HDFC Bank Bundle

Can HDFC Bank Maintain Its Dominance in the Indian Banking Sector?

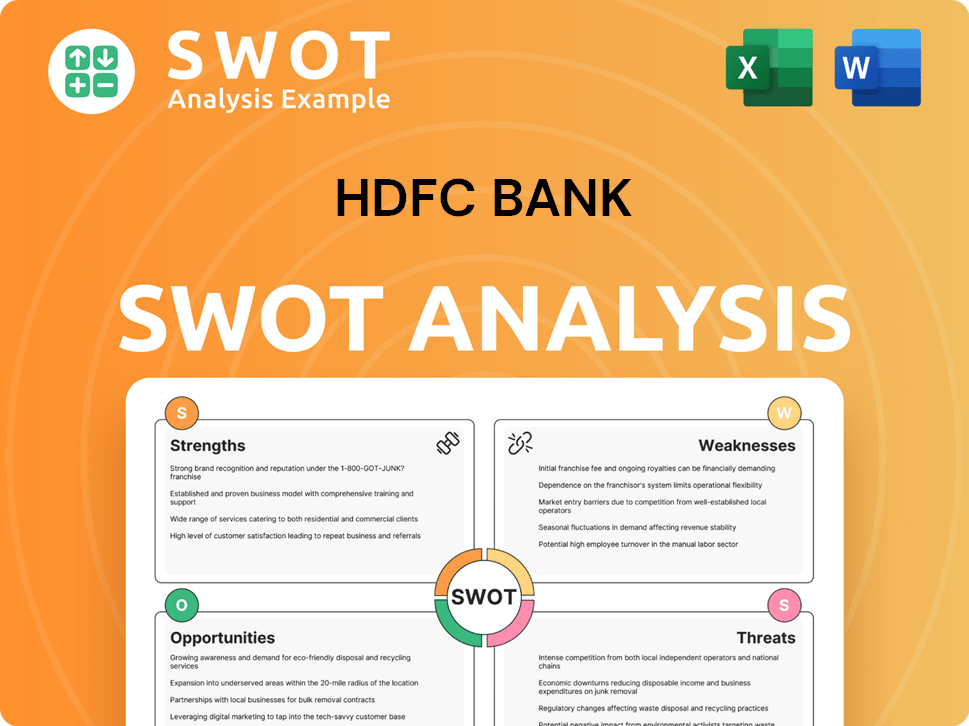

HDFC Bank, a titan of the Indian financial landscape, has consistently redefined the boundaries of growth. From its inception, driven by a vision to revolutionize housing finance, the bank has evolved into a financial powerhouse. This HDFC Bank SWOT Analysis provides a comprehensive overview of the bank's strengths and weaknesses, and opportunities and threats.

This analysis delves into the core of HDFC Bank's growth strategy, examining its impressive financial performance and market share within the Indian banking sector. We'll explore its future prospects, including expansion plans and digital banking initiatives, while considering the challenges and opportunities that lie ahead. Furthermore, the bank's commitment to sustainable banking practices and its impact on the Indian economy will be thoroughly evaluated.

How Is HDFC Bank Expanding Its Reach?

To drive future growth, HDFC Bank is undertaking several expansion initiatives. These initiatives focus on both increasing its geographical reach and diversifying its product offerings. The bank is strategically expanding its physical presence, particularly in rural and semi-urban areas, to tap into new customer bases and enhance its market share.

A key component of HDFC Bank's growth strategy involves a significant expansion of its branch network. Post-merger, the bank added 1,700 new branches and plans to roll out an additional 13,000 branches by 2028. This aggressive expansion is aimed at improving its Loan-to-Deposit Ratio (LDR) and boosting deposit growth. As of March 2024, the bank operates approximately 8,738 branches and 20,938 ATMs, serving customers across 4,065 cities in India.

Beyond physical expansion, HDFC Bank is focused on diversifying its product offerings and entering new market segments. The bank has launched over 250 innovative products catering to retail and corporate customers as of 2024. The bank is also keen on leveraging the growing corporate banking sector in India, anticipating double-digit growth in banking credit in the coming years. Furthermore, there is an unexplored potential for HDFC Bank to expand into overseas markets as globalization continues to grow.

HDFC Bank is actively expanding its physical presence, especially in rural and semi-urban areas. The bank aims to add 13,000 new branches by 2028, with a focus on Tier 2 and Tier 3 cities. As of March 2024, the bank has about 8,738 branches and 20,938 ATMs across 4,065 cities in India.

