Doral Financial Corp. Bundle

What Went Wrong at Doral Financial Corp.?

Doral Financial Corporation, once a major player in Puerto Rico's financial landscape, offered a wide array of Doral Financial Corp. SWOT Analysis, including commercial and retail banking, mortgage lending, and investment services. Founded in 1972, the company rapidly expanded, accumulating billions in assets and establishing a significant presence in key markets. Understanding the inner workings of Doral Financial, including its operational model and revenue streams, is vital for anyone studying the banking industry.

The story of Doral Financial Corp. provides a crucial case study in the financial services sector. Examining its corporate structure, strategic decisions, and ultimate downfall offers valuable lessons for investors and business strategists alike. Delving into the company's history, from its peak to its eventual FDIC receivership in 2015, reveals critical insights into risk management and the complexities of the banking industry. Exploring the financial performance of Doral Bank and its subsidiaries helps to understand the challenges faced by the company.

What Are the Key Operations Driving Doral Financial Corp.’s Success?

Doral Financial Corp. (DFC) centered its operations on providing a wide array of financial services, primarily within the Puerto Rico market. Its core business focused on commercial and retail banking, mortgage lending, and investment services, all channeled through its subsidiary, Doral Bank. The company aimed to create value by emphasizing high-quality customer service and maintaining an extensive network of retail mortgage origination branches across Puerto Rico.

The company's operational model involved significant activities in mortgage origination and servicing. It also purchased loans and mortgage servicing rights from third parties. Furthermore, DFC specialized in originating construction loans and financing new housing developments. Through its commercial banking operations via Doral Bank PR, it operated numerous branches throughout Puerto Rico, offering a variety of mortgage products similar to its mortgage banking units. Doral Bank extended its reach to the New York City metropolitan area and Florida through its federal savings bank subsidiary, Doral Bank, F.S.B.

The value proposition of Doral Financial stemmed from its diverse financial offerings and its established presence in Puerto Rico, which fostered a strong base of customer relationships. DFC leveraged its reputation as a leading mortgage banker and the fourth-largest commercial bank in Puerto Rico to cross-sell various financial services to its client base, which exceeded 300,000 accounts. For more information on the ownership structure, you can read the article about Owners & Shareholders of Doral Financial Corp.

Doral Financial Corp. primarily focused on commercial and retail banking, mortgage lending, and investment services. These services were delivered through Doral Bank, its main subsidiary, which operated extensively in Puerto Rico. The company's operations were designed to meet diverse financial needs, offering products like checking and savings accounts, commercial lending, and institutional securities services.

The operational processes involved mortgage origination, servicing, and the purchase of loans. Doral Financial also specialized in construction loans and financing for new housing. Doral Bank PR operated numerous branches, offering various mortgage products, while Doral Bank, F.S.B. expanded its reach to the New York City metropolitan area and Florida.

The value proposition centered on diversified financial offerings and a strong presence in Puerto Rico. Doral Financial leveraged its reputation to cross-sell services to its client base. Its branch network was crucial for direct customer interaction and service delivery, while digital banking platforms expanded its reach.

Doral Financial offered a wide range of services, including checking and savings accounts, commercial lending, and institutional securities services. The company's focus on customer service and its extensive branch network were key elements of its strategy. These services were designed to cater to the diverse financial needs of its clients.

Key Operational Highlights

Doral Financial's operations were primarily focused on the Puerto Rico market, providing a comprehensive suite of financial services. The company's strategy involved a blend of traditional banking services and specialized financial products. The company aimed to offer a wide range of financial solutions to meet the diverse needs of its customers.

- Mortgage Origination and Servicing: A core function of DFC's operations.

- Commercial and Retail Banking: Offered through Doral Bank, with a significant branch network.

- Investment Services: Provided to a broad customer base.

- Customer Base: Exceeded 300,000 accounts, highlighting its market reach.

