Essent Bundle

Unlocking the Secrets of Essent Company: How Does It Thrive?

In the ever-changing landscape of U.S. housing, understanding the players shaping the market is crucial. Essent Group Ltd. stands out as a key provider of private mortgage insurance, a service that directly impacts homeownership and the stability of the financial system. With mortgage rates and affordability constantly in the spotlight, Essent's role in mitigating risk is more important than ever.

This exploration of the Essent SWOT Analysis will dissect the Essent business model and its core operations. We'll examine how Essent Company provides its essential Essent services, generates revenue, and navigates the complexities of the mortgage industry. Investors, homebuyers, and industry professionals alike will gain valuable insights into this critical component of the financial ecosystem.

What Are the Key Operations Driving Essent’s Success?

The Essent Company operates by providing private mortgage insurance (MI) to lenders and investors in the United States. Their core offering is mortgage insurance, which protects against losses if a borrower defaults on their single-family mortgage loans. This service is primarily directed towards mortgage originators, banks, and credit unions, as well as government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac. The Essent business model centers around risk transfer and capital relief, allowing lenders to offer loans with smaller down payments and meet regulatory capital requirements.

The operational foundation of Essent services includes robust underwriting, risk management, and claims processing. They use advanced proprietary models and analytics to assess borrower creditworthiness and the risks associated with individual mortgage loans. This involves evaluating factors such as credit scores, loan-to-value (LTV) ratios, and debt-to-income (DTI) ratios. Technology development is crucial for efficient policy issuance, premium collection, and data management. Sales channels involve direct engagement with mortgage lenders and integration with loan origination systems to streamline the application process.

The company's value proposition lies in offering reliable coverage, competitive pricing, and streamlined processes. This facilitates greater access to affordable mortgage financing for homebuyers and reduces credit risk for lenders. The supply chain involves the efficient and secure exchange of mortgage loan data from lenders, which is then processed to determine insurance eligibility and pricing. Partnerships with technology providers enhance analytical capabilities and operational efficiency. Their distribution networks are built on direct relationships with lender clients across the country. A data-driven, risk-adjusted approach to underwriting, which is highlighted by strong underwriting standards and capital management, makes their operations unique and effective compared to competitors. For more insights, consider exploring the Marketing Strategy of Essent.

Essent uses sophisticated models to evaluate borrower creditworthiness and loan risk. This includes assessing credit scores, LTV ratios, and DTI ratios. Strong risk management helps maintain financial stability and ensures the long-term viability of the insurance policies.

Efficient claims processing is critical for Essent. This involves quickly and accurately assessing claims, ensuring timely payments, and maintaining customer satisfaction. Streamlined processes help maintain lender confidence.

Essent directly engages with mortgage lenders and integrates with loan origination systems. This streamlines the application and approval process for mortgage insurance. Strong relationships with lenders are essential for business growth.

Technology is crucial for policy issuance, premium collection, and data management. Efficient data management ensures accuracy and compliance. Investing in technology enhances operational efficiency.

Key Customer Benefits

Essent's operations translate into several key benefits for its customers, including reliable coverage, competitive pricing, and streamlined processes. These benefits contribute to greater access to affordable mortgage financing and reduce credit risk for lenders.

- Reliable Coverage: Provides financial protection to lenders in case of borrower default.

- Competitive Pricing: Offers mortgage insurance at attractive rates, helping lenders manage costs.

- Streamlined Processes: Simplifies the mortgage insurance application and approval process.

- Risk Reduction: Reduces the credit risk for lenders, making them more willing to offer loans.

