Helia Group Bundle

How Does Helia Group Navigate the Australian Housing Market?

Delve into the core operations of Helia Group SWOT Analysis, a key player in Australia's financial sector, particularly within the housing market. This company provides lenders mortgage insurance (LMI), acting as a crucial risk mitigator for banks and financial institutions. Understanding the Helia Group company is vital for anyone involved in financial services or tracking the health of the Australian housing market.

Helia Group's role is fundamental to the Australian mortgage sector, enabling higher loan-to-value mortgages and broadening access to home financing. This exploration of Helia Group business will uncover its operational framework, revenue streams, and strategic positioning. Analyzing Helia Group's services and structure is essential for investors and industry watchers alike, offering insights into its resilience and future prospects within a dynamic economic environment.

What Are the Key Operations Driving Helia Group’s Success?

The core operations of the Helia Group company center on providing Lenders Mortgage Insurance (LMI). This specialized insurance protects lenders from financial losses if a borrower defaults on their home loan, and the sale of the property doesn't cover the outstanding debt. Helia Group primarily serves banks, credit unions, and other authorized deposit-taking institutions across Australia, offering them a crucial risk management tool.

Helia Group's value proposition to these lenders is multifaceted, encompassing risk transfer, capital relief, and operational efficiency. By transferring the credit risk associated with high Loan-to-Value Ratio (LVR) loans to Helia Group, lenders can reduce their regulatory capital requirements, freeing up capital for other lending activities. This also streamlines the loan approval process for certain borrowers, as the LMI acts as a credit enhancement.

The operational process starts when lenders submit loan applications to Helia Group for LMI assessment. The company employs sophisticated underwriting models and data analytics to assess borrower creditworthiness and the risks associated with the property. This involves analyzing factors like income, employment stability, credit history, and property valuation. If approved, Helia Group issues an LMI policy to the lender. In the event of a borrower default and subsequent loss, Helia Group indemnifies the lender for the agreed-upon loss amount.

Helia Group services are focused on the provision of LMI, a crucial product for the Australian mortgage market. This insurance protects lenders against losses from borrower defaults. They offer comprehensive risk management solutions tailored to the needs of Australian lenders.

Helia Group operations involve a sophisticated underwriting process using advanced data analytics. They assess risk, manage policies, and handle claims efficiently. Their operations are primarily digital, facilitating seamless data exchange with lenders.

Helia Group's structure is designed to support its core business of providing LMI. The company has a robust IT infrastructure to support its operations. Helia Group has strong relationships with major Australian financial institutions, key to its distribution network.

Helia Group's value proposition includes risk transfer, capital relief, and operational efficiency for lenders. They enable lenders to reduce capital requirements and streamline loan approvals. Their expertise in the Australian housing market adds significant value.

Key Aspects of Helia Group's Operations

Helia Group distinguishes itself through deep expertise in the Australian housing market and longstanding lender relationships. Their ability to refine underwriting models using historical data and predictive analytics is a key differentiator. This translates to reduced risk exposure for lenders and potentially increased access to home financing for borrowers.

- Risk Assessment: Utilizing advanced data analytics for thorough borrower and property evaluations.

- Policy Management: Efficient issuance and management of LMI policies.

- Claims Handling: Streamlined processes for indemnifying lenders in case of defaults.

- Market Expertise: Deep understanding of the Australian housing market dynamics.

