Humm Group Bundle

Can Humm Group Continue Its Ascent in the Fintech Arena?

Humm Group, a key player in the financial services sector, has evolved significantly since its inception, transforming from Certegy Ezi-Pay to a leading provider of buy now, pay later (BNPL) solutions. With a strong presence in Australia and New Zealand, the company's journey reflects the critical role of a robust growth strategy in a competitive market. This article explores the Humm Group SWOT Analysis and its future prospects.

As the BNPL market continues to evolve, understanding Humm Group's growth strategy becomes paramount. The company's strategic initiatives and expansion plans are crucial for investors and stakeholders alike, especially considering the dynamic shifts in the financial landscape. This analysis will provide insights into Humm Group's business model and its approach to navigating the challenges and opportunities within the buy now pay later market, offering a comprehensive view of its potential for long-term growth and financial performance.

How Is Humm Group Expanding Its Reach?

The Humm Group growth strategy centers on expanding its market presence and diversifying its revenue streams. This involves strengthening its position in existing markets, particularly Australia and New Zealand, while exploring opportunities in new sectors. The company aims to capture a broader range of consumer spending by moving beyond its traditional strongholds.

Humm Group's expansion plans include enhancing its existing Buy Now, Pay Later (BNPL) products to cater to a wider range of transaction values. This includes refining credit assessment models to improve customer experience. Partnerships with major retailers and e-commerce platforms are crucial to the company's expansion, increasing visibility and accessibility to potential customers.

The company's strategic initiatives are driven by the need to access new customer segments, diversify its revenue base, and maintain a competitive edge in the financial services landscape. The company's focus is on sustainable growth and adapting to the evolving market dynamics. For a deeper understanding of the company's financial model, consider exploring Revenue Streams & Business Model of Humm Group.

Humm Group is actively working to strengthen its presence in Australia and New Zealand. This involves increasing merchant partnerships and customer acquisition. The company is focused on expanding its BNPL services within these key markets to drive growth and market share.

The company is exploring opportunities to expand its BNPL services into new retail sectors. This includes targeting segments like healthcare, home improvement, and automotive. These sectors offer larger ticket items that align well with its financing solutions, providing new avenues for revenue growth.

Humm Group is enhancing its existing BNPL products, such as 'humm big things' and 'humm little things'. These enhancements aim to cater to a broader spectrum of transaction values. This includes refining credit assessment models to improve customer experience and promote responsible lending.

Partnerships with major retailers and e-commerce platforms are crucial. By integrating its payment solutions directly into the checkout process of more merchants, Humm Group aims to increase its visibility and accessibility to potential customers. These partnerships are key for customer acquisition and transaction volume growth.

Key Expansion Strategies

The company's expansion strategy is multifaceted, focusing on market penetration, sector diversification, and product enhancements. These initiatives aim to drive sustainable growth and enhance the company's competitive position in the BNPL market. The focus is on both organic growth and strategic partnerships.

- Strengthening presence in Australia and New Zealand.

- Expanding into new retail sectors like healthcare and home improvement.

- Enhancing existing BNPL products and refining credit assessment models.

- Forming strategic partnerships with major retailers and e-commerce platforms.

