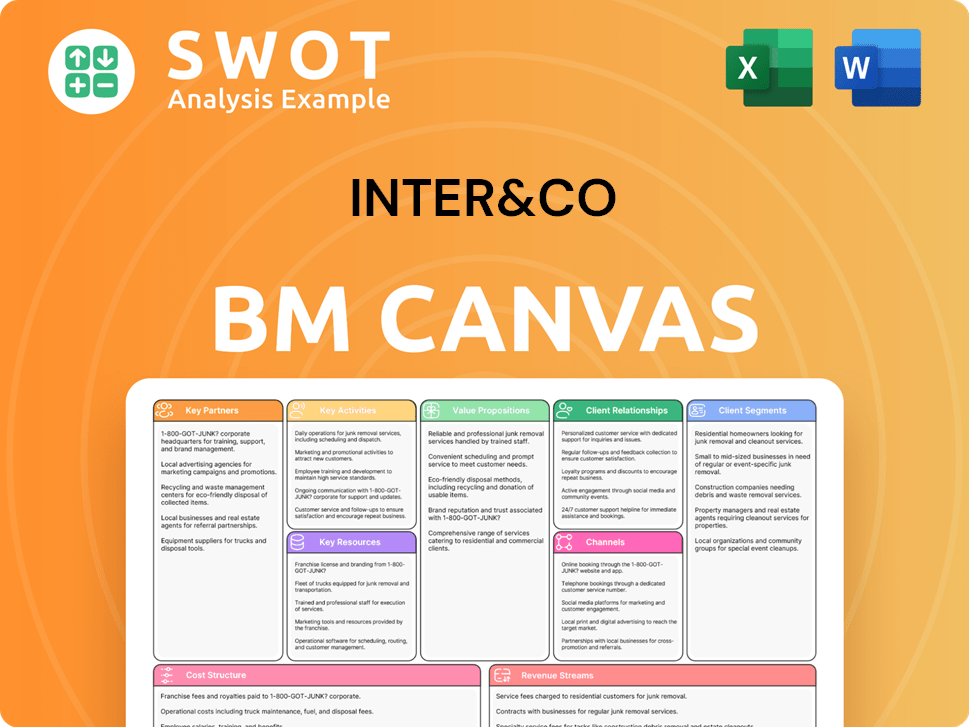

Inter&Co Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Inter&Co Positioning Itself for Continued Success?

The financial institution, Inter&Co, has established a robust position within the Brazilian financial services sector. It has consistently increased its market share in key areas. By Q4 2024, the company held a significant market share in several key segments, demonstrating its growing influence and reach within the industry. The company's strategic initiatives and focus on customer engagement are central to its sustained growth and expansion in the market.

Inter&Co's digital-first approach and comprehensive super app have fostered significant customer loyalty. Its client base reached 37.7 million by Q1 2025, with an activation rate of 57.2%. The company is also expanding its global reach, with 3.9 million clients outside Brazil, primarily through its international accounts targeting the Brazilian expatriate population. This expansion highlights Inter&Co's commitment to providing services that meet the evolving needs of its diverse customer base.

Inter&Co has a strong presence in the Brazilian market, with a focus on digital services. It has a significant market share in transactions and foreign exchange. This positions the company as a key player in the rapidly evolving fintech landscape.

The company faces risks from macroeconomic factors in Brazil, including high interest rates. Competition in the fintech market poses a constant challenge. Regulatory changes and technological disruptions are also ongoing risks.

Inter&Co aims for continued growth and profitability through strategic initiatives. The company is pursuing global expansion and product innovation, such as cryptocurrency trading. It projects loan growth of 25-30% in 2025.

By Q4 2024, Inter&Co held an 8.3% market share in transactions through Brazil's Pix system, 8.0% in foreign exchange transactions, and 7.9% in mortgage lending. The company is targeting 60 million clients, a 30% efficiency ratio, and a 30% ROE by 2027.

Strategic Initiatives and Growth

Inter&Co's strategy includes global expansion, product innovation, and leveraging its super app ecosystem. The company is focused on sustainable growth and market expansion. This approach is designed to capitalize on market opportunities and enhance customer value.

- Expansion into new markets, including Latin America, the United States, and Europe.

- Continued investment in product innovation, such as cryptocurrency trading and financial planning tools.

- Focus on hyper-personalization and loyalty programs to enhance customer engagement.

- Sustainable, collateralized growth to maintain financial stability.

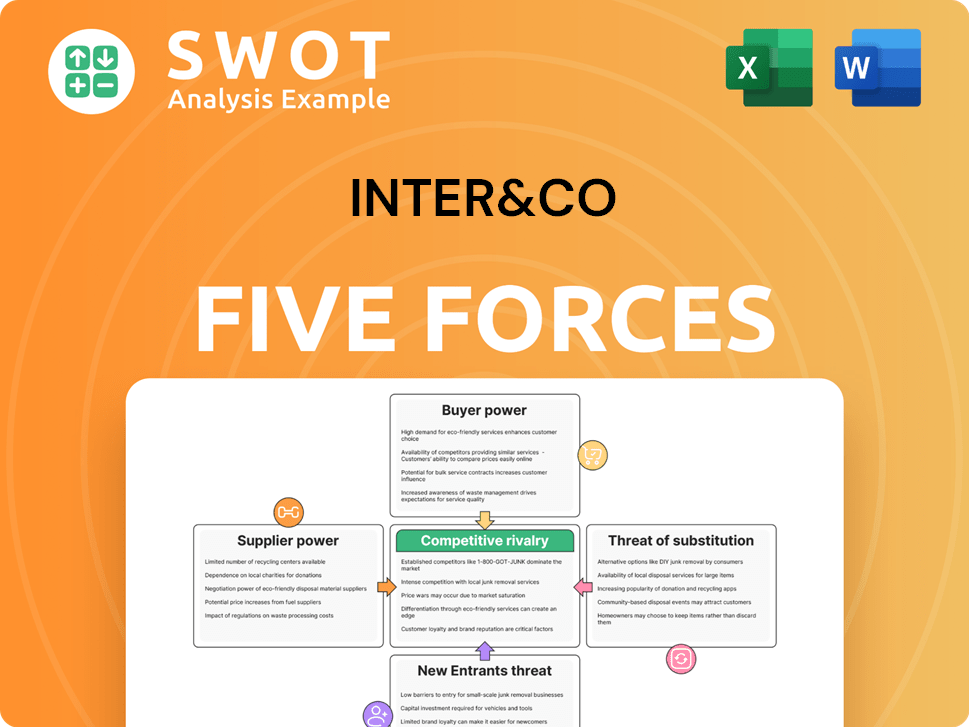

Inter&Co Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Inter&Co Company?

- What is Competitive Landscape of Inter&Co Company?

- What is Growth Strategy and Future Prospects of Inter&Co Company?

- What is Sales and Marketing Strategy of Inter&Co Company?

- What is Brief History of Inter&Co Company?

- Who Owns Inter&Co Company?

- What is Customer Demographics and Target Market of Inter&Co Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.