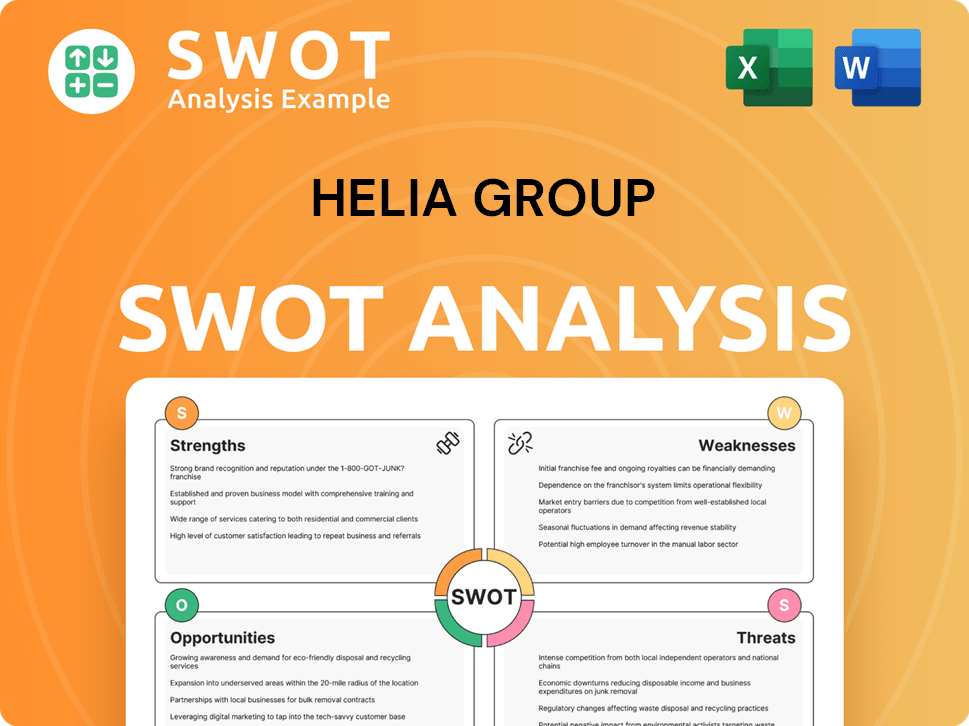

Helia Group SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Helia Group Make Money?

The primary revenue stream for the Helia Group business is derived from premiums collected on lenders mortgage insurance (LMI) policies. These premiums are typically paid upfront by borrowers, often incorporated into their loan amounts. The premium rates are determined by factors such as the loan-to-value ratio (LVR), loan amount, loan type, and the borrower's creditworthiness.

In 2023, the

As of December 31, 2023, the investment portfolio generated investment income of $98.1 million, contributing significantly to overall profitability. This approach, combining insurance premiums with investment returns, is a common strategy for insurance companies. The monetization strategy of

Key Revenue Drivers and Monetization Strategies

The core of

- LMI Premiums: The primary source of revenue comes from premiums on LMI policies, which are influenced by loan characteristics and borrower profiles.

- Investment Income: A significant portion of revenue is generated from the investment of premiums and reserves.

- Risk Assessment: Accurate risk pricing through underwriting models is crucial for maintaining profitability.

- Product Innovation: Potential for tailored solutions within the mortgage insurance space, though the main focus remains on LMI premiums and investment management.

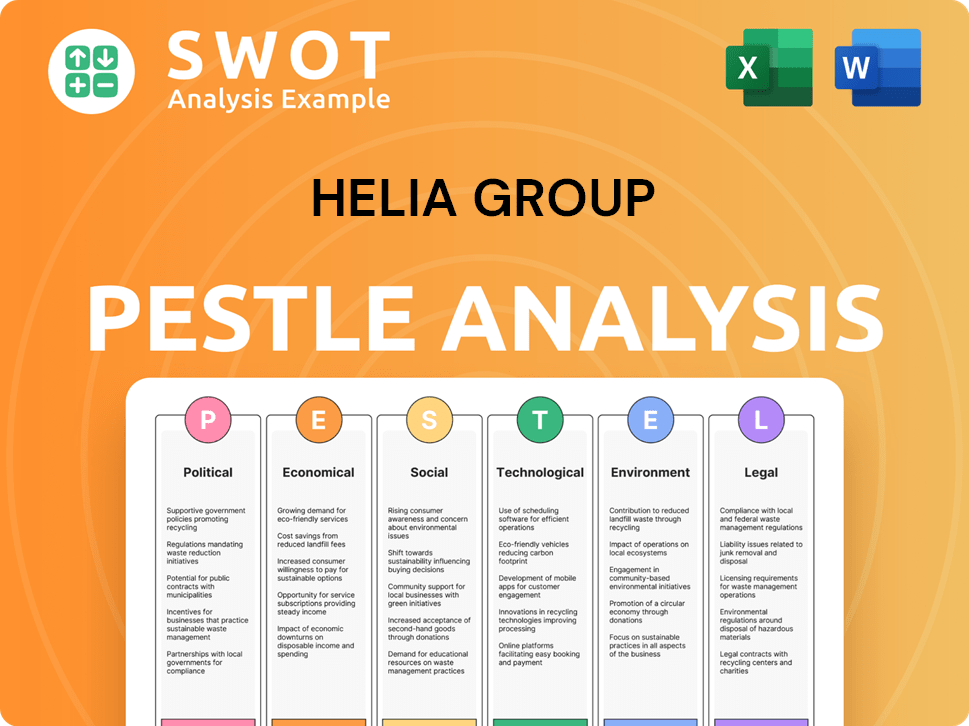

Helia Group PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Helia Group’s Business Model?

