Northeast Bank Bundle

Can Northeast Bank Sustain Its Impressive Growth Trajectory?

Founded in 1872, Northeast Bank has transformed from a local Maine institution into a regional banking force with national aspirations. Managing $4.23 billion in total assets by Q3 2025, a 35% surge from June 2024, showcases its remarkable expansion. This growth is fueled by a dual-growth strategy, blending community banking with a robust national lending division and digital innovation. The bank's loan portfolio has grown by an impressive 37.7% since June 30, 2024, reaching $3.80 billion, particularly through strategic loan acquisitions, setting the stage for an in-depth analysis.

This Northeast Bank SWOT Analysis provides a comprehensive overview of the bank's strategic initiatives and financial performance. Delving into Northeast Bank's future prospects requires an understanding of its expansion plans, competitive landscape, and customer acquisition strategies within the banking industry. We will explore Northeast Bank's digital transformation strategy and its impact on the local economy. Furthermore, we will analyze its profitability, risk management, and sustainable growth strategies, providing insights into its long-term investment potential and market share analysis.

How Is Northeast Bank Expanding Its Reach?

The Northeast Bank growth strategy heavily relies on its expansion initiatives, particularly through its National Lending Division and its online savings platform, ableBanking. This approach allows the bank to broaden its loan portfolio and diversify revenue streams by accessing new markets nationwide. The bank's ability to acquire opportunistic loans and form strategic partnerships is pivotal to its expansion plans. The bank's recent performance indicates a strong focus on growth and strategic positioning within the banking industry analysis.

The bank has been aggressively acquiring loans in high-yield segments. This strategy is evident in its recent acquisitions, including a significant volume of commercial real estate loans. These initiatives are aimed at strengthening its market position and increasing profitability. This proactive approach to expansion is a key factor in understanding the Northeast Bank future prospects.

As of Q2 2025, the National Lending Division's loan book reached $3.6 billion. This growth reflects the bank's commitment to expanding its lending operations. The bank's strategic moves and financial results provide valuable insights into its performance and future potential. For more details, you can read about Owners & Shareholders of Northeast Bank.

Since June 30, 2024, the bank acquired $805 million in commercial real estate loans, marking its second-largest quarterly loan purchase volume. This follows a previous acquisition of $1 billion in loans in late 2022. These acquisitions are a key element of the bank's expansion strategy.

The bank's partnership with Newity in the SBA loan market has propelled it to become the nation's number-one SBA lender by deal volume in early fiscal 2025. SBA loan originations increased significantly, reaching $121.3 million in Q3 2025, a substantial rise from $29.0 million year-over-year. This partnership is a significant driver of growth.

The bank is leveraging at-the-market (ATM) equity funding, aiming to raise up to $75 million. This funding is intended to materially increase its SBA lending volumes. This strategy supports its growth initiatives and strengthens its financial position.

In July 2024, the bank partnered with CorServ to launch a comprehensive credit card program for its business and commercial customers. This initiative aims to provide tailored banking solutions and expand its service offerings. This strategic move enhances its customer service capabilities.

Key Expansion Strategies

The bank's expansion initiatives are multifaceted, encompassing strategic loan acquisitions, SBA lending partnerships, and leveraging equity funding. These strategies are designed to drive growth and enhance market share. They demonstrate a proactive approach to the financial institution performance.

- Aggressive acquisition of high-yield loans, particularly in commercial real estate.

- Strategic partnership with Newity to become a leading SBA lender.

- Utilizing ATM equity funding to boost SBA lending volumes.

- Launching a credit card program in partnership with CorServ.