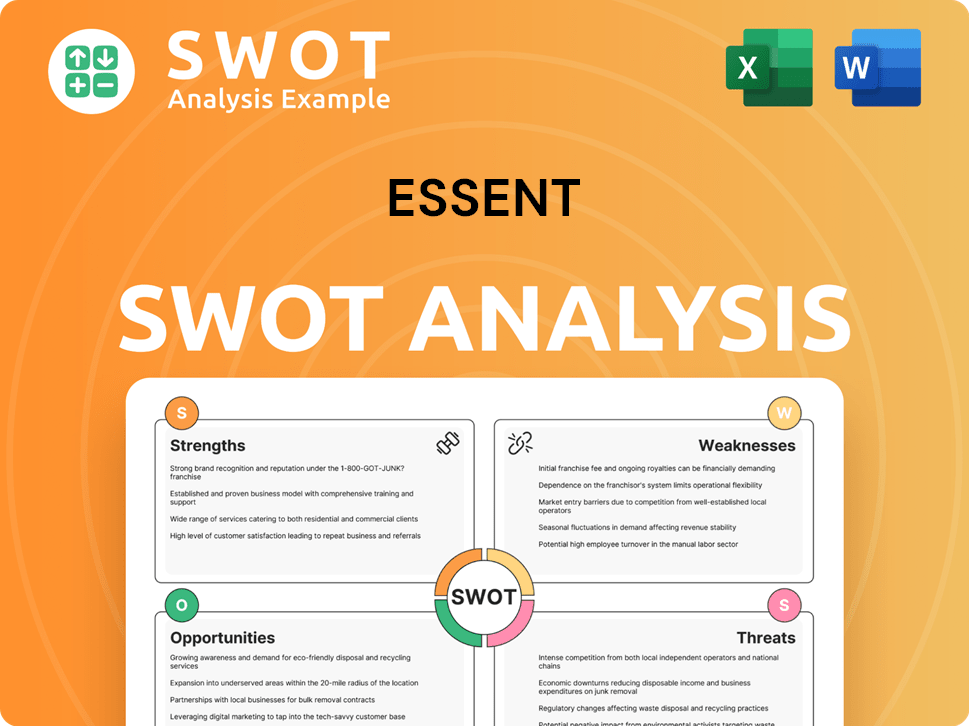

Essent SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Essent Make Money?

The primary revenue stream for Essent Group Ltd. comes from premiums on its private mortgage insurance (PMI) policies. This core business generates the vast majority of its income. In 2023, Essent reported total revenues of approximately $1.15 billion, with net premiums earned being the most significant contributor.

Essent's monetization strategy is centered on charging lenders a premium to cover the credit risk of a portion of their mortgage loan portfolios. These premiums are usually paid either upfront or, more commonly, through recurring monthly or annual payments. The company's business model is designed to provide financial protection to lenders, allowing more people to become homeowners.

A smaller portion of Essent's revenue comes from investment income generated from its investment portfolio. This portfolio consists of accumulated premiums that have not yet been paid out as claims. While not the main focus, strategic management of this portfolio contributes to the company's overall profitability. The company's revenue streams are relatively consistent across regions, focusing primarily on the U.S. single-family mortgage market. There are no significant differences in revenue mix by product line, as private mortgage insurance is its singular core offering.

Revenue Stream Details

Essent's revenue generation is primarily driven by premiums from private mortgage insurance. The company focuses on optimizing its premium rates and risk selection. Understanding the Competitors Landscape of Essent can provide insights into its market position.

- Premiums from PMI: The main source of revenue, collected from lenders.

- Investment Income: Revenue from managing the investment portfolio.

- Consistent Revenue Streams: Primarily focused on the U.S. single-family mortgage market.

- Strategic Focus: Continuous refinement of underwriting models and pricing strategies.

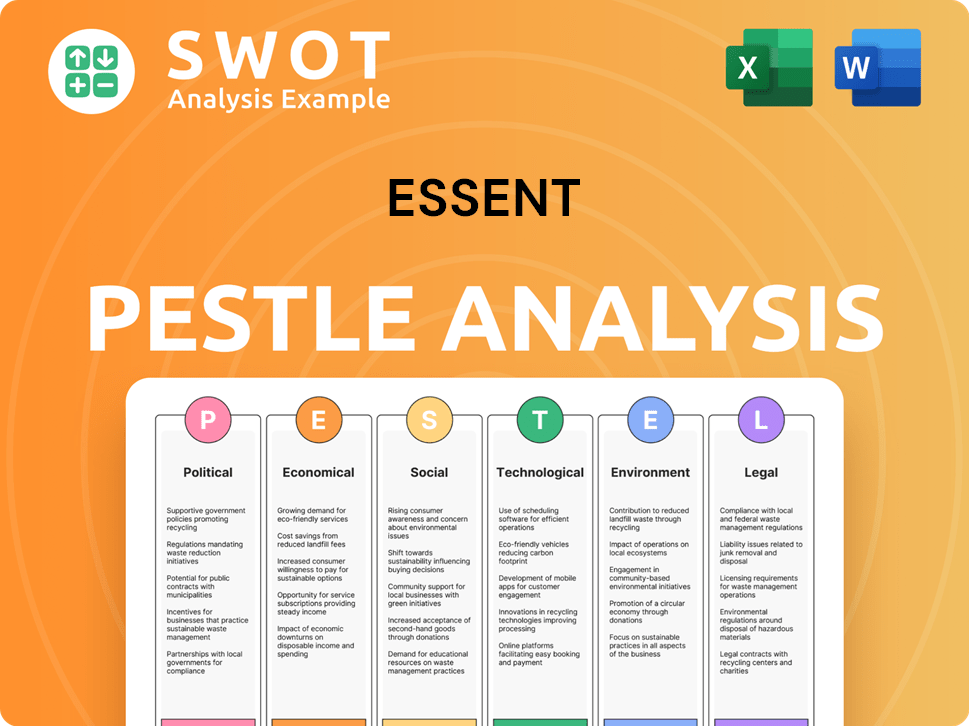

Essent PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Essent’s Business Model?

