Alkami Bundle

How is Alkami Reshaping Digital Banking?

Alkami Technology is making waves in the financial technology sector, providing cutting-edge Alkami SWOT Analysis and digital banking solutions. With impressive revenue growth, including a 28.5% year-over-year increase in Q1 2025, Alkami is rapidly expanding its footprint. This innovative company is transforming how financial institutions operate and engage with their customers, making it a key player to watch.

The Alkami platform offers a comprehensive suite of services, from account access and bill pay to robust customer support, all delivered through a consistent user experience. Its cloud-based platform and strategic acquisitions, such as MANTL, underscore Alkami’s commitment to innovation and its mission to enhance the capabilities of financial institutions. Understanding Alkami's core technology and its impact on the evolving digital banking landscape is essential for anyone interested in financial technology.

What Are the Key Operations Driving Alkami’s Success?

The core operations of the company revolve around its cloud-based digital banking platform. This platform is designed to boost customer engagement, improve operational efficiency, and drive revenue growth for financial institutions. The company offers a comprehensive suite of digital banking products, which expanded significantly over time.

The company's value proposition lies in its ability to provide a scalable and efficient digital banking solution. Serving a diverse range of financial institutions, including community, regional, and super-regional banks and credit unions, the company's architecture allows for rapid deployment of new features and updates. Data differentiation through transaction insights across millions of accounts provides a significant competitive advantage.

The company's strategic focus on its software-as-a-service (SaaS) solution is evident in its supply chain and distribution networks. Partnerships and acquisitions further enhance its offerings, solidifying its position as a premier digital sales and service platform. This approach allows the company to continuously innovate and meet the evolving needs of its clients in the financial technology sector.

The company's core offerings include a comprehensive suite of digital banking products. In 2024, the company's product suite expanded to 34 products, a significant increase from the 9 products offered in 2015. This expansion reflects the company's commitment to providing a wide range of solutions for its clients.

Clients utilized an average of 14 products as of December 31, 2024. New clients in 2024 contracted for an average of 20 products, indicating deeper product adoption over time. This demonstrates the value and versatility of the company's platform.

The company operates on a true cloud, multi-tenant architecture. This architecture enables rapid deployment of new features and updates. This approach fosters continuous innovation and client satisfaction, providing a competitive edge in scalability and efficiency.

Partnerships, such as those with Trustmark Bank and the U.S. Postal Inspection Service, enhance offerings. The acquisition of MANTL in February 2025 expanded capabilities in onboarding and account opening solutions. These strategic moves strengthen the company's position in the market.

Key Advantages of the Alkami Platform

The Growth Strategy of Alkami relies on several key advantages. These include a robust digital banking platform, a focus on customer engagement, and operational efficiency. The company's ability to provide data differentiation through transaction insights is another significant advantage.

