Vietnam Prosperity Joint-sock Commercial Bank Bundle

Can VPBank Conquer Vietnam's Banking Landscape?

Established in 1993, Vietnam Prosperity Joint-stock Commercial Bank (VPBank) is on a mission to become a banking titan. With aspirations to be among Vietnam's top three banks and a top 100 Asian bank by 2025, VPBank is undergoing a significant transformation. This journey involves a strategic shift towards digital solutions and comprehensive financial services, positioning it at the forefront of Vietnam's evolving economy.

VPBank's Vietnam Prosperity Joint-sock Commercial Bank SWOT Analysis reveals a dynamic growth strategy fueled by a strategic partnership with Sumitomo Mitsui Banking Corporation (SMBC). This collaboration is pivotal in VPBank's evolution into a multifunctional bank, expanding its reach beyond retail and SMEs. This comprehensive analysis will delve into VPBank's strategic initiatives, exploring its growth strategy, financial performance, and future prospects within the competitive banking sector in Vietnam.

How Is Vietnam Prosperity Joint-sock Commercial Bank Expanding Its Reach?

The Target Market of Vietnam Prosperity Joint-sock Commercial Bank, or VPBank, is evolving, with the bank focusing on both market penetration and diversification to fuel its growth strategy. This involves expanding its reach across different customer segments and geographical areas. The bank's strategic initiatives are designed to strengthen its position in the Vietnamese banking sector and enhance its financial performance.

VPBank's expansion plans include targeting new customer segments, particularly large corporate clients, in addition to its traditional retail and SME base. This strategic shift is supported by its partnership with SMBC. Furthermore, the bank is exploring international expansion by establishing branches, subsidiary banks, or representative offices abroad as business opportunities arise.

Product and service diversification is another key element of VPBank's growth strategy. The bank is actively enhancing its offerings, especially through its consumer finance subsidiary, FE Credit, which is expected to contribute significantly to profit. This multi-faceted approach aims to drive sustainable growth and increase VPBank's market share.

VPBank is targeting large corporate clients to diversify its customer base. This move complements its existing focus on retail and SME clients, enhancing its market presence. The strategic partnership with SMBC supports this expansion into new segments.

VPBank plans to expand internationally by establishing branches, subsidiary banks, or representative offices. This geographical expansion aims to capitalize on business opportunities in foreign markets. The bank's expansion plans are designed to increase its global footprint.

VPBank is enhancing its product and service offerings to meet evolving customer needs. FE Credit, the bank's consumer finance subsidiary, is a key driver of this strategy. The bank aims to improve its financial performance through these enhancements.

VPBank is supporting GPBank, which it is taking over, by providing management, IT, and business model improvements. This acquisition is expected to increase its foreign ownership limit to 49%, attracting new investors. The bank's strategic initiatives include partnerships to drive growth.

Financial Targets and Projections

FE Credit aims for a pre-tax profit of VND1.13 trillion ($43.5 million) in 2025, a 120% increase from 2024. VPBank is targeting robust credit growth of 20%-25% and strong deposit growth of over 30% in 2025. These targets reflect VPBank's ambitious growth strategy and its commitment to sustainable growth.

- FE Credit's loan book grew in Q4 2024, and total new disbursements increased by 40% year-on-year in 2024.

- Strategic segments are projected to expand by 30%-40% in 2025, subject to the State Bank of Vietnam's approval.

- VPBank plans to attract more customer deposits by enhancing partnership channels and launching new certificate deposit products.

- The bank is diversifying funding sources, including domestic interbank and offshore funding, to support its growth.