The bank is diversifying its product offerings to cater to both retail and corporate customers. Over 250 innovative products have been launched as of 2024. HDFC Bank is also focused on leveraging the growing corporate banking sector, anticipating significant growth in banking credit.

HDFC Bank is forming strategic partnerships with fintech companies and e-commerce platforms. These collaborations enable the bank to access new technologies and explore innovative business models. The bank is also involved in CSR initiatives like 'Parivartan' to support rural development and financial inclusion.

HDFC Bank is exploring opportunities to expand into overseas markets. As globalization continues, the bank sees potential for international growth. This expansion is expected to contribute to the bank's overall growth strategy and increase its global footprint.

Strategic Partnerships and CSR Initiatives

Strategic partnerships are crucial for HDFC Bank's growth, allowing access to new technologies and innovative business models. The bank's CSR initiative, 'Parivartan,' aims to increase the income of 5 lakh marginal farmers by 2025 and provide skill training to nearly 2 lakh individuals, demonstrating a commitment to rural development. This initiative also includes promoting 25,000 community-led enterprises, with 50% being women-led, and bringing 2 lakh acres of unirrigated land under irrigation by 2025.

- Collaborations with fintech and e-commerce platforms.

- 'Parivartan' initiative focused on rural development.

- Targeting financial inclusion and sustainable practices.

- Emphasis on supporting women-led enterprises.

The bank's focus on expansion, product diversification, and strategic partnerships supports its long-term growth objectives. For a deeper dive into the bank's marketing strategies, consider reading about the Marketing Strategy of HDFC Bank.

HDFC Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does HDFC Bank Invest in Innovation?

The innovation and technology strategy of HDFC Bank is crucial for its sustained growth within the Indian Banking Sector. This strategy focuses on leveraging technology to enhance customer experience, streamline operations, and maintain a competitive edge. The bank's commitment to digital transformation is evident through significant investments and the continuous development of cutting-edge solutions.

HDFC Bank's approach to technology is multifaceted, encompassing digital banking initiatives, partnerships with fintech companies, and core system overhauls. These efforts are designed to meet evolving customer needs and preferences, ensuring the bank remains at the forefront of financial innovation. This proactive stance is essential for navigating the dynamic landscape of the financial sector and capitalizing on future growth opportunities.

The bank's initiatives are geared towards improving efficiency, reducing costs, and offering innovative financial products and services. This includes the launch of new digital credit cards, AI-powered chatbots, and digital lending platforms. These innovations are key components of the bank's strategy to enhance its market share and maintain its strong financial performance.

Digital Transformation Investments

In 2024, HDFC Bank invested approximately ₹1,000 crores in technology and digital initiatives. This investment underscores the bank's commitment to staying ahead in the digital space. The bank's total investment in technology and digital initiatives was about ₹3,500 crores in FY 2022-2023.

PIXEL Credit Cards

HDFC Bank launched PIXEL, a new range of fully digital credit cards in May 2024. These cards cater to digital-native customers and offer customization options. This initiative is part of the bank's customer acquisition strategies.

AI-Powered Chatbot

The AI-powered chatbot launched in 2023 reduced customer query response times by 40%. This improvement highlights the bank's focus on customer service. This technology enhances HDFC Bank's customer acquisition strategies.

Fintech Partnerships

Partnerships with fintech companies led to the creation of new digital lending platforms. These platforms contributed to a 30% increase in loan disbursements. This demonstrates the bank's ability to adapt and integrate new technologies effectively.

Core System Overhaul

In July 2024, HDFC Bank completed a core system overhaul to improve efficiency. This overhaul routed UPI and small-ticket transactions through peripheral servers. This eliminated previous outages and improved system reliability.

Innovation Programs

Programs like Digital Factory, Enterprise Factory, and Enterprise IT drive innovation within the bank. HDFC Tech Innovators 2024 engages with startups across sectors. This fosters a collaborative ecosystem for innovation and supports HDFC Bank's future growth opportunities.

Key Technological Initiatives

HDFC Bank's technological initiatives are designed to enhance customer experience and drive operational efficiency. These initiatives contribute to the bank's competitive advantages and support its overall HDFC Bank Growth Strategy.

- Digital Credit Cards: Launch of PIXEL credit cards tailored for digital-native customers.

- AI-Powered Chatbot: Reduced customer query response times, improving customer service.

- Fintech Partnerships: Development of digital lending platforms, boosting loan disbursements.

- Core System Overhaul: Improved system reliability and efficiency for transactions.