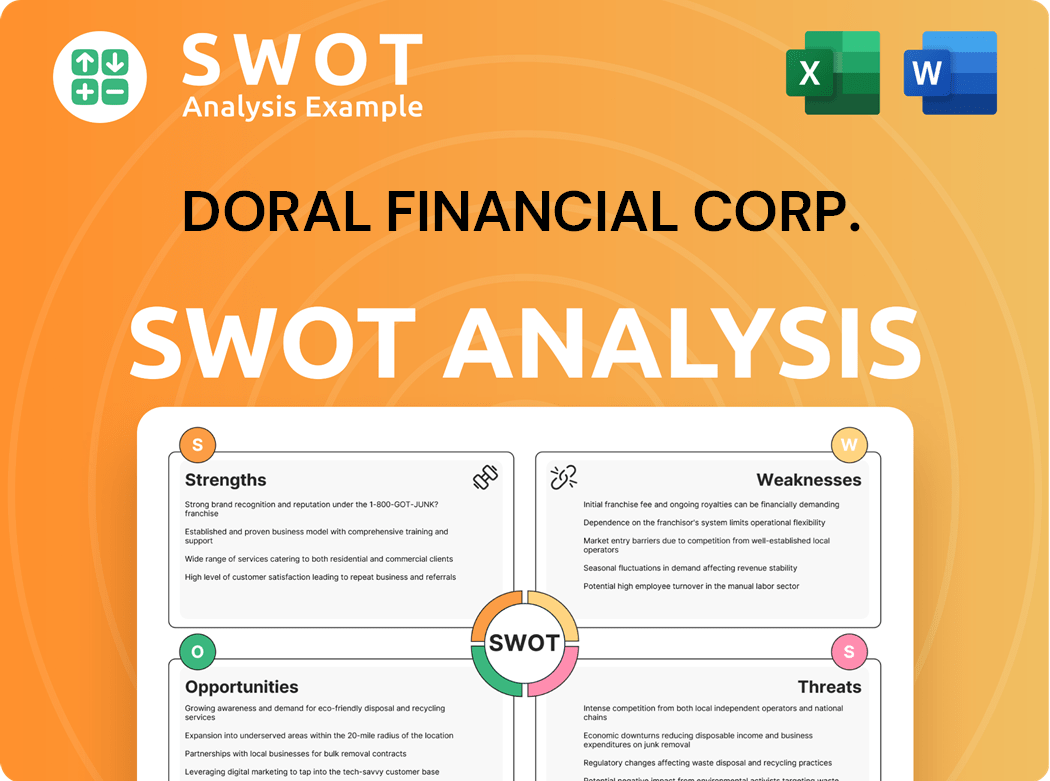

Doral Financial Corp. SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Doral Financial Corp. Make Money?

The revenue streams and monetization strategies of Doral Financial Corp. were centered around a diversified portfolio of financial services. The company's primary focus was on mortgage lending, commercial and retail banking, and investment services. This approach allowed Doral Financial to generate income from various sources within the financial sector.

Doral Financial's business model aimed at maximizing net interest income, particularly through its mortgage banking operations. The company strategically held mortgage-backed securities, especially Puerto Rico tax-exempt mortgage-backed securities, to generate revenue. Additionally, the company expanded its services through its subsidiaries, including Doral Bank and Doral Securities, Inc., to offer a wider range of financial products.

The company's monetization strategies involved leveraging its extensive branch network for retail and mortgage banking activities. Doral Financial also aimed to cross-sell services to its customer base. A strategic shift towards becoming a more traditional lending institution, with less emphasis on trading, was also implemented to provide a more stable income stream. You can learn more about the Marketing Strategy of Doral Financial Corp.

Key Revenue Streams and Monetization Strategies

Doral Financial Corp. generated revenue through a mix of financial services, with a strong emphasis on mortgage lending. Monetization strategies included leveraging its branch network and cross-selling services.

- Mortgage Lending: A primary revenue stream, with a focus on the Puerto Rico market.

- Commercial and Retail Banking: Offered through Doral Bank, providing various loan and deposit products.

- Investment Services: Conducted through Doral Securities, Inc., including brokerage, financial advisory, and investment banking services.

- Insurance Agency: Doral Insurance Agency, Inc., contributed to revenue through insurance services.

- Strategic Shift: Moving towards a more traditional lending model to stabilize income.