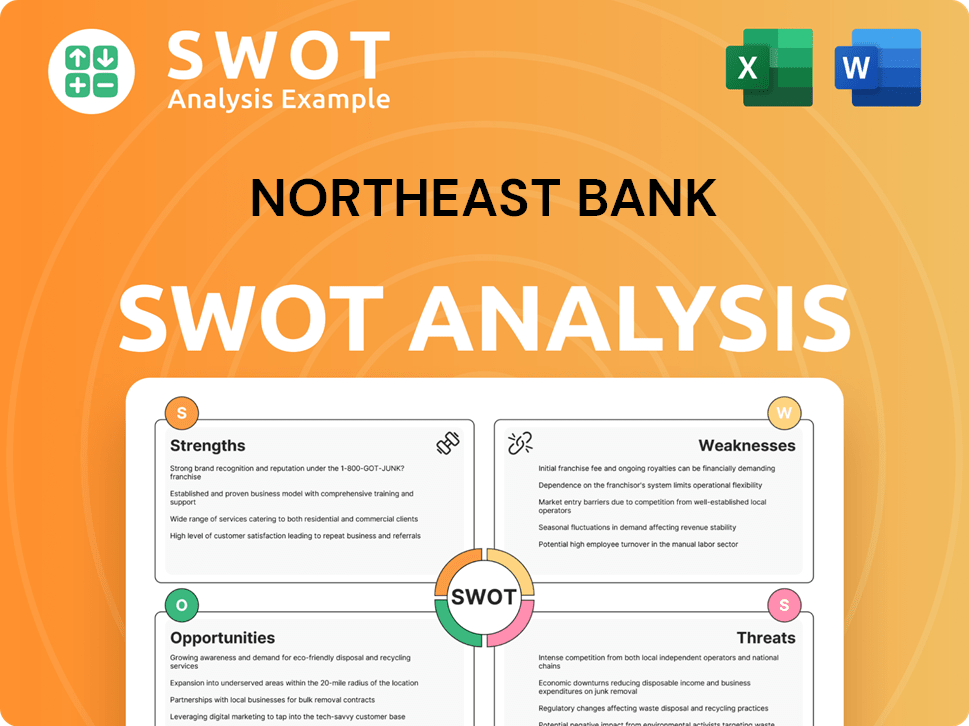

Northeast Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Northeast Bank Invest in Innovation?

The financial sector is rapidly evolving, with customer expectations and technological advancements reshaping the banking landscape. To stay competitive, financial institutions must prioritize digital transformation and customer-centric strategies. Addressing these needs is crucial for sustained growth and market share expansion.

Understanding the current market dynamics and anticipating future trends is essential for any financial institution aiming for success. This involves a deep dive into customer preferences, technological innovations, and the competitive landscape. This helps to create strategies that enhance customer experience and drive operational efficiency.

The Marketing Strategy of Northeast Bank showcases the bank's commitment to innovation and customer satisfaction, highlighting its proactive approach to address these evolving demands.

Digital Account Opening

A key element of the bank's innovation strategy is the digital account opening experience, launched in September 2023. This initiative, powered by Narmi, enables customers to open accounts online efficiently.

Deposit Growth

The digital-first approach has significantly boosted deposit growth. CD growth has increased by well over 300% since the partnership with Narmi.

Omnichannel Banking

The bank is committed to providing an omnichannel banking experience. This ensures that customers can seamlessly interact across various channels without any functional lag.

Digital Banking Services

The bank offers comprehensive digital banking services. This includes online, mobile, and telephone banking platforms, alongside remote deposit capture.

Strategic Partnerships

The bank strategically partners with technology providers. This is evident through its use of Narmi and CorServ, demonstrating its commitment to cutting-edge solutions.

Commercial Credit Cards

The bank utilizes CorServ for its commercial credit card programs. This enhances its offerings and supports its growth objectives.

Key Technological Integrations

The bank’s technology strategy focuses on enhancing customer experience and operational efficiency through digital tools and strategic partnerships. These integrations support the bank's objectives for growth.

- Narmi: Powers the digital account opening process, enabling quick and efficient account setup.

- CorServ: Provides commercial credit card programs, expanding financial service offerings.

- Omnichannel Banking: Ensures consistent functionality across all banking channels, improving customer satisfaction.

- Digital Deposit Program: AbleBanking, serves customers across the U.S., expanding the bank's reach.