- Innovation Programs: Digital Factory, Enterprise Factory, and Enterprise IT to foster innovation.

The bank's focus on technology and innovation is a key component of its overall strategy. For more insights into the financial aspects, you can explore the information on Owners & Shareholders of HDFC Bank. These initiatives are crucial for maintaining the bank's market share and navigating the challenges and threats within the Indian banking sector.

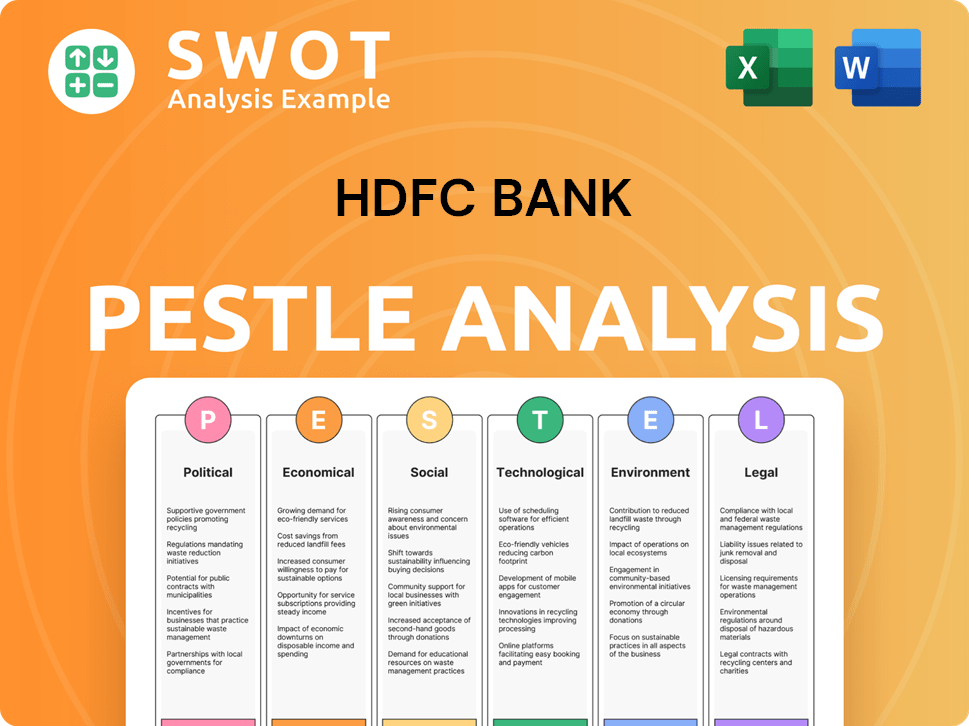

HDFC Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is HDFC Bank’s Growth Forecast?

The financial outlook for HDFC Bank appears promising, supported by robust financial performance and strategic initiatives. The bank's growth strategy focuses on expanding its market share and enhancing its digital banking initiatives. A comprehensive HDFC Bank company analysis indicates a strong position within the Indian banking sector, poised for continued expansion and profitability.

HDFC Bank's financial performance reflects its commitment to sustainable growth. The bank's focus on customer acquisition strategies and investment in technology has contributed to its strong financial results and outlook. Its expansion plans in rural areas and international expansion plans further support its growth trajectory.

The bank's strategic objectives include achieving sustainable growth in deposits, particularly in the retail segment, to improve profitability metrics. This proactive approach is designed to enhance the bank's Return on Assets (RoA) and Earnings Per Share (EPS), demonstrating its commitment to financial health and shareholder value. For more insights, consider reading about the Revenue Streams & Business Model of HDFC Bank.

For the year ended March 31, 2025, HDFC Bank reported a profit after tax of ₹673.5 billion, a 10.7% increase year-over-year. Consolidated net revenue for the same period was ₹1,683.0 billion. These figures highlight the bank's strong financial health and its ability to generate substantial revenue and profit.

In the quarter ended March 31, 2025, the standalone net profit grew by 6.7% year-on-year to ₹17,616 crore. Net interest income increased by 10.3% to ₹32,070 crore. These quarterly results indicate consistent growth and profitability for the bank.

Gross advances as of March 31, 2025, were ₹26,435 billion, a 5.4% increase over March 31, 2024. Retail loans grew by 9.0%, and commercial and rural banking loans by 12.8%. Total deposits rose by 15.8% for the nine months ended December 31, 2024, reflecting strong customer confidence.