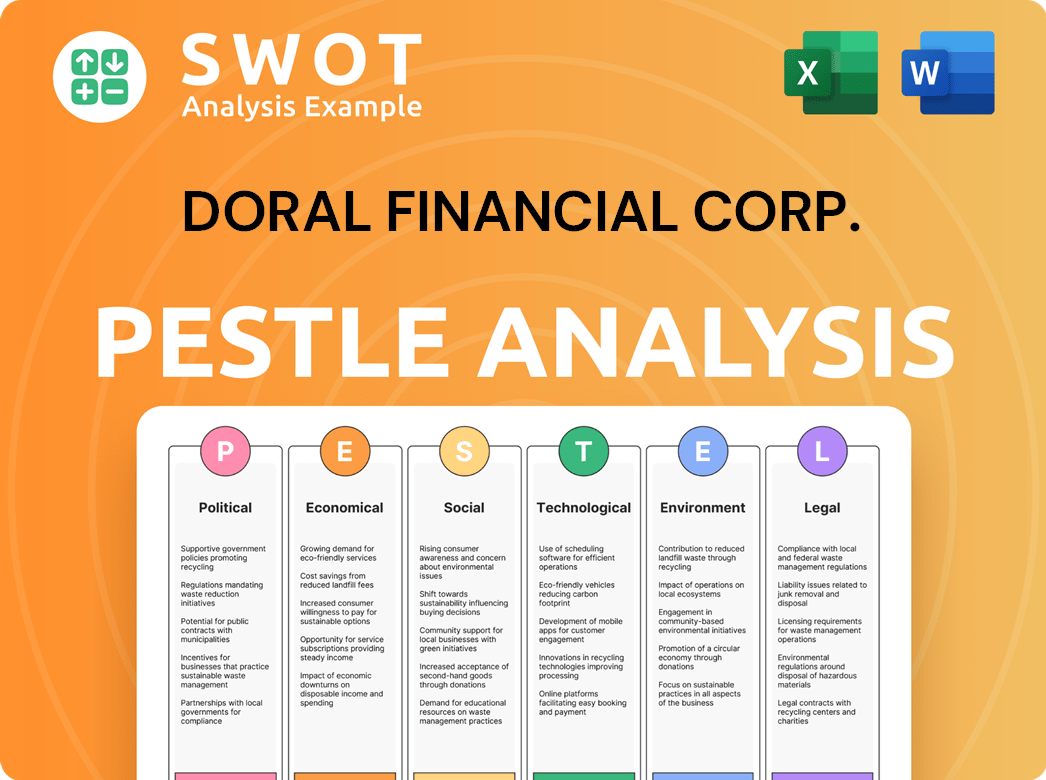

Doral Financial Corp. PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Doral Financial Corp.’s Business Model?

The story of Doral Financial Corp. is marked by significant milestones and strategic shifts that ultimately shaped its trajectory within the financial services sector. Initially founded in 1972, the company's banking arm, Doral Bank, was established in 1981 as a mutually owned federal savings bank. A pivotal moment occurred in September 1993 when Doral Financial Corporation acquired and recapitalized the bank, setting the stage for its future expansion.

Doral Financial's strategic moves included converting the bank's charter to a state non-member bank in October 1997, aiming to boost its market presence. By December 2004, the company's total assets reached a peak of $11.2 billion. The company also broadened its footprint beyond Puerto Rico, opening its first branch in New York in 1999 and establishing operations in the New York City metropolitan area and Florida.

However, Doral Financial faced considerable operational and market challenges. In April 2005, the company announced the need to restate financial statements from 2000 to 2004 due to irregularities in its mortgage business. The company also grappled with regulatory compliance issues and a dispute with the Puerto Rican government over a $230 million tax refund, significantly impacting its capital position. These issues ultimately led to Doral Bank being deemed 'critically undercapitalized' by regulators.

Doral Financial Corp. was founded in 1972. Doral Bank, the banking subsidiary, was established in 1981. The acquisition and recapitalization of Doral Bank by Doral Financial Corporation occurred in September 1993.

The bank converted its charter to a state non-member bank in October 1997. Expansion into New York and Florida began in 1999. Doral Financial aimed to become a leader in mortgage banking.

Doral Financial's competitive edge historically stemmed from its established presence in Puerto Rico. It focused on mortgage banking and offered diversified financial services. The company leveraged its branch network and a customer base of over 300,000 clients for cross-selling.

The company faced financial difficulties, including regulatory issues and a tax refund dispute. Doral Bank was closed by the Commissioner of Financial Institutions of Puerto Rico on February 27, 2015. Banco Popular de Puerto Rico acquired most of Doral Bank's operations. Doral Financial Corporation filed for Chapter 11 bankruptcy on March 11, 2015.

Detailed Analysis

Doral Financial Corp. aimed to be a major player in the banking industry. The company's business model included a strong emphasis on mortgage banking and providing a range of financial services. The company's history is a case study in the challenges faced in the financial services sector, as further detailed in this article about Growth Strategy of Doral Financial Corp.

- Doral Financial Corp. had a significant customer base.

- The company's expansion into new markets aimed to increase its market share.

