goeasy Bundle

How Does the goeasy Company Thrive in the Lending Market?

goeasy Ltd. stands out as a key player in Canada's financial services sector, focusing on the non-prime consumer market. With its easyfinancial division experiencing remarkable growth, the company's loan portfolio has significantly expanded, reaching $3.54 billion by the end of 2023. This growth highlights goeasy's crucial role in providing accessible credit solutions to those often overlooked by traditional lenders.

goeasy offers diverse financial products, including installment loans and point-of-sale financing, through its easyhome and easyfinancial brands. The company's strategic focus on responsible lending and customer satisfaction has fueled its expansion. To gain a deeper understanding of goeasy's competitive strategies, consider exploring a detailed goeasy SWOT Analysis to uncover its strengths, weaknesses, opportunities, and threats within the market. Understanding the goeasy company is essential for anyone interested in the Canadian financial landscape, including insights into goeasy loans, easyfinancial products, and the loan application process.

What Are the Key Operations Driving goeasy’s Success?

The goeasy company creates value by offering financial solutions to non-prime Canadians through its two main divisions: easyfinancial and easyhome. easyfinancial provides various lending products, including installment loans, secured loans, and point-of-sale financing. This caters to individuals who may have lower credit scores or limited credit history, making it challenging to obtain credit from traditional banks. The value proposition lies in providing a clear path to credit building and financial inclusion for this underserved demographic.

Operationally, easyfinancial uses a strong credit assessment process that uses its own scoring models and data analytics to assess risk and determine loan eligibility. The company operates through both online and physical locations, with over 400 easyfinancial locations across Canada, complemented by a strong digital presence. This approach enhances customer accessibility and convenience. Loan servicing is primarily handled in-house, focusing on customer support and responsible collection practices.

easyhome, the leasing division, offers furniture, appliances, and electronics to customers through a lease-to-own model. This allows consumers to acquire essential household items without needing immediate upfront payment or good credit. The operational process involves sourcing products, managing inventory, and facilitating lease agreements through a network of easyhome stores. goeasy's supply chain for its leasing division involves relationships with various manufacturers and distributors to ensure a diverse product offering. The company's unique operational effectiveness stems from its specialized underwriting capabilities for non-prime borrowers, its extensive branch network for personalized service, and its integrated technology platforms that streamline the application and servicing processes. This allows goeasy to deliver tailored financial solutions that address the specific needs of its target customer segments, differentiating it from traditional lenders.

easyfinancial offers a range of lending products tailored to non-prime borrowers. These include unsecured installment loans, secured loans, and point-of-sale financing. The company focuses on providing accessible financial solutions to individuals who may have difficulty obtaining credit from traditional sources. The company's approach is detailed in Growth Strategy of goeasy.

easyhome provides furniture, appliances, and electronics through a lease-to-own model. This allows customers to acquire essential household items without requiring immediate upfront payment or good credit. The model is designed to offer flexibility and accessibility to consumers who may not qualify for traditional financing options.

goeasy leverages a robust credit adjudication process and an omni-channel approach. This includes proprietary scoring models and data analytics to assess risk and determine loan eligibility. The company's extensive branch network and integrated technology platforms streamline the loan application and servicing processes.

The value proposition of goeasy lies in providing accessible and responsible financial solutions. This includes a clear path to credit building and financial inclusion for underserved demographics. The company's focus on customer support and responsible collection practices further enhances its value proposition.

Key Operational Highlights

goeasy operates through two main divisions, easyfinancial and easyhome, to serve non-prime borrowers. The company's operational efficiency is enhanced by its extensive branch network and integrated technology platforms. This approach allows goeasy to deliver tailored financial solutions.

- easyfinancial offers installment loans, secured loans, and point-of-sale financing.

- easyhome provides furniture, appliances, and electronics through a lease-to-own model.

- goeasy uses proprietary scoring models and data analytics for credit assessment.

- The company has over 400 easyfinancial locations across Canada.