The Helia Group company, formerly known as Genworth Mortgage Insurance Australia, rebranded in 2022, marking a significant milestone. This strategic move aimed to establish a distinct identity in the Australian market and reflect its evolution. The company's focus on maintaining strong relationships with major Australian lenders is crucial for its distribution and market penetration. The Helia Group has navigated various market challenges, including economic uncertainty and fluctuating interest rates.

The company emphasizes its prudent risk management framework to maintain a strong financial position. This approach has been critical in adapting to changes in the economic environment. The Helia Group's ability to adapt and its continuous investment in technology contribute to its sustained business model. The company's strong capital position provides a buffer against potential shocks, supporting future growth.

The competitive edge of the Helia Group stems from its established market position, deep understanding of the Australian mortgage market, and sophisticated risk assessment capabilities. As a long-standing provider of LMI, Helia Group benefits from economies of scale and extensive historical data. Its strong brand recognition and trusted lender relationships further solidify its advantage. For a deeper dive into the company's operations, consider reading about the [Helia Group company overview](https://www.example.com/helia-group-overview).

Key Competitive Strengths

The Helia Group's competitive strengths include a strong market position and deep understanding of the Australian mortgage market. Its sophisticated risk assessment capabilities and strong brand recognition within the financial services sector are also key. The company's strong capital position, with a pro forma Common Equity Tier 1 (CET1) ratio of 165.7% as of December 31, 2023, is another key strength.

- Established Market Position: Long-standing provider of LMI in Australia.

- Risk Management: Prudent risk management framework.

- Financial Strength: Strong capital position to absorb potential shocks.

- Adaptability: Ability to adapt to new market trends.

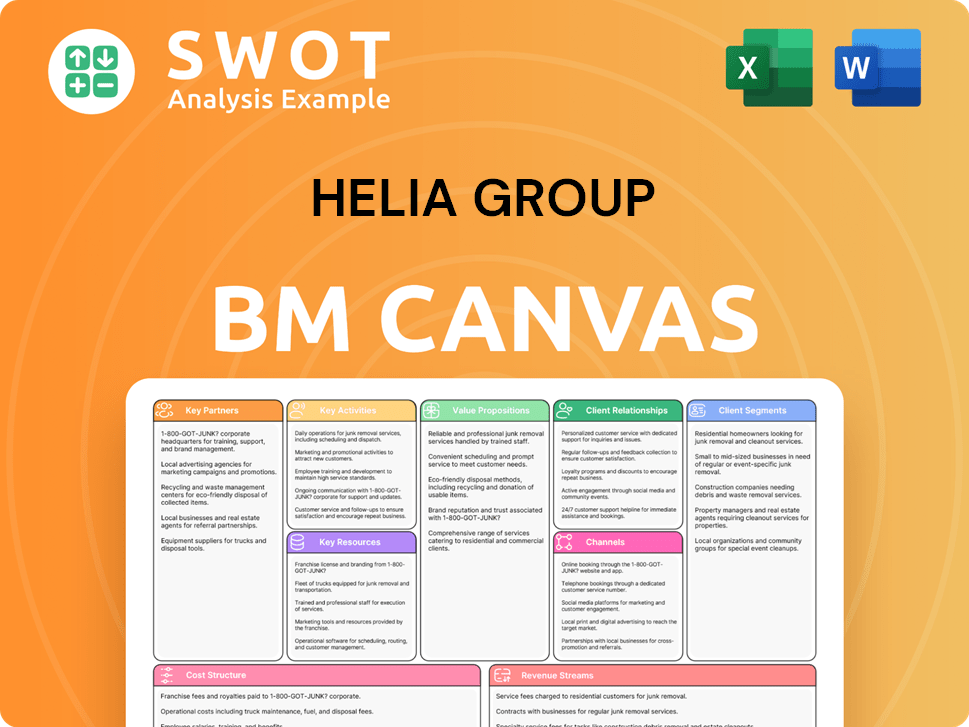

Helia Group Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Helia Group Positioning Itself for Continued Success?

