Home Bancorp Bundle

Can Home Bancorp Continue Its Impressive Growth?

Home Bancorp, Inc. is making waves as a significant regional financial institution, and its recent performance is turning heads. From its humble beginnings in 1908 as a community bank, Home Bancorp has evolved into a prominent player with a strong focus on customer relationships and local decision-making. With assets reaching $3.5 billion as of March 31, 2025, and a network of 43 locations, the company's growth is undeniable.

This analysis dives deep into the Home Bancorp SWOT Analysis, exploring its impressive Q1 2025 earnings, including net income of $11.0 million and diluted EPS of $1.37, to dissect the Home Bancorp growth strategy and future prospects. We'll examine the Home Bancorp financial performance, conduct a Home Bancorp market analysis, and evaluate the Home Bancorp business strategy to uncover potential Home Bancorp investment opportunities and assess the company's long-term growth potential. This exploration will also touch upon Home Bancorp's expansion plans and strategic initiatives, providing a comprehensive view of its trajectory.

How Is Home Bancorp Expanding Its Reach?

The growth strategy of Home Bancorp is heavily influenced by its expansion initiatives. These initiatives include both organic growth and strategic mergers and acquisitions, which are key components of their business strategy. The company's approach is designed to enhance its market presence and financial performance.

Since 2010, Home Bancorp has completed six acquisitions, contributing to substantial asset growth. As of March 31, 2025, the Compound Annual Growth Rate (CAGR) for assets stood at 12.3%. This demonstrates a commitment to strategic expansion and financial growth, positioning the company for future success.

Home Bancorp strategically expands its geographical footprint. A significant focus is on the Houston market, which now accounts for 20% of its loan portfolio and 11% of its deposits. This expansion is further evidenced by plans to open a new branch in Northwest Houston by late 2025. This expansion strategy aims to access new customer bases and diversify revenue streams.

Home Bancorp's loan portfolio totaled $2.7 billion at March 31, 2025. This reflects an increase of $29.1 million (1.1%) from December 31, 2024. This represents an annualized increase of 4%, indicating steady growth in lending activities.

Deposits reached $2.8 billion at March 31, 2025, marking a rise of $46.5 million (1.7%) from December 31, 2024. The annualized increase for deposits was 7%, demonstrating strong customer confidence and deposit growth.

The company anticipates loan growth to be between 4% and 6% in 2025. This projection reflects the Home Bancorp's strategic initiatives and its expectations for continued financial performance. These initiatives are designed to drive sustainable growth.

Home Bancorp maintains a diversified loan portfolio. Commercial real estate owner-occupied loans represent 26%, 1-4 family mortgages at 18%, and commercial real estate non-owner-occupied at 17% as of March 31, 2025. This diversification helps mitigate risk.

Strategic Risk Management

The strategic diversification across loan types and geographic markets helps mitigate risk and supports sustained growth. This approach is crucial for long-term growth potential. The company's expansion plans are designed to enhance shareholder value.

- Focus on the Houston market for expansion.

- Diversification across loan types.

- Strategic mergers and acquisitions.

- Anticipated loan growth between 4% and 6% in 2025.