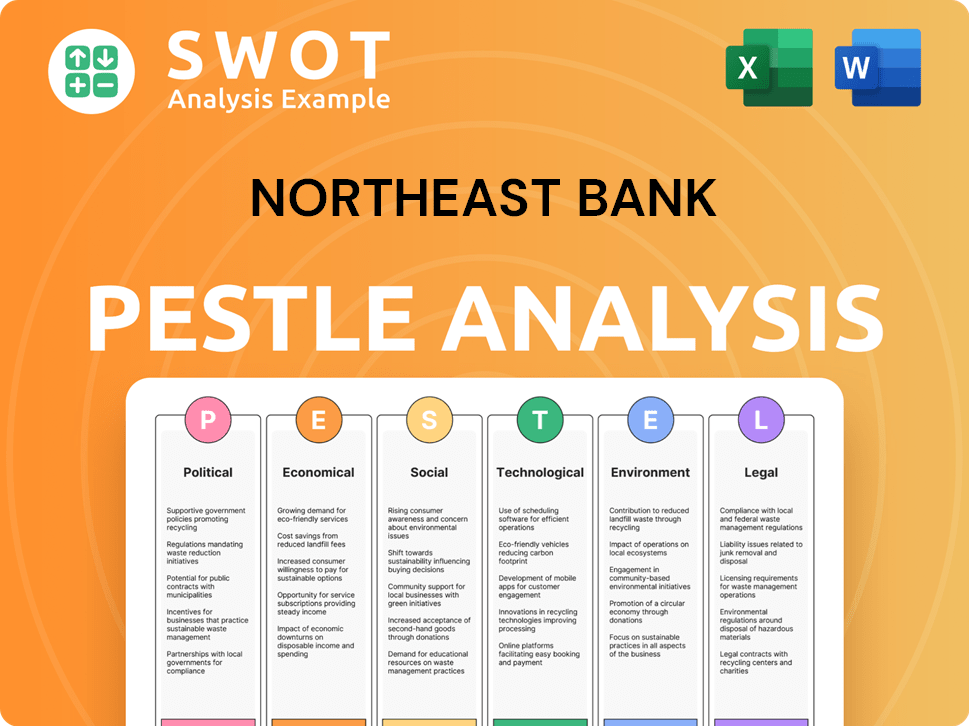

Northeast Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Northeast Bank’s Growth Forecast?

The financial outlook for Northeast Bank is robust, underpinned by strong recent performance and strategic initiatives. The bank has demonstrated impressive growth, with key metrics signaling a positive trajectory. This outlook is further supported by strategic decisions and analyst forecasts, making it a noteworthy subject for Banking industry analysis and investors alike.

Northeast Bank's financial performance is a key indicator of its Northeast Bank growth strategy and future potential. The bank's ability to maintain profitability while expanding its loan portfolio and assets highlights its effective management and strategic focus. Investors and stakeholders should pay close attention to the trends and projections.

For the third quarter of fiscal year 2025, Northeast Bank reported a net income of $18.7 million, marking a significant 34.5% increase year-over-year from $13.9 million in Q3 FY2024. Total assets grew by 35%, reaching $4.23 billion from $3.13 billion in June 2024. The loan portfolio expanded substantially by 37.7% to $3.80 billion since June 30, 2024, driven by its National Lending Division and the small balance SBA 7(a) program. This strong financial performance provides a solid foundation for the bank's future prospects.

Northeast Bank's disciplined approach is evident in its key financial metrics, which include a 15% annual credit portfolio growth with a delinquency rate below the industry average. The bank's 17% return on equity (ROE) outperforms its peers, and a 4.9% net interest margin (NIM) is driven by high-yielding loan purchases. These metrics underscore the bank's strong Financial institution performance.

The bank maintains a strong efficiency ratio of 42%, which is well below the industry average. In December 2024, Northeast Bank announced an at-the-market (ATM) offering of its voting common stock, aiming to raise up to $75 million. The proceeds are intended for general corporate purposes and to support additional growth. These strategic initiatives are designed to enhance the bank's Regional bank outlook.

Analysts forecast the NBN stock price to rise over the next 12 months, with an average 1-year price target of $106.50. The market is also revising upward the revenue expectations for Northeast Bank for FY2025. This positive outlook reflects confidence in the bank's Northeast Bank and its long-term investment potential.

The ATM offering of common stock is a strategic move to bolster the bank's capital base, supporting its expansion plans and Northeast Bank expansion plans. This capital injection will enable the bank to pursue further growth opportunities and strengthen its market position. This is a key element of the Northeast Bank strategic initiatives 2024.