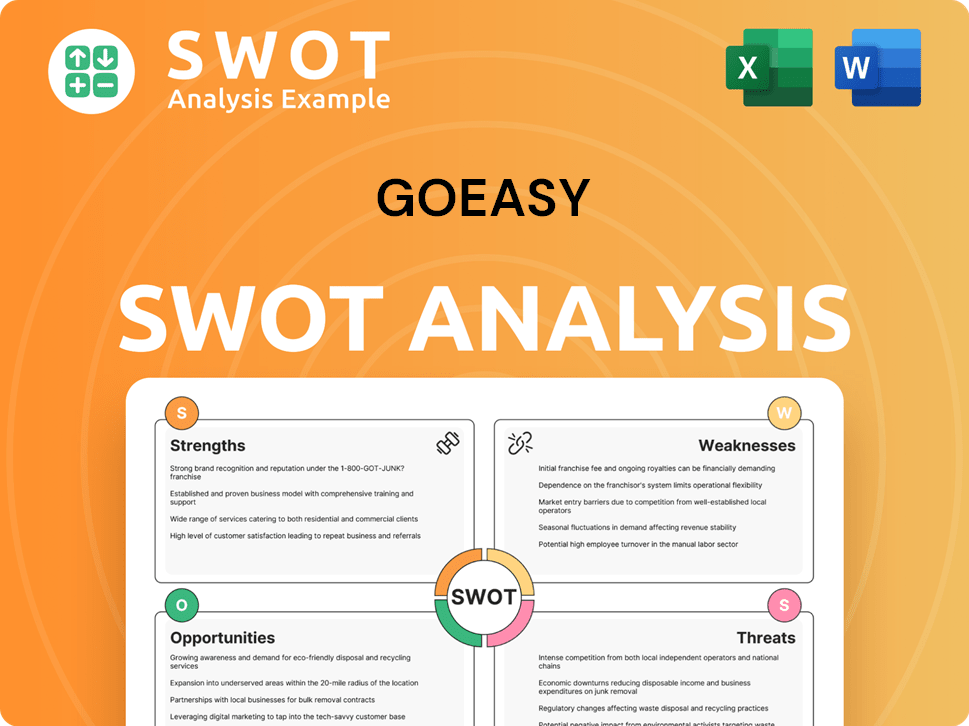

goeasy SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does goeasy Make Money?

The revenue streams and monetization strategies of the goeasy company are primarily centered around its lending and leasing operations. The company’s financial performance is significantly driven by its easyfinancial division, which contributes the majority of the revenue. This focus allows goeasy to serve the non-prime market effectively while managing risk through strategic pricing and diversification.

For the fiscal year ending December 31, 2023, easyfinancial's revenue reached $1.09 billion, showcasing its substantial contribution to goeasy's overall financial performance. Easyhome, the leasing division, provides a steady stream of recurring revenue, although it is smaller in scale compared to easyfinancial. The company also generates revenue through point-of-sale financing solutions offered in partnership with various retailers.

The total loan portfolio reached $3.54 billion by the end of 2023, highlighting the significant scale of its lending activities. goeasy uses a tiered pricing model for loans, adjusting interest rates based on the borrower's credit risk profile. The company focuses on cross-selling opportunities between its easyfinancial and easyhome divisions and has expanded its revenue through strategic partnerships.

Key Revenue Streams and Monetization Strategies

The core revenue streams for easyfinancial include interest income from its unsecured and secured loan portfolios, as well as fees associated with loan origination and servicing. Several monetization strategies are employed by goeasy to maximize its revenue potential and market reach.

- Interest Income: Generated from unsecured and secured loans.

- Fees: Origination and servicing fees associated with loans.

- Tiered Pricing: Interest rates are adjusted based on the borrower's credit risk profile.

- Cross-Selling: Encouraging customers to utilize services from both easyfinancial and easyhome.

- Strategic Partnerships: Partnerships with automotive dealerships for vehicle financing.

