Bank of India Bundle

How Does Bank of India Thrive in India's Financial Landscape?

Bank of India (BOI), a cornerstone of the Indian banking sector, has consistently demonstrated its resilience and growth. With a substantial 62% year-on-year profit surge in early 2024, the public sector bank showcases its pivotal role in India's economic expansion. Its extensive network and comprehensive financial services make it a key player both domestically and internationally.

This analysis aims to dissect the operational framework of Bank of India, exploring its core functions and revenue streams. From retail and corporate banking to international services, BOI offers a wide array of financial services. Understanding its operations is crucial for investors, customers, and industry observers alike, especially when considering the Bank of India SWOT Analysis.

What Are the Key Operations Driving Bank of India’s Success?

Bank of India (BOI) is a prominent public sector bank in India, offering a wide range of banking and financial services. Its core operations focus on serving diverse customer segments, including individuals, small and medium enterprises (SMEs), large corporations, and institutional clients. BOI's value proposition centers on providing accessible, convenient, and comprehensive financial solutions tailored to meet the varied needs of its customers.

The bank's offerings span deposit products like savings accounts and fixed deposits, alongside a diverse portfolio of loans. These loans include retail options such as housing, auto, and personal loans, as well as agricultural and corporate loans. Additionally, BOI provides credit cards, debit cards, and investment products like mutual funds and government bonds. This comprehensive approach ensures that BOI caters to a wide spectrum of financial requirements.

BOI's operational processes are multifaceted, designed to support its extensive service offerings. Retail banking relies on a vast branch network and robust digital platforms for online and mobile banking. Corporate banking involves specialized relationship management teams and structured finance solutions. The international banking division handles foreign exchange services, trade finance, and remittances. BOI's focus on digital transformation and its broad reach, particularly in semi-urban and rural areas, are key differentiators.

BOI's banking operations are supported by an extensive network of branches and ATMs across India. As of March 31, 2023, the bank had 5,100 branches and 5,545 ATMs. These physical touchpoints are crucial for customer service and transaction processing, especially in areas with limited digital infrastructure.

BOI has significantly invested in digital banking to enhance customer experience and operational efficiency. The bank offers online banking, mobile banking apps, and digital payment solutions. These digital platforms enable customers to manage their accounts, make transactions, and access various banking services remotely, improving convenience and accessibility.

BOI's financial performance reflects its operational efficiency and market position. For the fiscal year 2023, the bank reported a net profit of ₹4,023 crore. The bank's total business stood at ₹10.54 lakh crore. These figures highlight the bank's robust financial health and its ability to generate value for its stakeholders.

BOI is committed to providing excellent customer service through multiple channels. Customers can access support through branches, online portals, mobile apps, and customer service helplines. The bank's focus on customer satisfaction is evident in its efforts to streamline processes and resolve customer queries efficiently.

Key Features of BOI's Operations

BOI's operations are characterized by a blend of traditional banking and digital innovation, ensuring a wide reach and enhanced customer experience. The bank's focus on digital transformation, coupled with its extensive branch network, allows it to serve a diverse customer base effectively.

- Extensive Branch Network: Provides physical access to banking services, particularly in rural and semi-urban areas.

- Digital Banking Platforms: Offers online and mobile banking for convenient account management and transactions.

- Diverse Product Portfolio: Includes savings accounts, loans, credit cards, and investment products to meet various financial needs.

- Customer-Centric Approach: Focuses on providing excellent customer service through multiple channels.