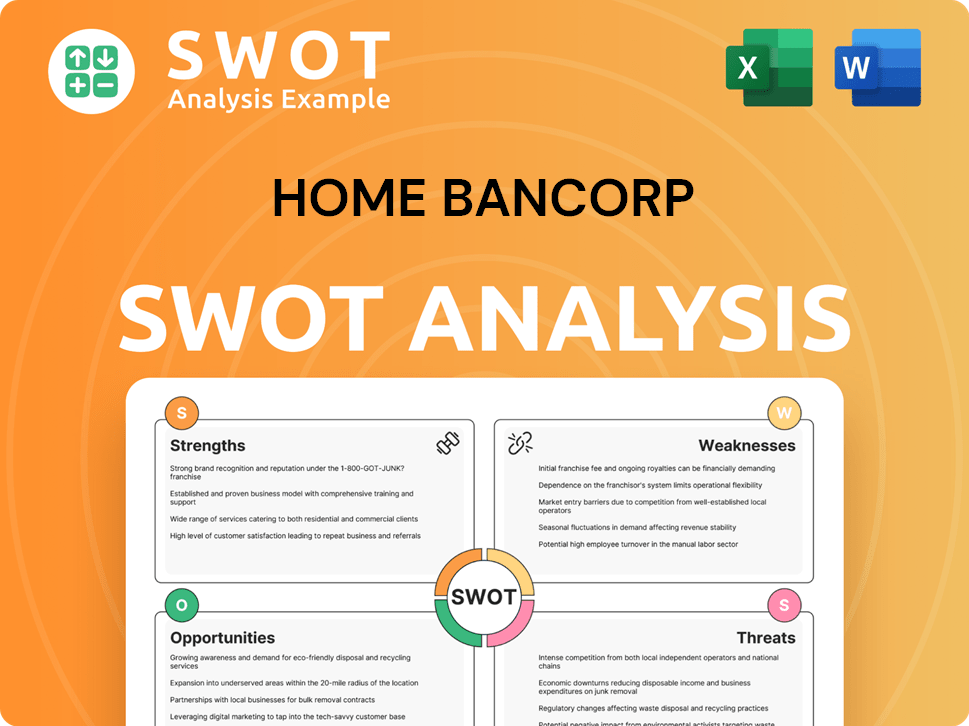

Home Bancorp SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Home Bancorp Invest in Innovation?

The company's approach to innovation and technology is geared towards enhancing operational efficiency and improving customer offerings. This strategy is crucial for sustaining growth, especially in a competitive financial landscape. While specific details on research and development investments are not always extensively disclosed, the emphasis on digital transformation and customer relationship management indicates a strong commitment to technological advancements.

The company's focus on community banking, coupled with a forward-looking approach to innovative banking options and new technology, showcases a strategy to meet evolving customer needs and maintain a competitive edge. This includes providing online banking services and leveraging technology to improve customer relationships. The company's ability to adapt and maintain strong performance, even amidst rapid interest rate changes, suggests a solid technological foundation supporting agile financial management.

The increasing non-interest expenses, particularly those related to data processing fees, occupancy costs, and professional services, highlight ongoing investments in technology and infrastructure. These investments are essential for supporting growth and improving operational efficiency. The company's strategic initiatives likely include modernizing its technological capabilities to enhance its services and streamline operations.

Digital Banking Services

The company offers online banking services. These digital platforms are essential for attracting and retaining customers in today's market. This includes mobile banking, online account management, and other digital tools.

Customer Relationship Management (CRM)

Technology is used to improve customer relationships. This involves using data analytics and CRM systems to understand customer behavior and preferences. This helps in providing personalized services and improving customer satisfaction.

Operational Efficiency

Technology investments aim to improve operational efficiency. This includes automating processes, reducing manual tasks, and streamlining workflows. This leads to cost savings and improved productivity.

Data Processing and Infrastructure

Investments in data processing and infrastructure are crucial. This includes upgrading IT systems, enhancing cybersecurity measures, and ensuring data integrity. These investments support the company's growth and operational efficiency.

Strategic Initiatives

The company likely has strategic initiatives focused on digital transformation. This includes adopting new technologies, exploring innovative banking options, and enhancing its digital capabilities. These initiatives are designed to meet evolving customer needs and stay competitive.

Financial Management

Technology supports agile financial management. This includes using advanced analytics and financial modeling tools to make informed decisions. This helps in maintaining profitability and navigating market changes effectively.

The company's financial performance, as discussed in Owners & Shareholders of Home Bancorp, is influenced by its technological investments. For 2025, the company anticipates a 3.5% increase in non-interest expenses, partly due to technology-related costs. This investment is critical for supporting the company's Home Bancorp growth strategy and future prospects. The effective pricing of loans and deposits, facilitated by technological capabilities, contributes to the expansion of the net interest margin. The company's focus on digital transformation and customer relationship management underscores its commitment to innovation, which is essential for long-term success in the financial sector. The company's ability to adapt to rapid interest rate changes and its consistent net interest margin expansion suggest an underlying technological capability that supports agile financial management.

Key Technological Investments

The company's technology strategy focuses on digital banking, customer relationship management, and operational efficiency. These investments are designed to meet evolving customer needs and stay competitive. Key areas of investment include:

- Online Banking Platforms: Enhancing digital banking services to provide convenient and secure access for customers.

- Data Analytics: Utilizing data analytics to understand customer behavior and personalize services.

- Automation: Implementing automation to streamline processes and reduce costs.