- Comprehensive suite of digital banking products

- Cloud-based, multi-tenant architecture

- Data differentiation through transaction insights

- Strategic partnerships and acquisitions

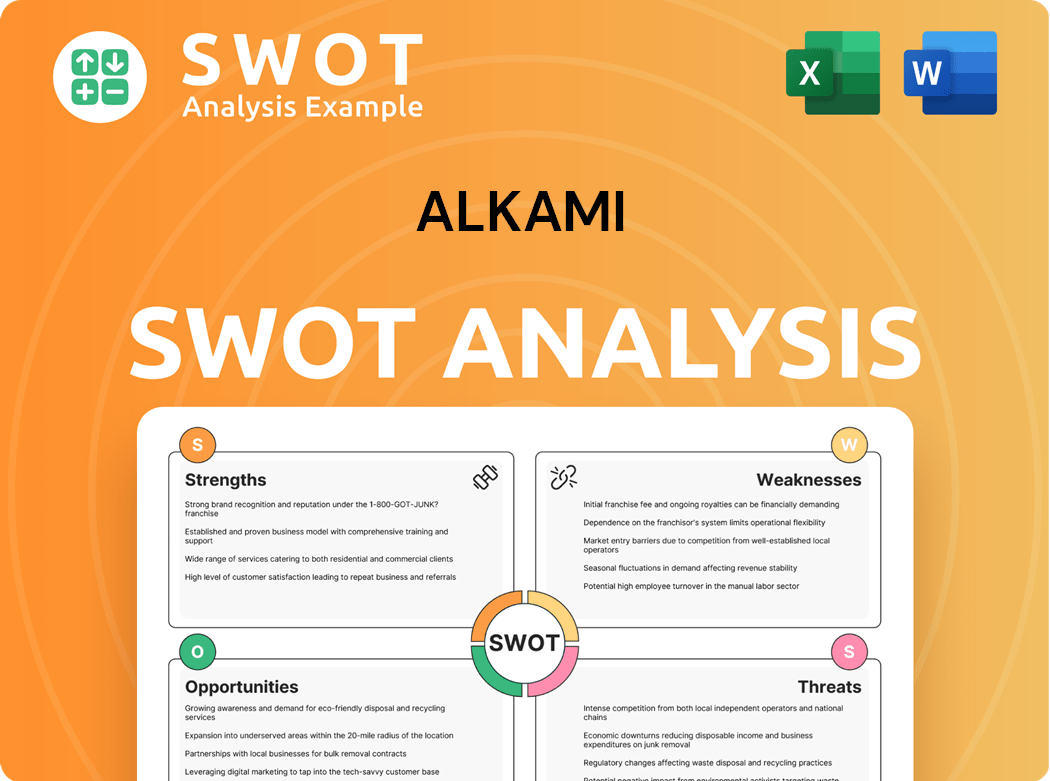

Alkami SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Alkami Make Money?

Understanding the financial dynamics of a company like Alkami, which provides digital banking solutions, is crucial for investors and stakeholders. Alkami's revenue streams and monetization strategies are key indicators of its financial health and growth potential. This analysis will delve into how Alkami generates revenue and the methods it uses to maximize its earnings.

The company's approach to revenue generation centers on its core products and services. Alkami's ability to attract and retain clients, along with its strategies for expanding revenue from existing customers, are critical to its financial performance. The following sections provide a detailed look at Alkami's revenue streams and monetization strategies.

Alkami Technology primarily generates revenue through subscription services and professional services. The company's digital banking platform subscriptions form the bulk of its income, providing a recurring revenue stream as financial institutions pay for access and usage of the platform. Professional services, including implementation, training, and customization, also contribute to its revenue.

Revenue Streams and Monetization Strategies

In 2024, subscription revenue reached $314.4 million, representing 95.6% of total revenues, a 26.2% increase from $218.5 million in 2023. For Q1 2025, subscription revenue grew by 27% and represented 95% of total revenue, reaching $92.8 million. This growth underscores the importance of the Alkami platform in the financial technology landscape. The company's 'land and expand' approach is a key monetization strategy, securing clients initially and then driving further revenue through increased user adoption and cross-selling additional products. This strategy is crucial for the long-term success of the company.

- Subscription Revenue: The primary revenue stream comes from subscriptions to its digital banking platform.

- Professional Services: Includes implementation, training, and customization services.

- Land and Expand Strategy: Focuses on acquiring clients and then increasing revenue through greater product adoption and cross-selling.

- Annual Recurring Revenue (ARR): Reached $404 million in Q1 2025, up 33% year-over-year.

- Revenue Per User: Revenue per registered user increased to $19.74, an 18% increase compared to the year-ago quarter.

- Acquisition Impact: The acquisition of MANTL is expected to contribute approximately $31.4 million in revenue to Alkami's 2025 full-year financial performance.