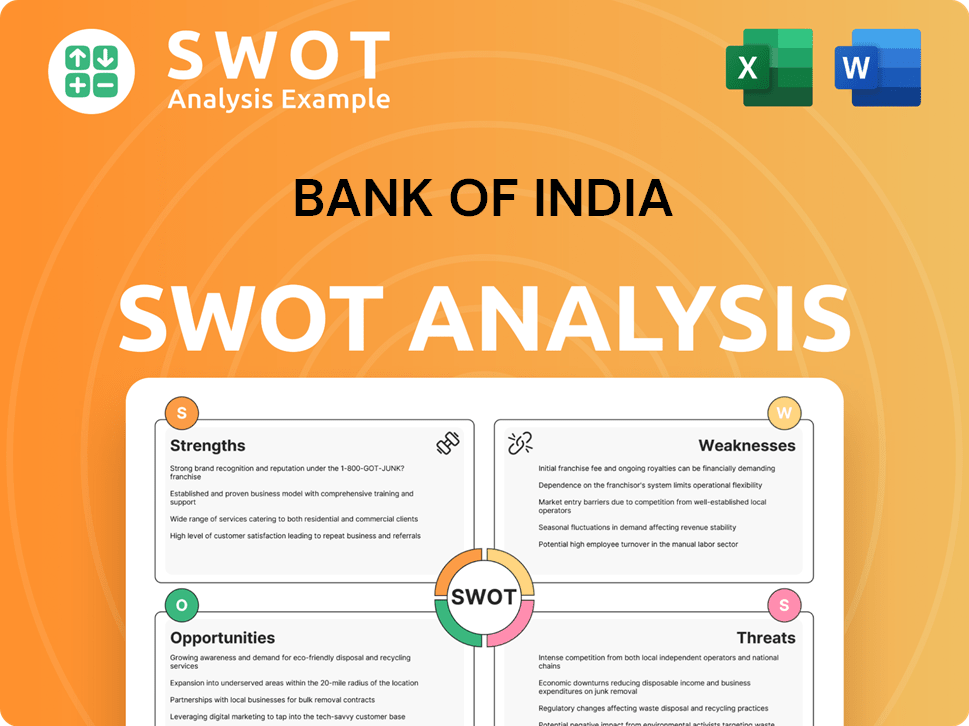

Bank of India SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Bank of India Make Money?

Bank of India (BOI) generates revenue through a variety of streams, primarily centered around its core banking operations. The bank's financial performance is significantly influenced by its ability to effectively manage these revenue streams and adapt to market dynamics. Understanding these strategies provides insight into BOI's financial health and operational efficiency.

The bank's revenue model is designed to maximize profitability through interest income, non-interest income, and strategic monetization of its services. BOI leverages its extensive network and digital platforms to diversify its revenue base and enhance customer experience. The bank's focus on asset quality and operational efficiency further supports its financial performance.

BOI's primary revenue source is interest income, derived from loans and advances. For the third quarter of fiscal year 2023-24, the net interest income (NII) stood at ₹5,700 crore. This income is generated from various loan products, including housing, personal, and vehicle loans, as well as corporate credit facilities. Additionally, income from investments in government securities and other financial instruments contributes to this stream.

Non-Interest Income and Diversification

Non-interest income is another crucial revenue stream for BOI, encompassing fees and commissions from various services. This includes fees from remittance services, foreign exchange transactions, locker rentals, and credit and debit card usage. BOI also earns from wealth management services and insurance product distribution. For the same period, the bank reported a non-interest income of ₹2,279 crore. Treasury operations, including profits from trading investments, also contribute to the bank's earnings.

- Tiered pricing for banking services.

- Cross-selling insurance and mutual funds.

- Bundled services for corporate clients.

- Digital platform services like online bill payments.

BOI's monetization strategies involve tiered pricing for banking services and cross-selling financial products. The bank actively promotes insurance and mutual funds to its existing customer base, enhancing its revenue streams. Digital platforms are also leveraged to offer fee-based services, such as online bill payments and digital loan applications. These strategies are part of BOI's broader approach to enhance its financial performance and customer service. To further understand BOI's approach to the market, consider reading about the Marketing Strategy of Bank of India.

