Columbia Bank Online Bundle

How is Columbia Bank Navigating the Financial Landscape?

Columbia Bank, a key Columbia Bank SWOT Analysis, is a prominent financial institution serving New Jersey and beyond, offering a wide array of

This exploration delves into the inner workings of Columbia Bank, examining its financial performance, including its

What Are the Key Operations Driving Columbia Bank’s Success?

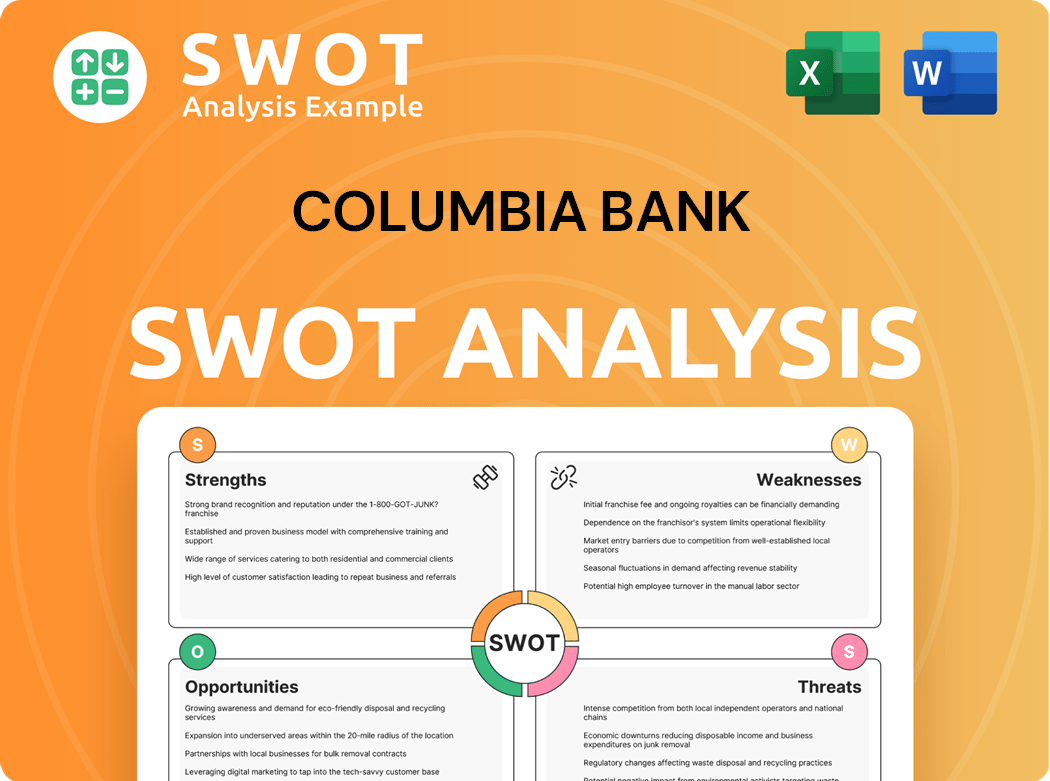

Columbia Bank, a financial institution, creates and delivers value through a diverse array of financial products and services. These offerings are tailored for individuals, families, and businesses, primarily within the New Jersey market. The bank's core services include various deposit accounts, such as checking and savings, and a comprehensive suite of loan products. This includes both commercial and consumer loans, such as affordable home loans.

The bank also provides wealth management solutions to help clients manage their financial assets. This approach allows Columbia Bank to cater to diverse customer preferences, offering both traditional relationship-based banking and seamless digital access. This dual approach allows the bank to cater to diverse customer preferences, offering both traditional relationship-based banking and seamless digital access.

Operationally, Columbia Bank leverages an extensive branch network and digital platforms to serve its customers. This includes a focus on digital banking solutions, such as a new business online banking platform introduced in 2024, and a redesigned and modernized website as of Q1 2025. This dual approach allows the bank to cater to diverse customer preferences, offering both traditional relationship-based banking and seamless digital access.

Columbia Bank provides a range of financial products, including deposit accounts (checking and savings) and various loan products. These loans include commercial and consumer options. The bank also offers wealth management services to assist clients with their financial assets.