- Regulatory issues and capital problems led to its eventual closure.

- The bankruptcy filing marked the end of its operations.

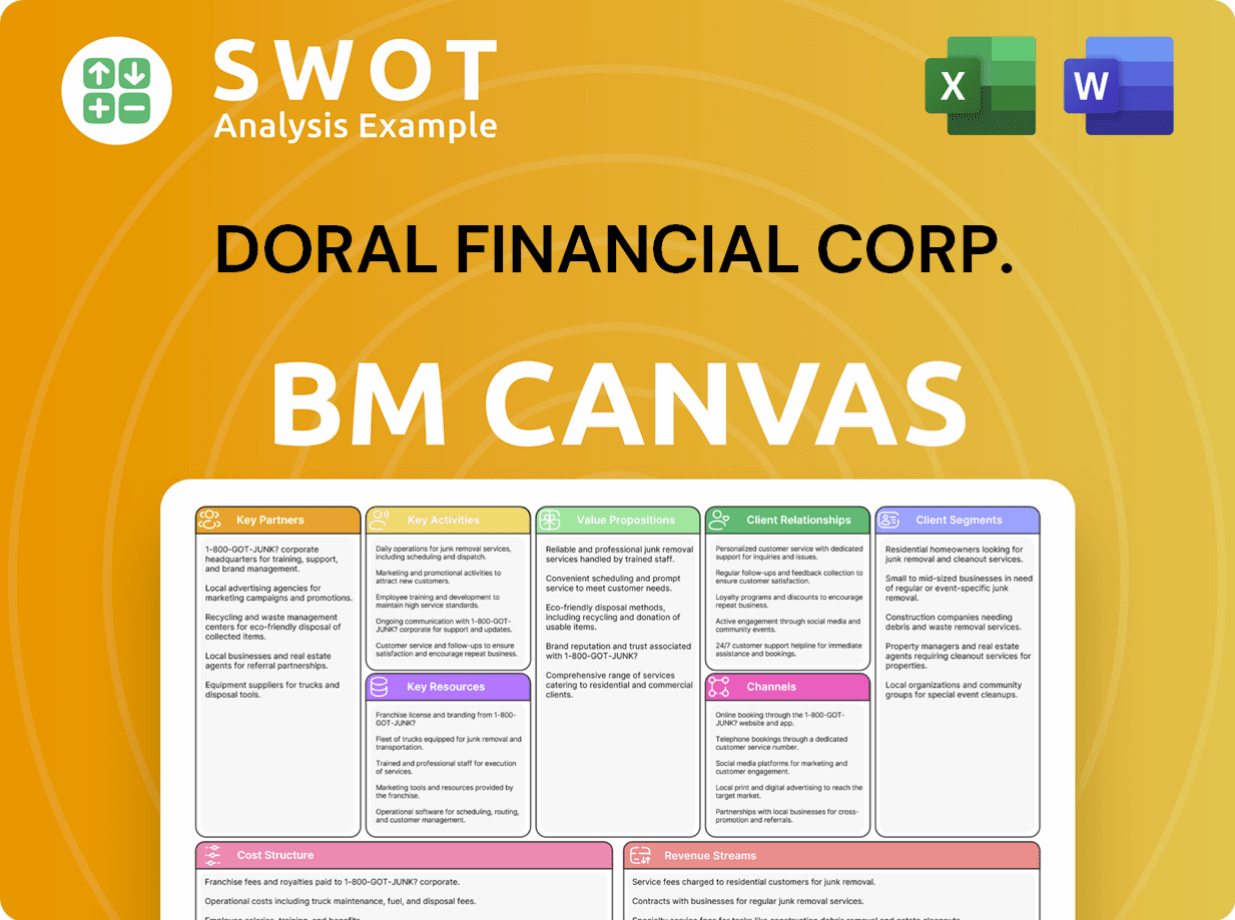

Doral Financial Corp. Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Doral Financial Corp. Positioning Itself for Continued Success?

Before its 2015 receivership, Doral Financial Corp held a significant position in Puerto Rico's financial landscape. As a leading mortgage banking institution and the fourth-largest commercial bank, it served over 300,000 clients. Its strong presence in mortgage originations and diverse offerings were key to its market standing.

However, Doral Financial faced considerable challenges. Financial struggles, including restatements and regulatory capital issues, were major concerns. A dispute over a $230 million tax refund and increased regulatory pressure from the FDIC further weakened its position. The struggling Puerto Rican economy amplified these difficulties.