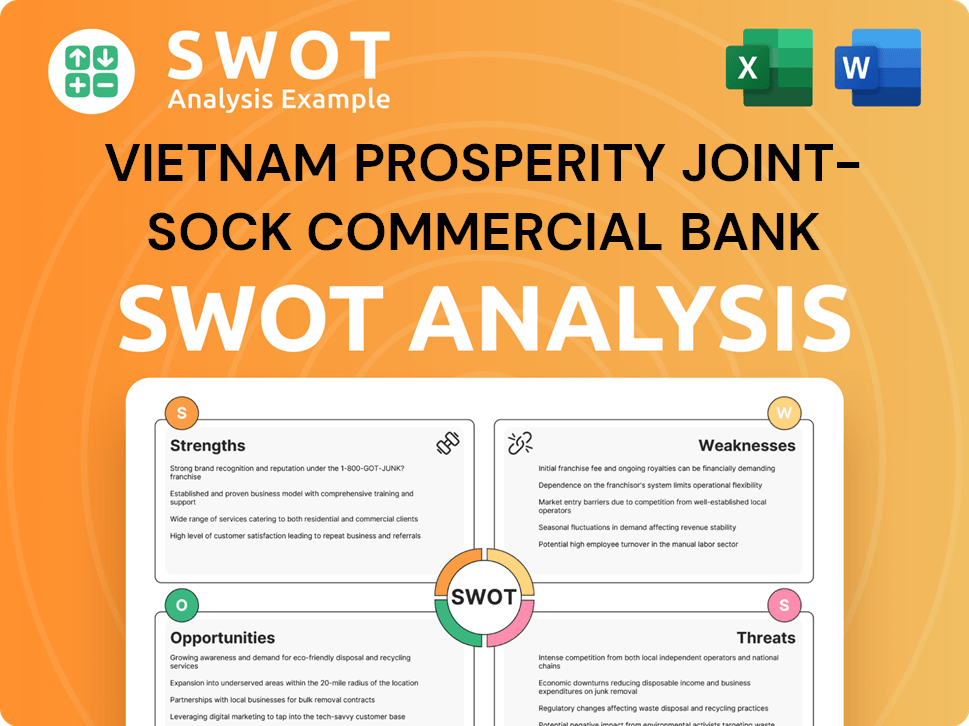

Vietnam Prosperity Joint-sock Commercial Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Vietnam Prosperity Joint-sock Commercial Bank Invest in Innovation?

VPBank's innovation and technology strategy is central to its growth strategy, focusing on digital transformation to become a leading multi-purpose financial services provider. This approach is vital in the rapidly evolving banking sector in Vietnam. The bank leverages technology to enhance customer experiences, streamline operations, and gain a competitive edge. The bank's strategic initiatives are designed to capitalize on technological advancements and meet the changing needs of its customers.

The bank is committed to creating a seamless digital ecosystem that connects various member companies across banking, consumer finance, securities, digital insurance (OPES), and other multiservice platforms. This integration aims to provide comprehensive financial solutions and improve customer service. By prioritizing digital initiatives and AI/GenAI, VPBank aims to optimize operations and boost productivity, ensuring it remains competitive in the financial market.

The bank's digital transformation journey is a key element of its strategy, with significant investments in IT infrastructure and cloud migration. These investments are expected to increase the Cost-to-Income Ratio (CIR) to around 25% in 2025, which is considered low compared to peers, indicating efficiency gains. This approach is part of VPBank's broader plan to enhance its market position and drive sustainable growth. For more insights, consider exploring the Marketing Strategy of Vietnam Prosperity Joint-sock Commercial Bank.

Digital Transformation on AWS

VPBank migrated critical workloads to Amazon Web Services (AWS) as part of its five-year digital transformation strategy. Within 11 months in 2023, the bank successfully moved 28 applications from on-premise infrastructure to AWS Cloud.

Cloud Migration Plans

VPBank plans to migrate all remaining applications to the cloud in 2024 and 2025. This comprehensive cloud migration is designed to enhance scalability, improve security, and reduce operational costs.

Digital Bank 'Cake by VPBank'

'Cake by VPBank,' launched in 2021, serves 5 million customers with only 250 employees. The digital bank processes 700,000 credit applications monthly, demonstrating the effectiveness of its technology-driven approach.

Digital Insurer OPES

OPES, VPBank's digital insurer, recorded a revenue of $102 million in 2024. OPES operates with only 110 employees, showcasing the efficiency of digital operations.

AI and GenAI Integration

VPBank is actively prioritizing digital initiatives and leveraging the power of AI/GenAI. This focus aims to continuously optimize operations and improve productivity across all areas of the business.

Productivity Improvement Goals

The bank aims to improve productivity by 20-30% by strengthening its IT infrastructure. This will enable and automate digital strategies, helping VPBank stay ahead of the competition.

Key Strategic Focus Areas

VPBank's innovation and technology strategy is centered around several key areas, including cloud migration, AI/GenAI integration, and the development of a seamless digital ecosystem. These initiatives aim to enhance customer experience, streamline operations, and drive sustainable growth.

- Digital Transformation: Migrating critical workloads to the cloud to improve scalability and reduce costs.

- AI and GenAI: Leveraging AI to optimize operations, improve productivity, and enhance customer service.