Investment Opportunities and Market Analysis

Northeast Bank presents attractive Northeast Bank investment opportunities, supported by strong financial performance and strategic initiatives. An in-depth Northeast Bank financial performance review reveals the bank's robust growth trajectory. The bank's ability to outperform its peers and its strategic focus on high-yielding loans and efficient operations position it favorably. For more insights, consider reading about the Mission, Vision & Core Values of Northeast Bank.

- The bank's strong ROE and NIM indicate effective management and profitability.

- The expansion of the loan portfolio and asset growth are key drivers of future performance.

- The ATM offering of common stock will support further growth and strategic initiatives.

- Analysts' positive stock price forecasts reflect confidence in the bank's long-term potential.

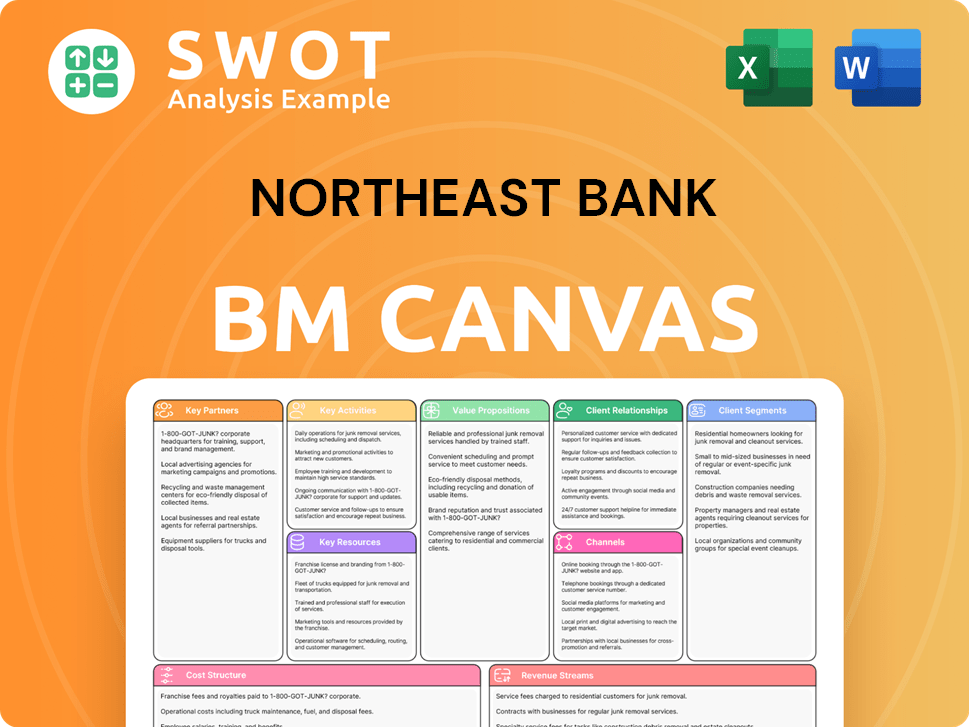

Northeast Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Northeast Bank’s Growth?

The growth strategy of Northeast Bank faces several challenges, including competition and economic uncertainties. The bank must navigate a dynamic market while managing risks related to lending and regulatory changes. Understanding these potential obstacles is crucial for assessing the bank's future prospects.

Market competition presents a significant risk, with larger national banks potentially impacting pricing power. Economic downturns and rising interest rates also pose challenges, potentially affecting commercial lending. Despite maintaining low non-performing assets, continuous monitoring of these risks is essential.

Regulatory changes and cybersecurity threats add further complexity to Northeast Bank's operational environment. Compliance costs and digital banking risks require proactive management to protect profitability and customer data. The bank's risk management framework is designed to address these multifaceted challenges.

Market Competition

Larger national banks could undercut pricing, affecting Northeast Bank's market share. The Northeast Bank must compete with institutions that may have greater resources and broader geographic reach, which could pressure profit margins. This competitive landscape requires careful strategic planning and execution.

Economic Downturns and Interest Rate Risks

Economic downturns and rising interest rates could impact commercial lending. A potential spike in non-performing loans (NPLs) is a key concern. While Northeast Bank has demonstrated strong credit quality, with NPAs at 0.8% as of September 2024, the bank must remain vigilant.