The bank's capital adequacy ratio as of March 31, 2025, was 19.6%, well above the regulatory requirement of 11.7%. Analysts project the share price to reach ₹2,050 – ₹2,052 in 2025. The bank aims to grow its loan book at a CAGR of 15% and deposits at 18% from FY24 to FY26.

Key Growth Indicators

HDFC Bank's future growth opportunities are underpinned by several key strategies and targets. The bank's focus on sustainable banking practices and risk management strategies is crucial for long-term stability.

- Loan Book Growth: Aiming for a 15% CAGR from FY24 to FY26.

- Deposit Growth: Targeting an 18% growth rate during the same period.

- Earnings Growth: Expected to grow earnings at 18% from FY24 to FY26.

- RoA Improvement: Aiming to improve RoA to approximately 1.8% by FY26 from 1.6% in FY24.

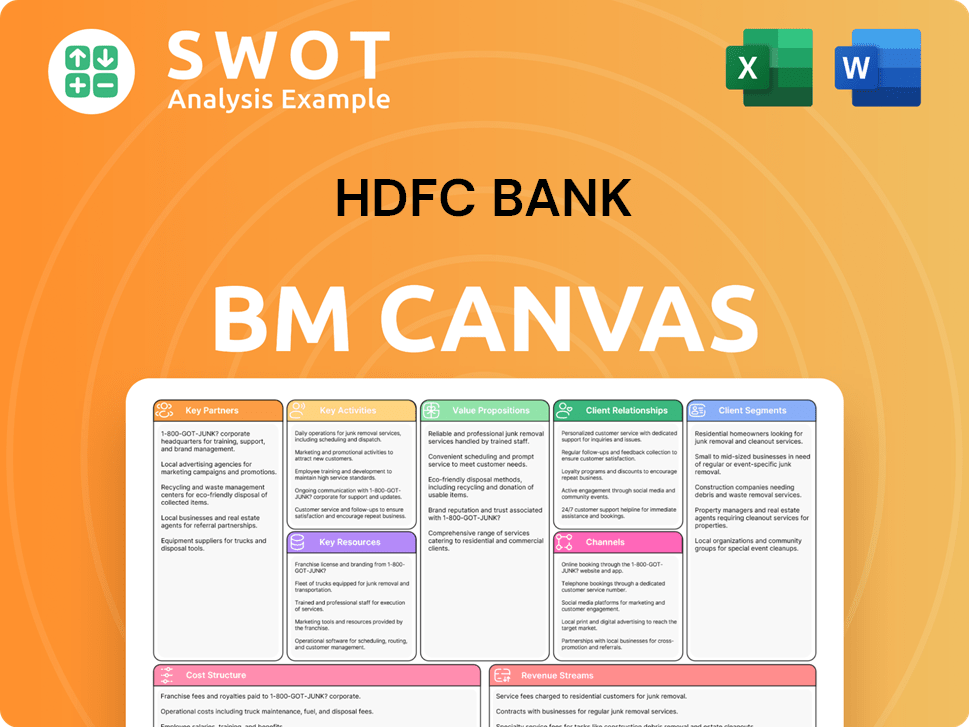

HDFC Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow HDFC Bank’s Growth?

The HDFC Bank Growth Strategy faces several potential risks and obstacles that could impact its HDFC Bank Future Prospects. These challenges range from intense market competition to the complexities of integrating major acquisitions. Understanding these risks is crucial for a comprehensive HDFC Bank Company Analysis.

The Indian banking sector is dynamic, and HDFC Bank must navigate various hurdles to maintain its strong position. Economic volatility and regulatory changes add layers of complexity to their operational environment. Furthermore, the bank's financial health is constantly scrutinized, making effective risk management and strategic planning essential.

Market competition is a significant challenge for HDFC Bank. Rivals such as ICICI Bank employ aggressive marketing strategies, intensifying the competition. The increasing presence of fintech startups, non-banking financial companies (NBFCs), and digital banks in the Indian financial sector further complicates the landscape. This competition directly affects HDFC Bank Market Share and the ability to attract and retain customers.

Regulatory Challenges

Stricter guidelines from the Reserve Bank of India (RBI) could lead to operational challenges and increased compliance costs. In 2020, the RBI restricted HDFC Bank's digital offerings and froze new credit card issuances for eight months due to technology outages. As of December 2024, KPMG anticipates that regulators will continue to focus on resilience, particularly in capital and liquidity management, scenario testing, and recovery planning, and will have heightened expectations for risk management frameworks in 2025.