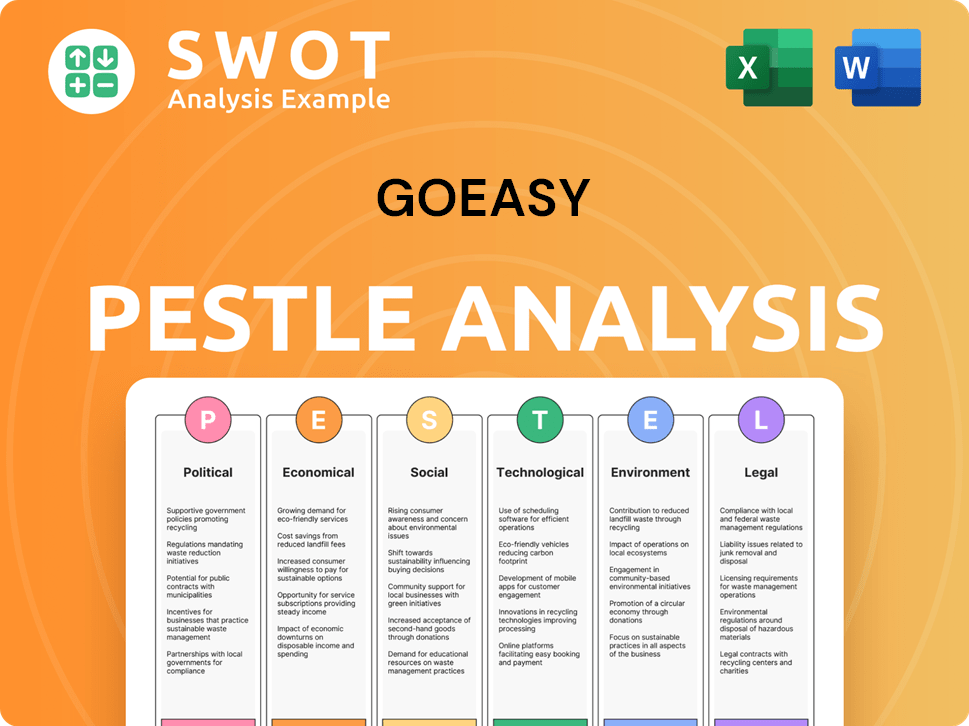

goeasy PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped goeasy’s Business Model?

The journey of the goeasy company has been marked by significant milestones and strategic shifts, shaping its operational and financial standing. A key development was the launch and expansion of its easyfinancial lending division, which has become the primary driver of the company's growth. Strategic acquisitions and partnerships, such as the 2021 acquisition of PayBright, have broadened its reach and diversified its product offerings, allowing it to capitalize on the expanding buy-now-pay-later market.

The company has also adapted to operational challenges, including evolving financial services regulations and managing credit risk amid economic fluctuations. goeasy has consistently responded by enhancing its credit assessment models and investing in technology to improve efficiency and customer experience. Investments in digital platforms have streamlined the loan application process and improved customer engagement. For example, in the first quarter of 2024, goeasy reported a 16% increase in revenue year-over-year, driven by strong demand for its loan products.

goeasy's competitive advantage is multifaceted, including strong brand recognition, particularly with easyfinancial, which fosters customer trust within the non-prime segment. The company benefits from economies of scale due to its extensive branch network and robust digital infrastructure. Its expertise in underwriting and managing risk for non-prime borrowers, combined with diversified product offerings, creates a barrier to entry for competitors. Furthermore, goeasy's commitment to responsible lending and helping customers improve their credit scores supports its sustainable business model. To learn more about how the company approaches its marketing, you can read about the Marketing Strategy of goeasy.

The launch and expansion of easyfinancial was a pivotal moment, becoming the main growth engine. The acquisition of PayBright in 2021 significantly expanded its market reach. These moves have allowed goeasy to adapt to market changes and consumer needs.

goeasy has focused on technological advancements to streamline loan processes and improve customer experience. The company has also adapted to regulatory changes and managed credit risk through enhanced models. This includes ongoing investments in digital platforms to improve efficiency.

goeasy benefits from strong brand recognition and customer trust, particularly with easyfinancial. The company's extensive branch network and digital infrastructure enable efficient customer acquisition and service delivery. goeasy's expertise in risk management and diversified product offerings creates a significant competitive advantage.