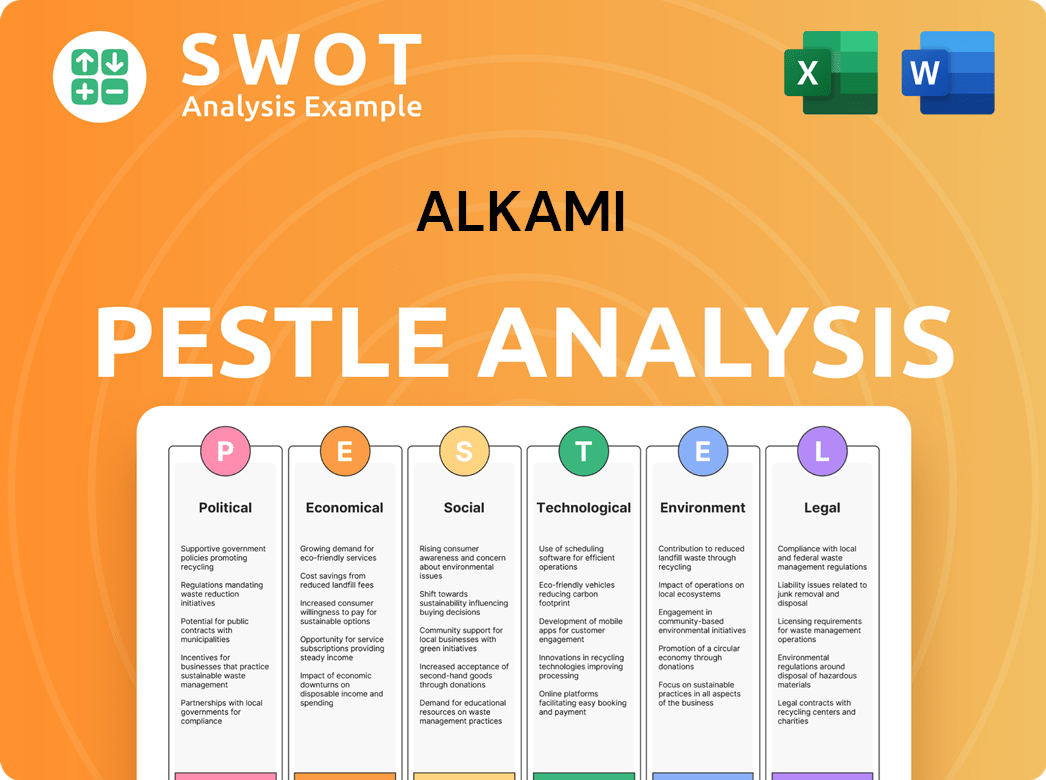

Alkami PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Alkami’s Business Model?

Alkami Technology has achieved significant milestones, shaping its operations and financial performance. A notable strategic move was the acquisition of Fin Technologies, Inc. (MANTL) in February 2025 for approximately $380 million. This acquisition aimed to enhance its onboarding and account opening solutions, broadening Alkami's service capabilities.

In 2024, Alkami expanded its product suite to 34 products, demonstrating its commitment to addressing the evolving needs of financial institutions. The company also established a new subsidiary in India in 2024 to support future operational needs. These strategic moves highlight Alkami's focus on growth and innovation within the digital banking sector.

Operationally, Alkami has focused on continuous product innovation, investing 28.8% of its revenues in research and development in 2024. This investment has led to a robust platform that supports 20.5 million registered users as of Q1 2025, a 13% increase from the previous year. Alkami's competitive advantages stem from its specialized focus on the digital banking sector for community and regional financial institutions, offering a comprehensive and unified platform.

Alkami's key milestones include the acquisition of MANTL in February 2025 for approximately $380 million, expanding its service capabilities. In 2024, the company expanded its product suite to 34 products and established a new subsidiary in India.

Strategic moves include the acquisition of MANTL to enhance onboarding and account opening solutions. Alkami also focuses on continuous product innovation, investing heavily in research and development to maintain its competitive edge in the market.

Alkami's competitive advantages include its specialized focus on digital banking for community and regional financial institutions. Its cloud-based, multi-tenant architecture provides scalability and efficiency, allowing rapid deployment of new features. The company also benefits from strong customer relationships and a reputation for excellent customer service.

Alkami's financial performance is supported by its 'land and expand' strategy, long-term contracts, and escalating contract minimums, contributing to a high net dollar retention rate. The net dollar retention rate was 113% as of December 31, 2024.

Alkami's Strengths and Strategies

Alkami's strengths include its cloud-based platform, which offers scalability and efficiency, and its focus on customer service, as evidenced by its J.D. Power certifications. The company's 'land and expand' strategy, coupled with long-term contracts, contributes to a high net dollar retention rate.

- Specialized focus on digital banking for community and regional financial institutions.

- Cloud-based, multi-tenant architecture for scalability.

- Strong customer relationships and excellent customer service.

- Continuous investment in research and development.