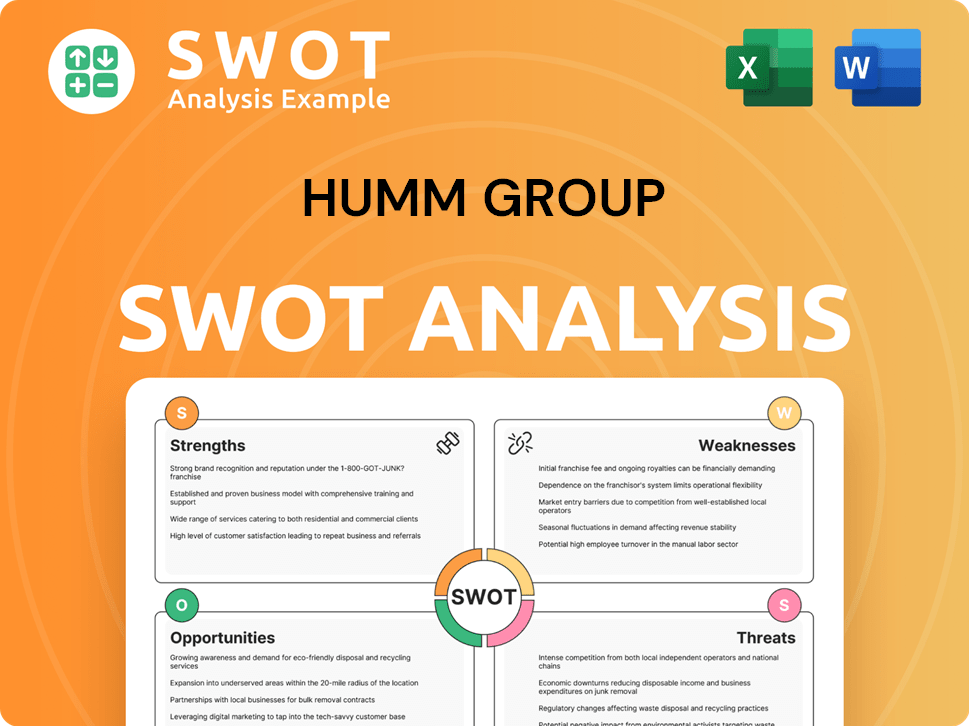

Humm Group SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Humm Group Invest in Innovation?

The growth strategy of the company is heavily reliant on its technological advancements and innovative approaches. The company consistently invests in research and development to enhance its existing platforms and introduce new financial products, focusing on digital transformation and automation to boost operational efficiency and scalability.

A key element of this strategy involves the continuous improvement of its digital platforms, including both the consumer-facing app and merchant portals. This involves enhancing user experience, simplifying the application process, and integrating advanced analytics to provide personalized offers. These efforts are aimed at improving customer acquisition and retention, enhancing operational efficiency, and enabling the development of new, competitive products.

The company leverages data analytics and machine learning to refine its credit decisioning processes, aiming for faster approvals and reduced risk while ensuring responsible lending practices. This technological advancement allows the company to process a higher volume of transactions more efficiently and accurately. The company's commitment to technological innovation is crucial for maintaining a competitive edge in the rapidly evolving financial technology sector.

Digital Platform Enhancements

Focus on improving user experience within the consumer app and merchant portals. Streamlining the application process for a smoother customer journey. Integration of advanced analytics to offer personalized financial products and services.

Data Analytics and Machine Learning

Utilizing data analytics and machine learning to refine credit decision-making. Aiming for faster approval times while maintaining responsible lending practices. Improving the efficiency and accuracy of transaction processing.

Technological Integration

Exploring the potential of cutting-edge technologies like AI and IoT. Assessing how these technologies can optimize operations and improve fraud detection. Developing features like budgeting tools to add value for customers.

Competitive Edge

Ongoing investment in technology to maintain a competitive advantage. Adapting to the rapid evolution of the financial technology sector. Enhancing customer acquisition and retention through technological capabilities.

Operational Efficiency

Digital transformation and automation are central to operational efficiency. Processing a higher volume of transactions more efficiently and accurately. Improving customer experience.

Product Development

Enabling the development of new, competitive products. Utilizing advanced AI to refine credit scoring models. Offering tailored financial solutions.

The company's strategy includes exploring the potential of advanced technologies like AI and IoT to enhance its offerings. While specific details on new patents or industry awards for 2024-2025 are not widely publicized, the company's ongoing investment in its technology stack demonstrates its dedication to maintaining a competitive edge. For example, advanced AI could further refine its credit scoring models, leading to more precise risk assessments and better customer segmentation. The development of new features within its app, such as budgeting tools or personalized spending insights, also showcases its commitment to leveraging technology to add value for its customers. For additional insights into the company's target market, consider reading the article on Target Market of Humm Group.

Key Technological Initiatives

The company's technological initiatives are focused on enhancing user experience, streamlining processes, and integrating advanced analytics. These efforts contribute to the company's growth objectives by improving customer acquisition and retention, enhancing operational efficiency, and enabling the development of new, competitive products.

- Platform Enhancements: Continuous improvement of digital platforms, including the consumer app and merchant portals.

- Data-Driven Decision Making: Leveraging data analytics and machine learning to refine credit decisioning processes.

- AI and Automation: Exploring the application of AI and automation to optimize operations and improve fraud detection.

- Product Innovation: Developing new features, such as budgeting tools, to add value for customers.

- Competitive Advantage: Investing in technology to maintain a competitive edge in the financial technology sector.