The bank utilizes a network of branches and digital platforms to serve its customers. As of December 31, 2024, Columbia Bank had 68 full-service branches and 4 regional lending centers. They also invest in digital banking solutions, including a new business online banking platform and a redesigned website.

Columbia Bank emphasizes a community-focused approach. In 2024, the bank originated 12 Small Business Association (SBA) loans totaling approximately $25.0 million and 32 community development loans totaling approximately $68.8 million. Their supply chain is primarily localized within New Jersey.

The bank has been actively renovating branches, incorporating modern designs and digital displays. They have also introduced a new business online banking platform in 2024 and a redesigned website in Q1 2025. These updates aim to improve the customer experience.

Key Differentiators

Columbia Bank distinguishes itself through its community focus, personalized service, and ongoing investments in technology. This approach sets it apart from larger commercial banks. The bank's commitment to local initiatives and partnerships further strengthens its ties within the community.

- Extensive branch network and digital platforms.

- Strong community involvement, including SBA and community development loans.

- Focus on personalized service and local needs.

- Continuous investment in technology and customer experience.

Columbia Bank Online SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Columbia Bank Make Money?

Understanding the revenue streams and monetization strategies of Columbia Bank is crucial for evaluating its financial performance. The bank primarily generates revenue through its core banking activities, with a significant portion derived from net interest income. Additionally, Columbia Bank leverages non-interest income sources and employs various strategies to optimize its revenue generation and customer engagement.

The bank's approach involves a combination of interest-based and fee-based income, along with strategic financial management to enhance profitability. This includes managing its balance sheet to improve net interest margins and offering bundled services to attract and retain customers. The following sections will delve into specific revenue streams and monetization strategies employed by Columbia Bank.

For the quarter ended March 31, 2025, net interest income was a substantial contributor to Columbia Bank's revenue. It reached $50.3 million, marking a 19.3% increase from $42.2 million in the same period of 2024. This growth was fueled by higher interest income from loans and securities, along with reduced interest expenses on deposits and borrowings. The net interest margin also improved, rising by 36 basis points to 2.11% for the quarter ended March 31, 2025, compared to 1.75% in the first quarter of 2024.

Non-Interest Income and Strategic Initiatives

Beyond net interest income, Columbia Bank also generates revenue through non-interest income sources. In the first quarter of 2025, non-interest income was $8.5 million, reflecting a $1.0 million or 13.7% increase from $7.5 million in the first quarter of 2024. This rise was largely due to the absence of a $1.3 million loss on securities transactions recorded in the 2024 period and a $475,000 increase in fees from commercial account treasury services. The bank's strategic balance sheet repositioning in the fourth quarter of 2024, which involved the sale of debt securities, was undertaken to enhance future earnings potential and expand its net interest margin, indicating an active approach to optimizing revenue generation.

- Net Interest Income: The primary source, driven by interest earned on loans and investments, less interest paid on deposits and borrowings.

- Non-Interest Income: Includes fees from services like treasury services and other banking activities.

- Bundled Services and Tiered Pricing: Strategies to attract and retain customers through tailored service packages.

- Strategic Balance Sheet Management: Activities like selling debt securities to improve earnings and margins.

Columbia Bank Online PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Columbia Bank’s Business Model?

The following details the key milestones, strategic moves, and competitive advantages of Columbia Bank. The bank's recent activities highlight its commitment to growth, technological advancement, and community engagement. These elements are crucial for understanding the bank's current position and future prospects within the financial sector.

Columbia Bank has strategically expanded its operations and enhanced its technological capabilities to improve customer service and operational efficiency. These efforts, combined with a focus on community involvement, have positioned the bank to meet the evolving needs of its customers and adapt to market changes. The bank's approach includes both internal improvements and external initiatives to strengthen its market presence and customer relationships.

A significant milestone was the consolidation and integration of Freehold Bank in October 2024, which aimed to expand the bank's regional presence and streamline operations. In preparation for this, Columbia Bank and its foundation awarded over $100,000 in grants to 18 organizations in the Freehold area. These actions underscore Columbia Bank's strategic growth and commitment to community support.