The company, has achieved several key milestones that have significantly influenced its financial and operational performance. A pivotal moment was its initial public offering (IPO) in 2013, which provided the necessary capital for expansion and solidified its position as a publicly traded entity within the mortgage insurance sector. Subsequent achievements include consistent growth in new insurance written (NIW) and in-force policies, demonstrating its increasing market penetration and lender acceptance. For instance, in the fourth quarter of 2023, the company reported new insurance written of $13.6 billion.

Strategic initiatives have included a disciplined approach to underwriting, which has allowed the company to maintain a strong credit profile for its insured portfolio, even amidst economic uncertainties. The company has also strategically focused on operational efficiency and technology integration to streamline processes and enhance its service offerings to lenders. These efforts are crucial to maintaining a competitive edge in the dynamic mortgage insurance market, ensuring the provision of reliable services.

Navigating operational challenges, such as fluctuating interest rates, shifts in housing market conditions, and evolving regulatory landscapes, has been crucial for the company's success. The company has adapted by maintaining rigorous underwriting standards, investing in technology to enhance analytics and customer experience, and actively managing its capital to ensure financial strength. This proactive approach is vital for sustaining the company's position and ensuring its ability to provide consistent and reliable services within the mortgage finance landscape.

The company's competitive advantages are multifaceted, stemming from its strong brand reputation and technological leadership. Its advanced underwriting and risk management platforms provide a significant edge, supported by economies of scale as the in-force portfolio expands. The company's robust financial position, as reflected in strong credit ratings, builds confidence among lenders and investors.

To remain competitive, the company constantly monitors housing market dynamics, technological advancements, and regulatory changes. This proactive stance ensures that its business model remains resilient and adaptable to the evolving mortgage finance landscape. For more insights into the company's growth strategy, you can refer to Growth Strategy of Essent.

Key Strengths of Essent

The company's strengths lie in its robust financial health and operational efficiency. The company's ability to adapt to market changes and maintain strong relationships with lenders is also a key advantage. These factors contribute to the company's ability to provide reliable mortgage insurance services.

- Strong Brand Reputation: Built on reliability and efficient service.

- Technology Leadership: Advanced underwriting and risk management platforms.

- Economies of Scale: Lower per-unit costs with an expanding portfolio.

- Financial Strength: Robust capital position and strong credit ratings.

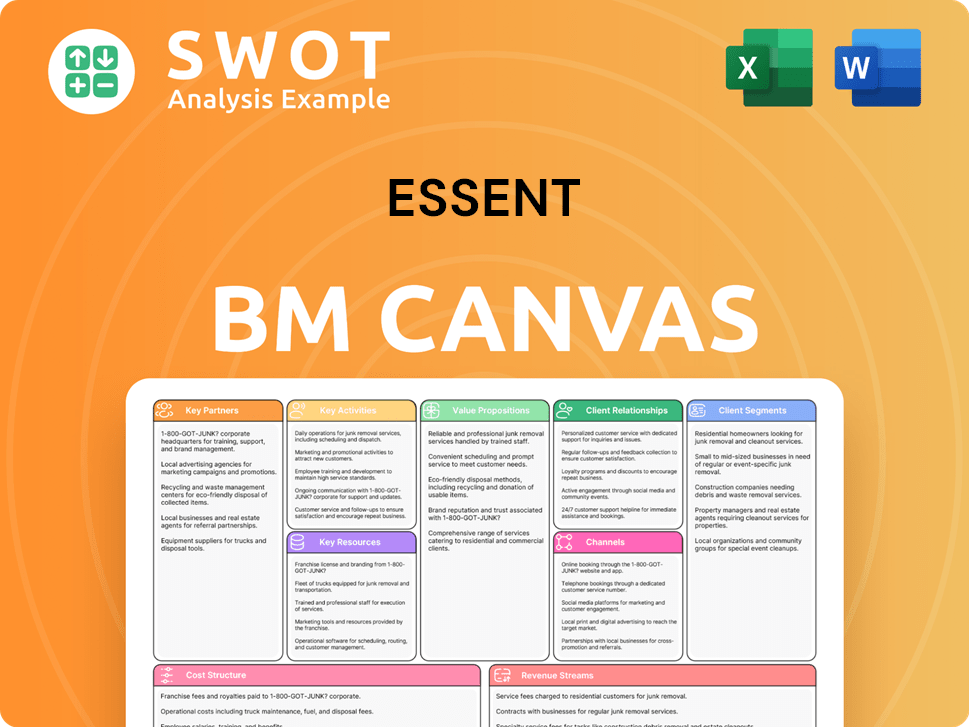

Essent Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Essent Positioning Itself for Continued Success?