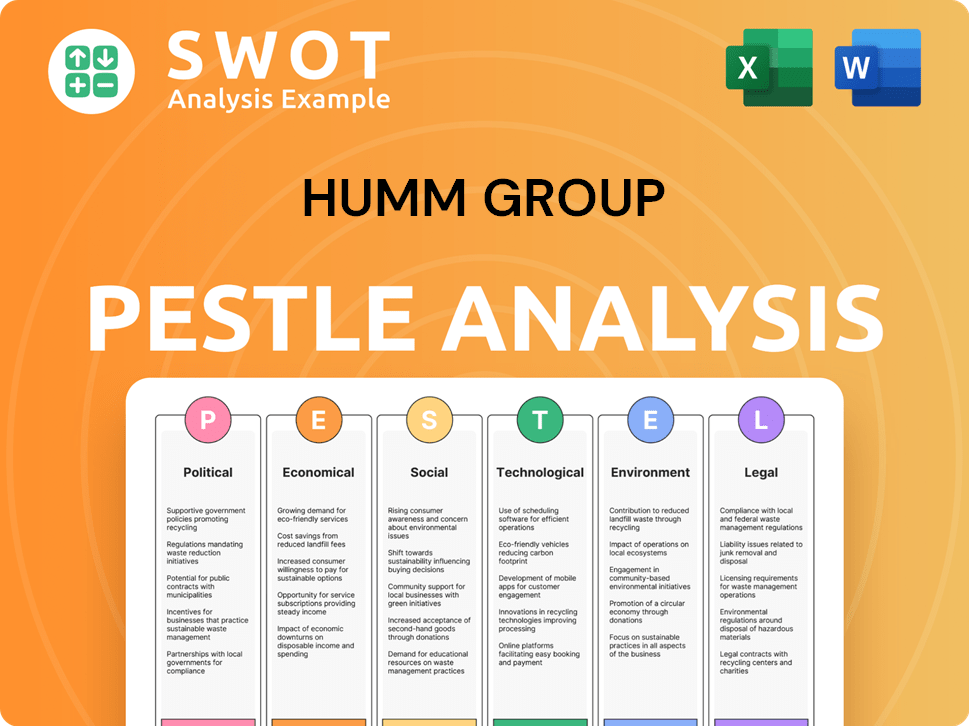

Humm Group PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Humm Group’s Growth Forecast?

The financial outlook for Humm Group reflects a strategic pivot towards sustainable growth and profitability within the competitive buy now, pay later (BNPL) market. The company's recent performance highlights a focus on optimizing its existing portfolio and leveraging its stronger performing segments. This approach is crucial in navigating the dynamic market landscape and achieving long-term success.

In the first half of the 2024 financial year, Humm Group demonstrated a significant turnaround, reporting a statutory net profit after tax of $3.5 million, a substantial improvement from a loss of $13.5 million in the prior corresponding period. This shift underscores the effectiveness of the company's strategic initiatives and its ability to adapt to market challenges. The financial results indicate a focus on disciplined growth, emphasizing profitability and efficiency.

Humm Group's business model is evolving to meet the demands of the market. The company's recent performance and strategic direction provide insights into its future prospects. For more details on the company's ownership, you can explore Owners & Shareholders of Humm Group.

Humm Group's financial performance in 1H24 showed a statutory net profit after tax of $3.5 million, a significant improvement from the $13.5 million loss in the prior period. This improvement was driven by strong results from the Commercial and New Zealand Consumer businesses. The overall net receivables grew by 2.6% to $923.5 million.

The Commercial segment, particularly with 'hummpro', experienced robust growth. Receivables in this segment increased by 21.3% to $233.1 million in 1H24. This strong performance indicates the effectiveness of the commercial strategy and its contribution to the overall Humm Group growth strategy.

The New Zealand Consumer business also performed well, with receivables up 11.2% to $201.2 million. Gross Loans and Advances in this segment increased by 20.3% to $240.2 million, highlighting the success of Humm Group's expansion plans in this market.

The Australian Consumer business faced challenges, with Gross Loans and Advances decreasing by 17.5% to $489.1 million in 1H24. This segment faces intense competition and a challenging economic environment, impacting the overall Humm Group market analysis.

Strategic Focus Areas

Humm Group is focusing on higher-yielding commercial and New Zealand consumer finance. This strategic shift aims to improve overall portfolio quality and profitability. The company is also emphasizing cost management to enhance financial efficiency.

Cost Management

Operating expenses decreased by 12.3% in 1H24 compared to the previous corresponding period. This demonstrates Humm Group's commitment to optimizing its cost structure and improving profitability. Such measures are crucial for the Humm Group business model analysis.

Market Dynamics

The BNPL market is highly competitive, requiring continuous adaptation and strategic adjustments. Humm Group's ability to navigate these dynamics will be key to its future prospects. Understanding the Humm Group competitive landscape is essential.