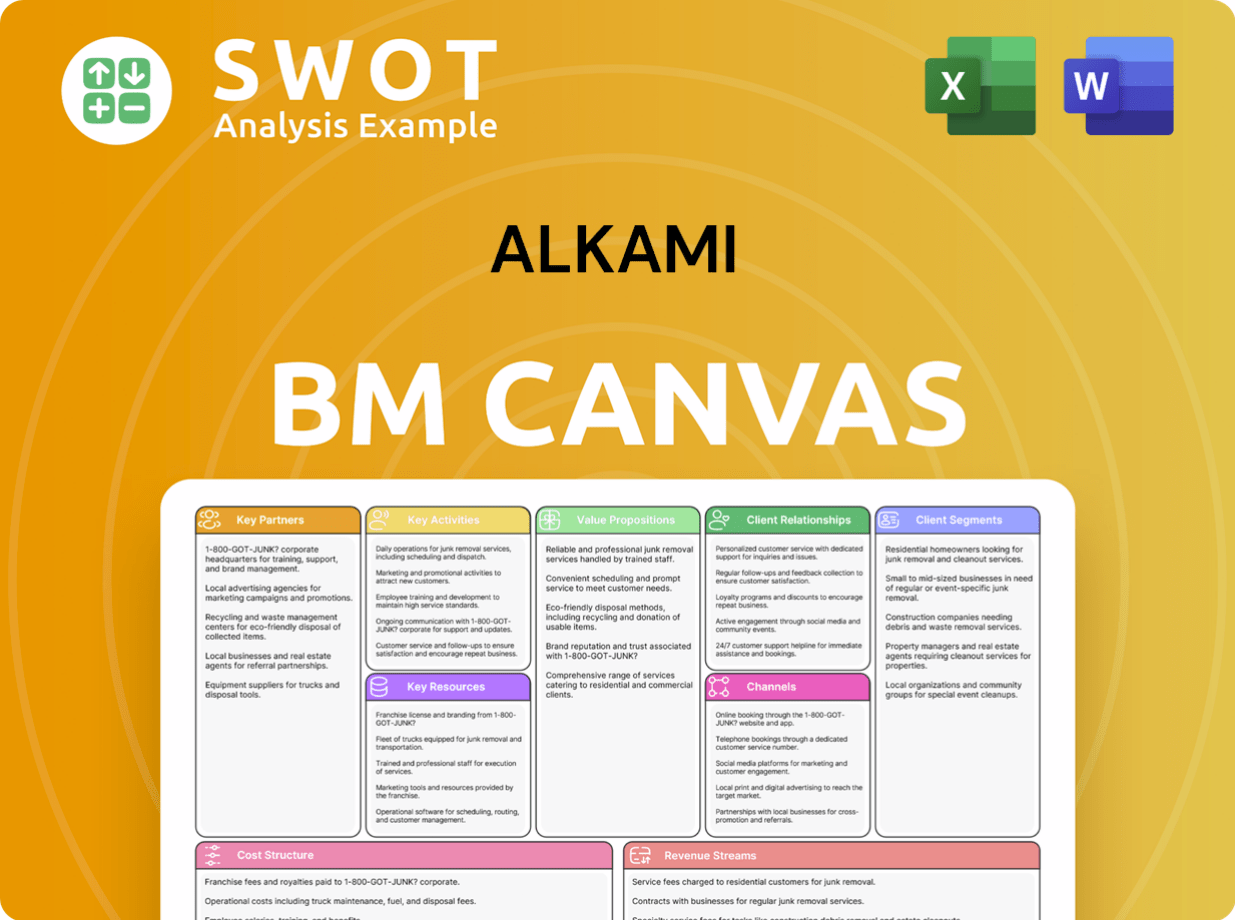

Alkami Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Alkami Positioning Itself for Continued Success?

Alkami Technology holds a significant market position in the digital banking solutions sector, primarily serving community, regional, and super-regional financial institutions in the U.S. As of Q1 2025, the company served 278 financial institutions through its digital banking platform, expanding from 244 in Q1 2024. The company had 20.5 million registered users. Alkami's total addressable market is estimated at $14 billion, with digital banking representing the largest segment at $8.8 billion.

Alkami faces several key risks despite its strong position and growth. The digital banking solutions market is intensely competitive, and rapid technological changes require continuous innovation. Cybersecurity threats are a constant concern, and economic downturns could impact financial institutions' technology spending. The recent MANTL acquisition also carries integration risks and has increased Alkami's debt-to-equity ratio significantly to 123.69% in Q1 2025.

Alkami is a key player in the digital banking space, focusing on community and regional financial institutions. The Owners & Shareholders of Alkami have seen the company grow, with a significant number of financial institutions using its platform. The company's gross margin reached 64.3% in Q1 2025, up from 56.8% in 2021, showing operational efficiency.