Doral Financial Corp. was a prominent player in Puerto Rico's financial services sector. It was recognized as a leading mortgage lender and a significant commercial bank. The company had a substantial customer base, reflecting its importance in the local banking industry.

The company faced significant risks, including financial instability and regulatory scrutiny. Disputes over tax refunds and economic downturns in Puerto Rico added to these challenges. These factors ultimately led to the company's downfall.

Due to its closure, there is no direct future for Doral Financial Corp. Its assets were acquired by other entities to stabilize the Puerto Rican banking sector. The industry in 2024-2025 shows robust profitability, but faces economic and regulatory pressures.

In 2024, the Puerto Rico banking industry showed a pre-tax return on equity exceeding 20%. Non-performing loans reached a low of 1.75%. The sector is also undergoing digital transformation and focusing on fintech solutions.

Further Insights into Doral Financial Corp.

Doral Financial's history highlights the risks in the banking industry. The company's collapse underscores the importance of financial stability. The current Puerto Rican banking sector faces ongoing economic and regulatory challenges.

- The company's difficulties included regulatory non-compliance.

- Economic conditions in Puerto Rico significantly impacted the company.

- The FDIC played a crucial role in addressing the financial crisis.

- The acquisition of Doral's assets aimed to stabilize the market.

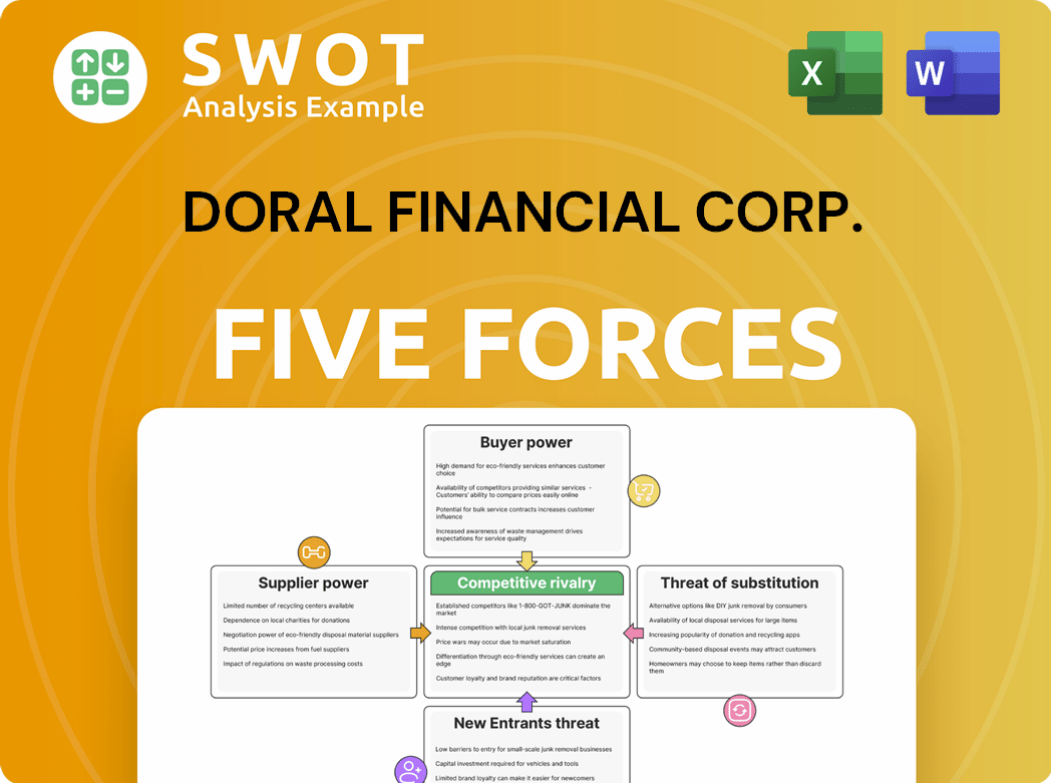

Doral Financial Corp. Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Doral Financial Corp. Company?

- What is Competitive Landscape of Doral Financial Corp. Company?

- What is Growth Strategy and Future Prospects of Doral Financial Corp. Company?

- What is Sales and Marketing Strategy of Doral Financial Corp. Company?

- What is Brief History of Doral Financial Corp. Company?

- Who Owns Doral Financial Corp. Company?

- What is Customer Demographics and Target Market of Doral Financial Corp. Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.