Revenue Growth Drivers

The company is leveraging its stronger performing segments, such as the Commercial and New Zealand Consumer businesses, to drive revenue growth. This strategic focus helps in improving the Humm Group financial performance. This strategy is a key part of the Humm Group buy now pay later strategy.

Profitability Analysis

The focus on higher-yielding segments and cost management contributes to enhanced profitability. The statutory net profit after tax of $3.5 million in 1H24 reflects this positive trend. This is a crucial aspect of the Humm Group investment potential.

Long-Term Growth

While specific forecasts are subject to market conditions, the company's recent performance suggests a focus on disciplined growth. This approach is vital for the Humm Group long-term growth forecast and overall success. The Humm Group strategic initiatives are designed to support this growth.

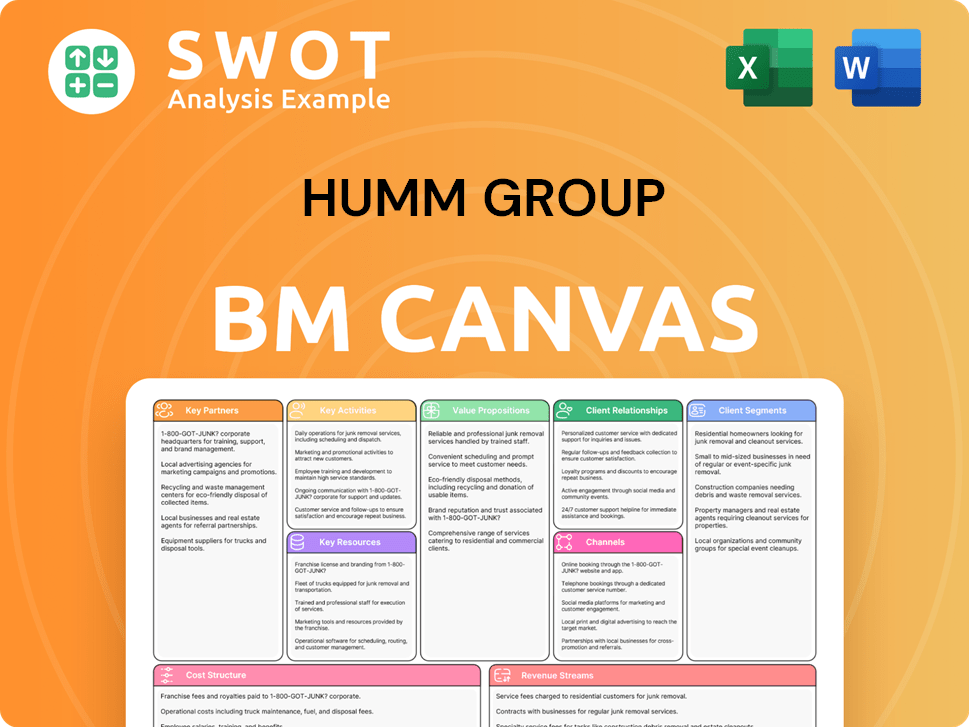

Humm Group Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Humm Group’s Growth?

The Humm Group growth strategy faces several potential risks and obstacles that could influence its Humm Group future prospects. The competitive landscape in the Buy Now, Pay Later (BNPL) sector is intense, with established players and new entrants vying for market share. This competition can squeeze profit margins and increase the costs associated with acquiring new customers, thereby affecting Humm Group's business performance.

Regulatory changes also pose a significant challenge. The BNPL industry is under increasing scrutiny from financial authorities worldwide. Stricter regulations related to consumer protection, responsible lending, and data privacy could lead to higher compliance costs and changes to the business model, which would impact Humm Group. The company actively monitors and adapts to these evolving regulatory requirements.

Furthermore, technological disruption and broader economic factors add layers of complexity. Rapid advancements in financial technology could introduce new payment methods, making existing BNPL services less attractive. Economic downturns, including rising interest rates and inflation, can impact consumer spending and increase credit risk. Humm Group addresses these challenges through robust risk management and strategic diversification.

Competitive Market Pressure

The BNPL market is highly competitive, with established players like Afterpay and Zip Co continuously innovating. New entrants and traditional credit providers also compete, applying pressure on merchant fees and customer acquisition costs. This intense competition can limit Humm Group's ability to maintain market share and revenue growth.

Regulatory Risks

Governments and financial authorities are increasing scrutiny of the BNPL industry, particularly in areas such as consumer protection and responsible lending. Stricter regulations could lead to higher compliance costs and operational changes. Humm Group must adapt to these changes to maintain compliance and profitability.