In Q1 2024, goeasy reported a 16% increase in revenue year-over-year. The company's focus on responsible lending and helping customers improve their credit scores contributes to its sustainable business model and positive market perception. This financial performance reflects the success of its strategic initiatives.

Operational and Financial Highlights

goeasy's strategy includes expanding its digital capabilities and enhancing its online platforms. This is in response to the increasing demand for digital financial services. The company continues to adapt to market trends and customer needs.

- Focus on digital platforms to streamline loan applications.

- Enhancements to customer engagement through technology.

- Investment in credit adjudication models to manage risk.

- Diversification of product offerings to meet market demands.

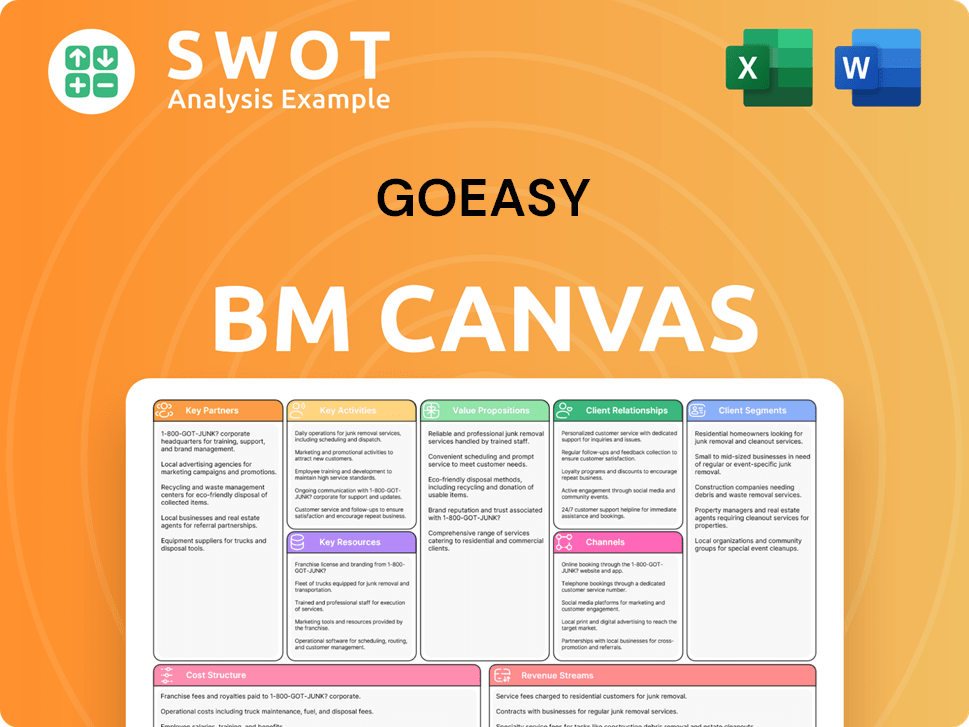

goeasy Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is goeasy Positioning Itself for Continued Success?

The goeasy company holds a prominent position in Canada's non-prime lending and leasing market. Its extensive loan portfolio and broad branch network, combined with a strong digital presence, solidify its status as a leading player. While precise market share data for the entire non-prime segment fluctuates, goeasy's consistent growth in loan originations and portfolio size underscores its robust standing compared to smaller, regional competitors. Customer loyalty is enhanced through repeat business and the company's focus on helping clients improve their financial standing, potentially transitioning them to prime credit. The company's national presence provides a wide reach across Canada.

Despite its strong market position, goeasy faces several significant risks. Regulatory changes within the financial services sector, particularly concerning interest rate caps or consumer protection laws, could impact its profitability and operational model. The emergence of new competitors, including FinTech startups offering alternative lending solutions, presents a continuous competitive threat. Economic downturns or rising unemployment rates could lead to increased loan defaults and affect asset quality. Furthermore, technological disruption, such as advancements in AI-driven credit assessment or new payment technologies, requires continuous adaptation and investment from goeasy.

goeasy is a leading player in the Canadian non-prime lending and leasing market. It has a substantial loan portfolio and a wide branch network. The company's digital presence further strengthens its market position. The company focuses on helping clients improve their financial standing.