- Cybersecurity: Investing in robust cybersecurity measures to protect customer data and financial assets.

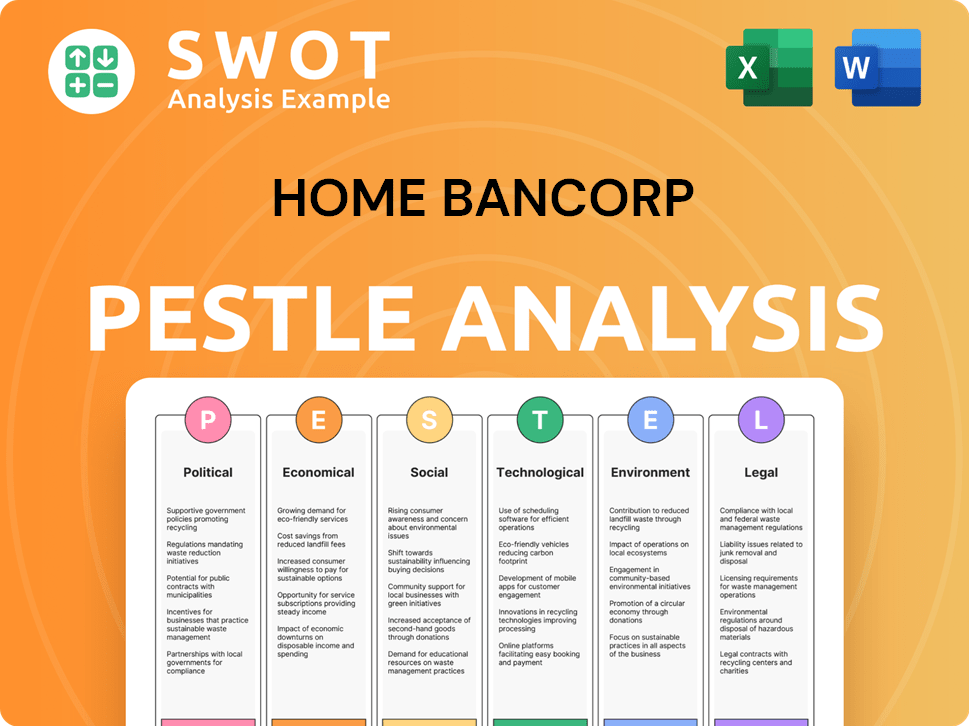

Home Bancorp PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Home Bancorp’s Growth Forecast?

The financial outlook for Home Bancorp is robust, with strong performance indicators and positive projections. The company's strategic initiatives and market analysis suggest a promising trajectory for future growth. This positive outlook is supported by recent financial results and strategic decisions.

Home Bancorp's financial performance in the first quarter of 2025 showcased significant growth. The company's ability to expand its net interest margin and maintain strong capital positions highlights its financial health. These achievements are crucial for sustaining long-term growth potential and enhancing shareholder value.

The company's commitment to shareholder returns, demonstrated by increased dividends and a new share repurchase plan, further underscores its financial strength. As the company navigates industry trends, its focus on digital transformation and customer acquisition strategies will likely contribute to its continued success. For more details, you can explore Revenue Streams & Business Model of Home Bancorp.

Home Bancorp reported a net income of $11.0 million, or $1.37 per diluted common share, for Q1 2025. This represents a 13% increase from the previous quarter and a 20% increase year-over-year. The company's earnings exceeded analyst estimates of $1.14 per share.

Net interest income for Q1 2025 was $31.7 million, up 1% from the prior quarter. The net interest margin expanded to 3.91% from 3.82% in Q4 2024, marking the fourth consecutive quarter of NIM expansion.

As of March 31, 2025, total assets reached $3.5 billion. Loans totaled $2.7 billion, and deposits were at $2.8 billion, demonstrating healthy balance sheet growth. This growth is a key indicator of the company's expansion plans.

The tangible common equity ratio improved to 9.4% from 8.7%, indicating a strengthening capital position. The quarterly dividend was increased to $0.27 per share, a 4% increase. The annualized payout now reaches $1.08 per share.

Loan Growth Projections

Management anticipates loan growth to be between 4% and 6% in 2025. This growth is expected to contribute to the company's revenue growth projections.

Non-Interest Income Forecast

Non-interest income is expected to range between $3.6 million and $3.8 million over the next two quarters. This forecast reflects the company's strategic initiatives.