Economic Volatility

Economic volatility, both global and domestic, can dampen growth prospects. This can affect consumer spending, loan demand, and increase default rates. Fluctuations in the economy directly influence HDFC Bank Financial Performance.

Asset Quality Concerns

Asset quality concerns, such as an increase in non-performing assets (NPAs) due to economic slowdowns in key sectors, also remain a risk. While HDFC Bank's asset quality remains strong, its Gross Non-Performing Assets (GNPA) stood at 1.33% in March 2025. This requires proactive risk management strategies.

Integration Risks

The integration of HDFC Ltd. into HDFC Bank, while transformational, carries execution risks, including aligning operations and managing potential short-term disruptions to profitability. The bank is actively working to improve its Loan-to-Deposit Ratio (LDR) to pre-merger levels, which was a key agenda for FY25.

Risk Management Framework

HDFC Bank has implemented a robust risk management framework, including ESG-based risk assessment for wholesale banking loans exceeding ₹100 crore, to mitigate potential environmental and social risks. The bank also conducts regular stress tests and scenario analyses to identify and prepare for potential risks. Further insights can be found in the Brief History of HDFC Bank.

Digital Banking Initiatives

Continuous investment and innovation are essential to stay competitive. The success of HDFC Bank's digital banking initiatives relies on robust cybersecurity measures and seamless user experiences. The bank must adapt to evolving customer expectations and technological advancements to maintain its position.

The bank faces the challenge of managing and mitigating these risks effectively. Economic fluctuations, regulatory changes, and competitive pressures require proactive strategies. The ability to adapt to these challenges will be crucial for sustaining growth.

Effective risk management is critical for navigating these challenges. This includes stress testing, scenario analysis, and robust compliance frameworks. By focusing on these strategies, HDFC Bank can enhance its resilience and ensure long-term sustainability.

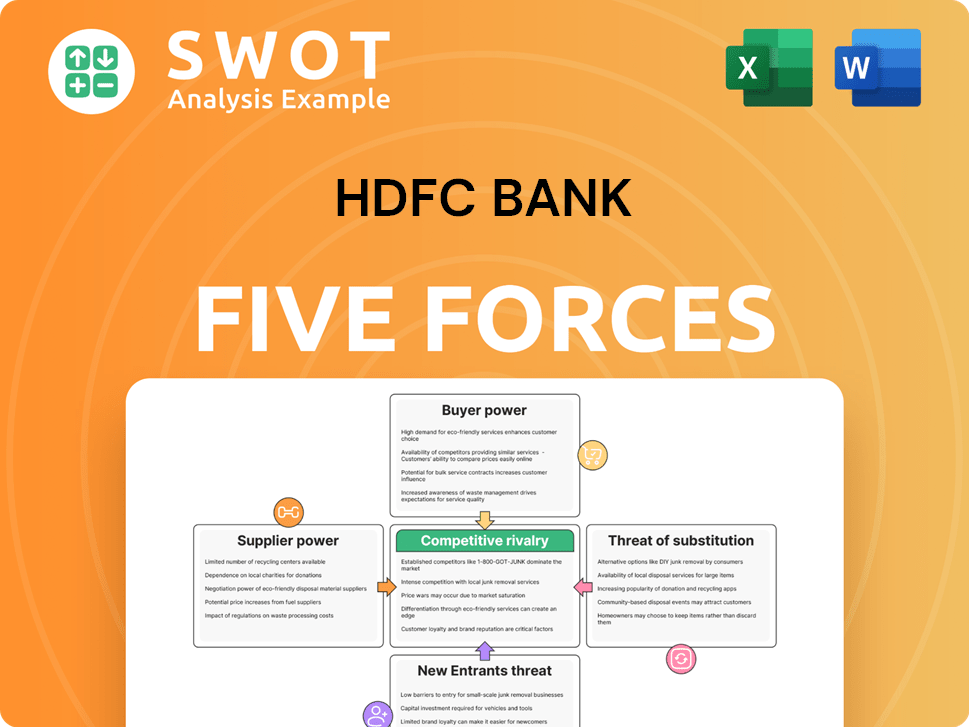

HDFC Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of HDFC Bank Company?

- What is Competitive Landscape of HDFC Bank Company?

- How Does HDFC Bank Company Work?

- What is Sales and Marketing Strategy of HDFC Bank Company?

- What is Brief History of HDFC Bank Company?

- Who Owns HDFC Bank Company?

- What is Customer Demographics and Target Market of HDFC Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.