Columbia Bank has continuously invested in its technology infrastructure, including launching a new business online banking platform and adopting a new customer relationship management (CRM) tool in 2024. Further investments planned for 2025 include continued enhancements to its customer-focused technology stack. Additionally, the bank renovated seven branch locations in 2024, incorporating modern designs and digital displays.

Columbia Bank's competitive advantages include its strong brand recognition as a reliable, community-based financial institution with nearly 100 years of service in New Jersey. The bank emphasizes personalized, relationship-based banking combined with expanding digital solutions. Community involvement, such as the Advancing Access Program and financial literacy initiatives, strengthens its ties within the communities it serves.

In 2024, Columbia Bank navigated economic and political uncertainties while maintaining its focus on growth, particularly in its commercial loan products. The bank's ability to adapt to market conditions and competitive threats is supported by its strong customer relationships and community focus. To learn more about the bank's approach, consider reading about the Growth Strategy of Columbia Bank.

Key Takeaways

Columbia Bank's strategic moves and community focus have positioned it for continued growth and customer satisfaction. Recent investments in technology and physical infrastructure, along with a commitment to community engagement, highlight its dedication to adapting to market changes and meeting customer needs.

- Consolidation of Freehold Bank in October 2024 expanded regional presence.

- Continued investment in technology, including a new business online banking platform.

- Strong brand recognition and community involvement provide a competitive edge.

- Focus on personalized banking and digital solutions enhances customer service.

Columbia Bank Online Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Columbia Bank Positioning Itself for Continued Success?

Columbia Bank, a significant independent financial institution, holds a strong position within the New Jersey banking sector. As of December 31, 2024, the bank managed approximately $10.4 billion in assets, supported by a diverse deposit base exceeding 215,000 accounts. This community bank differentiates itself through personalized service and community engagement, fostering customer loyalty.

However, the bank faces various challenges. These include risks from economic slowdowns, interest rate uncertainties, and competitive pressures from larger institutions and fintech. Concerns about credit quality and volatility in the mortgage business also pose potential risks. Understanding these factors is crucial for a comprehensive assessment of Columbia Bank's performance and future prospects.

Columbia Bank's position in the New Jersey market is strong, with approximately $10.4 billion in assets as of late 2024. It competes with other regional and national banks, as well as fintech companies. The bank's focus on customer service and community involvement helps it stand out.

Key risks for Columbia Bank include economic slowdowns, interest rate changes, and competition. Integration challenges from acquisitions and 'credit noise' are also potential concerns. Volatility in the mortgage business presents another risk factor.

Columbia Bank plans strategic initiatives to enhance profitability. This includes investing in technology, expanding its branch network, and optimizing revenue streams. The bank aims to leverage its community roots and digital advancements for sustained growth.

In 2025, Columbia Bank is focused on technology investments to improve customer experience and drive revenue. Branch network expansion, supported by efficiencies from 2024 consolidations, is also a key strategy. The bank aims to strengthen its non-interest income and wealth management services.

Strategic Focus and Opportunities

Columbia Bank's future strategy emphasizes customer-centric technology and branch network expansion. The bank aims to optimize its revenue structure, focusing on non-interest income and wealth management. The bank's commitment to prudent risk management and customer service, as well as its digital and strategic expansions, positions it to maintain its market position and create value.

- Continued investment in technology to enhance customer experience.

- Expansion of the branch network, leveraging savings from prior consolidations.

- Strengthening non-interest income and wealth management services.

- Prudent risk management and commitment to customer service.

For those interested in understanding the customer base, consider exploring the Target Market of Columbia Bank. This analysis provides insights into the demographics and financial behaviors of the bank's customers, which is essential for strategic planning and growth initiatives.

Columbia Bank Online Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Columbia Bank Company?

- What is Competitive Landscape of Columbia Bank Company?

- What is Growth Strategy and Future Prospects of Columbia Bank Company?

- What is Sales and Marketing Strategy of Columbia Bank Company?

- What is Brief History of Columbia Bank Company?

- Who Owns Columbia Bank Company?

- What is Customer Demographics and Target Market of Columbia Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.