RCBC Bundle

Can RCBC Continue Its Ascent in the Philippine Banking Sector?

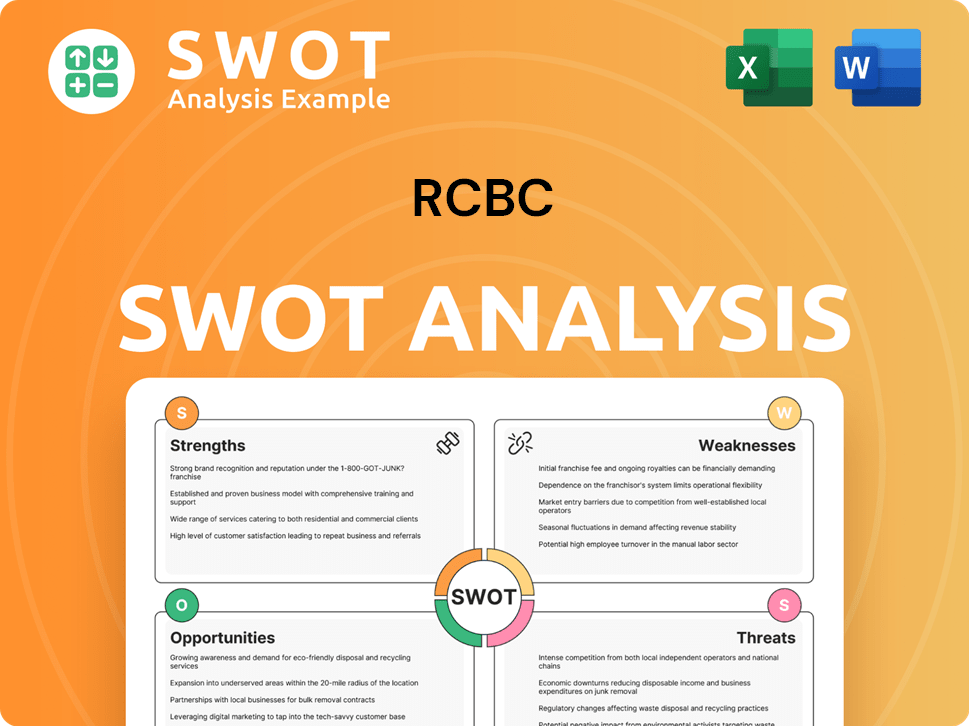

In the ever-evolving landscape of the Philippine banking industry, understanding the RCBC SWOT Analysis is crucial for investors and strategists alike. This analysis delves into RCBC's growth strategy and future prospects, offering a comprehensive look at its strategic initiatives and market position. Established in 1960, RCBC has evolved significantly, becoming a major player in the financial sector.

RCBC's commitment to innovation and strategic partnerships, such as its bancassurance collaboration, highlights its proactive approach to the RCBC Company Analysis. The bank's ability to adapt to technological advancements and evolving customer expectations will be key to its future success. A deep dive into RCBC's financial performance review and expansion plans will reveal its capacity for sustained growth within the Philippine Banking Industry.

How Is RCBC Expanding Its Reach?

The focus of the RCBC Growth Strategy includes significant expansion initiatives designed to broaden its market reach and diversify revenue streams. The bank's strategic moves underscore its commitment to adapting to the evolving landscape of the Philippine Banking Industry.

RCBC's Future Prospects are closely tied to its ability to execute these expansion plans effectively. Key areas of focus include digital banking, product diversification, and sustainable finance. These initiatives are aimed at enhancing customer experience, driving financial inclusion, and aligning with global trends.

These strategic moves are part of a broader RCBC Company Analysis, which evaluates the bank's performance and future potential. The bank is actively pursuing several strategic expansion initiatives to broaden its market reach and diversify its revenue streams.

Digital expansion is a key component of RCBC's growth strategy. The bank is leveraging its digital banking platform, RCBC Pulz, launched in 2024, to enhance the digital banking experience for its customers. This platform offers seamless transactions and improved accessibility to financial services.

RCBC's ATM Go service, a mobile ATM, is being expanded to reach underserved areas. This initiative provides essential banking services to remote communities and drives financial inclusion. It aligns with the bank's goal of expanding its customer base beyond traditional branch networks.