- Digital Ecosystem: Creating a connected platform across banking, consumer finance, and other services.

- Customer Experience: Focusing on providing seamless and user-friendly digital banking solutions.

- Operational Efficiency: Streamlining processes through automation and technology to reduce costs.

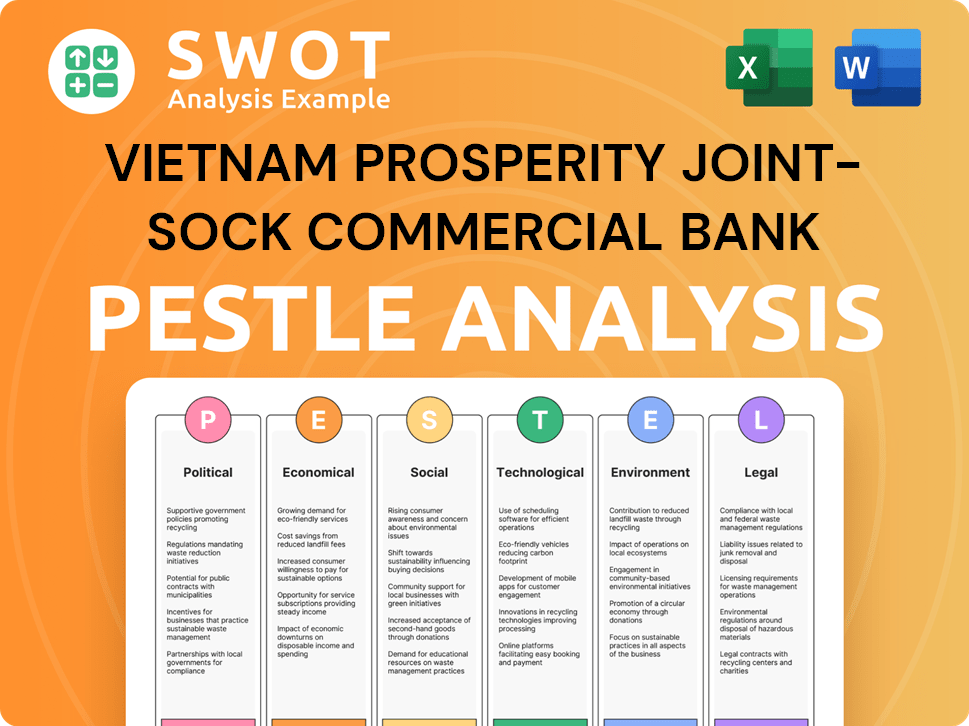

Vietnam Prosperity Joint-sock Commercial Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Vietnam Prosperity Joint-sock Commercial Bank’s Growth Forecast?

VPBank's financial outlook for 2024 and 2025 highlights ambitious growth targets within the Banking sector Vietnam. The bank is focused on improving profitability and asset quality to achieve these goals. The strategic initiatives are designed to strengthen its position in the market and drive sustainable growth.

In 2024, VPBank aimed for a pre-tax profit of VND23.17 trillion ($914.18 million), a substantial increase of 114% year-on-year. The bank's projections also included significant growth in total assets and customer deposits. These targets reflect VPBank's commitment to expanding its market share and enhancing its financial performance.

For 2025, VPBank anticipates continued strong performance. The consolidated pre-tax profit is expected to reach VND25.27 trillion ($971.9 million). This growth is driven by robust performance across various business segments, including the parent bank, FE Credit, VPBank Securities (VPBankS), and digital insurer OPES. The bank's expansion plans include annual credit growth of 35% over the next five years, especially after taking over GPBank. For more details, see the Brief History of Vietnam Prosperity Joint-sock Commercial Bank.

In 2024, VPBank aimed for a pre-tax profit of VND23.17 trillion ($914.18 million), representing a 114% year-on-year increase. The bank targeted VND974.27 trillion ($38.44 billion) in total assets and VND598.86 trillion ($23.63 billion) in customer deposits. Credit growth was expected to hit 25%, equivalent to outstanding debt of VND752.1 trillion ($29.67 billion).

For 2025, VPBank's consolidated pre-tax profit is expected to reach VND25.27 trillion ($971.9 million), a 26% increase from 2024. The parent bank's standalone profit is estimated at VND22.22 trillion ($854.6 million), up 26%, while FE Credit's pre-tax profit is projected to increase by 120% to VND1.13 trillion ($43.5 million).