Regulatory and Compliance Costs

Changes in regulations, particularly those related to digital banking and interstate lending, could increase costs. These costs can squeeze profit margins. The bank needs to adapt to evolving regulatory environments to maintain financial stability.

Cybersecurity and Digital Banking Threats

Cybersecurity risks are increasing, with the average cost of a data breach in financial services reaching $5.72 million in 2023. Banking-related cyberattacks increased by 61% from 2022 to 2023. Northeast Bank needs to invest in robust cybersecurity measures to protect customer data and financial assets.

Risk Management Framework

Northeast Bank’s risk management framework is crucial for mitigating potential threats. With a dedicated Risk Management Department comprising 37 specialized professionals, the bank conducts quarterly comprehensive risk assessments. This disciplined approach is vital for sustainable growth.

Capital-Light Structure

The bank's capital-light structure helps in managing risks and enhancing financial flexibility. This strategic approach supports the bank’s ability to adapt to market changes and maintain strong credit quality. Northeast Bank is focused on long-term financial health.

Northeast Bank employs several strategies to mitigate identified risks. The bank maintains strong credit quality, with a conservative loan-to-value (LTV) ratio averaging 48% as of Q4 2024. Continuous monitoring and disciplined execution are key components of their risk management approach. This helps ensure financial stability and supports the bank's Brief History of Northeast Bank.

Comparing Northeast Bank’s performance to industry averages provides valuable context. The bank's exceptionally low NPAs of 0.8% as of September 2024, compared to the industry average of 1.5%, highlight its strong credit management. This performance reflects effective risk assessment and mitigation strategies.

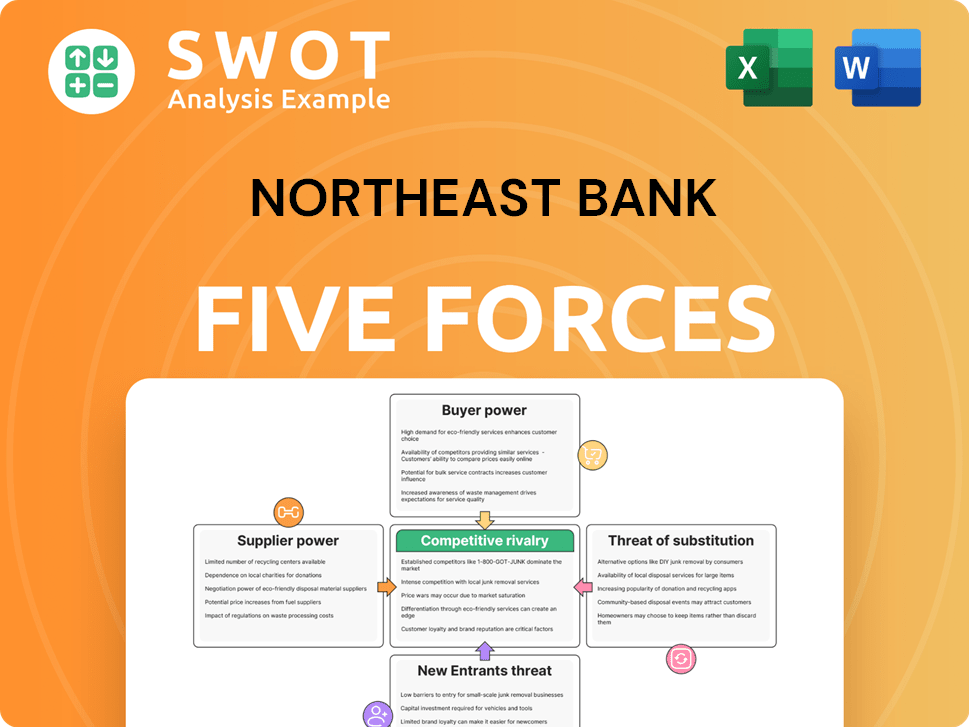

Northeast Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Northeast Bank Company?

- What is Competitive Landscape of Northeast Bank Company?

- How Does Northeast Bank Company Work?

- What is Sales and Marketing Strategy of Northeast Bank Company?

- What is Brief History of Northeast Bank Company?

- Who Owns Northeast Bank Company?

- What is Customer Demographics and Target Market of Northeast Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.