Capital Ratios

As of March 31, 2025, the Tier 1 leverage ratio was 11.48%, and the total risk-based capital ratio was 14.58%. These ratios demonstrate the company's strong financial health and risk management strategies.

Dividend and Share Repurchase

The increased quarterly dividend of $0.27 per share and the new share repurchase plan highlight the company's commitment to shareholder value. These actions support Home Bancorp's business strategy.

Market Analysis and Industry Trends

The company's performance reflects positive industry trends and a strong market share analysis. These factors contribute to Home Bancorp's long-term growth potential.

Digital Transformation Strategy

Home Bancorp's digital transformation strategy is expected to enhance customer acquisition strategies and improve operational efficiency. This is a key aspect of the company's Home Bancorp growth strategy.

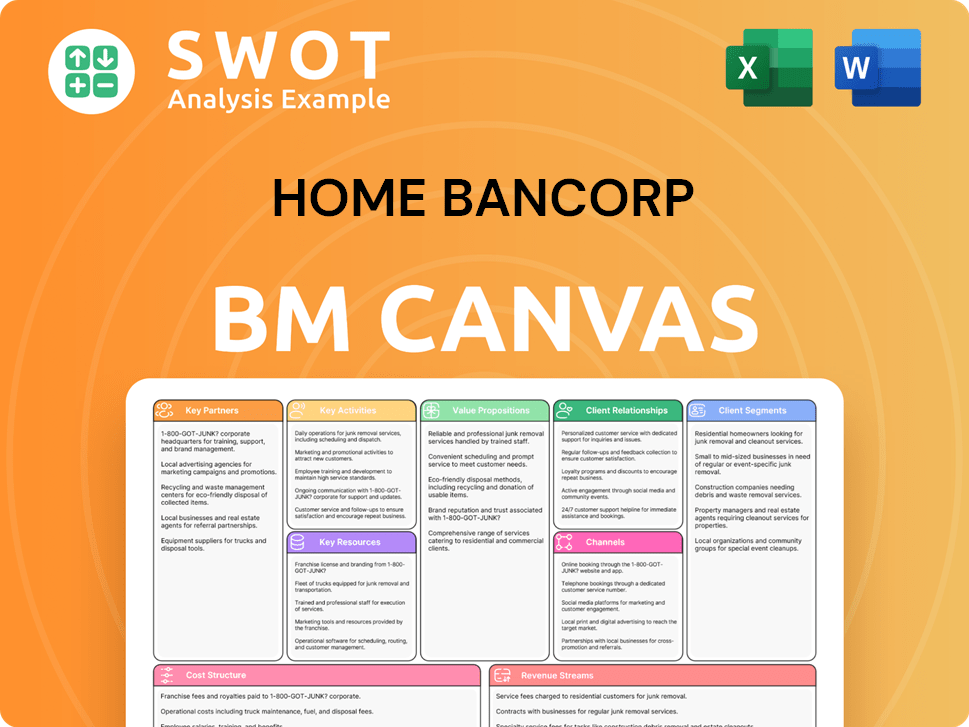

Home Bancorp Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Home Bancorp’s Growth?

Even with a positive outlook, Home Bancorp faces potential risks that could affect its growth. These challenges include market competition, regulatory changes, and credit quality concerns. Understanding these obstacles is crucial for evaluating Home Bancorp's long-term prospects.

The banking sector is highly competitive, which could influence loan yields and the ability to attract deposits. Moreover, evolving regulations require constant adaptation, potentially increasing operational costs and impacting strategic flexibility. These factors are essential for investors to consider when analyzing Home Bancorp's financial performance.

Credit quality is another area to watch. Nonperforming assets increased to $21.5 million, or 0.62% of total assets, by March 31, 2025, up from $15.6 million (0.45% of total assets) at the end of 2024. This rise, mainly due to two loan relationships reclassified as substandard in 2024 and moved to nonaccrual status in Q1 2025, could strain future earnings if loan defaults rise.

Market Competition

The banking sector is intensely competitive. This can affect Home Bancorp's ability to maintain loan yields and efficiently acquire deposits. Successfully navigating this competitive environment is crucial for sustained growth and maintaining a strong Marketing Strategy of Home Bancorp.