VPBank's net interest margin (NIM) was 6.0% in 9M2024, up 44 basis points year-on-year, primarily due to a sharp decline in the cost of funds (COF). While NIM is expected to remain flat year-on-year in 2025 due to upward pressure on funding costs and loan pricing competition, the bank anticipates significant increases in NIM for FY2025/2026.

Total operating income for 9M2024 was VND44,602 billion (+22.5% YoY), with net interest income recovering strongly by 32.3%. The cost-to-income ratio (CIR) was a highlight at 23.7% in 9M2024, the lowest among banks, contributing to a 67.5% year-on-year growth in profit after tax (PAT) to VND10,939 billion. For FY2025/2026, PAT is expected to grow by 26.0% and 33.4%.

Key Financial Highlights

VPBank's financial performance in 2024 and 2025 is driven by strong growth across various segments. The bank's focus on cost efficiency and strategic initiatives is expected to yield significant improvements in profitability.

- Pre-tax profit growth targets for 2024 and 2025.

- NIM improvements driven by lower COF.

- Strong growth in operating income and net interest income.

- Low CIR and high PAT growth.

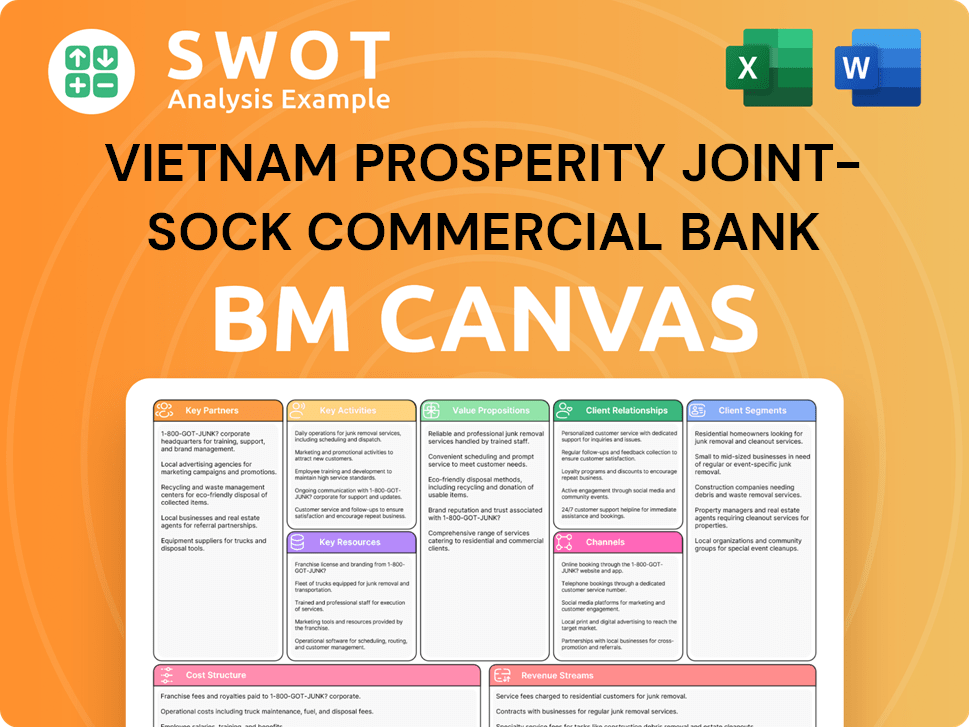

Vietnam Prosperity Joint-sock Commercial Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Vietnam Prosperity Joint-sock Commercial Bank’s Growth?

VPBank faces several risks that could hinder its growth. These challenges include exposure to the real estate sector, regulatory changes, and intense market competition. The bank's strategies to mitigate these risks are crucial for maintaining its financial health and achieving its strategic goals.

A significant risk stems from VPBank's substantial involvement in the real estate sector. The high loan-to-deposit ratio, along with the potential for increased funding costs, adds to the complexity. Addressing these issues effectively is essential for VPBank's long-term success.

The bank is actively working to manage these challenges. VPBank's proactive measures, such as digital transformation and focus on NPL management, are vital for navigating the evolving financial landscape. For further insight into the bank's foundational principles, you can read about the Mission, Vision & Core Values of Vietnam Prosperity Joint-sock Commercial Bank.

Real Estate Exposure

As of December 2024, approximately 27% of VPBank's total loans were in the real estate sector. This concentration poses a risk due to the high leverage of real estate developers and potential for a slowdown in new housing transactions. The bank's asset quality is expected to stabilize and improve through 2025, but overall profitability may face pressure.

