Globe Life Bundle

Decoding Globe Life: How Does It Thrive?

Globe Life Inc. (NYSE: GL) is a powerhouse in the U.S. insurance industry, especially for middle and lower-middle-income families. With a strong Q1 2025 showing a significant increase in net income, the company showcases its financial strength. Its diverse offerings and strategic capital management make it a compelling case study for investors and industry watchers alike.

Globe Life Insurance offers a range of Globe Life SWOT Analysis, including life and supplemental health insurance, distributed through various segments. Their consistent performance, driven by premium and investment income, is key to understanding their market position. This analysis will explore the inner workings of this life insurance company, offering insights into its value creation and strategic direction within the competitive landscape of term life insurance and whole life insurance.

What Are the Key Operations Driving Globe Life’s Success?

focuses on providing essential life and supplemental health insurance products, primarily targeting middle and lower-middle-income American families. This approach allows the company to offer accessible and flexible insurance options, including policies that do not require a medical exam. Their value proposition centers on delivering basic protection, which contributes to lower lapse rates compared to some competitors, especially in stable economic conditions.

The company distributes its products through a multi-channel network. This includes direct-to-consumer channels and agency networks. The agency networks encompass captive agents, independent agents, and other channels. This diversified distribution strategy enhances market reach and customer engagement, ensuring that their products are accessible to a broad audience.

The company operates through five distinct segments: American Income Life, Family Heritage Life, Globe Life Direct Response, Globe Life Liberty National, and Globe Life Senior Benefits. Each segment is designed to focus on specific customer needs and distribution methods, allowing for targeted marketing and efficient service delivery. For those interested in the company's approach, you can read more about the Marketing Strategy of Globe Life.

In Q1 2025, the American Income Life Division saw a 6% increase in life premiums. The Liberty National Division reported a 4% increase in net life sales and a 6% rise in life premiums. The Family Heritage Division experienced a 7% increase in health net sales and a 9% increase in health premiums.

The Liberty National Division saw an 8% increase in the average producing agent count in Q1 2025. The Family Heritage Division's average producing agent count increased by 9%. These figures highlight the company's expanding reach and ability to connect with customers.

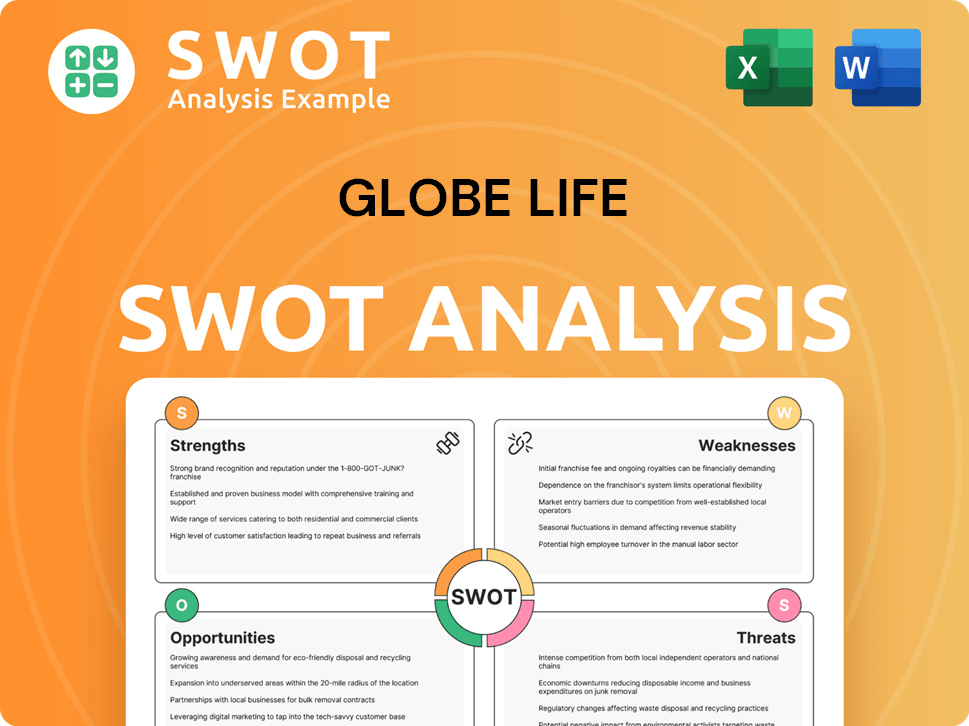

Key Operational Strengths

The company's operational processes are designed to provide basic protection, which contributes to lower lapse rates. The investment portfolio primarily comprises public, investment-grade bonds.