RCBC continues to enhance its loan portfolio, with a notable increase in its gross loan portfolio. The bank is also actively expanding its credit card services, reflected by a 29% growth in credit card receivables in the first quarter of 2024.

RCBC is exploring opportunities in sustainable finance, aiming to increase its green and sustainability loan portfolio. The bank has already secured significant green financing, including a 150 million Euro green bond from the ASEAN Green Bond Fund in early 2024, demonstrating its commitment to sustainable growth.

Key Financial Highlights

Financial Performance RCBC shows positive trends. The gross loan portfolio increased by 17% year-on-year to P672 billion as of the end of March 2024. Corporate loans grew by 15%, and consumer loans increased by 21%. Credit card receivables grew by 29% in the first quarter of 2024.

- Digital banking platform RCBC Pulz launched in 2024.

- ATM Go service expanding to underserved areas.

- Gross loan portfolio increased by 17% year-on-year.

- Secured a 150 million Euro green bond in early 2024.

For a deeper understanding of the bank's history, you can read more in the Brief History of RCBC.

RCBC SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does RCBC Invest in Innovation?

The company is heavily investing in technology and innovation to foster sustainable growth and strengthen its competitive position. A central element of its strategy involves the continuous development and enhancement of its digital platforms, particularly RCBC Pulz. This platform is designed to improve customer interactions, offer personalized financial insights, and facilitate a broader range of digital transactions, thereby expanding the bank's reach and improving customer retention. The company aims to migrate a significant portion of its transactions to digital channels, reducing operational costs and improving efficiency.

The company's approach to innovation extends beyond retail banking. It is leveraging technology to optimize internal operations and risk management. The company is exploring the application of artificial intelligence (AI) and machine learning (ML) for data analytics, fraud detection, and credit scoring, which will enhance decision-making and mitigate financial risks. Automation is also a key focus, with the bank implementing robotic process automation (RPA) in various back-office functions to improve efficiency and reduce manual errors. The company's commitment to innovation extends to its ATM Go service, which utilizes mobile technology to deliver banking services to remote and underserved areas, demonstrating a blend of social responsibility and technological innovation.

Strategic partnerships are also crucial to the company's innovation agenda. Collaborations with fintech companies and technology providers enable the company to integrate cutting-edge solutions and stay ahead of emerging trends. These initiatives are part of the overall RCBC's target market strategy, aiming to provide better services and reach a wider customer base within the Philippine Banking Industry.

Digital Platform Enhancement

Continuous improvement of digital platforms, especially RCBC Pulz, is a key focus. This includes enhancing user experience, expanding transaction capabilities, and personalizing financial insights. The goal is to increase customer engagement and satisfaction through digital channels.

AI and ML Integration

The company is actively exploring the use of AI and ML for data analytics, fraud detection, and credit scoring. These technologies will help in making data-driven decisions, improving risk management, and enhancing operational efficiency. The focus is on leveraging data to improve service delivery and reduce financial risks.

Automation Initiatives

Implementation of robotic process automation (RPA) in back-office functions is underway. This will streamline operations, reduce manual errors, and improve overall efficiency. The aim is to optimize internal processes and reduce operational costs through automation.

ATM Go Expansion

The ATM Go service is being used to extend banking services to remote and underserved areas. This initiative demonstrates a commitment to social responsibility and technological innovation. The goal is to improve financial inclusion by making banking services more accessible.

Strategic Partnerships

Collaborations with fintech companies and technology providers are essential for integrating cutting-edge solutions. These partnerships help the company stay abreast of emerging trends and offer innovative services. The focus is on leveraging external expertise to enhance technological capabilities.

Digital Transformation Goals

The company aims to increase the proportion of transactions conducted through digital channels. This shift is intended to reduce operational costs, improve efficiency, and enhance the overall customer experience. The goal is to become a leader in digital banking within the Philippines.

Key Technological Investments and Strategies

The company's investment in technology is a core component of its strategy to achieve sustainable growth and maintain a competitive edge. These investments are geared towards enhancing customer experience, improving operational efficiency, and mitigating risks. The focus is on digital transformation and leveraging technology to drive innovation within the Philippine banking sector.

- Digital Banking Platforms: Continuous upgrades and enhancements to digital banking platforms, such as RCBC Pulz, to offer a more intuitive and comprehensive digital banking experience.