The digital banking market is highly competitive, with larger companies vying for market share. Rapid technological advancements require continuous innovation to stay relevant. Cybersecurity threats pose a significant risk, and economic downturns could affect revenue. The MANTL acquisition adds integration risks and impacts the debt-to-equity ratio.

Alkami plans to sustain and expand revenue through continuous strategic initiatives, including R&D, which was 27.5% of revenues in Q1 2025. The company projects annual revenue for 2025 to be between $443 million and $447 million, representing 33% to 34% growth. Adjusted EBITDA is expected to nearly double to $51 million in 2025.

Alkami is focused on enhancing its product suite and maintaining innovation leadership. The company aims to deepen existing client relationships and expand its client base. The MANTL acquisition is projected to contribute approximately $31.4 million in revenue to 2025 results and is expected to be accretive to adjusted EBITDA in 2026.

Key Financial Projections

Alkami's financial outlook for 2025 includes significant growth in both revenue and adjusted EBITDA. The company is strategically positioned to leverage its comprehensive digital banking platform. The focus is on enhancing existing client relationships and expanding the client base.

- Revenue growth of 33% to 34% in 2025.

- Adjusted EBITDA nearly doubling to $51 million in 2025.

- Organic growth of 25% to 26%.

- MANTL acquisition contributing to revenue and EBITDA.

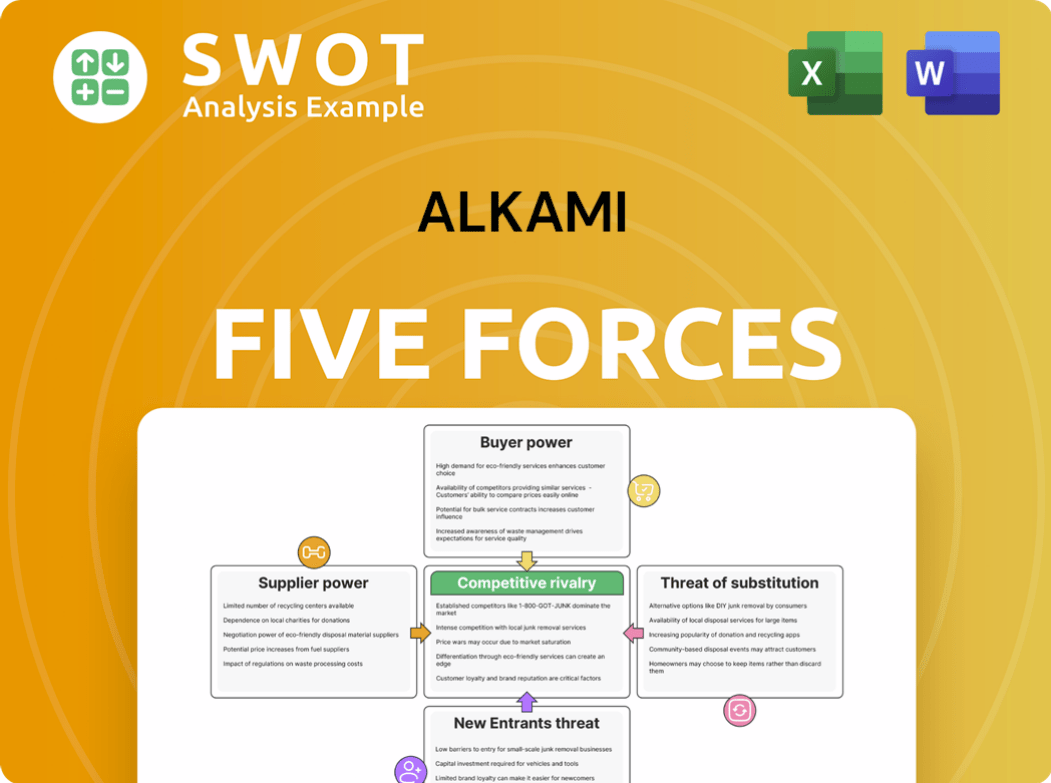

Alkami Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Alkami Company?

- What is Competitive Landscape of Alkami Company?

- What is Growth Strategy and Future Prospects of Alkami Company?

- What is Sales and Marketing Strategy of Alkami Company?

- What is Brief History of Alkami Company?

- Who Owns Alkami Company?

- What is Customer Demographics and Target Market of Alkami Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.