The Helia Group holds a significant position within the Australian lenders mortgage insurance (LMI) market. It operates as a key player, supported by long-standing relationships with major banks and financial institutions. This strong market presence is a result of its established connections and specialized services within the financial sector.

Despite its strengths, the

Helia Group has a substantial market share in the Australian LMI sector, benefiting from strong relationships with major lenders. Its national reach covers all states and territories, ensuring broad market penetration. Customer loyalty among its lender partners is high, which strengthens its position.

Regulatory changes and shifts in the housing market pose significant risks to Helia Group's operations. Economic downturns, rising unemployment, and interest rate increases could lead to higher default rates. The emergence of new competitors or alternative solutions could also challenge its market dominance.

Helia Group is focused on leveraging its core strengths to sustain and expand its revenue generation capabilities. Strategic initiatives include refining underwriting models and exploring opportunities within the evolving mortgage landscape. The company is committed to delivering sustainable returns to shareholders.

Helia Group services are designed to support homeownership in Australia. The company navigates economic cycles and regulatory shifts to ensure continued growth and profitability. Helia Group's commitment to prudent risk management is central to its future success.

Key Considerations

Helia Group's ability to adapt to regulatory changes and economic shifts is crucial. Maintaining strong relationships with lenders and managing risk effectively are also key factors. The company's strategic initiatives will influence its long-term performance within the LMI market.

- Underwriting model refinements.

- Exploration of mortgage landscape opportunities.

- Prudent risk management.

- Efficient capital deployment.

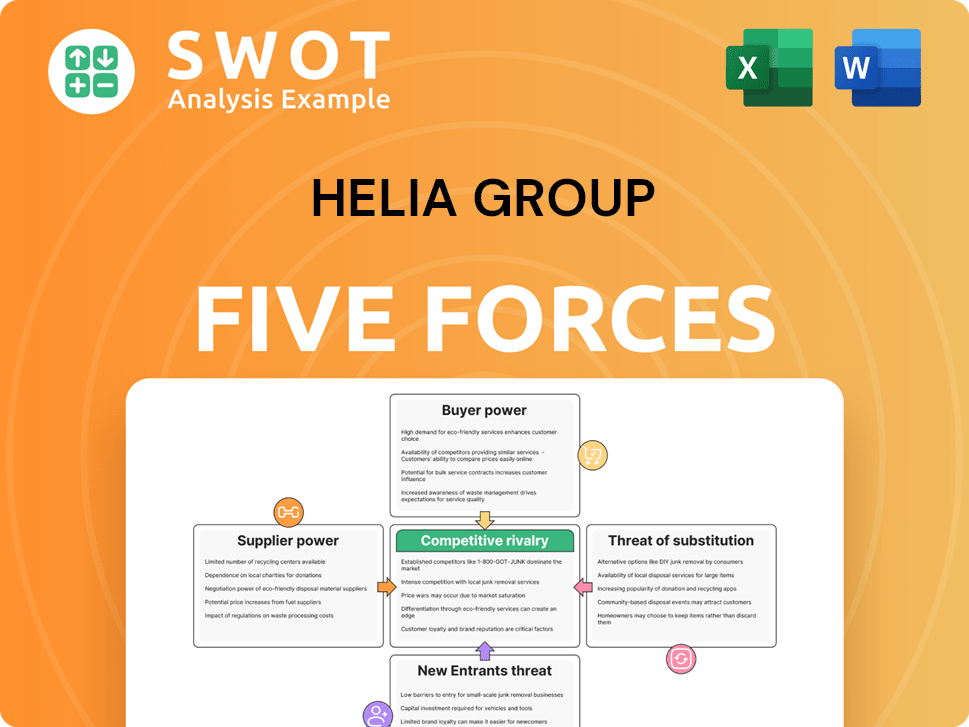

Helia Group Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Helia Group Company?

- What is Competitive Landscape of Helia Group Company?

- What is Growth Strategy and Future Prospects of Helia Group Company?

- What is Sales and Marketing Strategy of Helia Group Company?

- What is Brief History of Helia Group Company?

- Who Owns Helia Group Company?

- What is Customer Demographics and Target Market of Helia Group Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.