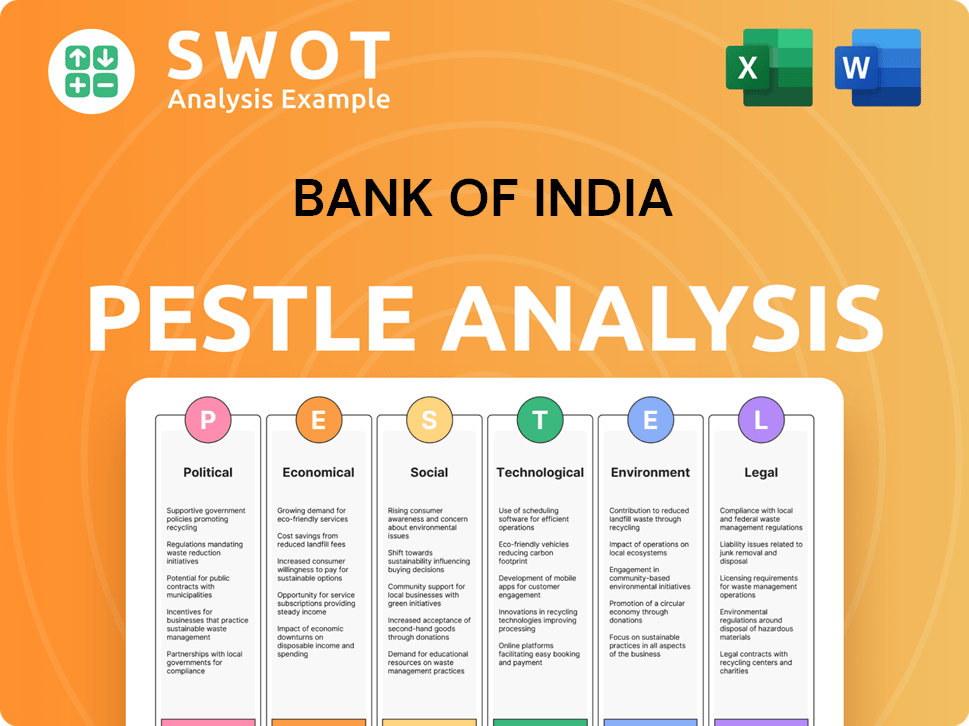

Bank of India PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Bank of India’s Business Model?

Bank of India (BOI) has experienced significant milestones and strategic shifts that have shaped its operational and financial trajectory. A key focus has been improving asset quality and credit growth. As of December 2023, the bank's gross non-performing assets (GNPA) ratio improved to 6.83%, and the net non-performing assets (NNPA) ratio decreased to 1.61%. This strategic focus has significantly boosted financial performance, leading to higher profitability.

Another crucial strategic move involves the bank's emphasis on digital transformation. This includes investing in technology to enhance customer experience, streamline operations, and expand digital offerings, such as mobile banking and online loan applications. These initiatives are aimed at improving customer service and operational efficiency. BOI continues to adapt to new trends by embracing fintech partnerships and exploring opportunities in emerging areas like green finance and sustainable banking, ensuring its relevance in a rapidly evolving financial landscape.

Operational challenges include managing the impact of economic downturns and regulatory changes. BOI has responded through prudent risk management practices and adherence to new banking norms. The bank's competitive advantages stem from its vast branch network, particularly its strong presence in semi-urban and rural areas, providing deep reach into diverse customer segments. For a deeper understanding of the bank's growth strategy, you can read more at Growth Strategy of Bank of India.

BOI has navigated several key milestones, including expansions and strategic pivots. The bank has focused on improving asset quality, as seen in the reduction of GNPA and NNPA ratios. Digital transformation efforts, including mobile banking and online loan applications, mark significant progress in enhancing customer experience and operational efficiency.

The bank's strategic moves include a strong emphasis on digital transformation and fintech partnerships. BOI is also focused on sustainable banking practices and exploring green finance opportunities. These moves are designed to enhance customer service, streamline operations, and expand digital offerings.

BOI's competitive advantages include its extensive branch network, especially in semi-urban and rural areas. Its long-standing brand reputation and customer trust also provide a significant edge. As a public sector bank, it benefits from government support and a large public sector client base.