Technological Disruption

Rapid advancements in financial technology could introduce new payment methods that make existing BNPL services less appealing. Humm Group must invest in its technology platform and continuously innovate to remain competitive. Staying ahead of technological changes is crucial for long-term sustainability.

Economic Factors

Broader economic conditions, such as rising interest rates and inflation, can impact consumer spending and increase credit risk. A downturn in the economy could lead to higher default rates and affect Humm Group's loan book quality. Robust risk management is essential to navigate these challenges.

Cybersecurity and ESG Factors

Evolving cybersecurity threats and the increasing importance of environmental, social, and governance (ESG) factors present new risks. Cybersecurity breaches could affect operations and reputation. ESG considerations can influence investor sentiment and increase operational costs. Humm Group must address these emerging risks to maintain investor confidence.

Supply Chain Vulnerabilities

While less direct, supply chain issues can indirectly impact merchant partners and affect transaction volumes. Humm Group mitigates this through portfolio diversification and by focusing on both consumer and commercial lending. The company adapts to market challenges by shifting focus to higher-yielding segments.

Humm Group's financial performance is closely tied to its ability to manage these risks. The company's Humm Group market analysis reveals the importance of adapting to changing market dynamics. For example, in 2024, the company emphasized the Commercial and New Zealand Consumer businesses to navigate market challenges. Humm Group's Humm Group expansion plans must consider these factors to ensure sustainable growth and profitability. For more detailed insights, you can refer to this article on Humm Group's strategic initiatives.

Humm Group employs several strategies to mitigate these risks. These include robust risk management frameworks, portfolio diversification, and a focus on both consumer and commercial lending. The company actively monitors regulatory changes and adapts its internal frameworks to meet compliance requirements. Continuous innovation and investment in technology are also key to maintaining a competitive edge. The company's proactive approach is crucial for navigating the complex landscape of the BNPL market.

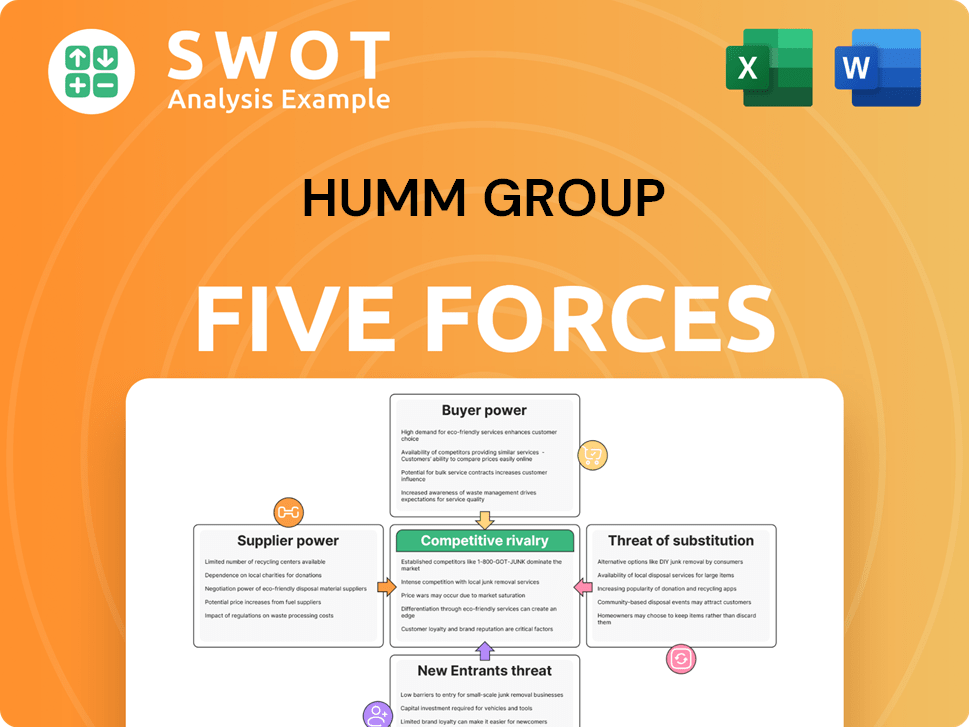

Humm Group Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Humm Group Company?

- What is Competitive Landscape of Humm Group Company?

- How Does Humm Group Company Work?

- What is Sales and Marketing Strategy of Humm Group Company?

- What is Brief History of Humm Group Company?

- Who Owns Humm Group Company?

- What is Customer Demographics and Target Market of Humm Group Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.