Loan-to-Deposit Ratio

VPBank's loan-to-deposit ratio reached 143% as of December 2024, the highest among its rated peers. This indicates that its loan growth has outpaced deposit growth. Managing this ratio is crucial to ensure sufficient funding and maintain financial stability.

Regulatory and Policy Risks

Changes in regulations and government policies present potential obstacles. Vietnam's economy is sensitive to US trade policies. Legal and regulatory bottlenecks in the real estate market could also hinder project resolution. VPBank's CEO has called for a review of the risk coefficient for real estate loans, currently at 200%.

Market Competition and Technological Disruption

Maintaining a competitive edge in the rapidly evolving financial landscape requires continuous innovation. VPBank is investing heavily in digital transformation. The bank's ability to leverage AI and GenAI to enhance productivity and maintain an efficient cost-to-income ratio is critical for its future success.

Non-Performing Loans (NPLs)

VPBank is actively managing its non-performing loan (NPL) ratio, which is expected to peak in the first half of 2025, primarily among real estate borrowers. The bank aims to keep its standalone NPL ratio below 3% in 2025. This proactive approach is key to maintaining asset quality.

Funding Diversification

VPBank is working to diversify its funding sources and enhance partnerships to manage funding costs and attract deposits. This strategy is essential for mitigating the risks associated with a high loan-to-deposit ratio and ensuring financial stability. Diversification is critical for sustainable growth.

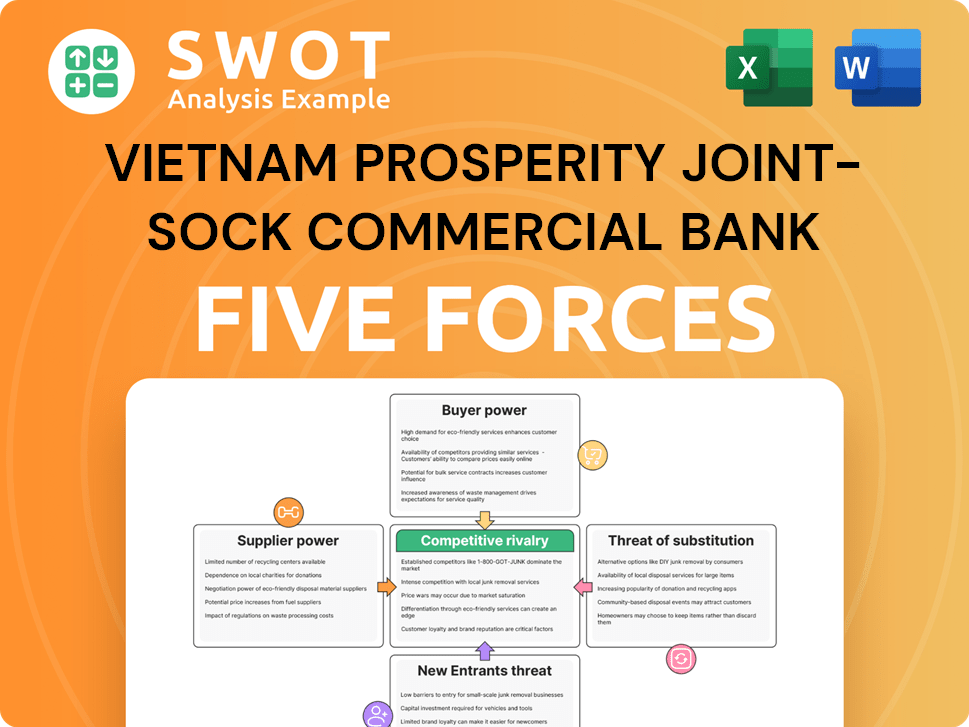

Vietnam Prosperity Joint-sock Commercial Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Vietnam Prosperity Joint-sock Commercial Bank Company?

- What is Competitive Landscape of Vietnam Prosperity Joint-sock Commercial Bank Company?

- How Does Vietnam Prosperity Joint-sock Commercial Bank Company Work?

- What is Sales and Marketing Strategy of Vietnam Prosperity Joint-sock Commercial Bank Company?

- What is Brief History of Vietnam Prosperity Joint-sock Commercial Bank Company?

- Who Owns Vietnam Prosperity Joint-sock Commercial Bank Company?

- What is Customer Demographics and Target Market of Vietnam Prosperity Joint-sock Commercial Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.