The U.S. private mortgage insurance industry sees Essent Group Ltd. as a key player, holding a strong competitive position. They are among the leading providers, with a notable market share and a broad customer base within the mortgage lending sector. Their customer loyalty remains high due to reliable service, competitive pricing, and strong financial backing. Essent's operations are primarily focused on the U.S. market, serving a nationwide network of mortgage originators.

However, Essent faces risks such as regulatory changes affecting GSEs or capital requirements. New competitors or technological disruptions in the mortgage finance sector also pose threats. Economic downturns, rising interest rates, or housing value declines could increase mortgage defaults and claims, impacting profitability. Changing consumer preferences could also influence the demand for Essent's services.

Essent holds a leading position in the U.S. private mortgage insurance market. They have a strong market share and a broad customer base, primarily serving mortgage lenders. Their reach is focused on the U.S. market, serving a nationwide network of mortgage originators.

Regulatory changes, new competitors, and economic downturns pose significant risks. Changes in GSE policies or capital requirements can impact operations. Economic fluctuations and shifts in consumer preferences add to the uncertainty.

Essent is focused on disciplined underwriting, optimizing capital structure, and enhancing technology. They aim to capitalize on the continued demand for mortgage financing. Their focus on prudent risk selection and efficient operations is expected to underpin profitability.

The company is committed to responsible growth and strong risk management. They are continuously improving their analytical tools and platforms. Leadership consistently emphasizes delivering value to shareholders.

Essent's strategic initiatives include disciplined underwriting and technological enhancements. The company is focused on responsible growth and risk management. They are also continuously improving their analytical tools. For more information on Essent's target market, you can read this article: Target Market of Essent. The company's focus on prudent risk selection and efficient operations is expected to underpin its profitability and allow it to navigate potential challenges in the housing and financial markets. In 2024, the mortgage insurance industry saw approximately $8.5 billion in premiums written, with Essent being a significant contributor. The company continues to adapt to evolving market conditions, demonstrating resilience in the face of economic uncertainties.

Key Factors for Success

Essent's success depends on several key factors in the mortgage insurance industry. Maintaining strong customer relationships and adapting to regulatory changes are crucial.

- Disciplined Underwriting: Maintaining strict standards.

- Technology Investments: Improving risk assessment.

- Risk Management: Adapting to economic changes.

- Customer Focus: Delivering reliable services.

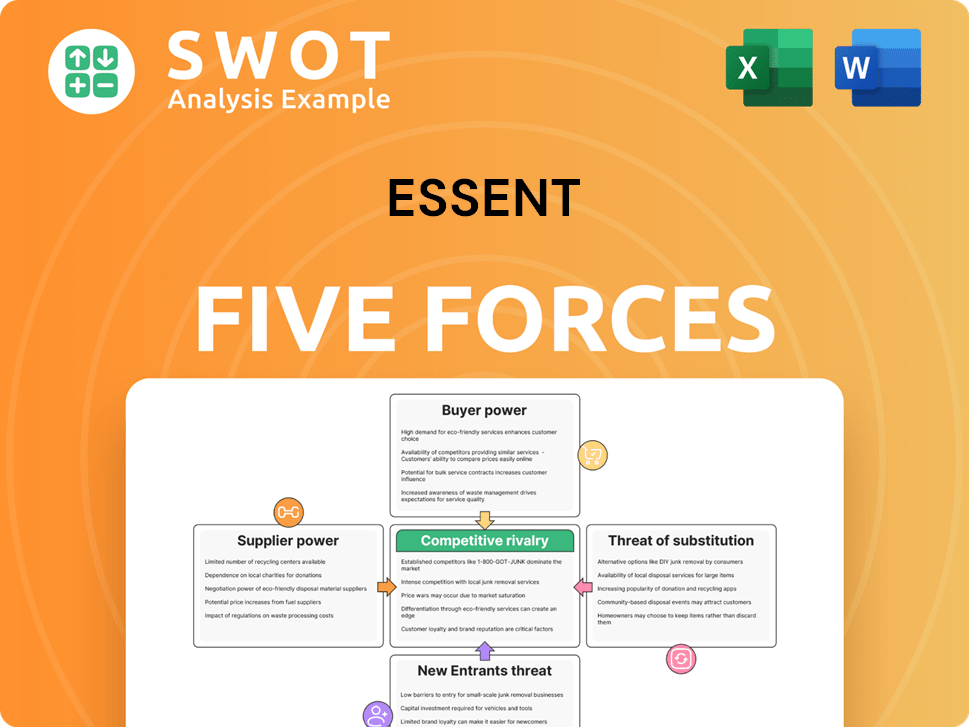

Essent Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Essent Company?

- What is Competitive Landscape of Essent Company?

- What is Growth Strategy and Future Prospects of Essent Company?

- What is Sales and Marketing Strategy of Essent Company?

- What is Brief History of Essent Company?

- Who Owns Essent Company?

- What is Customer Demographics and Target Market of Essent Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.