- AI and Machine Learning: Implementation of AI and ML for data analytics, fraud detection, and credit scoring to improve decision-making and risk management.

- Automation: Adoption of robotic process automation (RPA) in back-office functions to streamline operations and reduce manual errors.

- ATM Go: Expansion of the ATM Go service, utilizing mobile technology to provide banking services in remote and underserved areas.

- Strategic Partnerships: Collaborations with fintech companies and technology providers to integrate cutting-edge solutions and stay abreast of emerging trends.

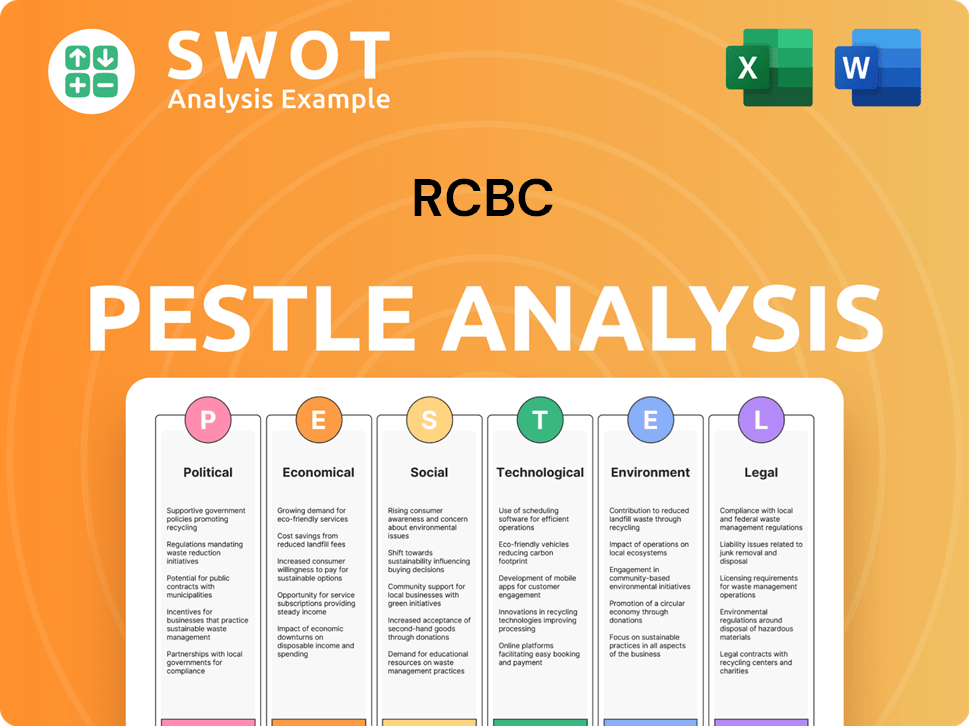

RCBC PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is RCBC’s Growth Forecast?

The financial outlook for RCBC appears promising, reflecting strong performance and ambitious growth targets. As of the first quarter of 2024, RCBC demonstrated significant financial progress, providing a positive outlook for the RCBC Growth Strategy. The bank's ability to increase its net income and loan portfolio indicates a solid foundation for future expansion within the Philippine Banking Industry.