BOI's financial performance has been bolstered by improved asset quality. The reduction in GNPA and NNPA ratios indicates better financial health. The bank's focus on digital transformation and fintech partnerships is expected to drive further improvements in operational efficiency and customer service.

Key Operational and Strategic Highlights

BOI's recent performance reflects a strategic focus on improving asset quality and digital transformation. The bank has shown improvements in its financial metrics, including a reduction in non-performing assets. These strategic moves aim to enhance customer experience and operational efficiency.

- Reduced GNPA and NNPA ratios, indicating improved asset quality.

- Significant investment in digital transformation, including mobile banking and online loan applications.

- Expansion of digital offerings to enhance customer experience and streamline operations.

- Strategic partnerships with fintech companies to drive innovation and reach.

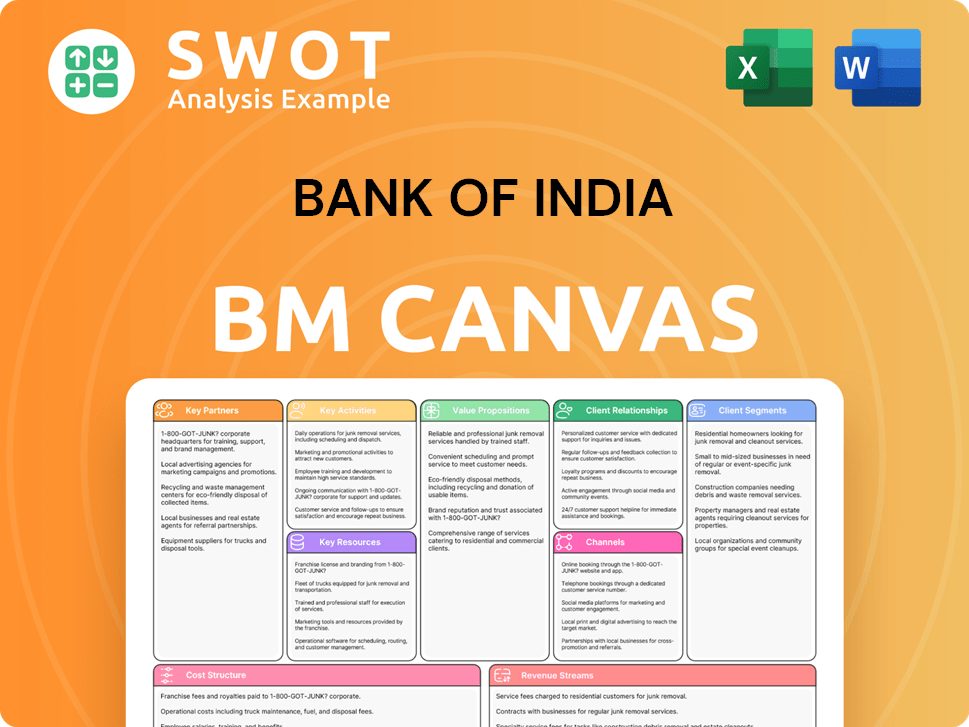

Bank of India Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Bank of India Positioning Itself for Continued Success?

Bank of India (BOI) holds a prominent position within the Indian banking sector, ranking among the leading public sector banks. As of early 2024, it demonstrates a significant market share in deposits and advances, supported by a strong customer base. Its global presence, with branches in 15 foreign countries, provides a competitive edge and opportunities for international business expansion. This widespread network and established legacy contribute to its solid foundation in the financial services landscape.

Despite its strengths, BOI faces risks such as interest rate fluctuations and credit risk within its loan portfolio. Regulatory changes and increasing competition from private sector banks and fintech companies pose ongoing challenges. Strategic initiatives focus on digital banking, expanding retail and SME lending, and improving asset quality. The bank's focus on sustainable growth, customer service, and leveraging technology aims to enhance its competitive position and revenue generation capabilities.