- Focus on Underserved Markets: Targeting middle and lower-middle-income families.

- Niche Distribution Relationships: Partnerships with unions and bilingual agents.

- Accessible Insurance Options: Including no-medical-exam policies.

- Financial Strength: Investment-grade bond portfolio for long-term stability.

Globe Life SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Globe Life Make Money?

Understanding the revenue streams and monetization strategies of a company like Globe Life is crucial for assessing its financial health and investment potential. The company primarily generates revenue through premiums from life and supplemental health insurance policies. These strategies include a focus on direct-to-consumer sales and agency networks.

The company's financial performance is a key indicator of its success. For the quarter ending March 31, 2025, total premium revenue increased, demonstrating growth in its core business. This growth, coupled with other financial strategies, paints a picture of a company focused on shareholder value and market expansion.

Globe Life's revenue streams are primarily driven by insurance premiums. The company's ability to cross-sell products and its focus on different distribution channels contribute to its revenue mix. The company also benefits from its ongoing share repurchase program, which enhances shareholder value.

Premium Revenue Breakdown

In Q1 2025, total premium revenue reached $1.20 billion, a 4.8% increase. Life insurance accounted for 80% of the insurance underwriting margin and 69% of total premium revenue in Q1 2025.

Life and Health Insurance Performance

Life insurance premium revenue rose by 3% to $830 million in Q1 2025. Health insurance premium revenue increased by 8% to $370 million during the same period.

Investment Income

Net investment income is another significant revenue source. In Q4 2024, net investment income grew by 4% compared to the year-ago quarter.

Share Repurchase Program

The company actively repurchases its shares to enhance shareholder value. In 2024, $993.7 million was spent to repurchase 10.6 million shares. In Q1 2025, 1.5 million shares were repurchased for $177 million.

Dividend Increases

Globe Life is committed to returning capital to shareholders. The quarterly dividend increased to $0.24 per share in 2024 and to $0.27 per share in Q1 2025.

Monetization Strategies

The company employs tiered pricing for its various policies. It also cross-sells products across its different segments. The company's focus on direct-to-consumer and agency networks contributes to its diverse revenue mix.

Key Takeaways

The financial performance of Globe Life, as indicated by its revenue streams and monetization strategies, reflects a company focused on growth and shareholder value. The increase in premium revenue, along with strategic initiatives such as share repurchases and dividend increases, showcases a commitment to financial strength. For more insights into the competitive landscape, consider reading about the Competitors Landscape of Globe Life.

- Life insurance remains a significant driver of revenue and underwriting margin.

- Health insurance contributes substantially to the overall premium revenue.

- Net investment income provides an additional revenue stream.

- Share repurchases and dividend increases enhance shareholder value.

Globe Life PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Globe Life’s Business Model?

Navigating significant milestones and strategic shifts, has adapted to the evolving insurance landscape. A key move has been the transition to a virtual business model for its American Income Life (AIL) division, particularly notable after the pandemic. This shift has enabled the company to protect over 17 million policyholders, solidifying its position as a leading life insurance provider.

The company has faced operational and market challenges, including allegations of misconduct and fraud in April 2024, which led to a significant drop in its stock price. Despite these challenges, the company has maintained strong financial health with a 'GREAT' financial health score according to InvestingPro. This resilience underscores its commitment to financial stability and customer protection within the life insurance sector.

The company's strategic focus on innovation and customer service, along with its financial health, positions it to capitalize on future growth opportunities. By understanding the intricacies of Globe Life Insurance's Growth Strategy, investors and stakeholders can gain valuable insights into its operational dynamics and market positioning.