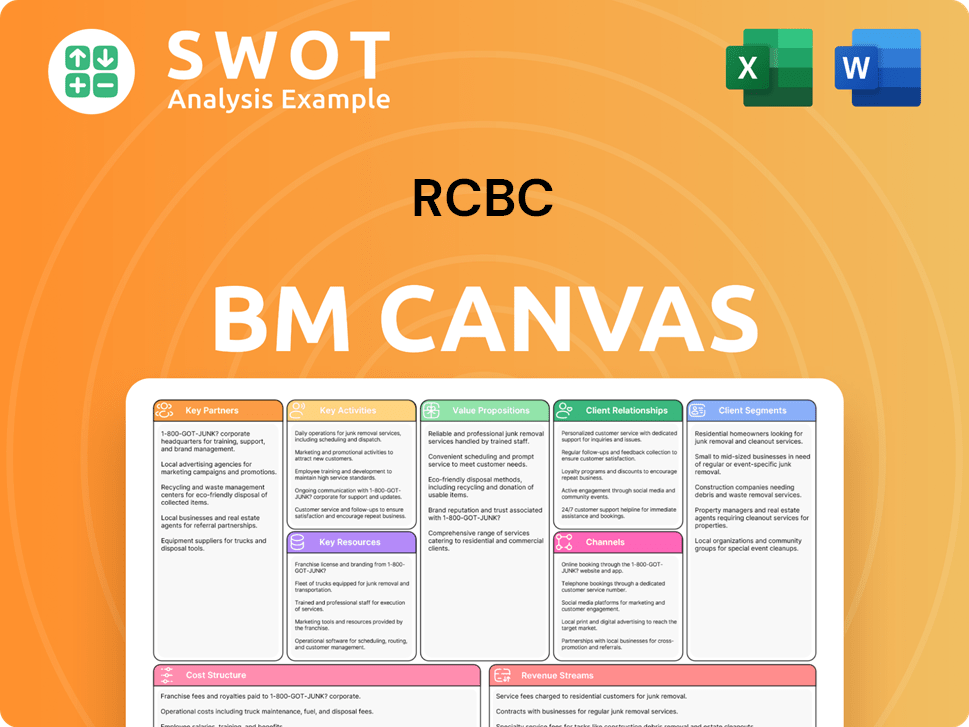

RCBC's strategic initiatives, including digital transformation and sustainable finance, are expected to drive operational efficiencies and attract environmentally conscious investors. The bank's focus on digital transformation, particularly through RCBC Pulz, positions it well to capitalize on the evolving financial landscape. With a focus on both corporate and consumer loans, RCBC is strategically positioned for continued growth. This approach is a key component of the RCBC Business Model.

RCBC's commitment to sustainable finance, including green bond issuances, aligns with global trends and attracts environmentally conscious investors. The bank's ability to maintain a healthy NPL ratio and coverage ratio further strengthens its financial position. For a deeper understanding of the bank's ownership structure, consider reading the article Owners & Shareholders of RCBC.

RCBC reported a net income of P2.1 billion in Q1 2024, marking a 19% year-on-year increase. This growth highlights the bank's strong financial performance and effective strategies. This positive trend supports the bank's overall RCBC Future Prospects.

The gross loan portfolio expanded by 17% to reach P672 billion in Q1 2024. Both corporate and consumer loans contributed to this growth. The bank is targeting double-digit loan growth for the full year 2024.

Net interest income increased substantially, rising by 24% to P9.8 billion in Q1 2024. This significant increase demonstrates the bank's ability to generate revenue efficiently. This is a key factor in the RCBC Company Analysis.

Credit card receivables surged by 29% in Q1 2024, indicating strong consumer spending. This growth reflects effective credit card acquisition strategies. This growth is a key indicator of RCBC's expansion plans in the Philippines.

Asset Quality and Strategic Focus

RCBC's asset quality improved, with the non-performing loan (NPL) ratio decreasing to 2.44% in Q1 2024. The NPL coverage ratio stood at a healthy 119.5%. The bank's strategic focus on digital transformation and sustainable finance is expected to drive future profitability.

- Digital Transformation: RCBC Pulz is expected to drive operational efficiencies.

- Sustainable Finance: Green bond issuances attract environmentally conscious investors.

- Customer Base: Digital transformation expands customer base.

- Economic Expansion: Supported by the Philippines' economic expansion.

RCBC Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow RCBC’s Growth?

The RCBC Growth Strategy faces several potential risks and obstacles that could impact its future prospects. The competitive landscape within the Philippine banking industry, coupled with evolving regulations, presents ongoing challenges. Adapting to technological advancements and maintaining robust cybersecurity measures are also critical for sustained success.

RCBC Company Analysis reveals that economic downturns and unforeseen global events could affect the bank's financial performance. Furthermore, geopolitical instability and supply chain vulnerabilities, while less direct, could indirectly affect the operating environment. To navigate these challenges, RCBC employs a comprehensive risk management framework.

The bank's proactive approach to digital transformation and its focus on financial inclusion are key strategies to build resilience. Understanding these risks is crucial for evaluating the RCBC Future Prospects and its ability to achieve its strategic goals.

Intense Market Competition

The Philippine Banking Industry is highly competitive, with numerous players vying for market share. This competition can pressure interest margins, impacting profitability. Continuous innovation is essential to retain and attract customers in this environment.