BOI is a major player in the Indian banking industry. As of December 2023, the bank's Capital Adequacy Ratio (CRAR) stood at 16.03%, indicating a strong capital base. It has a widespread domestic network and a significant international presence, which differentiates it from many other Indian banks. Its extensive reach and customer base are key strengths.

Key risks include interest rate volatility and credit risk. Regulatory changes and competition from private sector banks and fintech companies are also significant challenges. Maintaining asset quality and adapting to technological advancements are crucial. The bank must navigate these risks to sustain profitability and growth.

BOI aims to strengthen its digital banking capabilities and expand its retail and SME loan books. The bank is focused on sustainable growth and enhancing customer service. Leveraging technology will be critical to remaining competitive. BOI is strategically positioned to capitalize on growth opportunities.

BOI's strategic priorities include improving asset quality and expanding its digital presence. The bank is focused on enhancing customer experience and operational efficiency. These initiatives are designed to drive long-term value creation. For more details, you can review the Brief History of Bank of India.

Key Financial Metrics

BOI's financial performance is crucial for assessing its future prospects. The bank's ability to manage its assets and liabilities effectively will determine its success. BOI’s financial health is a key indicator of its overall stability and growth potential.

- Capital Adequacy Ratio (CRAR) of 16.03% (December 2023).

- Focus on digital banking and customer service.

- Expansion of retail and SME loan books.

- Emphasis on sustainable growth and leveraging technology.

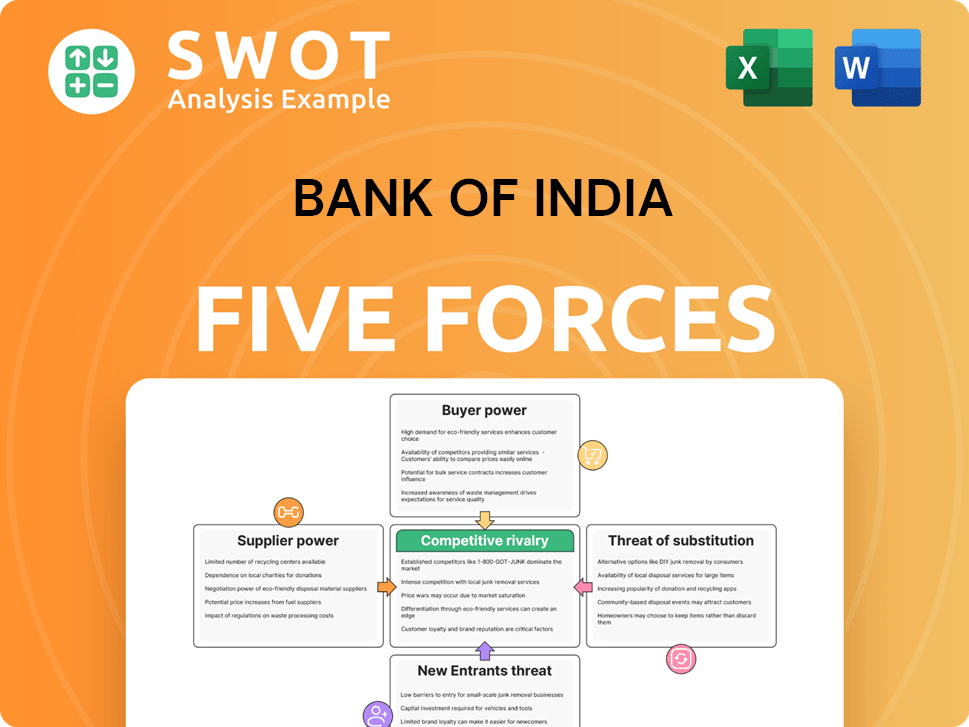

Bank of India Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Bank of India Company?

- What is Competitive Landscape of Bank of India Company?

- What is Growth Strategy and Future Prospects of Bank of India Company?

- What is Sales and Marketing Strategy of Bank of India Company?

- What is Brief History of Bank of India Company?

- Who Owns Bank of India Company?

- What is Customer Demographics and Target Market of Bank of India Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.