The transition to a virtual business model for the American Income Life (AIL) division, particularly after the pandemic, is a significant milestone. The agent count increased from over 8,000 in March 2020 to over 12,000 in November 2024. This expansion has enabled the company to issue more life insurance policies.

The company's strategic moves include maintaining a strong capital structure and liquidity position. It targets a consolidated Company Action Level RBC ratio of 300% to 320% for 2025. Innovation in underwriting automation and technology enhancements is another key focus.

The competitive advantages include brand strength and a controlled distribution force of captive and independent agents. Its low-risk products and variable cost structure allow it to serve underserved markets consistently. The company consistently performs in the top quartile among peers in terms of return on assets and equity.

The company aims to generate over 750,000 leads for its exclusive agencies in 2025. This focus on lead generation and technological advancements highlights its commitment to growth and efficiency in the competitive life insurance market. These strategies are designed to enhance its market position and customer service capabilities.

Key Financial and Operational Data

The company's financial health score is rated as 'GREAT' by InvestingPro. The consolidated Company Action Level RBC ratio target for 2025 is between 300% and 320%. The company aims to generate over 750,000 leads for its exclusive agencies in 2025, showing a strong focus on growth and market expansion.

- Agent count increased from over 8,000 in March 2020 to over 12,000 in November 2024.

- The company protects over 17 million policyholders.

- Focus on innovation in underwriting automation and technology enhancements.

- Consistent top quartile performance in return on assets and equity.

Globe Life Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Globe Life Positioning Itself for Continued Success?

The company holds a solid position in the U.S. insurance market, especially in providing life and supplemental health insurance to middle and lower-middle-income families. With approximately 17 million policies in force, it's one of the largest life insurance issuers in the country. As of January 2025, the customer loyalty, as measured by Net Promoter Score (NPS), was -14, with 41% promoters and 55% detractors.

The company's financial strength is reflected in its "A (Excellent)" rating from AM Best, showing a strong balance sheet and operating performance. However, the company faces risks from economic conditions, regulatory developments, and litigation. Recent challenges include an extortion investigation and a data breach that expanded in February 2025, adding to the regulatory scrutiny.

The company is a significant player in the U.S. life insurance market, focused on the middle and lower-middle-income demographic. Its substantial policy count, around 17 million policies, underscores its market presence. The company's financial strength is rated "A (Excellent)" by AM Best, which is a positive indicator of its stability.

The company faces risks related to economic conditions, regulatory changes, and litigation. Recent issues include an extortion investigation and a data breach that was expanded in February 2025. Changes in product competitiveness and the ability to get timely premium rate increases also pose challenges.

Globe Life projects net operating earnings per share between $13.45 and $14.05 for 2025, indicating an 11% growth at the midpoint. The company anticipates life premium revenue growth of 4.5% to 5% and health premium revenue growth of 7.5% to 8.5% in 2025. Strategic initiatives include maintaining a strong capital structure and expanding its agency force.

The company plans to maintain a strong capital structure, continue share repurchases, and leverage its investment strategy to enhance risk-adjusted returns. It also intends to expand its agency force, particularly in the American Income Life Division. The company aims to sustain and expand its profitability through continued innovation, particularly in underwriting automation and technology, to meet evolving consumer needs.

Financial Projections and Growth

For 2025, the company projects strong growth with anticipated increases in both life and health premium revenues. The projected net operating earnings per share are between $13.45 and $14.05, reflecting an expected 11% growth at the midpoint. These projections suggest a positive financial trajectory for the company.

- Life premium revenue growth: 4.5% to 5%.

- Health premium revenue growth: 7.5% to 8.5%.

- Focus on underwriting automation and technology to meet consumer needs.

- Expansion of the agency force, especially in the American Income Life Division.

For more detailed information about the company's financials and the market, you can read more in the article about Owners & Shareholders of Globe Life.

Globe Life Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Globe Life Company?

- What is Competitive Landscape of Globe Life Company?

- What is Growth Strategy and Future Prospects of Globe Life Company?

- What is Sales and Marketing Strategy of Globe Life Company?

- What is Brief History of Globe Life Company?

- Who Owns Globe Life Company?

- What is Customer Demographics and Target Market of Globe Life Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.