Regulatory Changes

The Bangko Sentral ng Pilipinas (BSP) frequently introduces new regulations. These changes, concerning capital adequacy, consumer protection, and digital banking, can increase operational costs. Adapting to these regulatory shifts requires significant resources and strategic flexibility.

Technological Disruption

Rapid technological advancements, especially in fintech and AI, pose a significant risk. To stay competitive, RCBC must constantly evolve its offerings. Failure to do so could result in being outmaneuvered by agile competitors or new entrants.

Cybersecurity Threats

Cybersecurity threats are a continuous operational risk, given the increasing sophistication of cyberattacks. Investing in robust cybersecurity measures is essential to protect customer data and maintain trust. This is a critical area for financial institutions.

Economic Downturns

Economic downturns or unforeseen global events could impact loan demand and increase non-performing loans. These conditions could reduce overall profitability. RCBC must prepare for potential economic fluctuations.

Geopolitical Instability

Geopolitical instability and supply chain vulnerabilities, though less directly impactful on a universal bank, could indirectly affect the economic environment. These factors could create uncertainty and impact the bank's operations.

To mitigate these risks, RCBC employs a comprehensive risk management framework. This includes diversifying its loan portfolio across various sectors and customer segments to reduce concentration risk. Regular stress tests and scenario planning are also conducted to assess resilience against adverse economic conditions. Moreover, the bank's digital transformation and financial inclusion initiatives, like ATM Go, serve to diversify service channels and customer base.

RCBC's strategic initiatives include a focus on digital transformation and financial inclusion. These efforts aim to diversify service channels and customer base. The bank's investment in technology and its adaptation to fintech are crucial for maintaining a competitive edge. For more details, explore the Revenue Streams & Business Model of RCBC.

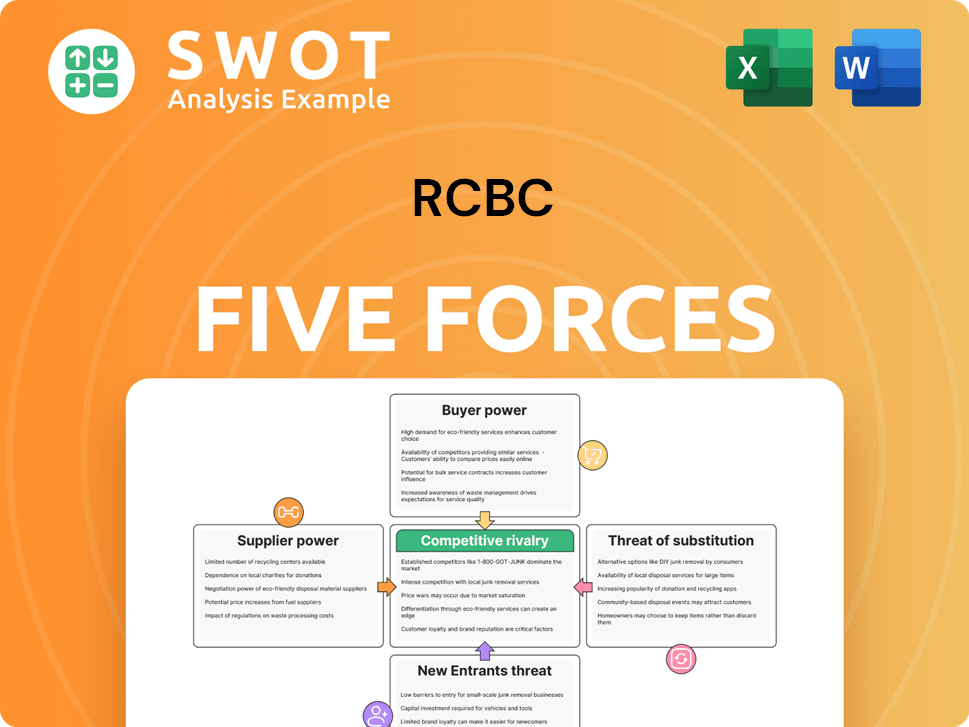

RCBC Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of RCBC Company?

- What is Competitive Landscape of RCBC Company?

- How Does RCBC Company Work?

- What is Sales and Marketing Strategy of RCBC Company?

- What is Brief History of RCBC Company?

- Who Owns RCBC Company?

- What is Customer Demographics and Target Market of RCBC Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.