Regulatory changes, such as interest rate caps, could impact profitability. New competitors, including FinTech startups, pose a threat. Economic downturns may lead to increased loan defaults. Technological advancements require continuous adaptation and investment.

The company plans to expand its loan portfolio, especially in secured lending. Investments in technology and digital transformation are ongoing. Leadership emphasizes responsible growth and exploring new product offerings. The company aims to capitalize on the demand for accessible credit.

Expansion of the loan portfolio, particularly in secured lending products. Ongoing investments in technology to improve efficiency. Focus on responsible growth and diversifying funding sources. Exploration of new product offerings to meet evolving customer needs.

Key Considerations for goeasy

For goeasy, maintaining its industry position involves strategic initiatives to navigate risks and capitalize on opportunities. The company’s focus on secured lending products and digital transformation are key strategies. Understanding the competitive landscape is crucial for sustained success. You can find more information on the Competitors Landscape of goeasy.

- Adaptation to regulatory changes and market dynamics is essential.

- Continuous investment in technology to enhance customer experience.

- Focus on responsible lending practices to manage credit risk.

- Strategic diversification of funding sources to ensure financial stability.

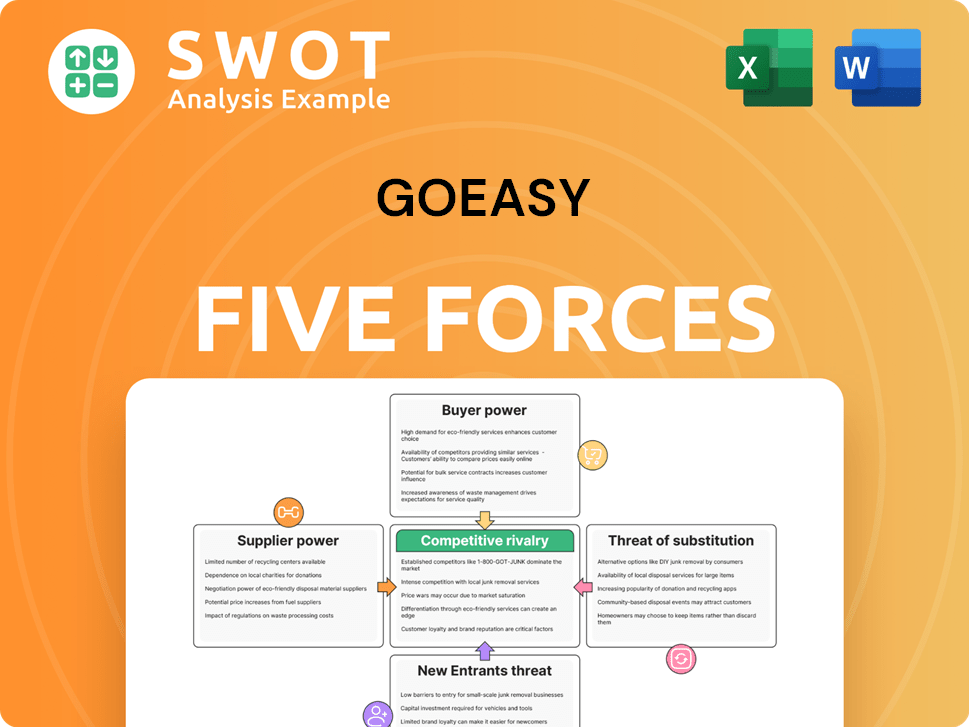

goeasy Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of goeasy Company?

- What is Competitive Landscape of goeasy Company?

- What is Growth Strategy and Future Prospects of goeasy Company?

- What is Sales and Marketing Strategy of goeasy Company?

- What is Brief History of goeasy Company?

- Who Owns goeasy Company?

- What is Customer Demographics and Target Market of goeasy Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.