Regulatory Changes

Regulatory changes pose an ongoing risk. Home Bancorp must adapt to evolving compliance requirements. This constant adaptation can increase operational costs and limit strategic flexibility, impacting its ability to respond quickly to market opportunities and maintain profitability.

Credit Quality

Credit quality presents a continuous risk. Nonperforming assets rose to $21.5 million, or 0.62% of total assets, by March 31, 2025. While the net charge-off was relatively low at $32,000 in Q1 2025, sustained increases in non-performing assets could impact future earnings if loan defaults increase.

Economic Volatility and Interest Rates

Economic volatility and rising interest rates can affect loan demand and profitability. Home Bancorp's performance could be significantly impacted by economic downturns in its key markets. Management must effectively manage these risks through careful financial planning.

Risk Management Strategies

Home Bancorp employs disciplined capital management. It maintains strong capital ratios and a conservative credit culture to prepare for potential risks. A diversified loan portfolio across various segments and geographic markets helps mitigate concentration risks, enhancing its ability to withstand economic pressures.

Strategic Initiatives

The company's strategic initiatives are crucial for navigating challenges. Home Bancorp's ability to adapt its business strategy, expand its market share, and develop new customer acquisition strategies will be critical for long-term growth. Successful execution of these initiatives is key to mitigating risks.

Economic instability in key markets could decrease loan demand. Rising interest rates could also affect the profitability of loans. Home Bancorp's ability to navigate these economic challenges will be crucial for maintaining financial performance. These factors require proactive risk management.

Rising interest rates may affect loan demand and profitability. Home Bancorp's earnings can be sensitive to interest rate fluctuations. The company's management must carefully monitor and manage interest rate risk to protect its financial health. This includes adjusting loan pricing.

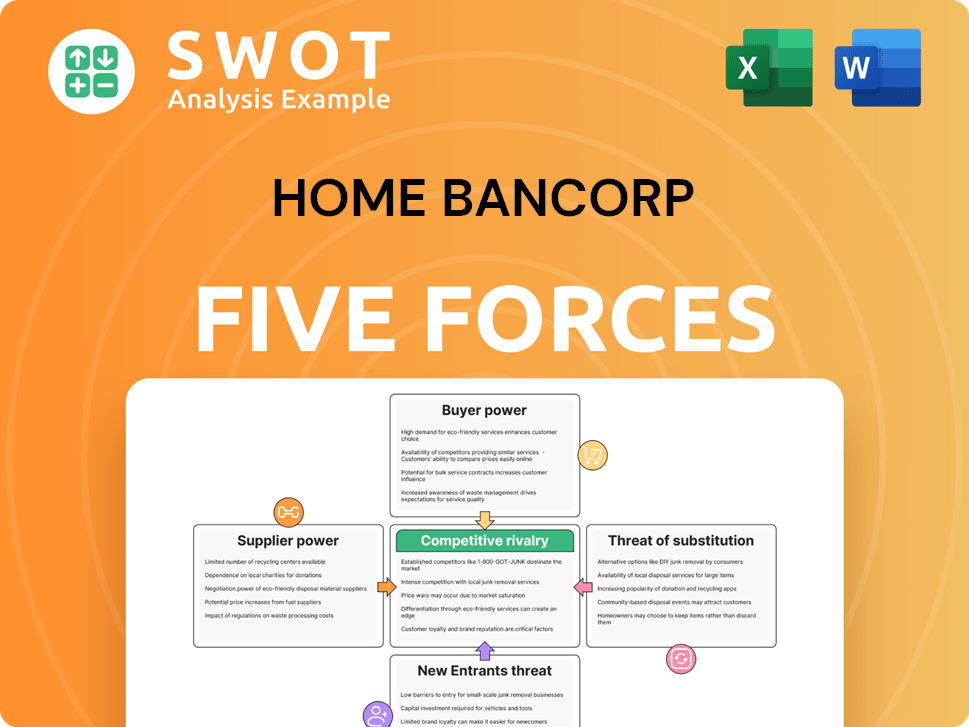

Home Bancorp Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Home Bancorp Company?

- What is Competitive Landscape of Home Bancorp Company?

- How Does Home Bancorp Company Work?

- What is Sales and Marketing Strategy of Home Bancorp Company?

- What is Brief History of Home Bancorp Company?

- Who Owns Home Bancorp Company?

- What is Customer Demographics and Target Market of Home Bancorp Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.